National Register of Historic Places Inventory -- Nomination Form

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Wabash—The Gould Downfall

THE WABASH—THE GOULD DOWNFALL THOMAS C. CAMPBELL, JR.1 Wabash- Pittsburgh Terminal Railway, known to THEmany people of Western Pennsylvania as the old Wabash Railroad, was constructed in the period from 1901 to 1904 by George Gould, the son of Jay Gould. This was not the first of the Gould railway ventures, nor the greatest finan- cially, but none of the others received more publicity. In1867, Jay Gould along with "Jim" Fisk and Daniel Drew decided to obtain control of the Erie Railroad through pur- chasing a majority of the outstanding stock. Commodore Cornelius Vanderbilt of the New York Central was at that same time planning to control the Erie as it was one of the New York Central's greatest competitors. Gould, Fisk, and Drew were directors of the Erie, and the Commodore de- sired to relieve them of their duties after purchasing a ma- jority of the Erie stock. He ordered his brokers to: "Buy the Erie. Buy it at the lowest figure you can, but buy it." The brokers in carrying out the orders discovered that they had bought more Erie stock than was legally in existence. After carefully examining the newly purchased stock, some of it appeared to have been printed on new paper with the ink hardly dry. The three Erie directors had been printing illegal issues of stock to sell to the brokers. Fisk's response was : "Give us enough rag paper, and we'll hammer the ever- lasting tar out of the mariner from Staten Island." Drew, in speaking of the incident, said: "It was goodnight for the Commodore, because there is no limit to blank shares a print- ing press can turn out. -

Riding the Rails Quiz

Riding the Rails The advanced industrial development of the United States and much of the white settlement of the Western portion of the country coincided with, and was spurred by, the invention and spread of the railroad in the 19th century. How much do you know about this history? 1. Pick the year when the most miles of railroad tracks were in service in the United States: 1896 1916 1946 1996 2. The immediate trigger of the Financial Panic of 1873 occurred when: The Northern Pacific Railroad, spurred by the grant of millions of acres of federal land, built financially unsustainable lines into these nearly uninhabited territories, finally causing its stock to fall and the finance house that was its agent to go bankrupt. The thousands of immigrant workers who had been employed by the Union Pacific and the Central Pacific Railroads to lay the first transcontinental line finished the job in 1869 and were laid off and suddenly entered the labor pool, driving down wages in many industries. A long strike by railroad workers on the Baltimore & Ohio Railroad spread nationwide and paralyzed the movement of freight, causing business activity around the country to stall. Financiers Jay Gould, James Fisk, and Daniel Drew manipulated the stock price of the Erie Railroad in order to gain complete control over the company from Cornelius Vanderbilt. 3. If you boarded a passenger train in 1870, with which of the following items of safety equipment was it likely equipped? Automatic air brakes Automatic coupling mechanisms to join and separate the car Steam heating in the passenger cars None of the above 4. -

Daniel Drew and the Saratoga & Hudson River

MADE AVAILABLE BY THE GREENE COUNTY HISTORICAL SOCIETY'S VEDDER RESEARCH LIBRARY A PUBLICATION OF THE GREENE COUNTY HISTORICAL SOCIETY, INC. 90 County Route 42 Volume 36 Numbers 1+2 Coxsackie, N. Y. 12051 ISBN 0894-8135 Spring & Summer 2012 UNCLE DANIEL'S WHITE ELEPHANT: DANIEL DREW AND THE SARATOGA & HUDSON RIVER RAILROAD BY DANIEL W. BIGLER Daniel Drew, shown here in an engraving from the Library of Congress, represented the American romantic ideal of the self-made man, rising from humble beginnings to a position of great wealth and power. He worked in a number of fields over the years, ranging from cattle-driving to the stock market to steamboats and railroads. Over the years Drew frequently found himself involved with Cornelius Vanderbilt, and in 1864 a joint railroad venture between them would bring Drew to the town of Athens in Greene County. This venture, officially known as the Saratoga & Hudson River Railroad, would become known colloquially as the "White Elephant Railroad." Drew was a prime example of the larger-than-life Romantic hero (or anti-hero), who would do whatever was necessary to get ahead, while the "White Elephant" represented the grand dreams of one particular community. Its dramatic end served as a fitting symbol of the end of its era. continued on page 02 DOUBLE EDITION: SPRING & SUMMER 2012 TOGETHER! VEDDER RESEARCH LIBRARY 90 COUNTY ROUTE 42, COXSACKIE, NY 12051 MADE AVAILABLE BY THE GREENE COUNTY HISTORICAL SOCIETY'S VEDDER RESEARCH LIBRARY UNCLE DANIEL'S WHITE ELEPHANT ... from page 01 FROM BOY TO MAN the Sixty-First New York State Militia Daniel Drew was born on a farm in Carmel, Regiment. -

Hudson River Railroad

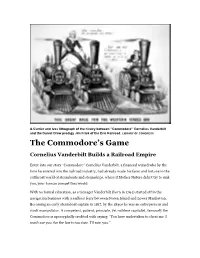

A Currier and Ives lithograph of the rivalry between “Commodore” Cornelius Vanderbilt and the Daniel Drew prodigy Jim Frisk of the Erie Railroad. LIBRARY OF CONGRESS The Commodore’s Game Cornelius Vanderbilt Builds a Railroad Empire Enter into our story “Commodore” Cornelius Vanderbilt, a financial wizard who by the time he entered into the railroad industry, had already made his fame and fortune in the cutthroat world of steamboats and steamships, where if Mother Nature didn’t try to sink you, your human competitors would. With no formal education, as a teenager Vanderbilt (born in 1794) started off in the navigation business with a sailboat ferry between Staten Island and Lower Manhattan. Becoming an early steamboat captain in 1817, by the 1830s he was an entrepreneur and stock manipulator. A competent, patient, principle, yet ruthless capitalist, famously the Commodore is apocryphally credited with saying: “You have undertaken to cheat me. I won't sue you, for the law is too slow. I'll ruin you.” The nickname “Commodore” came from Vanderbilt’s battles with the Hudson River steamboat monopolies, his eventual dominance of steam navigation in the Long Island Sound, ownership of the Staten Island Ferry, transport of California Gold Rush passengers through Central America, and a dalliance with trans-Atlantic steamship service. Once a common nickname for steamboat line owners – the name coming from the US Navy rank for a senior captain commanding a flotilla – the moniker became synonymous with Vanderbilt. During the American Civil War, the steamship tycoon donated his large and fast 331-foot long and 3,360 tons displacement SS Vanderbilt to the Union Navy, becoming the cruiser USS Vanderbilt. -

Daniel Drew Years: July 29, 1797- September 18, 1879 Residence: Carmel, New York

Name: Daniel Drew Years: July 29, 1797- September 18, 1879 Residence: Carmel, New York. Brewster, New York. Manhattan, New York Brief Biography Daniel Drew was born on July 29, 1797 in Carmel, New York to Gilbert Drew and Catherine Muckelworth. As a young business man he started by buying cattle and sheep to supply butchers in New York City. To improve his profits, it was said that he would not give water to the cattle and would feed them salt. This would result in the cattle drinking a lot of water before they were weighed in and sold according to weight. After marrying Roxana Mead and having a son, Drew invested his earnings in a steamboat fleet. By 1844, Drew was no longer selling livestock or taking part in the steamboat industry. Instead, Drew began to focus on the financial industry. He opened his own Wall Street banking and brokerage firm. There he paid special attention to railroad stocks. He was able to earn a fortune by manipulating stocks of the Erie Railroad in 1857. In 1866, Drew, James Fisk, and Jay Gould wreaked havoc on the stock market. They issued fraudulent stock to the public which led to the demand for regulation of railroads and securities. After Fisk and Gould took a major hit from a failed attempt to take advantage of the gold market, they drove down the value of Drew’s Erie stock. Drew lost millions and had to declare bankruptcy in 1876. He was estimated to be worth less than $500 when he died. Major Achievements Drew Made established himself in the business world by selling livestock and taking part in the steamboat industry. -

Cornelius Vanderbilt 1794-1877

CORNELIUS VANDERBILT 1794-1877 “Law? What do I care about the law? Hain’t I got the power?” That was the way Cornelius Vanderbilt defied the government and the public to make his millions. Born in New York, he had started as a Staten Island ferry boy when still quite young. He was quite illiterate but his Herculean strength, his dexterity, courage, and shiftiness made him a master of river and coastal sailing vessels in five years. He started his business career at the age of sixteen when he borrowed $100 from his mother to buy a shaky old boat, and in five years he owned a sizable number of ships, had repaid his mother and saved $1000. He possessed a wharf rat’s tongue and a rough wit. He took joy in combat. All his life he loved a fight. Opposition was a tonic to him. When there wasn’t any competition, he set out to create some. When his keen eye detected a line making a large profit, he would swoop down and “drive it to the wall” by offering better service at lower rates. When the opposition was driven out, he would raise rates without pity for his clients’ misery. During the War of 1812 the British fleet moved into New York harbor and menaced the people and the shipping. The American commissary general called for bids to transport supplies to the military posts around the harbor. Cornelius bid for the job and got it. He quickly gained a reputation for daring and reliability. No voyage stumped him. -

Large Investors, Price Manipulation, and Limits to Arbitrage: an Anatomy of Market Corners

Large Investors, Price Manipulation, and Limits to Arbitrage: An Anatomy of Market Corners Franklin Allen*, Lubomir Litov**, and Jianping Mei*** Draft of 1/14/2006 Abstract Corners were prevalent in the nineteenth and early twentieth century. We first develop a rational expectations model of corners and show that they can arise as the result of rational behavior. Then using a novel hand-collected data set we investigate price and trading behavior around several well-known stock market and commodity corners which occurred between 1863 and 1980. We find strong evidence that large investors and corporate insiders possess market power that allowed them to manipulate prices. Manipulation leading to a market corner tends to increase market volatility and has an adverse price impact on other assets. We also find that the presence of large investors makes it risky for would-be short sellers to trade against the mispricing. Therefore, regulators and exchanges need to be concerned about ensuring that corners do not take place since they are accompanied by severe price distortions. JEL Classification: G14, G18, K22. Keywords: Manipulation; Market Corner; Limits to Arbitrage. * Nippon Life Professor of Finance and Professor of Economics, Department of Finance, The Wharton School of the University of Pennsylvania, Philadelphia, PA 19104-6367, phone 215-898-3629, fax: 215-573- 2207, email: [email protected]. ** Assistant Professor of Finance, Olin School of Business, Washington University in St. Louis, phone: 314- 935-5740, fax: 314-935-6359, email: [email protected]. *** Associate Professor of Finance, Leonard Stern School of Business, New York University, New York NY 10012 and CCFR, phone: 212-998-0354, email: [email protected]. -

When Cornelius Vanderbilt Died in 1877, He Left an Estate

Cornelius Vanderbilt Born May 27, 1794 (Port Richmond, New York) Died January 4, 1877 (New York, New York) Shipping executive Railroad executive Financier ‘‘I for one will never go to a hen Cornelius Vanderbilt died in 1877, he left an estate court of law when I have W valued at $100 million. Vanderbilt’s astonishing fortune the power in my own ranked him as the richest American in his lifetime, and his wealth had seemed to grow right along with the rapidly expanding new hands to see myself right.’’ nation. Known as the ‘‘Commodore,’’ he made his first fortune in shippingandwentontoownalargesectionoftherailroadtracks that connected the East Coast to Chicago, Illinois. Vanderbilt had a skill for recognizing coming changes and trends, and his talent for investment opportunities made him one of the American Industrial Revolution’s leading figures. His estate also created one of the country’s great family fortunes. An early start in the shipping business Born in May 1794 on Staten Island, New York, Vanderbilt came from a Dutch farming family who lived in Port Richmond, on the north shore of the island. His great-great-great-grand- father, Jan Aertson, came to New York in 1650 as an indentured servant, a common form of contract labor in the era and a way for poor men and women to try their luck in the New World. In exchange for promising their labor for a number of years, the 234 Cornelius Vanderbilt. (ª Bettmann/Corbis.) indentured servant was provided with transportation to North America and food and shelter during his work years. -

Large Investors, Price Manipulation, and Limits to Arbitrage: an Anatomy of Market Corners

Large Investors, Price Manipulation, and Limits to Arbitrage: An Anatomy of Market Corners Franklin Allen*, Lubomir Litov**, and JianPing Mei*** Draft of 11/3/2004 Abstract Using a hand-collected new data set, this paper investigates price and trading behavior around several well-known stock market corners occurred between 1863 and 1980. We find strong evidence that large investors possessed market power that allowed them to manipulate prices. Manipulation leading to a corner tends to increase market volatility and has an adverse price impact on other assets. We also find that the presence of large investors makes it extremely risky for would-be short sellers to trade against the mispricing. Therefore, regulators need to be concerned about corners since they are accompanied by severe price distortions and liquidity erosion. JEL Classification: G14, G18, K22. Keywords: Manipulation; Market Corner; Limits to Arbitrage. * Nippon Life Professor of Finance and Professor of Economics, Department of Finance, The Wharton School of the University of Pennsylvania, Philadelphia, PA 19104-6367, phone 215-898-3629, fax: 215-573-2207, email: [email protected]. ** Doctoral student, Leonard Stern School of Business, New York University, New York 10012, phone: 212-998- 0883, fax: 212-995-4218, email: [email protected]. *** Associate Professor of Finance, Leonard Stern School of Business, New York University, New York NY 10012 and CCFR, phone: 212-998-0354, email: [email protected]. We are grateful to Niall Ferguson, William Goetzmann, Richard Sylla, Jeffrey Wurgler, and conference participants at the CEPR Conference on Early Securities Markets at the Humboldt University for valuable discussions. -

Fifty Years in Wall Street

ffirs.qxd 12/9/05 11:33 AM Page iii FIFTY YEARS IN WALL STREET HENRY CLEWS Foreword by Victor Niederhoffer JOHN WILEY & SONS, INC. ffirs.qxd 12/9/05 11:33 AM Page i FIFTY YEARS IN WALL STREET ffirs.qxd 12/9/05 11:33 AM Page ii INTRODUCING WILEY INVESTMENT CLASSICS There are certain books that have redefined the way we see the worlds of finance and investing—books that deserve a place on every investor’s shelf. Wiley Investment Classics will introduce you to these memorable books, which are just as relevant and vital today as when they were first published. Open a Wiley Investment Classic and rediscover the proven strategies, market philosophies, and definitive techniques that continue to stand the test of time. ffirs.qxd 12/9/05 11:33 AM Page iii FIFTY YEARS IN WALL STREET HENRY CLEWS Foreword by Victor Niederhoffer JOHN WILEY & SONS, INC. ffirs.qxd 12/9/05 11:33 AM Page iv Foreword © 2006 by Victor Niederhoffer. All rights reserved. Published by John Wiley & Sons, Inc., Hoboken, New Jersey. Published simultaneously in Canada. Full version originally published in 1908 by Irving Publishing Company. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except as permitted under Section 107 or 108 of the 1976 United States Copyright Act, without either the prior written permission of the Publisher, or authorization through payment of the appropriate per-copy fee to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, (978) 750-8400, fax (978) 750-4470, or on the web at www.copyright.com. -

Wall Street's Gilded Age: Nicknames Ofher Capitalists and Robber Barons

Wall Street's Gilded Age: Nicknames of Her Capitalists and Robber Barons Richard A. Sauers Lenape Investnzent Corporation The "Gilded Age," loosely defined here as 1861 to 1901, saw the emergence of a small group of men who played a leading role in the Industrial Revolution. Aptly described as both capitalist and robber baron, they were responsible for much of the economic framework that exists today. Through the takeover battle for control of the Erie Railroad Company, at the beginning of the period, and the organization of United States Steel Corporation, at its end, this essay examines historical and contemporary biographical information to explain that the nicknames of seven men involved in these two entities predominantly reflected not only their activities in the stock market, but also their occupations and character traits. The New York Stock Exchange, symbol of America's financial strength, traces its origins to an agreement among twenty-four Wall Streee brokers gathered in the shade of a sycamore tree on a spring day in 1792 (Buck 1992). The "Buttonwood Agreement," as it became known, established the trading of stocks among themselves on a common commission basis: "We the Subscribers, Brokers for the Purchase and Sale of Public Stock, do hereby solemnly promise and pledge ourselves to each other, that we will not buy or sell from this day for any person whatsoever, any kind of Public Stock at less rate than one-quarter percent Commission on the Specie value of, and that we will give a preference to each other in our Negotiations. In Testimony, whereof, we have set our hands on this seventeenth day of May at New York, 1792." Names 54:2 Oune 2006): 147-172 ISSN:0027-7738 Copyright 2006 by The American Name Society 147 148 • NAMES 54:2 (June 2006) This simple covenant was instrumental in the development of the stock market, formally organized as the New York Exchange and Stock Board in 1817, becoming the New York Stock Exchange in 1863.