Israel Equity 2020 Review & 2021 Outlook

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Emerging Markets Investment Universe by Jan Dehn and Joana Arthur

THE EMERGING VIEW August 2015 The Emerging Markets investment universe By Jan Dehn and Joana Arthur This is the fourth annual review of the Emerging Markets (EM) investment universe. We provide an overview of tradable debt and domestic credit markets in 54 EM countries as well as the large cap, small cap and Frontier Markets for equities. We compare debt statistics with similar metrics for developed economies to place EM in the global context. We highlight trends and discuss EM indices, the effect of regulation and USD strength, the rise of corporate bond markets, the likely implications of Fed hikes and other relevant aspects. We look towards the horizon of fixed income markets, including the growing Sukuk universe, the opening of China’s bond market, etc. We also peer into the future of EM equity markets, including the opening of markets in China, Saudi Arabia and Iran. Size and structure of global fixed income and EM countries now account for 57% of global GDP domestic credit1 As of the end of 2014, global tradable debt and domestic private on a purchasing power parity basis, but only sector credit was USD 197trn, or 255% of global GDP. Global around 20% of total debt and credit domestic credit to the private sector stood at USD 84trn, while global tradable debt was USD 113trn. The tradable EM debt universe Emerging Markets (EM) countries account for about 13% of the world’s tradable debt (USD 14.8trn) and 31% of the global The tradable EM corporate debt universe is now exactly the domestic credit to the private sector (USD 26trn). -

Investing in Emerging and Frontier Markets – an Investor Viewpoint

Contents Acknowledgements .............................................................................................................................................................................1 1. Executive Summary ........................................................................................................................................................................2 2. Introduction ........................................................................................................................................................................................3 3. Overview of Foreign Investor Activity ...................................................................................................................................4 4. Methodology ......................................................................................................................................................................................9 5. Discussion of interview findings ........................................................................................................................................... 13 Reference list .......................................................................................................................................................................................26 Investing in Emerging and Frontier Markets – An Investor Viewpoint Acknowledgements This research was only possible because of the willingness of investors to be interviewed for this report and to speak openly with -

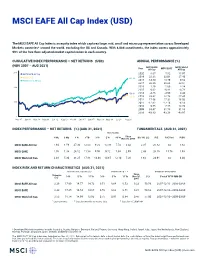

MSCI EAFE All Cap Index (USD)

MSCI EAFE All Cap Index (USD) The MSCI EAFE All Cap Index is an equity index which captures large, mid, small and micro cap representation across Developed Markets countries* around the world, excluding the US and Canada. With 8,088 constituents, the index covers approximately 99% of the free float-adjusted market capitalization in each country. CUMULATIVE INDEX PERFORMANCE — NET RETURNS (USD) ANNUAL PERFORMANCE (%) (NOV 2007 – AUG 2021) MSCI EAFE MSCI World Year All Cap MSCI EAFE All Cap 300 MSCI EAFE All Cap 2020 8.67 7.82 15.97 2019 22.38 22.01 27.40 MSCI EAFE 262.28 MSCI World All Cap 2018 -14.50 -13.79 -9.52 2017 26.35 25.03 22.51 200 2016 1.29 1.00 8.24 2015 0.62 -0.81 -0.78 158.80 2014 -4.86 -4.90 4.44 149.91 2013 23.62 22.78 27.45 2012 17.56 17.32 16.03 100 2011 -12.62 -12.14 -6.13 2010 9.55 7.75 13.74 2009 33.47 31.78 31.83 2008 -43.83 -43.38 -40.97 0 Nov 07 Jan 09 Mar 10 May 11 Jun 12 Aug 13 Oct 14 Dec 15 Jan 17 Mar 18 May 19 Jul 20 Aug 21 INDEX PERFORMANCE — NET RETURNS (%) (AUG 31, 2021) FUNDAMENTALS (AUG 31, 2021) ANNUALIZED Since 1 Mo 3 Mo 1 Yr YTD 3 Yr 5 Yr 10 Yr Nov 30, 2007 Div Yld (%) P/E P/E Fwd P/BV MSCI EAFE All Cap 1.94 1.59 27.30 12.03 9.20 10.09 7.74 3.42 2.35 20.82 na 1.82 MSCI EAFE 1.76 1.38 26.12 11.58 9.00 9.72 7.34 2.99 2.43 20.10 15.76 1.93 MSCI World All Cap 2.48 5.30 31.25 17.81 14.48 14.65 12.10 7.26 1.64 24.91 na 3.04 INDEX RISK AND RETURN CHARACTERISTICS (AUG 31, 2021) ANNUALIZED STD DEV (%) 2 SHARPE RATIO 2 , 3 MAXIMUM DRAWDOWN Turnover Since 1 3 Yr 5 Yr 10 Yr 3 Yr 5 Yr 10 Yr Nov 30, (%) Period YYYY-MM-DD -

Client Demand for Sustainable Investing Is Growing

Client demand for sustainable investing is growing Assets in US sustainable funds reached $231 billion by the end of 2020, up from $139 billion at the end of 2019 — a roughly 66% increase.1 In fact, 85% of all individual investors, including 95% of millennials, have expressed an interest in sustainable investing.2 When your clients and prospects ask you about sustainable investing, will you be prepared to have the conversation? INVESTING IN A MORE SUSTAINABLE ECONOMY We believe that capital markets will be shaped We seek to invest in companies that are profoundly by global sustainability challenges well-positioned to benefit from this transition including climate change, environmental to a more sustainable global economy, which pollution, natural resource constraints and is why we integrate environmental, social human capital issues such as diversity, inclusion ESG and governance (ESG) factors across all and gender equity. We expect these trends will drive growth our strategies. In-depth ESG analysis helps for well-positioned companies and create risks for those unable us understand a company’s quality and character, which we or unwilling to adapt. believe enhances our investment decisions. INTEGRATING ESG CRITERIA INTO FINANCIAL ANALYSIS CAN HELP ENHANCE RETURNS US INTERNATIONAL DEVELOPED EMERGING MARKETS 15.00 8.00 12.00 7.02 7.00 9.52 6.29 10.00 12.00 11.37 10.85 6.00 8.00 7.07 9.00 5.00 4.00 6.00 6.00 3.00 4.00 2.00 Annualized Return (%) Return Annualized 3.00 (%) Return Annualized (%) Return Annualized 2.00 1.00 0.00 0.00 0.00 (Annualized return: 5/1/90 to 6/30/21) (Annualized return: 10/1/07 to 6/30/21) (Annualized return: 6/6/13 to 6/30/21) MSCI KLD 400 Social Index MSCI EAFE ESG Leaders Index MSCI Emerging Markets ESG Leaders Index S&P 500 Index MSCI EAFE Index MSCI Emerging Markets Index Data as of 6/30/2021 Investing involves risk, including the loss of principal. -

Developed Markets Outlook 2021

Uncertain recovery Developed markets outlook 2021 Investment Outlook TLIM Due to the COVID-19-related lockdown measures, 2020 will go into the record books as the year that saw the deepest global recession in peacetime. For 2021, we expect global economic activity to rebound, although the recovery will likely be slow amidst recurring restrictive measures. Pre-pandemic activity levels can only be reached once a vaccine has become widely available. Despite positive vaccine trial results, we don’t expect this to happen before the final quarter of 2021. In the meantime, further stimulus will be needed. Bold policy choices need to be made so that the recovery can become sustainable and inclusive. This could be a vital first step towards a new economic system, one that is equipped to address the challenges of our time: climate change, biodiversity loss and inequality. Developed Markets Outlook 2021 An uncertain recovery: divided US suits the global status quo Joeri de Wilde The US is still the largest economy in the world, with Global economy: growth rebound with unable to reach pre-pandemic activity levels before This trend may very well to continue in 2021, a worrying over 24% of global GDP. The change of leadership in much uncertainty the final quarter of 2021, when a substantial part of realisation. Washington could, in theory, be the spark that ignites their citizens have been vaccinated. In our outlook the much-needed global reset of our economic system. In 2020, we project global economic activity to for 2020, we warned about the ultra-loose global For 2021, we expect global economic activity to President-elect Joe Biden wants the US to ‘lead the contract by an astonishing 4.1%. -

The New Neutral: the Long-Term Case for Currency Hedging

Robert Bush Thought Leadership Xpert Insights 12/17 The New Neutral—The long-term case for currency hedging It’s fair to say that currency-hedged approaches to The Long Term Case for Currency Hedging) and international investing have really come to the fore consider the more strategic reasons for hedging, and, over the last few years, with $14.8 billion of AUM in in particular, the potential risk reduction it offers. hedged ETFs at the beginning of 2014, compared with “$41bn of AUM as of the end of November Take a look at Figure 1, which reflects the difference 2017” (Source: Morningstar). Without asking every in volatility for the MSCI EAFE, a key benchmark single investor’s motivation, it’s impossible to say for international developed equity markets, on a exactly what the driving force behind this interest hedged (without currency) and an un-hedged (with has been, but we suspect the strong performance currency) basis. A positive number represents more of the dollar, particularly against the euro and the risk in the basket that includes currency. What was yen, where quantitative easing has weakened those surprising, to us at least, was that over this time currencies, has really shone a spotlight on the role period leaving currency in resulted in volatility on currencies can play in an international investment. average 2.7 percentage points higher 90% of the time. It really begs the question—why? What is it Instead of focusing on the tactical, return-oriented about currency—and, by the way, it’s not, in our aspects of the hedging decision, let’s focus on some view, additional return—that meant investors lost key findings from research we’ve recently undertaken out by retaining their exposure? (see our latest White Paper The New Neutral: Figure 1: The difference in volatility between MSCI EAFE hedged and un-hedged (2/1978–2/2017) 8.00 6.00 4.00 2.00 0.00 –2.00 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2017 Source: Morningstar Direct, 3/31/1973–11/30/17. -

Notice of Filing of Proposed Rule Change to List and Trade Options on the MSCI EAFE Index and on the MSCI Emerging Markets Index

SECURITIES AND EXCHANGE COMMISSION (Release No. 34-74430; File No. SR-CBOE-2015-023) March 4, 2015 Self-Regulatory Organizations; Chicago Board Options Exchange, Incorporated; Notice of Filing of Proposed Rule Change to List and Trade Options on the MSCI EAFE Index and on the MSCI Emerging Markets Index Pursuant to Section 19(b)(1) of the Securities Exchange Act of 1934 (the “Act” or “Exchange Act”),1 and Rule 19b-4 thereunder,2 notice is hereby given that on February 26, 2015, the Chicago Board Options Exchange, Incorporated (the “Exchange” or “CBOE”) filed with the Securities and Exchange Commission (the “Commission”) the proposed rule change as described in Items I, II, and III below, which Items have been prepared by the Exchange. The Commission is publishing this notice to solicit comments on the proposed rule change from interested persons. I. Self-Regulatory Organization’s Statement of the Terms of Substance of the Proposed Rule Change CBOE proposes to list and trade options that overlie the MSCI EAFE Index and the MSCI Emerging Markets Index (“EAFE options” and “EM options”). EAFE and EM options would be P.M., cash-settled contracts with European-style exercise. The text of the proposed rule change is available on the Exchange’s Web site (http://www.cboe.com/AboutCBOE/CBOELegal RegulatoryHome.aspx), at the Exchange’s Office of the Secretary, and at the Commission. II. Self-Regulatory Organization’s Statement of the Purpose of, and Statutory Basis for, the Proposed Rule Change In its filing with the Commission, the self-regulatory organization included statements concerning the purpose of and basis for the proposed rule change and discussed any comments it 1 15 U.S.C. -

Product Commentary CLEARBRIDGE INTERNATIONAL GROWTH FUND

2Q 2021 Product Commentary CLEARBRIDGE INTERNATIONAL GROWTH FUND Elisa Mazen, Michael Testorf, CFA, Pawel Wroblewski, CFA and Thor Olsson Portfolio Managers Average annual total returns and fund expenses (%) Key takeaways as of June 30, 2021 • Recent Fund outperformance has been broad- based, led by more defensive, secular growth Since Incept. Expenses companies, with structural and emerging growth Class A 3-mo 1-yr 5-yr 10-yr (02/03/09) Gross Net holdings also contributing. Excluding sales 6.77 29.06 16.17 11.55 14.43 1.10 1.06 charges • Banks and energy are two areas we have mostly Including effects avoided, but our valuation approach to growth of maximum 0.62 21.64 14.80 10.89 13.88 1.10 1.06 helped identify two European banks and a global sales charges oil services provider in the quarter whose MSCI EAFE (Net) 5.17 32.35 10.28 5.89 N/A - - risk/reward were too attractive to overlook. (USD) Performance shown represents past performance and is no guarantee of future • International equity markets have seen rotating results. Current performance may be higher or lower than the performance shown. leadership due to various factors, such as the Investment return and principal value will fluctuate so shares, when redeemed, may be likelihood of interest rate increases and differing worth more or less than the original cost. Class A shares have a maximum front-end sales charge of 5.75%. Total returns assume the reinvestment of all distributions at net asset monetary policies, moves creating short-term value and the deduction of all Fund expenses. -

S&P Dow Jones Indices' 2020 Country Classification Consultation

CONSULTATION S&P Dow Jones Indices’ 2020 Country Classification Consultation NEW YORK, AUGUST 19, 2020: S&P Dow Jones Indices (“S&P DJI”) is conducting its annual country classification consultation with market participants. S&P DJI’s global equity indices are divided into three major country classifications – developed, emerging, and frontier. Certain countries do not fall into one of these three categories and are considered “stand-alone” countries for index construction purposes. A number of factors are used in determining each country’s classification, both quantitative and qualitative in nature. Additionally, the opinions and experiences of institutional investors are critically important in determining whether a market should be classified as developed, emerging, or frontier. In that regard, S&P DJI is seeking feedback on the countries and markets covered by this consultation. Your participation in this consultation is important as we gather information from various market participants in order to properly evaluate your views and preferences. Please respond to this survey by October 15, 2020. After this date, S&P DJI will no longer accept survey responses. Prior to the Index Committee’s final review, S&P DJI may request clarifications from respondents as part of that review. To participate in this consultation, please visit the online survey available here. For further information about this consultation, please contact S&P Dow Jones Indices at [email protected]. Please be advised that all comments from this consultation will be reviewed and considered before a final decision is made; however, S&P DJI makes no guarantees or is under any obligation to comply with any of the responses. -

A Vision for the Development of the Luxembourg Financial Centre Contents

LUXFIN A VISION FOR THE DEVELOPMENT OF THE LUXEMBOURG FINANCIAL CENTRE CONTENTS Foreword by Pierre Gramegna, Minister of Finance 2 Executive Summary 4 01 Luxembourg’s development as a leading financial centre 6 02 The Luxembourg and European financial services industries 16 03 Core growth ambitions for the Luxembourg financial centre 04 26 Luxembourg’s growth enablers 34 05 Growth plans and potential in each sector of the financial centre 41 2 FOREWORD Foreword Over the course of the last three decades, Luxembourg has been able to build a financial industry which is uniquely specialized in cross-border activities. This is a common feature throughout the entire range of services provided in Luxembourg, whether Pierre Gramegna, in investment funds, wealth management, capital market Minister of Finance operations or advisory services. Enabling investors to connect November 2015 with different markets has become our trade. The success of the Luxembourg financial industry has not only benefited Luxembourg but Europe more generally. Luxembourg’s leading position in the investment fund area is foremost a success story of a European investment product, the UCITS. The assets raised in the fund industry through Luxembourg are assets that benefit companies all over Europe as they are being reinvested in various countries and help finance economic activity. Luxembourg’s expertise plays the role of enabler of this investment. Luxembourg has grown economically with the completion of the Single Market of the European Union where goods, people, services and capital can move freely. This Single Market has spurred trade and thus ensured growth. It is imperative not only to preserve it but also to continue to work for its completion. -

MSCI EAFE ESG Screened Index (USD)

MSCI EAFE ESG Screened Index (USD) The MSCI EAFE ESG Screened Index is based on the MSCI EAFE Index, its parent index, and includes large and mid-cap securities across 21 Developed Markets (DM)* countries excluding the U.S and Canada. The index excludes companies from the parent index that are associated with controversial, civilian and nuclear weapons and tobacco, that derive revenues from thermal coal and oil sands extraction and that are not compliant with the United Nations Global Compact principles. CUMULATIVE INDEX PERFORMANCE — NET RETURNS (USD) ANNUAL PERFORMANCE (%) (MAY 2012 – AUG 2021) MSCI EAFE Year ESG Screened MSCI EAFE MSCI EAFE ESG Screened 2020 9.27 7.82 MSCI EAFE 2019 22.43 22.01 231.82 2018 -14.27 -13.79 225.67 2017 25.13 25.03 200 2016 0.09 1.00 2015 -0.04 -0.81 2014 -4.61 -4.90 2013 23.88 22.78 100 50 May 12 Mar 13 Dec 13 Sep 14 Jun 15 Apr 16 Jan 17 Oct 17 Jul 18 May 19 Feb 20 Nov 20 Aug 21 INDEX PERFORMANCE — NET RETURNS (%) (AUG 31, 2021) FUNDAMENTALS (AUG 31, 2021) ANNUALIZED Since 1 Mo 3 Mo 1 Yr YTD 3 Yr 5 Yr 10 Yr May 31, 2012 Div Yld (%) P/E P/E Fwd P/BV MSCI EAFE ESG Screened 2.06 1.57 25.94 11.49 9.44 9.86 na 9.51 2.30 20.23 16.30 1.95 MSCI EAFE 1.76 1.38 26.12 11.58 9.00 9.72 na 9.19 2.43 20.10 15.76 1.93 INDEX RISK AND RETURN CHARACTERISTICS (MAY 31, 2012 – AUG 31, 2021) ANNUALIZED STD DEV (%) 2 SHARPE RATIO 2 , 3 MAXIMUM DRAWDOWN TrackingTurnover Since Beta 1 3 Yr 5 Yr 10 Yr 3 Yr 5 Yr 10 Yr May 31, (%) Period YYYY-MM-DD Error (%) (%) 2012 MSCI EAFE ESG Screened 0.99 0.66 4.50 17.51 14.42 na 0.53 0.64 na 0.68 33.72 2018-01-25—2020-03-23 MSCI EAFE 1.00 0.00 2.32 17.65 14.54 na 0.50 0.62 na 0.66 34.12 2018-01-25—2020-03-23 1 Last 12 months 2 Based on monthly net returns data 3 Based on ICE LIBOR 1M *DM countries include: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the UK. -

INVESTING in JAPAN Japan’S Relevance to the Global Economy Japan Is an Established Global Economic Leader Across a Wide Variety of Measures

November 2020 White Paper INVESTING IN JAPAN Japan’s Relevance to the Global Economy Japan is an established global economic leader across a wide variety of measures. It is the third largest economy in the world, behind only the United States and China1. Known for its economic diversity and sophistication, Japan has consistently ranked as the most complex economy in the world by Harvard studies2. It is home to leading companies in both production and technological advancements across a variety of industries. In addition to being the fourth-largest exporter in the world3, Japan also has a strong domestic economy powered by the third largest consumer market in the world4. Across various measures, Japan is an economic power to be reckoned with. Figure 1: Japan’s Economic Rankings: 10 Largest 10 Largest by 2019 GDP 10 Largest by 2019 Exports of 10 Largest by 2019 Household (US$ trillion) Goods and Services (US$ trillion) Consumption (US$ trillion) US $21.4 China $2.6 United States $14.0 China $14.7 US $2.5 China $5.4 Japan $5.1 Germany $1.8 Japan $2.8 Germany $3.9 Japan $0.9 Germany $2.1 India $2.9 UK $0.9 United Kingdom $1.9 UK $2.8 France $0.9 India $1.6 France $2.7 Netherlands $0.8 France $1.5 Italy $2.0 Korea $0.7 Italy $1.3 Brazil $1.8 Hong Kong $0.6 Brazil $1.2 Canada $1.7 Singapore $0.6 Canada $1.0 Source: World Bank as of 2019 Source: IMF as of 2019 Source: World Bank as of 2019 The Japanese equity market is no less significant.