Application for Prior Consent Under Section 7P

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hong Kong SAR and China

Regulatory Environment for Future Mobile Multimedia Services -- The Case of Hong Kong SAR and China Country Case Study Prepared for the ITU New Initiatives Workshop on the Regulatory Environment for Future Mobile Multimedia Services Xu Yan HKUST Business School [email protected] Mobile Multi-media Services in Hong Kong Highly competitive mobile market: 11 2G licenses + 4 3G licenses + 7 MVNO Licenses Market restructuring in past 12 months Poor usage of SMS Three trends in the 3G era Mobile/media Convergence Synergy of Corporate Resources and Strategies Fixed/mobile Convergence Mobile/media Convergence Mobile + TV Mobile + Radio Mobile + Newspaper Mobile + Internet Portal Synergy of Corporate Resources Shared channel by NOW and PCCW Mobile Fixed/mobile Convergence Home / Office/Retail WiseWatch Platform Mobile Operator WiseWatch Wired WiseWatch WiFi Camera Camera View from Mobile Data GPRS / EDGE / 3G Data 3GPP Video Streaming WS Mobile Video WAP Access Data Internet Surv App Server Servers 2G/3G Mobile Network Router (Wired/ Wireless) Broadband Modem View from PC Internet / IP Access Web Access Video Streaming Servers • Server Authentication Security • Automatic IP adaptation Internet / IP Access • Automatic screen sizing Video Streaming • Motion detection Mobile Multi-media Services in China Duopoly Market China Mobile China Unicom Impressive Growth of SMS 300000 249609 250000 200000 172600 150000 103000 40400 Million Messages 100000 6075 50000 440 0 2000 2001 2002 2003 2004 2005 Revenues from China Mobile’s New Services -

SUNDAY Communications Limited (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 0866)

The Stock Exchange of Hong Kong Limited takes no responsibility for the contents of this announcement, makes no representation as to its accuracy or completeness and expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. SUNDAY Communications Limited (Incorporated in the Cayman Islands with limited liability) (Stock Code: 0866) ANNOUNCEMENT (1) VERY SUBSTANTIAL DISPOSAL AND CONNECTED TRANSACTION (2) VOLUNTARY WITHDRAWAL OF LISTING AND PROPOSED DISTRIBUTION Offer to purchase substantially all the businesses and assets of the SUNDAY Group The Directors announce that on 25 September 2006, the Company received from PCCW, its controlling shareholder, an offer letter offering to purchase the entire issued share capital of SUNDAY Holdings, a wholly owned subsidiary of the Company. It is a condition precedent to completion of the sale and purchase of SUNDAY Holdings contemplated by the Offer Letter that an internal group reorganisation first be implemented. On completion of the internal group reorganisation, SUNDAY Holdings would be the holding company of: (a) Mandarin and SUNDAY 3G, which are the SUNDAY Group’s operating subsidiaries respectively providing 2G and 3G telecommunications services; (b) SUNDAY IP, which holds all of the intellectual property rights required by Mandarin and SUNDAY 3G for those businesses; and (c) SUNDAY China, which is the holding company for the SUNDAY Group’s back office operations located in the PRC, which are carried on by SUNDAY Communications Services (Shenzhen) Limited. Accordingly, the sale and purchase contemplated by the Offer Letter is a sale of substantially all the operating businesses and assets of the SUNDAY Group. -

PCCW CAPITAL NO. 4 LIMITED (Incorporated in the British Virgin Islands with Limited Liability)

PCCW CAPITAL NO. 4 LIMITED (incorporated in the British Virgin Islands with limited liability) U.S.$300,000,000 5.75% GUARANTEED NOTES DUE 2022 irrevocably and unconditionally guaranteed by PCCW LIMITED (incorporated in Hong Kong with limited liability) ISSUE PRICE: 98.775% The 5.75% Guaranteed Notes due 2022 (the “Notes”) in the aggregate principal amount of U.S.$300,000,000 to be issued by PCCW Capital No. 4 Limited (the “Issuer”) will be irrevocably and unconditionally guaranteed (the “Guarantee”) by PCCW Limited (the “Guarantor”). The Notes will bear interest from 17 April 2012 at the rate set forth above, payable semi-annually in arrear on 17 April and 17 October of each year (commencing on 17 October 2012). The Notes mature on 17 April 2022. The Notes are not redeemable prior to maturity, except that the Notes may be redeemed, in whole but not in part, in the event of certain developments affecting taxation at 100% of their principal amount plus accrued interest and in the event of a Change of Control (as defined in the Terms and Conditions of the Notes) at 101% of their principal amount plus accrued interest, as described in this Offering Circular. The Notes will constitute direct, general, unconditional, unsubordinated and (subject to the negative pledge set out in the Terms and Conditions of the Notes) unsecured obligations of the Issuer which will at all times rank pari passu among themselves and at least pari passu with all other present and future unsecured unsubordinated obligations of the Issuer, save for such obligations as may be preferred by provisions of law that are both mandatory and of general application. -

NETVIGATOR Broadband Service Guide

NETVIGATOR Broadband Service Guide About this Service Guide This NETVIGATOR Broadband Service Guide provides further information relating to NETVIGATOR Service (which includes NETVIGATOR Broadband and Fiber-to-the-Home Broadband Services), the Service Plans and options in your NETVIGATOR Application. Please read this Service Guide carefully as the Services entitlements, eligibility criteria and other important information applies to the Services, now TV services, MOOV services and the Extra Services you may additionally subscribe under your NETVIGATOR Application. All capitalized terms used in this Service Guide shall have the same meanings ascribed to them in the General Conditions and the applicable Special Conditions, unless the context may otherwise require or unless speci- fied otherwise in this Service Guide. PART I Important Information Service Providers – As applicable for the service(s) subscribed to as set out your NETVIGATOR Application n Hong Kong Telecommunications (HKT) Limited (“HKT”) provides all telecommunications Services (other than PCCW-HKT mobile services) upon the terms of your NETVIGATOR Application, this Service Guide, and the General Conditions of Telecommunications Service (Consumer Customers) (available at www.hkt.com/Terms+of+Use) (the “General Conditions”) and the applicable special conditions (if any). The Special Conditions of NETVIGATOR Broadband Service for Consumer Customer are available at http://cs.netvigator.com/tnc_e.html. HKT provides certain non-telecommunication services (including F-Secure Safe Everywhere services) upon the terms of your relevant Application and Service Guide, and HKT General Conditions of Service (available at http://cs.netvigator.com/tnc_e.html) and the applicable special conditions (if any). The Special Conditions of F-Secure Safe Everywhere Services are available at http://cs.netvigator.com/tnc_e.html. -

Interim Report 2020/2021

ABOUT US SmarTone Telecommunications Holdings Limited (0315.HK), listed in Hong Kong since 1996 and a subsidiary of Sun Hung Kai Properties Limited, is a leading telecommunications provider with operating subsidiaries in Hong Kong and Macau, offering voice, multimedia and mobile broadband services, as well as fixed fibre broadband services for both consumer and corporate markets. SmarTone spearheaded 5G development in Hong Kong since May 2020, with the launch of its territory-wide 5G services. SmarTone is your smart partner that delivers a trusted and connected experience through our high-quality network, people-driven products and services combined with innovation, passion and understanding of customer needs. SmarTone differentiates our content, excellent customer service, business and consumer products for all our Hong Kong customers, allowing them to live and feel smarter everyday. This strong presence is also backed by expert technical know-how, over 30 stores across Hong Kong, our 5 core brands and our innovative business strategies arm. CONTENTS About Us Business Highlights 2 Chairman’s Statement 6 Management Discussion and Analysis 8 Directors Profile 11 Staff Engagement 20 Community Engagement 22 Report on Review of Interim Financial Information 24 Condensed Consolidated Profit and Loss Account 25 Condensed Consolidated Statement of Comprehensive Income 26 Condensed Consolidated Balance Sheet 27 Condensed Consolidated Statement of Cash Flows 29 Condensed Consolidated Statement of Changes in Equity 30 Notes to the Condensed Consolidated Interim Financial Statements 32 Other Information 48 INTERIM REPORT 2020/21 INTERIM REPORT 1 BUSINESS HIGHLIGHTS Spearhead 5G and Smart City development in Hong Kong SmarTone provides nearly full 5G coverage in Hong Kong with the widest coverage* both indoors and outdoors, to bring a faster, stabler and smoother 5G experience. -

Arrangements for the Frequency Spectrum in the 2.5/2.6 Ghz Band

Arrangements for the Frequency Spectrum in the 2.5/2.6 GHz Band upon Expiry of the Existing Assignments for the Provision of Public Mobile Services and the Related Spectrum Utilisation Fee Consultation Paper 23 September 2020 PURPOSE This paper is jointly issued by the Communications Authority (“CA”) and the Secretary for Commerce and Economic Development (“SCED”) to seek views and comments of the telecommunications industry and other affected persons on the proposed arrangements for re-assignment of 90 MHz of spectrum in the 2.5/2.6 GHz band upon expiry of the existing assignments on 30 March 2024 and methods for setting the related spectrum utilisation fee (“SUF”). BACKGROUND 2. A total of 90 MHz of spectrum in the 2.5/2.6 GHz band was assigned in March 2009 for the provision of public mobile services, and the existing assignments are due to expire in March 2024. The assignments are made to three assignees1, each with an amount of 2 x 15 MHz in the frequency ranges of 2500 – 2515 MHz paired with 2620 – 2635 MHz and 2540 – 2570 MHz paired with 2660 – 2690 MHz (hereafter referred to as “Available Spectrum”)2. 1 China Mobile Hong Kong Company Limited (“CMHK”), Hong Kong Telecommunications (HKT) Limited (“HKT”) and Genius Brand Limited (“Genius Brand”) are the incumbent assignees of the Available Spectrum, with each of them holding 2 x 15 MHz of the spectrum. Genius Brand is a joint venture indirectly owned by HKT and Hutchison Telephone Company Limited (“Hutchison”). The spectrum in the 2.5/2.6 GHz band assigned to Genius Brand is assumed to be divided equally between HKT and Hutchison for the purpose of calculation of the spectrum holding in this consultation paper. -

Arrangements for the Frequency Spectrum in the 900 Mhz and 1800

Arrangements for the Frequency Spectrum in the 900 MHz and 1800 MHz Bands upon Expiry of the Existing Assignments for Public Mobile Telecommunications Services and the Spectrum Utilisation Fee Consultation Paper 3 February 2016 FOREWORD This paper seeks views and comments of the telecommunications industry and other affected persons on the arrangements for re-assignment of the frequency spectrum in the 900 MHz and 1800 MHz bands upon expiry of the existing assignments between November 2020 and September 2021. This paper also seeks views and comments on the methods for setting the related spectrum utilisation fee (“SUF”). The Communications Authority (“CA”) and the Secretary for Commerce and Economic Development (“SCED”) plan to conduct two rounds of public consultation on the arrangements for the spectrum re-assignment and the related SUF, with a view to making their respective decisions on the way forward by November 2017. For the avoidance of doubt, all the information given and views expressed in this consultation paper are for the purpose of discussion and consultation only. Nothing in this consultation paper represents or constitutes any decision made by the CA or the SCED. The consultation contemplated by this consultation paper is without prejudice to the exercise of the powers by the CA and the SCED under the Telecommunications Ordinance (Cap. 106) (“TO”) or any subsidiary legislation thereunder. Any person wishing to respond to the public consultation should do so on or before 18 April 2016. The CA and the SCED may publish all or part of the views and comments received, and disclose the identity of the source in such manner as they see fit. -

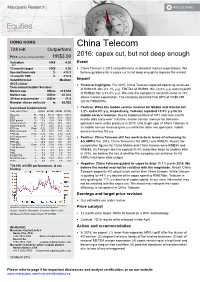

China Telecom 728 HK Outperform 2016: Capex Cut, but Not Deep Enough Price (At 05:20, 22 Mar 2016 GMT) HK$3.90

HONG KONG China Telecom 728 HK Outperform 2016: capex cut, but not deep enough Price (at 05:20, 22 Mar 2016 GMT) HK$3.90 Valuation HK$ 4.30 Event - DCF 12-month target HK$ 4.30 . China Telecom’s 2015 net profit came in ahead of market expectations. We Upside/Downside % +10.3 believe guidance for a capex cut is not deep enough to impress the market. 12-month TSR % +12.5 Volatility Index Medium Impact GICS sector . Financial highlights. For 2015, China Telecom reported operating revenues Telecommunication Services of RMB331.2bn (+2.1% y-y), EBITDA of RMB94.1bn (-0.8% y-y) and net profit Market cap HK$m 315,636 of RMB20.1bn (+13.4% y-y). We note the company’s net profit came in ~5% Market cap US$m 41,022 30-day avg turnover US$m 21.6 above market expectation. The company declared final DPS of HK$0.095 Number shares on issue m 80,932 (2014: HK$0.095). Investment fundamentals . Positive: While the mobile service revenue for Mobile and Unicom fell Year end 31 Dec 2014A 2015E 2016E 2017E 1.2% and 8.0% y-y, respectively, Telecom reported +3.5% y-y for its Revenue bn 324.4 351.8 380.6 400.7 mobile service revenue. Due to implementation of VAT and “one-month EBIT bn 28.5 30.4 36.0 42.2 EBIT growth % 3.8 6.8 18.4 17.2 mobile data carry-over” initiative, mobile service revenue for domestic Reported profit bn 17.7 20.5 24.6 29.3 operators were under pressure in 2015. -

Customer Name

Tariff No.: U0008-002-Jul2015-N Published on 20 July 2015 UNIFIED CARRIER LICENCE TELECOMMUNICATIONS ORDINANCE (CHAPTER 106) Hong Kong Telecommunications (HKT) Limited (“HKT”) Name of Tariff: PCCW mobile General Terms and Conditions Description of Tariff: CSL Mobile Limited (“CSL”) on behalf of HKT hereby publishes the tariffs of the Services provided by HKT. CSL acquires mobile services in bulk from HKT and is authorized to interface with and resell the mobile services to end customers. See Annex A for details. This tariff applies to all contracts entered into by (a) PCCW mobile consumer customers before 1 July 2011; and (b) PCCW mobile commercial customers before 7 July 2014 with CSL (formerly known as PCCW Mobile HK Limited). Effective Date of Tariff: 20 July 2015 Revision History: First publication on 20 July 2015. Page 0 of 6 Annex A PCCW mobile General Terms and Conditions The Service provided by PCCW mobile is subject to these General Terms and Conditions, the Special Conditions, the Service Literature and any other terms and conditions in the Application (if any). Capitalized terms in these General Terms and Conditions have the meanings given to them in Clause 13. 1. Application 1.1 PCCW mobile is entitled, in its discretion, to reject the Application for the Service if: (a) the Customer fails to submit proof of identity and address; (b) the Customer fails to satisfy the requisite creditability check; (c) the porting-out of the mobile number of the Customer from another mobile operator to PCCW mobile is unsuccessful (if applicable); or (d) the Customer fails to pay the stipulated price for the Mobile Device, Charges and/or deposit in full. -

MIMO in HSPA: the Real-World Impact MIMO in HSPA: the Real-World Impact

MIMO in HSPA: the Real-World Impact MIMO in HSPA: the Real-World Impact Contents 1 Executive Summary 2 2 The Role of MIMO in HSPA 3 2.1 What is MIMO, and What Does it Provide? 3 3 Implementation and Deployment 4 3.1 Co-existence of MIMO and Legacy Terminals 4 3.2 An Implementation Example 5 3.3 Deployment Considerations 7 4 Experiencing MIMO: from Field Trials to Network Deployments 9 4.1 Case Study at 2100MHz 9 4.2 Case Study at 900 MHz (Polsat) 11 5 The MIMO Ecosystem and Outlook 12 6 MIMO Evolution in 3GPP 13 6.1 MIMO Continues to Evolve in 3GPP 13 6.2 Leveraging Today’s MIMO Investments through Multi-User MIMO: 13 7 Conclusion and Recommendations 15 2 MIMO in HSPA: the Real-World Impact Figure List Figure 2.1: MIMO Improves Data Rates for all Users and Increases Capacity 3 Figure 3.1: Virtual Antenna Mapping 4 Figure 3.2: Overview of Huawei Co-Carrier Solution for MIMO & legacy Terminals 5 Figure 3.3: MIMO User Throughput Gain in Huawei Solution 6 Figure 3.4: MIMO Cell Throughput Gain in Huawei Solution 6 Figure 3.5: Different Evolution Strategies, where MIMO Plays a Fundamental Role 7 Figure 3.6: Easy Long-Term Evolution Steps of HSPA and LTE (Typical Example) 8 Figure 4.1: Field Test, Relative Average Cell Gain of MIMO Compared to 16 QAM and to 64 QAM 9 Figure 4.2: Field Measurement of Single User HSPA+ Performance (UDP Traffic) 10 Figure 4.3: Field Measurement of Multi-User HSPA+ Performance (2 Users with UDP Traffic) 10 Figure 4.4: Field Measurement of Dual Carrier vs Single Carrier (SIMO) HSPA+ Capacity 10 Figure 4.5: Average Throughput of Single User at More Than 30 Test Locations./ Peak Rate in Lab Test. -

DELIVERING HONG KONG's FIRST QUADRUPLE-PLAY EXPERIENCE

PCCW annual report 2006 9 BUSINESS OVERVIEW DELIVERING HONG KONG’s FIRST QUADRUPLE-PLAY EXPERIENCE Year 2006 saw PCCW become Hong Kong’s first “quadruple- A whole new vista of opportunity then materialized as PCCW play” operator, changing the face of the local set out to discover more imaginative ways of applying our telecommunications industry. quadruple-play capability to produce a succession of innovative-yet-affordable services. Customers are now able to tailor their own digital lifestyles at home, at work and on the move, thanks to PCCW’s newfound Synergies between formerly disparate units soon began to power to provide innovative services across four platforms – emerge, giving rise to new lines of business and the fixed line, broadband Internet access, TV and mobile. transformation of the Company from access provider – as a traditional telecoms operator – to new breed of ICT/media- A prime example was the world’s first screening of real-time delivery player, bringing a whole new meaning to the PCCW television on 3G handsets using Cell Multimedia Broadcast brand. technology to take programming from our now TV platform to mobile phones. In addition, our award-winning innovation at home in the public and private sectors is now in demand overseas, opening up more revenue opportunities and positioning the Company as an industry role model on the world stage. 10 PCCW annual report 2006 BUSINESS OVERVIEW Telecommunications Services (TSS) Services (TSS) ENRICHING OUR FIXED-LINE OFFERING PCCW annual report 2006 11 LOCAL TELEPHONY The Company’s Commercial Group scored a number of Yet more innovative services and functionality from PCCW lucrative contract wins last year, especially in Macau’s continued to enrich Hong Hong’s fixed-line experience in booming hospitality and gaming market, which resulted in 2006, helping the Company to enjoy more net line gain and some HK$200 million in new income generated by telecoms stability, and focus on increasing average revenue per user. -

Press Release Ericsson

PRESS RELEASE March 19, 2020 SmarTone selects Ericsson’s 5G to power digitalization in Hong Kong • Ericsson chosen for radio access network (RAN) and Core • SmarTone to use Ericsson Spectrum Sharing solution to launch 5G services on existing bands • Deal also includes Ericsson’s Dual-Mode 5G Core including a full NFV stack, AI-powered RAN capabilities and Ericsson Orchestrator Ericsson (NASDAQ: ERIC) and SmarTone, one of the leading communication service providers in Hong Kong, have agreed to a five-year contract for the deployment of 5G in Hong Kong. Ericsson is the sole supplier of SmarTone’s 4G network and will continue as their sole 5G vendor – extending the companies’ 28 years of partnership. Stephen Chau, Chief Technology Officer of SmarTone, says: “SmarTone has been preparing for the 5G era with Ericsson in Hong Kong since January 2017, when we conducted the first 5G technology demo in this market. Together, Ericsson and SmarTone have led global technology developments in mobility and delivered multiple ‘firsts’ through early joint trials, shared research and collaborative product development. We will continue to leverage our long-term partnership to build a world-class and robust 5G network in Hong Kong and deliver best-of-breed 5G network experience to customers. SmarTone is also proud to be playing a key role in Hong Kong’s transformation to a smart city.” SmarTone will be the first operator in Hong Kong to deploy Ericsson Spectrum Sharing – a unique spectrum sharing technology that enables dynamic sharing of spectrum between 4G and 5G and more efficient use of its existing spectrum and existing Ericsson Radio System infrastructure for 5G deployment.