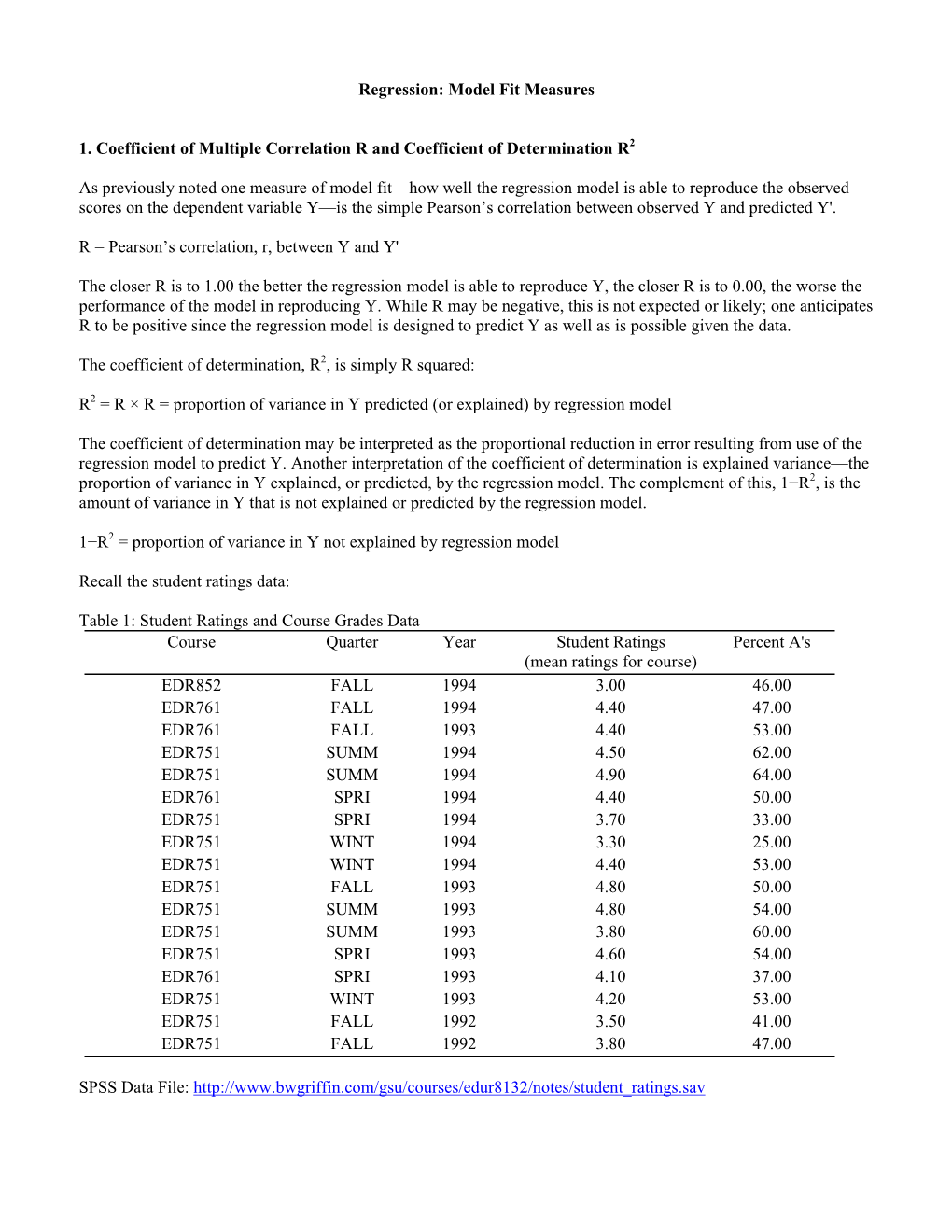

Regression: Model Fit Measures

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Applied Biostatistics Mean and Standard Deviation the Mean the Median Is Not the Only Measure of Central Value for a Distribution

Health Sciences M.Sc. Programme Applied Biostatistics Mean and Standard Deviation The mean The median is not the only measure of central value for a distribution. Another is the arithmetic mean or average, usually referred to simply as the mean. This is found by taking the sum of the observations and dividing by their number. The mean is often denoted by a little bar over the symbol for the variable, e.g. x . The sample mean has much nicer mathematical properties than the median and is thus more useful for the comparison methods described later. The median is a very useful descriptive statistic, but not much used for other purposes. Median, mean and skewness The sum of the 57 FEV1s is 231.51 and hence the mean is 231.51/57 = 4.06. This is very close to the median, 4.1, so the median is within 1% of the mean. This is not so for the triglyceride data. The median triglyceride is 0.46 but the mean is 0.51, which is higher. The median is 10% away from the mean. If the distribution is symmetrical the sample mean and median will be about the same, but in a skew distribution they will not. If the distribution is skew to the right, as for serum triglyceride, the mean will be greater, if it is skew to the left the median will be greater. This is because the values in the tails affect the mean but not the median. Figure 1 shows the positions of the mean and median on the histogram of triglyceride. -

Lecture 13: Simple Linear Regression in Matrix Format

11:55 Wednesday 14th October, 2015 See updates and corrections at http://www.stat.cmu.edu/~cshalizi/mreg/ Lecture 13: Simple Linear Regression in Matrix Format 36-401, Section B, Fall 2015 13 October 2015 Contents 1 Least Squares in Matrix Form 2 1.1 The Basic Matrices . .2 1.2 Mean Squared Error . .3 1.3 Minimizing the MSE . .4 2 Fitted Values and Residuals 5 2.1 Residuals . .7 2.2 Expectations and Covariances . .7 3 Sampling Distribution of Estimators 8 4 Derivatives with Respect to Vectors 9 4.1 Second Derivatives . 11 4.2 Maxima and Minima . 11 5 Expectations and Variances with Vectors and Matrices 12 6 Further Reading 13 1 2 So far, we have not used any notions, or notation, that goes beyond basic algebra and calculus (and probability). This has forced us to do a fair amount of book-keeping, as it were by hand. This is just about tolerable for the simple linear model, with one predictor variable. It will get intolerable if we have multiple predictor variables. Fortunately, a little application of linear algebra will let us abstract away from a lot of the book-keeping details, and make multiple linear regression hardly more complicated than the simple version1. These notes will not remind you of how matrix algebra works. However, they will review some results about calculus with matrices, and about expectations and variances with vectors and matrices. Throughout, bold-faced letters will denote matrices, as a as opposed to a scalar a. 1 Least Squares in Matrix Form Our data consists of n paired observations of the predictor variable X and the response variable Y , i.e., (x1; y1);::: (xn; yn). -

In This Segment, We Discuss a Little More the Mean Squared Error

MITOCW | MITRES6_012S18_L20-04_300k In this segment, we discuss a little more the mean squared error. Consider some estimator. It can be any estimator, not just the sample mean. We can decompose the mean squared error as a sum of two terms. Where does this formula come from? Well, we know that for any random variable Z, this formula is valid. And if we let Z be equal to the difference between the estimator and the value that we're trying to estimate, then we obtain this formula here. The expected value of our random variable Z squared is equal to the variance of that random variable plus the square of its mean. Let us now rewrite these two terms in a more suggestive way. We first notice that theta is a constant. When you add or subtract the constant from a random variable, the variance does not change. So this term is the same as the variance of theta hat. This quantity here, we will call it the bias of the estimator. It tells us whether theta hat is systematically above or below than the unknown parameter theta that we're trying to estimate. And using this terminology, this term here is just equal to the square of the bias. So the mean squared error consists of two components, and these capture different aspects of an estimator's performance. Let us see what they are in a concrete setting. Suppose that we're estimating the unknown mean of some distribution, and that our estimator is the sample mean. In this case, the mean squared error is the variance, which we know to be sigma squared over n, plus the bias term. -

Minimum Mean Squared Error Model Averaging in Likelihood Models

Statistica Sinica 26 (2016), 809-840 doi:http://dx.doi.org/10.5705/ss.202014.0067 MINIMUM MEAN SQUARED ERROR MODEL AVERAGING IN LIKELIHOOD MODELS Ali Charkhi1, Gerda Claeskens1 and Bruce E. Hansen2 1KU Leuven and 2University of Wisconsin, Madison Abstract: A data-driven method for frequentist model averaging weight choice is developed for general likelihood models. We propose to estimate the weights which minimize an estimator of the mean squared error of a weighted estimator in a local misspecification framework. We find that in general there is not a unique set of such weights, meaning that predictions from multiple model averaging estimators might not be identical. This holds in both the univariate and multivariate case. However, we show that a unique set of empirical weights is obtained if the candidate models are appropriately restricted. In particular a suitable class of models are the so-called singleton models where each model only includes one parameter from the candidate set. This restriction results in a drastic reduction in the computational cost of model averaging weight selection relative to methods which include weights for all possible parameter subsets. We investigate the performance of our methods in both linear models and generalized linear models, and illustrate the methods in two empirical applications. Key words and phrases: Frequentist model averaging, likelihood regression, local misspecification, mean squared error, weight choice. 1. Introduction We study a focused version of frequentist model averaging where the mean squared error plays a central role. Suppose we have a collection of models S 2 S to estimate a population quantity µ, this is the focus, leading to a set of estimators fµ^S : S 2 Sg. -

Calibration: Calibrate Your Model

DUE TODAYCOMPUTER FILES AND QUESTIONS for Assgn#6 Assignment # 6 Steady State Model Calibration: Calibrate your model. If you want to conduct a transient calibration, talk with me first. Perform calibration using UCODE. Be sure your report addresses global, graphical, and spatial measures of error as well as common sense. Consider more than one conceptual model and compare the results. Remember to make a prediction with your calibrated models and evaluate confidence in your prediction. Be sure to save your files because you will want to use them later in the semester. Suggested Calibration Report Outline Title Introduction describe the system to be calibrated (use portions of your previous report as appropriate) Observations to be matched in calibration type of observations locations of observations observed values uncertainty associated with observations explain specifically what the observation will be matched to in the model Calibration Procedure Evaluation of calibration residuals parameter values quality of calibrated model Calibrated model results Predictions Uncertainty associated with predictions Problems encountered, if any Comparison with uncalibrated model results Assessment of future work needed, if appropriate Summary/Conclusions Summary/Conclusions References submit the paper as hard copy and include it in your zip file of model input and output submit the model files (input and output for both simulations) in a zip file labeled: ASSGN6_LASTNAME.ZIP Calibration (Parameter Estimation, Optimization, Inversion, Regression) adjusting parameter values, boundary conditions, model conceptualization, and/or model construction until the model simulation matches field observations We calibrate because 1. the field measurements are not accurate reflecti ons of the model scale properties, and 2. -

Bayes Estimator Recap - Example

Recap Bayes Risk Consistency Summary Recap Bayes Risk Consistency Summary . Last Lecture . Biostatistics 602 - Statistical Inference Lecture 16 • What is a Bayes Estimator? Evaluation of Bayes Estimator • Is a Bayes Estimator the best unbiased estimator? . • Compared to other estimators, what are advantages of Bayes Estimator? Hyun Min Kang • What is conjugate family? • What are the conjugate families of Binomial, Poisson, and Normal distribution? March 14th, 2013 Hyun Min Kang Biostatistics 602 - Lecture 16 March 14th, 2013 1 / 28 Hyun Min Kang Biostatistics 602 - Lecture 16 March 14th, 2013 2 / 28 Recap Bayes Risk Consistency Summary Recap Bayes Risk Consistency Summary . Recap - Bayes Estimator Recap - Example • θ : parameter • π(θ) : prior distribution i.i.d. • X1, , Xn Bernoulli(p) • X θ fX(x θ) : sampling distribution ··· ∼ | ∼ | • π(p) Beta(α, β) • Posterior distribution of θ x ∼ | • α Prior guess : pˆ = α+β . Joint fX(x θ)π(θ) π(θ x) = = | • Posterior distribution : π(p x) Beta( xi + α, n xi + β) | Marginal m(x) | ∼ − • Bayes estimator ∑ ∑ m(x) = f(x θ)π(θ)dθ (Bayes’ rule) | α + x x n α α + β ∫ pˆ = i = i + α + β + n n α + β + n α + β α + β + n • Bayes Estimator of θ is ∑ ∑ E(θ x) = θπ(θ x)dθ | θ Ω | ∫ ∈ Hyun Min Kang Biostatistics 602 - Lecture 16 March 14th, 2013 3 / 28 Hyun Min Kang Biostatistics 602 - Lecture 16 March 14th, 2013 4 / 28 Recap Bayes Risk Consistency Summary Recap Bayes Risk Consistency Summary . Loss Function Optimality Loss Function Let L(θ, θˆ) be a function of θ and θˆ. -

Random Variables and Applications

Random Variables and Applications OPRE 6301 Random Variables. As noted earlier, variability is omnipresent in the busi- ness world. To model variability probabilistically, we need the concept of a random variable. A random variable is a numerically valued variable which takes on different values with given probabilities. Examples: The return on an investment in a one-year period The price of an equity The number of customers entering a store The sales volume of a store on a particular day The turnover rate at your organization next year 1 Types of Random Variables. Discrete Random Variable: — one that takes on a countable number of possible values, e.g., total of roll of two dice: 2, 3, ..., 12 • number of desktops sold: 0, 1, ... • customer count: 0, 1, ... • Continuous Random Variable: — one that takes on an uncountable number of possible values, e.g., interest rate: 3.25%, 6.125%, ... • task completion time: a nonnegative value • price of a stock: a nonnegative value • Basic Concept: Integer or rational numbers are discrete, while real numbers are continuous. 2 Probability Distributions. “Randomness” of a random variable is described by a probability distribution. Informally, the probability distribution specifies the probability or likelihood for a random variable to assume a particular value. Formally, let X be a random variable and let x be a possible value of X. Then, we have two cases. Discrete: the probability mass function of X specifies P (x) P (X = x) for all possible values of x. ≡ Continuous: the probability density function of X is a function f(x) that is such that f(x) h P (x < · ≈ X x + h) for small positive h. -

Calculating Variance and Standard Deviation

VARIANCE AND STANDARD DEVIATION Recall that the range is the difference between the upper and lower limits of the data. While this is important, it does have one major disadvantage. It does not describe the variation among the variables. For instance, both of these sets of data have the same range, yet their values are definitely different. 90, 90, 90, 98, 90 Range = 8 1, 6, 8, 1, 9, 5 Range = 8 To better describe the variation, we will introduce two other measures of variation—variance and standard deviation (the variance is the square of the standard deviation). These measures tell us how much the actual values differ from the mean. The larger the standard deviation, the more spread out the values. The smaller the standard deviation, the less spread out the values. This measure is particularly helpful to teachers as they try to find whether their students’ scores on a certain test are closely related to the class average. To find the standard deviation of a set of values: a. Find the mean of the data b. Find the difference (deviation) between each of the scores and the mean c. Square each deviation d. Sum the squares e. Dividing by one less than the number of values, find the “mean” of this sum (the variance*) f. Find the square root of the variance (the standard deviation) *Note: In some books, the variance is found by dividing by n. In statistics it is more useful to divide by n -1. EXAMPLE Find the variance and standard deviation of the following scores on an exam: 92, 95, 85, 80, 75, 50 SOLUTION First we find the mean of the data: 92+95+85+80+75+50 477 Mean = = = 79.5 6 6 Then we find the difference between each score and the mean (deviation). -

An Analysis of Random Design Linear Regression

An Analysis of Random Design Linear Regression Daniel Hsu1,2, Sham M. Kakade2, and Tong Zhang1 1Department of Statistics, Rutgers University 2Department of Statistics, Wharton School, University of Pennsylvania Abstract The random design setting for linear regression concerns estimators based on a random sam- ple of covariate/response pairs. This work gives explicit bounds on the prediction error for the ordinary least squares estimator and the ridge regression estimator under mild assumptions on the covariate/response distributions. In particular, this work provides sharp results on the \out-of-sample" prediction error, as opposed to the \in-sample" (fixed design) error. Our anal- ysis also explicitly reveals the effect of noise vs. modeling errors. The approach reveals a close connection to the more traditional fixed design setting, and our methods make use of recent ad- vances in concentration inequalities (for vectors and matrices). We also describe an application of our results to fast least squares computations. 1 Introduction In the random design setting for linear regression, one is given pairs (X1;Y1);:::; (Xn;Yn) of co- variates and responses, sampled from a population, where each Xi are random vectors and Yi 2 R. These pairs are hypothesized to have the linear relationship > Yi = Xi β + i for some linear map β, where the i are noise terms. The goal of estimation in this setting is to find coefficients β^ based on these (Xi;Yi) pairs such that the expected prediction error on a new > 2 draw (X; Y ) from the population, measured as E[(X β^ − Y ) ], is as small as possible. -

Review of Basic Statistics and the Mean Model for Forecasting

Review of basic statistics and the simplest forecasting model: the sample mean Robert Nau Fuqua School of Business, Duke University August 2014 Most of what you need to remember about basic statistics Consider a random variable called X that is a time series (a set of observations ordered in time) consisting of the following 20 observations: 114, 126, 123, 112, 68, 116, 50, 108, 163, 79, 67, 98, 131, 83, 56, 109, 81, 61, 90, 92. 180 160 140 120 100 80 60 40 20 0 0 5 10 15 20 25 How should we forecast what will happen next? The simplest forecasting model that we might consider is the mean model,1 which assumes that the time series consists of independently and identically distributed (“i.i.d.”) values, as if each observation is randomly drawn from the same population. Under this assumption, the next value should be predicted to be equal to the historical sample mean if the goal is to minimize mean squared error. This might sound trivial, but it isn’t. If you understand the details of how this works, you are halfway to understanding linear regression. (No kidding: see section 3 of the regression notes handout.) To set the stage for using the mean model for forecasting, let’s review some of the most basic concepts of statistics. Let: X = a random variable, with its individual values denoted by x1, x2, etc. N = size of the entire population of values of X (possibly infinite)2 n = size of a finite sample of X 1 This might also be called a “constant model” or an “intercept-only regression.” 2 The term “population” does not refer to the number of distinct values of X. -

4. Descriptive Statistics

4. Descriptive statistics Any time that you get a new data set to look at one of the first tasks that you have to do is find ways of summarising the data in a compact, easily understood fashion. This is what descriptive statistics (as opposed to inferential statistics) is all about. In fact, to many people the term “statistics” is synonymous with descriptive statistics. It is this topic that we’ll consider in this chapter, but before going into any details, let’s take a moment to get a sense of why we need descriptive statistics. To do this, let’s open the aflsmall_margins file and see what variables are stored in the file. In fact, there is just one variable here, afl.margins. We’ll focus a bit on this variable in this chapter, so I’d better tell you what it is. Unlike most of the data sets in this book, this is actually real data, relating to the Australian Football League (AFL).1 The afl.margins variable contains the winning margin (number of points) for all 176 home and away games played during the 2010 season. This output doesn’t make it easy to get a sense of what the data are actually saying. Just “looking at the data” isn’t a terribly effective way of understanding data. In order to get some idea about what the data are actually saying we need to calculate some descriptive statistics (this chapter) and draw some nice pictures (Chapter 5). Since the descriptive statistics are the easier of the two topics I’ll start with those, but nevertheless I’ll show you a histogram of the afl.margins data since it should help you get a sense of what the data we’re trying to describe actually look like, see Figure 4.2. -

Annex : Calculation of Mean and Standard Deviation

Annex : Calculation of Mean and Standard Deviation • A cholesterol control is run 20 times over 25 days yielding the following results in mg/dL: 192, 188, 190, 190, 189, 191, 188, 193, 188, 190, 191, 194, 194, 188, 192, 190, 189, 189, 191, 192. • Using the cholesterol control results, follow the steps described below to establish QC ranges . An example is shown on the next page. 1. Make a table with 3 columns, labeled A, B, C. 2. Insert the data points on the left (column A). 3. Add Data in column A. 4. Calculate the mean: Add the measurements (sum) and divide by the number of measurements (n). Mean= ∑ x +x +x +…. x 3809 = 190.5 mg/ dL 1 2 3 n N 20 5. Calculate the variance and standard deviation: (see formulas below) a. Subtract each data point from the mean and write in column B. b. Square each value in column B and write in column C. c. Add column C. Result is 71 mg/dL. d. Now calculate the variance: Divide the sum in column C by n-1 which is 19. Result is 4 mg/dL. e. The variance has little value in the laboratory because the units are squared. f. Now calculate the SD by taking the square root of the variance. g. The result is 2 mg/dL. Quantitative QC ● Module 7 ● Annex 1 A B C Data points. 2 xi −x (x −x) X1-Xn i 192 mg/dL 1.5 2.25 mg 2/dL 2 188 mg/dL -2.5 6.25 mg 2/dL2 190 mg/dL -0.5 0.25 mg 2/dL2 190 mg/dL -0.5 0.25 mg 2/dL2 189 mg/dL -1.5 2.25 mg 2/dL2 191 mg/dL 0.5 0.25 mg 2/dL2 188 mg/dL -2.5 6.25 mg 2/dL2 193 mg/dL 2.5 6.25 mg 2/dL2 188 mg/dL -2.5 6.25 mg 2/dL2 190 mg/dL -0.5 0.25 mg 2/dL2 191 mg/dL 0.5 0.25 mg 2/dL2 194 mg/dL 3.5 12.25 mg 2/dL2 194 mg/dL 3.5 12.25 mg 2/dL2 188 mg/dL -2.5 6.25 mg 2/dL2 192 mg/dL 1.5 2.25 mg 2/dL2 190 mg/dL -0.5 0.25 mg 2/dL2 189 mg/dL -1.5 2.25 mg 2/dL2 189 mg/dL -1.5 2.25 mg 2/dL2 191 mg/dL 0.5 0.25 mg 2/dL2 192 mg/dL 1.5 2.25 mg 2/dL2 2 2 2 ∑x=3809 ∑= -1 ∑ ( x i − x ) Sum of Col C is 71 mg /dL 2 − 2 ∑ (X i X) 2 SD = S = n−1 mg/dL SD = S = 71 19/ = 2mg / dL The square root returns the result to the original units .