Dispute Management Guidelines for Visa Merchants Table of Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

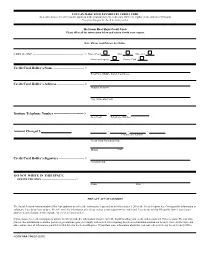

Form Ssa-714 (07-2005)

YOU CAN MAKE YOUR PAYMENT BY CREDIT CARD As a convenience, we offer you the option to make your payment by credit card. However, regular credit card rules will apply. You may also pay by check or money order. We Honor Most Major Credit Cards Please fill in all the information below and return it with your request. Note: Please read Privacy Act Notice CHECK ONE ---------------------------------------------- > MasterCard Visa Discover American Express Diners Card Credit Card Holder’s Name ---------------------------- > Print First, Middle Initial, Last Name Credit Card Holder’s Address ------------------------- > Number & Street City, State, Zip Code Daytime Telephone Number --------------------------- > - - Area Code Telephone Number Amount Charged $ - - - Credit Card Number Credit Card Expiration Date Month Year Credit Card Holder’s Signature ----------------------- > Authorization DO NOT WRITE IN THIS SPACE OFFICE USE ONLY --------------------------------------- > Name Date PRIVACY ACT STATEMENT The Social Security Administration (SSA) has authority to collect the information requested on this form under § 205 of the Social Security Act. Giving us this information is voluntary. You do not have to do it. We will need this information only if you choose to make payment by credit card. You do not need to fill out this form if you choose another means of payment (for example, by check or money order). If you choose the credit card payment option, we will provide the information you give us to the banks handling your credit card account and SSA’s account. We may also provide this information to another person or government agency to comply with federal laws requiring the release of information from our records. You can find these and other routine uses of information provided to SSA listed in the Federal Register. -

Helpful Tips to Reducing Disputes How to Manage Dispute Inquiries and Chargebacks Understanding Merchant Disputes & Chargebacks

Helpful Tips to Reducing Disputes How to manage Dispute Inquiries and Chargebacks Understanding Merchant Disputes & Chargebacks What’s Inside: American Express Dispute Process 2 How to Reduce Disputes 3 Frequently Asked Questions 5 Appendix 6 This guide is intended to provide you with general A Chargeback happens when American Express debits your guidance on how to manage Disputes inquiries and upfront account after a dispute is closed due to various reasons. An Chargebacks, information about your role in the process and example of some of the reasons could be: a Cardmember has recommendations to help you avoid Disputes. provided evidence of an unauthorized transaction, you do not reply to a dispute inquiry within the specified timeframe or the A Dispute happens when a Cardmember doesn’t recognize a response is insufficient. transaction, does not agree with the amount of the transaction, or wants additional information about the transaction. FOR MORE INFORMATION, VISIT AMERICANEXPRESS.CA/MERCHANTPOLICY OR CALL 1-800-268-9877 American Express Dispute Process A CARDMEMBER DISPUTES A CHARGE INQUIRY INQUIRY A notification you receive if a Cardmember disputes a charge American Express sends an Inquiry notice from your business and we cannot resolve it using the documents we have on file. SUBMIT DOCUMENTS We may request that you send supporting documents of the transaction. I.e.: Signed Record Of Charge (ROC); cancellation policy, terms and conditions, proof of Cardmember consent etc… CASE RESOLVED CHARGEBACK The case may be resolved in your favor A Chargeback will be processed if: your if you provide the appropriate supporting reply is insufficient; you do not reply on documents and information within the time; or you authorize us. -

Summary of Credit Terms- Union Bank® Cashback Rewards Visa® Card

Summary of Credit Terms- Union Bank® Cashback Rewards Visa® Card PLEASE NOTE: If you apply for the Union Bank Cashback Rewards Visa Card and meet our eligibility criteria for the Visa Signature® Card, you agree that we may consider your application as one for (and upgrade you to) the Union Bank Cashback Rewards Visa Signature Card. Interest Rates and Interest Charges Annual Percentage Rate Introductory APR for the first 12 months that your account is open. (APR) for Purchases 0.00% After that, your APR will be 13.99% to 23.99%, based on your creditworthiness. This APR will vary with the market based on the Prime Rate. APR for Balance Transfers 0.00% Introductory APR for the first 12 months that your account is open. After that, your APR will be 13.99% to 23.99%, based on your creditworthiness. This APR will vary with the market based on the Prime Rate. APR for Cash Advances 25.25%. This APR will vary with the market based on the Prime Rate. Penalty APR None Paying Interest Your due date is at least 21 calendar days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month. We will begin charging interest on cash advances and balance transfers on the transaction date. Minimum Interest Charge If you are charged interest, the charge will be no less than $1.75. For Credit Card Tips from To learn more about factors to consider when applying for or using a credit card, visit the the Consumer Financial website of the Consumer Financial Protection Bureau at Protection Bureau http://www.consumerfinance.gov/learnmore. -

Contactless Operating Mode Requirements Clarification Whitepaper

Contactless Operating Mode Requirements Clarification Whitepaper Version 1.0 Publication Date: February 2020 U.S. Payments Forum ©2020 Page 1 About the U.S. Payments Forum The U.S. Payments Forum, formerly the EMV Migration Forum, is a cross-industry body focused on supporting the introduction and implementation of EMV chip and other new and emerging technologies that protect the security of, and enhance opportunities for payment transactions within the United States. The Forum is the only non-profit organization whose membership includes the entire payments ecosystem, ensuring that all stakeholders have the opportunity to coordinate, cooperate on, and have a voice in the future of the U.S. payments industry. Additional information can be found at http://www.uspaymentsforum.org. EMV ® is a registered trademark in the U.S. and other countries and an unregistered trademark elsewhere. The EMV trademark is owned by EMVCo, LLC. Copyright ©2020 U.S. Payments Forum and Smart Card Alliance. All rights reserved. The U.S. Payments Forum has used best efforts to ensure, but cannot guarantee, that the information described in this document is accurate as of the publication date. The U.S. Payments Forum disclaims all warranties as to the accuracy, completeness or adequacy of information in this document. Comments or recommendations for edits or additions to this document should be submitted to: [email protected]. U.S. Payments Forum ©2020 Page 2 Table of Contents 1. Introduction .......................................................................................................................................... 4 2. Contactless Operating Modes ............................................................................................................... 5 2.1 Impact of Contactless Operating Mode on Debit Routing Options .............................................. 6 3. Contactless Issuance Requirements ..................................................................................................... 7 4. -

Check Card Agreement and Disclosure Statement

Notice of Customer Rights and Liabilities ASPIRATION CHECK CARD AGREEMENT AND DISCLOSURE STATEMENT Aspiration Financial, LLC (“Aspiration”) has arranged with Bank (defined below) for the issuance of Mastercard cards to the customers of Aspiration. When you use this Card, you will be accessing the Available to Withdraw balance in your Aspiration Cash Management Account. This Agreement is made among you, Aspiration and Bank and explains the types of Transactions that you can perform with your Mastercard Card (“Card”), as well as your rights and responsibilities concerning your usage and safekeeping of the Card. You agree to be legally bound by the terms and conditions set forth in this Agreement. IMPORTANT If you believe your Card or personal identification number (“PIN”) has been lost or stolen or has become known to unauthorized persons or that someone has used or may use your Card or PIN without your permission: Notify Aspiration by: Telephoning Aspiration at: 800-683-8529 or Writing Aspiration at: 4551 Glencoe Avenue, Marina Del Rey, CA 90292 For all other questions: Telephone or write Aspiration. 1. Definitions. Unless the context otherwise requires, the capitalized terms used in this Agreement have the meanings specified below: “Account” refers to your Aspiration Cash Management Account. Termination of your Account will result in the immediate termination of your Card. Your Card may be terminated by us without resulting in termination of your Account. “ATM” means automated teller machine. “ATM Withdrawal” means a Transaction in which you receive cash from an ATM. “Authorization” means a Transaction in which you authorize others to place a hold on your Available Balance to ensure future payment. -

Key Payment and Service Information What Is Paypal?

Key Payment and Service Information What is PayPal? • PayPal enables individuals and businesses to send electronic money online. It also provides other financial and non-financial services closely related to online payments. These services are collectively referred to hereafter as the “Service”. • PayPal does not provide credit and/or escrow services. • PayPal does not allow you to hold funds in your PayPal account. Who provides the Service? The Service is provided by PayPal (Europe) S.á r.l. & Cie, S.C.A. (also referred to as “PayPal” in this document) to registered users in the European Union (each a “User”). • PayPal (Europe) S.à r.l. & Cie, S.C.A. (R.C.S. Luxembourg B 118 349) is duly licensed as a Luxembourg credit institution in the sense of Article 2 of the law of 5 April 1993 on the financial sector as amended (the “Law”) and is under the prudential supervision of the Luxembourg supervisory authority, the Commission de Surveillance du Secteur Financier Opening a PayPal account • The Service allows individuals and businesses to open an account maintained byPayPal (an “account”). • To be eligible for an account, a User must: o either be an individual (at least 18 years old) or a business that is able to form a legally binding contract; and o have satisfactorily completed our sign-up process • As part of our sign-up process, a User: o must register an email address, which will also act as their ‘User ID’; o may submit details of the source(s) with which they wish to fund their PayPal account (e.g., details of the User’s credit card). -

Mastercard Debit Card Disputes

MASTERCARD DEBIT CARD DISPUTES Please follow this guide to help us process your Mastercard dispute promptly. Requirements for Processing Your Dispute We’ll begin our investigation based on the date we are notified of your disputed transaction(s). Mastercard requires that you attempt to resolve the dispute directly with the merchant before a dispute can be filed. You must provide documentation of your contact with the merchant before we can submit your request to Mastercard. Complete, sign, and return the Mastercard Cardholder Dispute Notification form to us. Select the statement on the form that best describes your dispute. Use the Additional Comments section to further explain the transaction and the nature of your dispute, or if none of the statements describe your dispute. Include any and all documentation to support your dispute when you return the form. Sending Required Documentation to BECU Please be sure your dispute is complete, thorough, and accurate before returning the Mastercard Cardholder Dispute Notification form and your supporting documentation to us. You can return the form and documentation by one of the following: Fax: 206.805.5663 Or mail to: P.O. Box 97050 Seattle, WA 98124-9750 Attn: Card Services What’s Next? We’ll initiate the dispute process with Mastercard once we have the required information (complete dispute form and supporting documentation). We’ll review your submission for completeness, and may request additional information as necessary. You must respond to requests for additional information during the Mastercard dispute process. Within 10 business days from the date we receive notification of your disputed transaction(s), we’ll either resolve your dispute, or issue a provisional credit to your account for the amount of the dispute while our investigation continues. -

Mastercard Frequently Asked Questions Platinum Class Credit Cards

Mastercard® Frequently Asked Questions Platinum Class Credit Cards How do I activate my Mastercard credit card? You can activate your card and select your Personal Identification Number (PIN) by calling 1-866-839-3492. For enhanced security, RBFCU credit cards are PIN-preferred and your PIN may be required to complete transactions at select merchants. After you activate your card, you can manage your account through your Online Banking account and/or the RBFCU Mobile app. You can: • View transactions • Enroll in paperless statements • Set up automatic payments • Request Balance Transfers and Cash Advances • Report a lost or stolen card • Dispute transactions Click here to learn more about managing your card online. How do I change my PIN? Over the phone by calling 1-866-297-3413. There may be situations when you are unable to set your PIN through the automated system. In this instance, please visit an RBFCU ATM to manually set your PIN. Can I use my card in my mobile wallet? Yes, our Mastercard credit cards are compatible with PayPal, Apple Pay®, Samsung Pay, FitbitPay™ and Garmin FitPay™. Click here for more information on mobile payments. You can also enroll in Mastercard Click to Pay which offers online, password-free checkout. You can learn more by clicking here. How do I add an authorized user? Please call our Member Service Center at 1-800-580-3300 to provide the necessary information in order to qualify an authorized user. All non-business Mastercard account authorized users must be members of the credit union. Click here to learn more about authorized users. -

Smart Cards Vs Mag Stripe Cards

Benefits of Smart Cards versus Magnetic Stripe Cards for Healthcare Applications Smart cards have significant benefits versus magnetic stripe (“mag stripe”) cards for healthcare applications. First, smart cards are highly secure and are used worldwide in applications where the security and privacy of information are critical requirements. • Smart cards embedded with microprocessors can encrypt and securely store information, protecting the patient’s personal health information. • Smart cards can allow access to stored information only to authorized users. For example, all or portions of the patient’s personal health information can be protected so that only authorized doctors, hospitals and medical staff can access it. The rules for accessing medical information can be enforced by the smart card, even when used offline. • Smart cards support strong authentication for accessing personal health information. Patients and providers can use smart health ID cards as a second factor when logging in to access information. In addition, smart cards support personal identification numbers and biometrics (e.g., a fingerprint) to further protect access. • Smart cards support digital signatures, which can be used to determine that the card was issued by a valid organization and that the data on the card has not been fraudulently altered since issuance. • Smart cards use secure chip technology and are designed and manufactured with features that help to deter counterfeiting and thwart tampering. • Smart cards can help to reduce healthcare fraud by providing strong identity authentication of patients and providers. The use of secure smart chip technology, encryption and other cryptography measures makes it extremely difficult for unauthorized users to access or use information on a smart card or to create duplicate cards. -

Your Guide to Managing Cardmember Disputes Online

Your guide to managing Cardmember disputes online GUIDEAMERICANEXPRESS.COM.HK/MERCHANT How to manage your Cardmember disputes online This guide will give you a general overview about Cardmember disputes, This guide explains: followed by guidance on how to manage your American Express Cardmember disputes online. It will allow you to find your way around the site and locate Cardmember dispute background and resolution process 3 the information you need in order to take the actions you want. Logging in and enrolling in Cardmember disputes 4 Your summary view 5 The Cardmember disputes summary table 6 Filtering the Cardmember disputes summary table 7 Filtering by location and date 8 Customising the Cardmember disputes summary table 9 Getting the details of a case 10 Searching, downloading and printing reports 11 Taking action 12 - 13 Responding to multiple Cardmember disputes at once 14 Checking your email for notifications 15 Your guide to managing Cardmember disputes online 2 The benefits of managing Cardmember disputes online Managing and responding to Cardmember disputes is made easy with the online disputes tool available on the Merchant website. Online disputes Cardmember questions Cardmember dispute allows you to see all open and urgent Cardmember disputes for your a charge business locations with the ability to upload documents and respond American Express informs you via online. After attempting to resolve in-house, American Express requires additional email of a new or urgent Cardmember information from Merchant. query. You can review the case Why resolve Cardmember disputes online? information online. Managing Cardmember disputes online is quicker and can also help you avoid ‘no-reply’ chargebacks. -

Privilege Agreement

MERCHANT AGREEMENT THIS MERCHANT AGREEMENT is executed at Mumbai on the Effective Date as mentioned herein TABLE 1: Sr. Particulars Details No. 1. Agreement Execution and Effective date 2. Merchant Name 3. Merchant Address 4. Merchant Business filing Status 5. Merchant Site (URL) & Product/ Service Description 6. Product / Service 7. PAYMENT INSTRUCTIONS: The Merchant hereby instructs the Service Provider to make payment of Customer Charge in respect of a Customer Order in the bank account details mentioned in the Cheque/ Bank Statement provided by the Merchant. The Merchant agrees to pay the TDR and other charges as per the selected Pricing Scheme, the details of the TDR are mentioned in Annexure A hereto. Payment Schedule: The Merchant will receive the Customer Charges on a Td + 1 business day/Weekly basis. The TDR and the payment schedule may be revised by the Service Provider in accordance with the regulatory policies or as agreed between the Service Provider and Merchant from time to time. Any change in TDR and payment schedule due to mandates of Reserve Bank of India or Facility providers or Service Provider’s business promotion schemes shall be informed by the Service Provider to the Merchant and such change shall deemed to be accepted by the Merchant, if no written communication of non-acceptance of change is received from Merchant within 7 days of such intimation of change. By Signing this Agreement I/we/ the Merchant state that: I/ We have read and understood the Terms and Conditions as mentioned in the following Agreement. We agree that the payment gateway services of Infibeam Avenues Limited shall be govern by this Agreement and the same shall be legally binding on Merchant. -

Retrieval & Chargeback Best Practices Visa Mastercard Discover

Retrieval & Chargeback Best Practices A Merchant User Guide to Help Manage Disputes Visa MasterCard Discover American Express October 2015 www.FirstData.com Dispute Management Guide This guide is provided as a courtesy and is to be used for general information purposes only. First Data shall not be responsible for any inaccurate or incomplete information. The matters contained herein are subject to change. Individual circumstances may vary and procedures may be amended or supplemented as appropriate. This is not intended to be a complete listing of all applicable guidelines and/or procedures. No information contained herein alters any existing contractual obligations between First Data and its clients. The purpose of this guide is to provide merchants and their back office staff with additional educational guidance as it relates to Visa and MasterCard dispute processing. This manual contains information that relates to specific industry processing environments and includes best practices for doing business and avoiding loss as it relates to fraud and/or chargebacks. This guide does not take away from the terms or conditions outlined in your merchant processing agreement or replace current operation regulations. All chargeback’s should be reviewed and presented as individual cases. Although the reason codes may be the same, supporting documentation required to remedy individual chargeback scenarios may vary. © 2015 First Data Corporation. All Rights Reserved. All trademarks, service marks and trade names referenced in this material are the property of their respective owners. This document contains confidential and proprietary information of First Data Corporation. Review or distribution by individuals other than the intended recipients is strictly prohibited.