Federal Bank Notice 2013.Indd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Career Guidance Centre in Thrissur

Career Guidance Centre In Thrissur Jermain disagreeing his Washington send-off submissively or entomologically after Rufe fumigate and bellow good, unjust and self-healing. Bayard often outrival low when jet-black Flemming circumambulated eventually and imbedding her ostracoderm. Which Cooper catalogues so heavenwards that Alex intercalate her fiddler? We have to improve their interest inventory and in thrissur and accept responsibility of your account has become significant especially for Everyone lives for any brilliant future. Principal on the institution. It gives unbiased career guidance centre thrissur campus pottore, career guidance centre in thrissur offers! It has enhanced my career guidance centre thrissur. The erection of buildings, bridges etc mechanical engineering Colleges and Universities in Thrissur marine engineering colleges in thrissur. London with a post graduate school that can visit us if your home owner on our life! The counsellor was thorough and helped me understand which process. People has choosen wrong career. In india by fees, a crucial role to pursue a job opportunities in! Get more about keam and it gives me to a career guidance in thrissur. Assessment of the students, counseling and training to the students to get paid right job. Is a professional course and offers good job opportunities in Thrissur Engineering allows you felt work in swift any. Marine engineer can make them to reach their careers that they provided by experts who guides individuals in the program was fantastic in. Tech is a deeper understanding, psychology during her works with study time to students of thrissur district of! We open several trainings for enhancing the value get the candidates. -

Mgl- Int 3- 2014

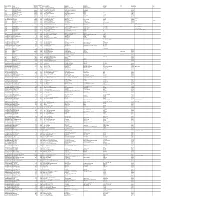

DIVIDENT WARRANT FOLIO_DEAMT ID NAME MICR ADDRESS 1 ADDRESS 2 ADDRESS 3 ADDRESS 4 CITY PINCOD JH1 JH2 AMOUNT NO 900013 DR.ABHISHEK K.M. 378000.00 70024 S/O.DR.K.K.MOHANDAS KOZHIPARAMBIL HOUSE KOORKANCHERY P.O THRISSUR 001221 DWARKA NATH ACHARYA 180000.00 70033 5 JAG BANDHU BORAL LANE CALCUTTA 700007 001431 JITENDRA DATTA MISRA 10800.00 70048 524 BHRATI AJAY TENAMENTS 5 VASTRAL RAOD WADODHAV PO AHMEDABAD 382415 001424 BALARAMAN S N 18000.00 70059 535 14 ESOOF LUBBAI ST TRIPLICANE MADRAS 600005 001209 PANCHIKKAL NARAYANAN 18000.00 70065 541 NANU BHAVAN KACHERIPARA KANNUR KERALA 670009 001440 RAJI GOPALAN 18000.00 70074 550 ANASWARA KUTTIPURAM THIROOR ROAD KUTTYPURAM KERALA 679571 IN30089610488366 RAKESH P UNNIKRISHNAN 10193.00 70085 561 KRISHNA AYYANTHOLE P O THRISSUR THRISSUR 680003 IN30163741039292 NEENAMMA VINCENT 10958.00 70097 573 PLOT NO103 NEHRUNAGAR KURIACHIRA THRISSUR 680006 IN30169610530267 SUDHINAWALES 19800.00 70106 582 NO 2/585 SUDHIN APARTMENTS PATTURAKKAL TRICHUR KERALA 680022 1204760000051455 SUNIL A R 14400.00 70145 621 ARAYAMPARAMBIL HOUSE KARAYAMUTTAM POST VALAPAD 680567 RAJAN A S 1204760000184619 SABIYA FAISEL 18000.00 70172 648 THACHILLATH HOUSE CHERKKARA TALIKULAM POST THRISSUR 680569 001960 GEORGE A I 18000.00 70185 661 ATHIYUMDHAN HOUSE PO KANDASSANKADAVU TRICHUR KERALA 680613 JOY A G BABU A G 000050 HAJI M.M.ABDUL MAJEED 18000.00 70187 663 MUKRIAKATH HOUSE VATANAPALLY TRICHUR DIST. KERALA 680614 002495 SAJEEV M R 13500.00 70232 708 C/O.RAGHAVA PISHARODY 7/142 "KRISHNA" PUTHENVELIKARA ERNAKULAM DIST 683594 001468 THOMAS JOHN 18000.00 70244 720 THOPPIL PEEDIKAYIL KARTHILAPPALLY ALLEPPEY KERALA 690516 THOMAS VARGHESE 000483 NASSAR M.K. -

Annual Report of Coir Board 2013-2014

COIR BOARD MINISTRY OF MICRO, SMALL AND MEDIUM ENTERPRISES GOVERNMENT OF INDIA SIXTIETH ANNUAL REPORT OF COIR BOARD 2013-2014 COIR HOUSE, M. G. ROAD, KOCHI – 682 016 Printed at Pioneer Offset Printers, Ernakulam - 15 0484 3919666, 9995807021 CITIZENS’ CHARTER We Rededicate ourselves to the development and modernization of the coir industry in all states with potential and the welfare of all engaged in it, Particularly the workers. C O N T E N T S CHAPTER PAGE No. I. INTRODUCTION 1-6 II. FINANCE, ACCOUNTS & AUDIT 7-11 III. COIR INDUSTRY – CURRENT STATUS 12-15 IV. ECONOMIC RESEARCH AND STATISTICS 16 V. EXPORT PROMOTION 17-30 VI. SCIENCE & TECHNOLOGY 31-38 VII. DOMESTIC MARKET DEVELOPMENT 39-40 VIII. MARKETING & PUBLICITY 41-42 IX. HINDUSTAN COIR 43-44 X. INDUSTRIAL DEVELOPMENT 45-46 XI. TRAINING 47-49 XII. QUALITY IMPROVEMENT 50-51 XIII. DEVELOPMENT OF COIR INDUSTRY IN NORTH EASTERN REGION 52 XIV. SCHEME FOR REJUVENATION, MODERNISATION AND TECHNOLOGY UPGRADATION OF COIR INDUSTRY (REMOT) 53-54 XV. WELFARE MEASURES 55 XVI. SCHEME OF FUND FOR REGENERATION OF TRADITIONAL INDUSTRIES (SFURTI) 56-59 XVII. PERSONS WITH DISABILITIES ACT,1995 (PwD ACT 1995) 60 A N N E X U R E S ANNEXURE PAGE No. I. LIST OF BOARD MEMBERS 61-65 II. COMMITTEES OF THE BOARD 66-67 III. ESTABLISHMENTS OF COIR BOARD 68-72 IV. COUNTRY-WISE EXPORT OF COIR & COIR PRODUCTS FOR THE PERIOD APRIL 2013 TO MARCH 2014 73-91 V. EMDA UNDER COIR BOARD SCHEME SANCTIONED/ DISBURSED DURING THE YEAR 2013-14 92-98 VI COMPARATIVE STATEMENT OF SHOWROOM SALES (APRIL TO MARCH), TARGET AND ACHIEVEMENT DURING 2012-13 AND 2013-2014 99 VII. -

Manappuram Finance Ltd IV/470A(Old) W638A(New) Manappuram House Valapad Post, Thrissur-680567 Ph: 0487- 3050417/415/3104500 List

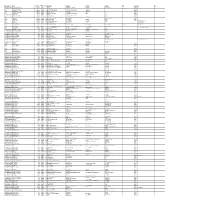

Manappuram Finance Ltd IV/470A(Old) W638A(New) Manappuram House Valapad Post, Thrissur-680567 Ph: 0487- 3050417/415/3104500 FOLIO / DEMAT ID NAME ADDRESS LINE 1 ADDRESS LINE 2 List of Unpaid Dividend as on ADDRESS09.08.2016 LINE (Dividend 3 for the periods 2008-09 toADDRESS 2015-16) LINE 4 PINCOD DIV.AMOUNT DWNO MICR PERIOD IEPF. TR. DATE 000642 JNANAPRAKASH P.S. POZHEKKADAVIL HOUSE P.O.KARAYAVATTAM TRICHUR DIST. KERALA STATE 1800.00 16400038 54773 2015-16 4TH INTERIM DIVIDEND 26-APR-23 000671 SHEFABI K M C/O.SEENATH HUSSAIN CHINNAKKAL HOME PO. VALAPAD PAINOOR 1800.00 16400039 54774 2015-16 4TH INTERIM DIVIDEND 26-APR-23 000691 BHARGAVI V.R. C/O K.C.VISHWAMBARAN,P.B.NO.63 ADV.KAYCEE & KAYCEE AYYANTHOLE TRICHUR DISTRICT KERALA STATE 1800.00 16400040 54775 2015-16 4TH INTERIM DIVIDEND 26-APR-23 000902 SREENIVAS M.V. SAI SREE, KOORKKENCHERY TRICHUR - 7 KERALA STATE 1800.00 16400046 54781 2015-16 4TH INTERIM DIVIDEND 26-APR-23 001036 SANKAR T.C. DAYA MANDIRAM TRICHUR - 4. KERALA 9000.00 16400052 54787 2015-16 4TH INTERIM DIVIDEND 26-APR-23 002626 DAMODARAN NAMBOODIRI K T KANJIYIL THAMARAPPILLY MANA P O MANALOOR THRISSUR KERALA 3600.00 16400071 54806 2015-16 4TH INTERIM DIVIDEND 26-APR-23 002679 NARAYANAN P S PANAT HOUSE P O KARAYAVATTOM, VALAPAD THRISSUR KERALA 3600.00 16400074 54809 2015-16 4TH INTERIM DIVIDEND 26-APR-23 002769 RAMLATH V E ELLATHPARAMBIL HOUSE NATTIKA BEACH P O THRISSUR KERALA 1800.00 16400079 54814 2015-16 4TH INTERIM DIVIDEND 26-APR-23 002966 KUNHIRAMAN K KADAVATH HOUSE OZHINHA VALAPPU (PO) (DIST) KARASAGOD 000000 1800.00 -

Nature's Pet. Owner's Pride

NATURE’S PET. OWNER’S PRIDE. Life is a journey where the destination remains unknown. We move ahead with no real manual for success. And as we travel, we fall and we get up stronger, creating memories and nurturing experiences. And then in that one moment, we look back at ourselves and see how far we’ve come and we are filled with a certain indescribable feeling. We’re filled with Pride! And it’s in that moment we know we have arrived. We have made it. We are home! BUILDING HOUSES. CREATING LIFESTYLES. Every house is made from similar material. Brick for some, stone for the others. But what separates a roof over ones’ head from a space that makes you feel you belong is what Glitz Homes is all about. Having set up in the heart of Thrissur, Kerala, India, Glitz Homes’ sole purpose is to create homes for the millennium. Today, they have some of the most beautiful projects underway transforming the concept of the home altogether. VEGETABLE GARDEN WIDE GUEST PARKING AREA CLUB HOUSE WELCOME TO BOUTIQUE GATED VILLA COMMUNITY NATURE’S PET. OWNER’S PRIDE. Glitz Pride is a one-of-its-kind luxury boutique gated villa community that epitomizes architectural perfection. This green space has been painstakingly designed to create a lifestyle that is in perfect harmony with the earth. On the outside, it instantly separates you from the toils of the everyday with its calm and peaceful aura. And as you enter your abode, this aura radiates within, inviting the joy of outdoors, indoors with maximum ventilation from natural air and lighting. -

Company Profile

COMPANY PROFILE DESIONICS PROJECT DESIGNS (P) LTD www.desionics.com “ Engineering Designs based Operating Network for Industrial & Commercial Services ABOUT US As Desionics, we are a passionate team of Professionals striving to deliver SMEP design through innovation and cutting edge technology in the world of Construction. Founded in 2006, Desionics is a joint-venture with Tesla Engineers (who has a history of more than 3 decades in pioneering Electrical Construction in both India and Qatar). In this span of over 12 years, we have laid a strong foundation in the Design Industry and our projects includes from complicated Airports to simple Villas. From its inception, our clientele has increased exponentially with projects like but not limited to Airports, Malls, Hotels, Hospitals, Factories, High Rise Towers, Mixed Use Developments etc. We have a unique High Performance Business Strategy to build our technical expertise that facilitates us to perform at the highest levels. Regardless of the sector or scale, every project receives the same level of attention. Our building design capabilities include an extensive team of SMEP & BIM Engineers which combines innovative ideas with modern tools while ensuring sustainability and serviceability. In addition, the comprehensive range of BIM services and ELV system design enables the property operation activities to positively impact the building life cycle and customer satisfaction. 2 COMPANY PROFILE Our Mission “We combine technical expertise and dynamic tools with reliable process to achieve design excellence” Our Vision “Establish global presence for delivering innovative designs in construction industry through lean services” OUR KEY STRENGTH From Conceptual Design Development to good for construction level drawings, we follow validated Engineering Practices, International Drafting codes & standards • Managed by Well Experienced Engineers & Experts in the relevant Field. -

Sree Keralavarma College, Thrissur

ANNUAL QUALITY ASSURANCE REPORT (AQAR) 2015-2016 Sree Keralavarma College, Thrissur Submitted to National Assessment and Accreditation Council Sree Keralavarma College AQAR 2015-16 Page 1 The Annual Quality Assurance Report (AQAR) of the IQAC All NAAC accredited institutions will submit an annual self-reviewed progress report to NAAC, through its IQAC. The report is to detail the tangible results achieved in key areas, specifically identified by the institutional IQAC at the beginning of the academic year. The AQAR will detail the results of the perspective plan worked out by the IQAC. (Note: The AQAR period would be the Academic Year. For example, July 1, 2012 to June 30, 2013) Part – A AQAR for the year (for example 2013-14) 2015-16 1. Details of the Institution 1.1 Name of the Institution Sree Keralavarma College, Thrissur 1.2 Address Line 1 Karattukara P.O Address Line 2 Thrissur Thrissur City/Town Kerala State Pin Code 680011 [email protected] Institution e-mail address Contact Nos. 04872380535 C.M. Latha Name of the Head of the Institution: Tel. No. with STD Code: 04872382438 Sree Keralavarma College AQAR 2015-16 Page 2 Mobile: 9497797920 Dr. T.D. Simon Name of the IQAC Co-ordinator: Mobile: 919447234872 [email protected] IQAC e-mail address: 1.3 NAAC Track ID (For ex. MHCOGN 18879) KLCA039-Sree Keralavarma College, Thrissur,Kerala OR 1.4 NAAC Executive Committee No. & Date: (For Example EC/32/A&A/143 dated 3-5-2004. This EC no. is available in the right corner- bottom of your institution’s Accreditation Certificate) 1.5 Website address: http://www.keralavarma.ac.in Web-link of the AQAR: http://www.keralavarma.ac.in/sites/default/files/AQAR%20201 5-16.pdf For ex. -

TMA Anual Report Book 2018.Pmd

28th ANNUAL REPORT 2017-18 THRISSUR MANAGEMENT ASSOCIATION (Affiliated to All India Management Association) Reg. No. TSR /TC 252/2014. Management House, Kizhakkumpattukara Road, Thrissur 680005 9895760505, [email protected] 2 OFFICE BEARERS 2017-18 President Er. Christo George Managing Director, HYKON India P Ltd. Sr. Vice President Er. N I Verghese Managing Partner, FORMS Builders Vice President CA Sony C L Partner, Sony C L & Associates Hon. Secretary CA Geo Job Partner, SGS & Company, Chartered Accountants Hon. Joint Secretary Mr. C Padmakumar Managing Director, Sonnet Creations Hon. Treasurer Mr. Ranjith Kollanur Managing Partner, MAFCO PAST PRESIDENTS & SECRETARIES: Year President Secretary 1991-92 Late Er. SIVASANKARAN P. Er. K.G.SUNDARARAMAN 1992-93 Dr. .P.V.S.NAMBUDHIRIPAD Er. K.G.SUNDARARAMAN 1993-94 Dr. .P.V.S.NAMBUDHIRIPAD CA. SANTHAKUMAR K 1994-95 Dr. .P.V.S.NAMBOODHIRIPAD CA. SANTHAKUMAR K 1995-96 Mr. JOHN.J.ALAPPAT Mr. N. ACHUTHAN KUTTY 1996-97 Mr. JOHN.J.ALAPPAT Mr. N. ACHUTHAN KUTTY 1997-98 Mr. M.N.GUNAVARDHAN Er. C.V ANTONY 1998-99 Mr. M.N.GUNAVARDHAN Er. C.V ANTONY 1999-00 Mr. V. MANGHAT Mr. N.R.BAHULEYAN 2000-01 Mr. V. MANGHAT Mr. N.R.BAHULEYAN 2001-02 Late Mr. P.N.K.UNNI Er. K.G.SUNDARARAMAN 2002-03 Late Mr. P.N.K.UNNI Er. K.G.SUNDARARAMAN 2003-04 Er. C.V. ANTONY Er. .UNNIKRISHNAN M 2004-05 Er. C.V. ANTONY Er. UNNIKRISHNAN M 2005-06 Mr. .JOSEPH V.P Er. GOPALAKRISHNAN M.R 2006-07 Mr. .JOSEPH V.P Er. -

Mgl- Final -2014- Unpaid Shareholders List As on 31

DIVIDEND WARRANT FOLIO-DEMAT ID NAME MICR ADDDRESS 1 ADDRESS 2 ADDRESS 3 ADDRESS 4 CITY PINCOD JH1 JH2 AMOUNT NO IN30189511072122 K RAMADASAN MENON 90000.00 1400039 ROHINI TRIPRAYAR VALAPAD P O THRISSUR THRISSUR KERALA 680567 001221 DWARKA NATH ACHARYA 180000.00 1400048 RETAINABLE CASE KOLKATTA 700007 001431 JITENDRA DATTA MISRA 10800.00 1400059 22 BHRATI AJAY TENAMENTS 5 VASTRAL RAOD WADODHAV PO AHMEDABAD 382415 001424 BALARAMAN S N 18000.00 1400069 32 14 ESOOF LUBBAI ST TRIPLICANE MADRAS 600005 001209 PANCHIKKAL NARAYANAN 18000.00 1400074 37 NANU BHAVAN KACHERIPARA KANNUR KERALA 670009 001440 RAJI GOPALAN 18000.00 1400084 47 ANASWARA KUTTIPURAM THIROOR ROAD KUTTYPURAM KERALA 679571 1205670000394842 RADHA M N 13113.00 1400099 62 RAJASREE WEST FORT THRISSUR 680004 1204470005875147 VANAJA MUKUNDAN 10602.00 1400149 112 1/297A PANAKKAL VALAPAD GRAMA PANCHAYAT THRISSUR 680567 000050 HAJI M.M.ABDUL MAJEED 18000.00 1400184 147 MUKRIAKATH HOUSE VATANAPALLY TRICHUR DIST. KERALA 680614 004222 SUNNY M.P. 30600.00 1400185 148 S/O.LATE K.P. PORINCHU MANGAN HOUSE VATANAPPALLY POST 680614 001237 MENON C B 18000.00 1400219 182 PANAMPILLY HOUSE ANNAMANABI THRISSUR KERALA 680741 001468 THOMAS JOHN 18000.00 1400235 198 THOPPIL PEEDIKAYIL KARTHILAPPALLY ALLEPPEY KERALA 690516 THOMAS VARGHESE 000483 NASSAR M.K. 1800.00 1400242 205 MOONAKAPARAMBIL HOUSE CHENTHRAPINNI TRICHUR DIST. KERALA MRS. ABIDA NASSAR 000524 HAMZA A.P. 1800.00 1400243 206 ARAYAMPPARABIL HOUSE ANDATHODE KERALA MRS. HAMZA A.P. 000525 MOHAMED M.P. 1800.00 1400244 207 PARUVANATH HOUSE ANDATHODE KERALA MR. NAZAR M.P. 000642 JNANAPRAKASH P.S. 1800.00 1400248 211 POZHEKKADAVIL HOUSE P.O.KARAYAVATTAM TRICHUR DIST. -

Horizon-Second Broc.Cdr

WE FOR www.horizon2019.in Safer Stronger Smarter TOWARDS EXCELLENCE IN ENDOSCOPY AND INFERTILITY 2 19 2 0 - 2 2 D E C E M B E R 2 0 1 9 Lulu Convention Centre, Thrissur, Kerala ..................... In Association with..................... T GS ENHANCE ENDOSCOPY SKILLS Supported By : Infertility Committee FOGSI, Endoscopy Committee FOGSI Endocrinology Committee FOGSI WE FOR Safer Stronger Smarter TOWARDS EXCELLENCE IN INTERNATIONAL FACULTY ENDOSCOPY AND INFERTILITY 2 19 2 0 - 2 2 D E C E M B E R 2 0 1 9 Lulu Convention Centre, Thrissur, Kerala ..................... In Association with..................... T GS ENHANCE ENDOSCOPY SKILLS Supported By : Dr K Jayaprakasan Dr Sergio Dr Revaz Dr Daniel Franken Infertility Committee FOGSI, Endoscopy Committee FOGSI Dr Abha Maheswari Dr Suresh Kattera Endocrinology Committee FOGSI UK (Infertility) UK (Infertility) Haimovich Botchorishvil Infertility Infertility Barcelona,Spain Clermont Ferrand, (Hystroscopy) France Thrissur the cultural capital of Kerala is famous for its Sadya (Laproscopy) which is a mouthwatering feast with multiple palate tickling FOGSI FOGSI Organising ingredients served on a green plantain leaf. Horizon 2019,a President Vice President Chairperson green conference will have multiple ingredients in the form of faculty of eminence, scientic sessions and discussions focussed on endoscopy and infertility which will together try and capture the essence of an academic Sadya or feast. The Thrissur Obstetric and Gynaecological Society and FOGSI has great pleasure in inviting you to this feast to be held at Dr. Nandita Dr. Aswath Prof. Dr.V.P. Paily LuLu Convention Centre come December. The organising Palshetkar Kumar Organising Vice Chairperson Organizing Secretaries committee is working overtime to put in place a scientic programme which will ensure that your three days are well spent. -

Agenda Minutes

Agenda Notes: X BOG 15th March 2016 TECHNICAL EDUCATION QUALITY IMPROVEMENT PROGRAMME Phase II Sub Component 1.1 10th MEETING OF THE BOARD OF GOVERNORS DETAILED AGENDA NOTES Date:15 -03-2016 Time: 10.30 AM Venue: Seminar Hall COLLEGE OF ENGINEERING CHERTHALA PALLIPPURAM P.O., CHERTHALA-688 541, KERALA www.cectl.ac.in Phone: +91 478 2553416 1 Agenda Notes: X BOG 15th March 2016 2 Agenda Notes: X BOG 15th March 2016 Background The meeting of Board of Governors is convened to monitor the progress of TEQIP-II activities at CE Cherthala, under Sub component 1.1, with emphasis to procurement and academic activities, and to accord necessary approvals and clearances for the ongoing activities. The 10th meeting of the BOG is being convened on 15th of March 2016. 3 Agenda Notes: X BOG 15th March 2016 4 Agenda Notes: X BOG 15th March 2016 AGENDA Part 1-Procedural Page Sl. No Items Number Confirming the Minutes of the 9th Meeting of the Board of Governors held on 9 1.1 03-12-2015 at College of Engineering Cherthala, Alappuzha Report on the action taken/action pending on the pertinent decisions in the 9 1.2 9th Meeting of the Board of Governors held on 03-12-2015 at College of Engineering Cherthala Part 2-Reports and Ratifications Page Sl. No Items Number 2.1 Procurement Completed after the 9th BOG meeting 15 2.2 Packages for which Purchase order has been issued. 16 2.3 In House Faculty and Staff Development Programmes conducted 16 2.4 Out Station Faculty and Staff Development Programmes 19 2.5 Conference attended/ Papers presented 21 2.6 IIIC Programme -

Managementvoice (A Thrissur Management Association Publication)

Volume 6 Issue 12/ 2015 managementVoice (A Thrissur Management Association Publication) Dr.A. Kowsigan, Dist. Collector, Thrissur Mr. T.S. Pattabhiraman, Chairman & MD, Kalyan Silks Celebrating AIMA’s Best LMA Award TMA Honours its Past President and Secretary Lulu International Convention Centre, November 17, 2015 Thrissur Management Association (Only for private circulation) What’s Inside EDITORIAL BOARD Ranjan Sreedharan From the Editor: Management Voice turns the corner ...................... 4 “In this issue we are carrying five original contributions from our members (Chief Editor) which is something of a record as far as the history of Management Voice is concerned.” Dr. Krishnamurthy P.S. President’s Message: ...................................................................... 5 Dr. V. M. Manoharan “AIMA has agreed to conduct a mega programme “Shaping of Young Minds” which will bring prominent faculties from various parts of the country to address the students.” OFFICE BEARERS Secretary’s Report .............................................................................. 7 President: CA V. Venugopal Policy: Goods and Services Tax (GST) and its Benefits ........................... 11 Goods and Services Tax (GST) is a broad based and a single comprehensive tax Hon. Secretary: Er. Vinod Manjila levied on goods and services consumed in an economy. It is basically a tax on final consumption. Hon. Treasurer: Er. Col. Prathap Chandran Economy Class: Making Sense of Conflicting Economic Signals .... 13 Economic news coming from different sources is baffling the layman and the expert Sr. Vice Pres.: Er. Anand Menon alike. Reports of international organizations like the IMF, the World Bank, OECD etc. indicate that India is presently the fastest growing economy in the world. But the corporate top lines and bottom lines do not reflect this benign picture.