The Traders Club Weekly Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Nikkei 225 Kagi Chart with MACD Applied (Charts: Tradingview)

Kagi What is it? • Created in Japan, • Been around since 1870’s. • Used to give a much more transparent picture of where the price of an individual asset was headed independent of time. • Ignores time and focus solely on price changes that meet a minimum requirement. • Great for taking the ‘noise’ out of the charts; another great ‘psychological’ helping chart! • Instead of using 'X's and O's like point and figure charts, the Kagi chart simply uses lines. These lines are known as the Yin and Yang lines. • The other fundamental concept of these charts, is that of the reversal in price. The lines change direction once the price moves a set amount. 1 Below you can see a typical example based on the S&P500 stock index (Charts: TradingView). In this example the thicker black line signifies up bullish periods (Yang line) and the thinner red line signifies bearish periods (Yin Line): 2 Also take a look at the same period on the Kagi S&P 500 chart versus the traditional candlestick chart S&P 500 chart. See how much less noise there is on the Kagi chart (Charts: TradingView): 3 Basics: • It is the study of pure price movement i.e. it doesn’t take into consideration ‘time’ when constructing its charts. • Uses simple lines known as ‘Yin’ and ‘Yang’ to measure price. • The lines change direction once the price moves a set amount. • Kagi charting is all about the price reversal. • Normally: Black (thicker) lines indicate bullish periods (Yang Line), Red (thin) lines signify bearish periods (Yin Line) • In my examples: Going Black to Red = Sell, Going Red to Black = Buy 4 Construction: • Step 1 is to calculate the reversal amount. -

Course Brochure

IFMC INSTITUTE COURSE BROCHURE IFMC BRANCHES NOIDA VAISHALI LAJPAT NORTH CAMPUS GHAZIABAD NAGAR (DELHI) (DELHI) MAAN SINGH SHOP No. - 3, RELIANCE PLAZA, E-90, COMPLEX SECTOR BACK PORTION, PLOT No. 3, FIRST 15 MAIN ROAD, VIJAY NAGAR SINGLE IInd FLOOR, 2, FLOOR, LAJPAT NEXT TO BHAGMAL STOREY NEAR NDPL NAGAR 1, COMPLEX NEAR Mc SECTOR 4, OFFICE NEW DELHI - 110024 DONALD VAISHALI, GHAZIABAD, NEW DELHI - 110009 PH: +919810216889 SECTOR 16, UTTAR PRADESH - PH: 0981060777 +91-810260089 NOIDA – 201301 201012 PH: +919810216889 PH: 9650066987 CONTENTS Technical Analysis Course ....................................................................................................................... 3 Quickest Way to Deal with Stock Market Losses ................................................................................ 3 What is Technical Analysis Course? .................................................................................................... 3 Technical Analysis Meaning: ............................................................................................................... 3 Learning Outcome: .......................................................................................................................... 4 Course Methodology: ..................................................................................................................... 4 Eligibility: ......................................................................................................................................... 5 Career Opportunity: -

Multicharts User Manual

MultiCharts User Manual Contents Charts ................................................................................................................. 10 MultiCharts Work Area ................................................................................................................................... 10 Understanding Chart Window ........................................................................................................................ 21 Creating Charts ............................................................................................................................................... 22 Volume Analysis .............................................................................................................................................. 30 Volume Profile ................................................................................................................................................ 30 Go To Specified Bar ......................................................................................................................................... 36 Chart Settings ..................................................................................................... 37 Chart Scaling ................................................................................................................................................... 37 Margins .......................................................................................................................................................... -

Trading View Tutorial

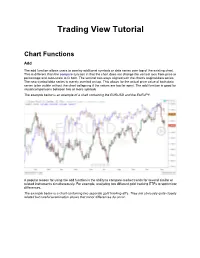

Trading View Tutorial Chart Functions Add The add function allows users to overlay additional symbols or data series over top of the existing chart. This is different than the compare function in that the chart does not change the vertical axis from price to percentage and auto-scale to fit both. The vertical axis stays aligned with the chart's original data series. The new symbol/data series is merely overlaid on top. This allows for the actual price value of both data series to be visible without the chart collapsing if the values are too far apart. The add function is good for visual comparisons between two or more symbols. The example below is an example of a chart containing the EURUSD and the EURJPY. A popular reason for using the add function is the ability to compare market trends for several similar or related instruments simultaneously. For example, analyzing two different gold tracking ETFs to spot minor differences. The example below is a chart containing two separate gold tracking etf's. They are obviously quite closely related but careful examination shows that minor differences do occur. To add a new symbol to overlay on top of the current data series/chart, simply click on the "Add" button on the toolbar along the top of the chart and type the symbol into the dialogue box and click the + sign. Another option is the "Overly the main chart" feature. If this is unchecked, the new symbol will not be overlaid on top of the original data series, it will be sent to a new panel beneath the original one. -

An Empirical Study Applying Chart Patterns to Indian Stock Market Crashes

Pacific Business Review International Volume 6, Issue 11, May 2014 An Empirical study applying Chart patterns to Indian Stock Market Crashes Varun Sarda Abstract Faculty, Acropolis Faculty of Charting techniques are used by analysts to predict the movements of prices in Management Research, Indore Financial Markets. However, most of them are based on the gradual movements of prices though the uncertain environment of today calls for an analysis of the rapid movements. This paper examines Kagi Charting Dr Yamini Karmarkar technique to analyze the Crashes of Indian stock markets based on Qualitative Reader, IIPS, DAVV, Indore parameter of Predictive Efficiency. The period of study is from 1997 to 2011. A crash is defined as a drop of 25% or above from the peak value of Sensex within a duration of 60 days from the peak. The results of the study show that Neha Lakhotia Kagi Charts are able to predict the crash with 100% predictive efficiency for Faculty, Prestige Institute of one of the three crashes analyzed in the study. Management Dewas Keywords: Stock Market, Crashes, India, Financial Markets. Introduction The analysis of securities has been done for years together with the use of charting techniques or technical analysis. Technical analysis involves making the use of recording the historical data on charts, studying these charts to find meaningful patterns and then further using the same to predict the future prices. There are different techniques which are used by professional analysts to recognize the specific pattern of the movements in order to apply it for predictive purposes. The importance lies in the identification of trends and recognition of the end of a trend and start of the movement of prices in the opposite direction. -

The Forex Chartist Companion

The Forex Chartist Companion The Forex Chartist Companion A Visual Approach to Technical Analysis MICHAEL D. ARCHER JAMES L. BICKFORD John Wiley & Sons, Inc. Copyright © 2007 by Michael D. Archer and James L. Bickford. All rights reserved. Published by John Wiley & Sons, Inc., Hoboken, New Jersey. Published simultaneously in Canada. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except as permitted under Section 107 or 108 of the 1976 United States Copyright Act, without either the prior written permission of the Publisher, or authorization through payment of the appropriate per-copy fee to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, (978) 750-8400, fax (978) 646-8600, or on the web at www.copyright.com. Requests to the Publisher for permission should be addressed to the Permissions Department, John Wiley & Sons, Inc., 111 River Street, Hoboken, NJ 07030, (201) 748-6011, fax (201) 748-6008, or online at http://www.wiley.com/go/permissions. Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best efforts in preparing this book, they make no representations or warranties with respect to the accuracy or completeness of the contents of this book and specifically disclaim any implied warranties of merchantability or fitness for a particular purpose. No warranty may be created or extended by sales representatives or written sales materials. The advice and strategies contained herein may not be suitable for your situation. You should consult with a professional where appropriate. -

Momentum 124 Momentum (Finance) 124 Relative Strength Index 125 Stochastic Oscillator 128 Williams %R 131

PATTERNS Technical Analysis Contents Articles Technical analysis 1 CONCEPTS 11 Support and resistance 11 Trend line (technical analysis) 15 Breakout (technical analysis) 16 Market trend 16 Dead cat bounce 21 Elliott wave principle 22 Fibonacci retracement 29 Pivot point 31 Dow Theory 34 CHARTS 37 Candlestick chart 37 Open-high-low-close chart 39 Line chart 40 Point and figure chart 42 Kagi chart 45 PATTERNS: Chart Pattern 47 Chart pattern 47 Head and shoulders (chart pattern) 48 Cup and handle 50 Double top and double bottom 51 Triple top and triple bottom 52 Broadening top 54 Price channels 55 Wedge pattern 56 Triangle (chart pattern) 58 Flag and pennant patterns 60 The Island Reversal 63 Gap (chart pattern) 64 PATTERNS: Candlestick pattern 68 Candlestick pattern 68 Doji 89 Hammer (candlestick pattern) 92 Hanging man (candlestick pattern) 93 Inverted hammer 94 Shooting star (candlestick pattern) 94 Marubozu 95 Spinning top (candlestick pattern) 96 Three white soldiers 97 Three Black Crows 98 Morning star (candlestick pattern) 99 Hikkake Pattern 100 INDICATORS: Trend 102 Average Directional Index 102 Ichimoku Kinkō Hyō 103 MACD 104 Mass index 108 Moving average 109 Parabolic SAR 115 Trix (technical analysis) 116 Vortex Indicator 118 Know Sure Thing (KST) Oscillator 121 INDICATORS: Momentum 124 Momentum (finance) 124 Relative Strength Index 125 Stochastic oscillator 128 Williams %R 131 INDICATORS: Volume 132 Volume (finance) 132 Accumulation/distribution index 133 Money Flow Index 134 On-balance volume 135 Volume Price Trend 136 Force -

Lesson 4 Chart Analysis – Bar-Building Techniqueslesson and Chart Styles 4

Lesson 4 Chart Analysis – Bar-Building TechniquesLesson and Chart Styles 4 Chart Analysis – Bar-Building Techniques and Chart Styles Table of Contents Chart Analysis Windows……………………............ 1 Requesting Data Using the Download Scheduler…… 7 Formatting the Symbol in a Chart………………….. 2 Changing the Style of a Symbol………………………. 8 Changing Symbol, Bar Interval and Range……….. 2 Formatting the Price Scale…………………………….. 10 Time-Based Intervals………………………………... 3 Symbol Properties and Trading Sessions……………. 11 Activity-Based Intervals……………………………... 4 Using Background Dragging…………………………… 12 Price-Based Intervals……………………………...... 4 Chart Analysis Windows Chart Analysis windows, or charts, are used to display price data for historical and real-time technical analysis, as well as for strategy back-testing and automation. You can create as many Chart Analysis windows as you like, on the same workspace or on different workspaces. To create a Chart Analysis window, click on the Chart Analysis icon from the TradingApp Launcher or click on the File – New – TradingApp Window… menu sequence and click Chart Analysis from the TradingApp Launcher. Page 1 of 13 Learning TradeStation Lesson 4 Chart Analysis – Bar-Building Techniques and Chart Styles Formatting the Symbol in a Chart You can change the settings and appearance of a Chart Analysis window by formatting the symbol. To access the Format Symbol dialog, click on the Format – Symbol… menu sequence or right-click on the background of a Chart Analysis window and click on Format Symbol… from the right-click menu. The Format Symbol dialog has four tabs with all the settings to customize the data and appearance in a Chart Analysis window. Changing Symbol, Bar Interval and Range In the Select Interval box, you can choose the method used to build bars. -

Ifmc Institute

IFMC INSTITUTE COURSE BROCHURE IFMC BRANCHES LAJPAT NAGAR VAISHALI NORTH CAMPUS GHAZIABAD NOIDA (DELHI) (DELHI) ND E-90, PLOT No. 3, 2 FLOOR, SHOP No. 3, VIJAY BASEMENT, FIRST FLOOR, RELIANCE PLAZA 2 NAGAR, HUDSON MAAN SINGH COMPLEX, LAJPAT NAGAR 1, MAIN MARKET LANE, KINGSWAY SECTOR 15 MAIN ROAD, NEW DELHI - 110024 SECTOR 4, VAISHALI, CAMP, OPPOSITE NEXT TO BHAGMAL GHAZIABAD - 201012 NDPL OFFICE, COMPLEX, NEAR Mc NEAR SHIV MANDIR, DONALD SECTOR 16, NEW DELHI - 110009 NOIDA – 201301 PH: +91-981-021-6889 PH: +91-120-437-7006 +91-981-026-0089 PH: +91-981-026-0089 PH: +91-981-021-6889 CONTENTS Stock Market Course for Traders ............................................................................................................ 3 Unique Feature of Stock Market Course for Traders .......................................................................... 3 What You Will Get ............................................................................................................................... 4 Fees and Duration ............................................................................................................................... 4 Detail Curriculum ................................................................................................................................ 4 Module 1: capital market & its operation ....................................................................................... 4 Module 2: Derivatives Market & its Operations ............................................................................ -

TECHNICAL ANALYSIS This Page Intentionally Left Blank TECHNICAL ANALYSIS

TECHNICAL ANALYSIS This page intentionally left blank TECHNICAL ANALYSIS THE COMPLETE RESOURCE FOR FINANCIAL MARKET TECHNICIANS THIRD EDITION Charles D. Kirkpatrick II, CMT Julie Dahlquist, Ph.D., CMT Publisher: Paul Boger Editor-in-Chief: Amy Neidlinger Executive Editor: Jeanne Levine Editorial Assistant: Kristen Watterson Cover Designer: Chuti Prasertsith Managing Editor: Kristy Hart Senior Project Editor: Betsy Gratner Copy Editor: Gill Editorial Services Proofreader: Sarah Kearns Indexer: WordWise Publishing Services Compositor: Nonie Ratcliff Manufacturing Buyer: Dan Uhrig © 2016 by Pearson Education, Inc. Publishing as FT Press Old Tappan, New Jersey 07675 This book is sold with the understanding that neither the author nor the publisher is engaged in rendering legal, accounting, or other professional services or advice by publishing this book. Each individual situation is unique. Thus, if legal or financial advice or other expert assistance is required in a specific situation, the services of a competent professional should be sought to ensure that the situation has been evaluated carefully and appropri- ately. The author and the publisher disclaim any liability, loss, or risk resulting directly or indirectly from the use or application of any of the contents of this book. For information about buying this title in bulk quantities, or for special sales opportunities (which may include elec- tronic versions; custom cover designs; and content particular to your business, training goals, marketing focus, or branding interests), please contact our corporate sales department at [email protected] or (800) 382-3419. For government sales inquiries, please contact [email protected]. For questions about sales outside the U.S., please contact [email protected]. -

A Comparison of Japanese Kagi Charting with Point & Figure Charting

A Comparison of Japanese Kagi Charting with Point & Figure Charting Julia E. Bussie, CMT Introduction Kagi As the world shrinks to become one global community with Kagi charts are drawn with straight lines, the thickness of the borders and language barriers disappearing, individuals become line depending on whether the market is in a bullish or bearish more receptive to the ideas, methods and techniques of other mode. A bullish or rising trend in prices is designated by a thick cultures. Such has been the case in recent years in the C.S. con- kagi line called the “>-ang” line. The thin kagi line, called the cerning market analysis methods historically used by Japanese “yin” line, is used when prices are falling in a bearish trend. The investors. Thanks in most part to the efforts of analyst and au- line changes from thick to thin or pang to yin (bullish to bearish) thor Steve Nison, CMT, who researchedJapanese methods of tech- and lice versa when the trend changes, allowing a quick and clear nical analysis for his books Jananese Candlestick Chartirw Tech- reading of whether a market is in a bullish or bearish trend. The niques and Beyond Candlesticks, such terms as “candlesticks,” proportion of a line that is yang versus yin (thick I-ersus thin) “kagi” and “renko” are familiar to American technicians. Candle- indicates the relative strength or weakness of the market. ‘Kn” sticks are now included in most computer programs for technical and ‘Yang” are ancient Chinese philosophic and religious terms analysis. These methods have similarities with certain techniques that fbrmed the basis for Chinese medical practices as far back as that have been in use in the IVest for manv vears,~ but each has its the 8th century B.C., and it is likely through medicine that the\ own unique flavor providing differing vantage points for viewing were introduced into Japanese culture. -

Master Thesis

Masaryk University Faculty of Economics and Administration Study Programme: Finance THE USE OF TECHNICAL ANALYSIS IN TRADING ON FOREX MARKET Master Thesis Supervisor: Author: Ing. Peter Mokrička Bc. Marián Hockicko Brno, May 2014 Masaryk University Faculty of economics and administration Department of finance Academic year 2013/2014 ASSIGNEMENT Name: HOCKICKO Marián Department: Finance Topic: THE USE OF TECHNICAL ANALYSIS IN TRADING ON FOREX MARKET /Czech/ Vyuţití technické analýzy při obchodování na trhu FOREX P r i n c i p l e s : The aim: To propose an optimization of selected technical analysis indicators on the Forex market and formulate recommendations for intraday traders. Approach of work and the methods used: 1. Definition and characteristics of FOREX market 2. Characteristics of technical analysis and technical analysis indicators 3. Creating, testing and optimization of defined trading strategy 4. Formulation of conclusions and recommendations Methods: description, analysis, comparison, deduction, synthesis Graphic pictures: acoording to instructions Extent: 60 – 80 pages Bibliography: BACHRATÝ, Milan. Forex :dobrodružstvo vývoja stratégie. [Slovensko]: Fxmprofit, 2012. 190 s. ISBN 9788097092603. VESELÁ, Jitka. Investování na kapitálových trzích. Vyd. 1. Praha: ASPI, 2011. 789 s. ISBN 9788073576479. HARTMAN, Ondřej. Jak se stát forexovým obchodníkem :naučte se vydělávat na měnových trzích. Praha: FXstreet.cz, 2009. 230 s. ISBN 978-80-904418-0. O'KEEFE, Ryan. Making Money in Forex: Trade Like a Pro Without Giving Up Your Day Job. : John Wiley and Sons, 2010. ISBN 0-470-48728-3. HARTMAN, Ondřej a Ludvík TUREK. První kroky na FOREXu. Vyd. 1. Brno: Computer Press, 2009. 120 s. ISBN 978-80-251-2006. Trading and investing in the Forex market using chart techniques.