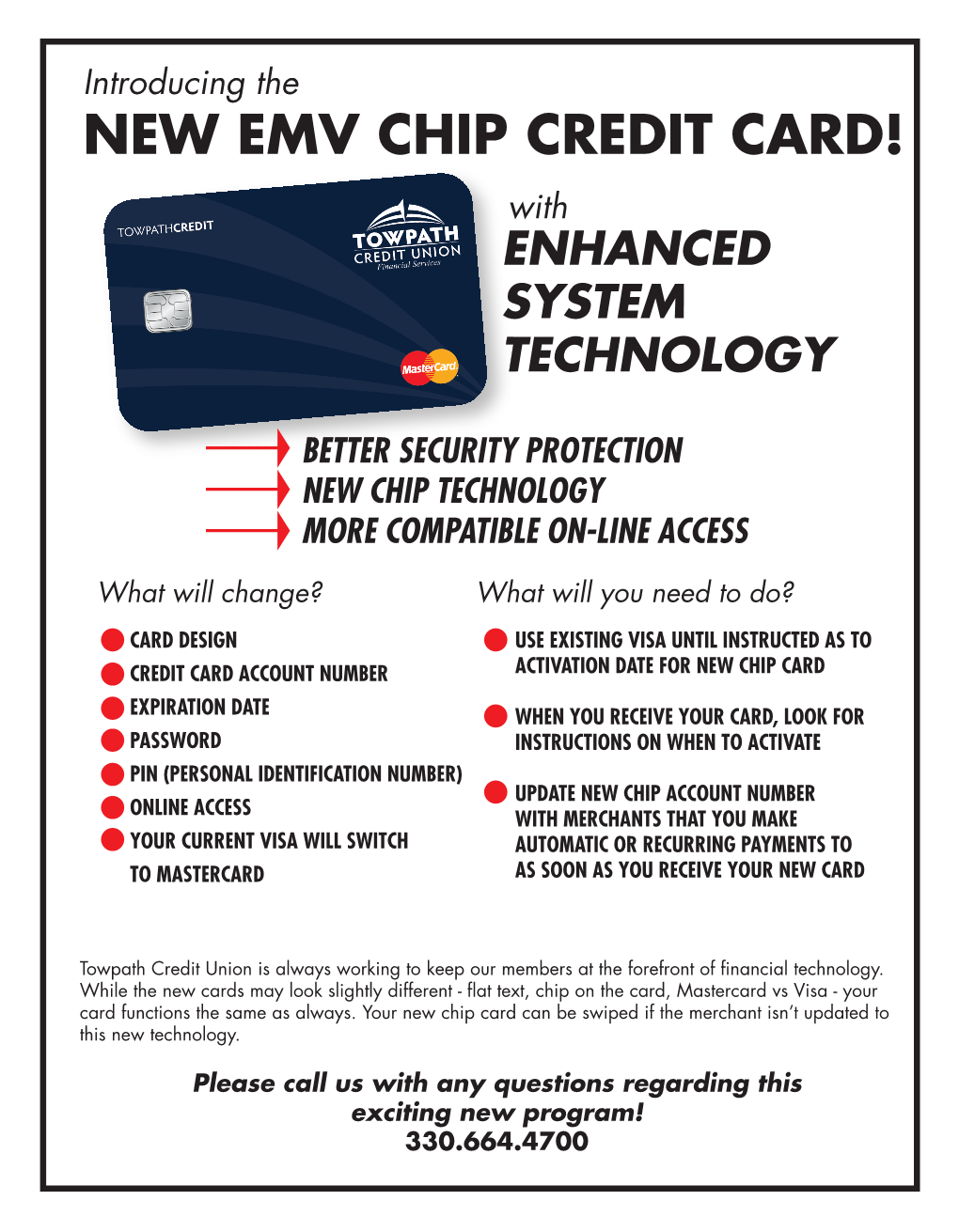

NEW EMV CHIP CREDIT CARD! with ENHANCED SYSTEM TECHNOLOGY

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Milesaway Business Card

BUSINESS CARD 14001 University Avenue • Clive, Iowa 50325-8258 Toll-free 1-888-400-5711 • Fax 1-800-704-9416 Cardholder Agreement Revised May 2020 This Cardholder Agreement (“Agreement”) and the application you signed or otherwise submitted (collectively, the “Cardholder Documents”) govern the use of your MilesAway MasterCard credit card account (“Account”) with us. The word “Card” means one or more cards or other access devices, such as account numbers, that we have issued to you to permit you to obtain credit under this Agreement. Your signature (including any electronic or digital signature) on your Card, on any application, on any accepted sales slip, or on any other document you sign in connection with the use of your Card or your Account is part of and incorporated into this Agreement. Please read and keep the Cardholder Documents for your records. In this Agreement and in your monthly Periodic Statement (as defned below), the words “you”, “your” and “yours” mean all persons responsible for complying with this Agreement, including but not limited to, the person who applied for the Account and the person to whom we address the periodic Statements, as well as any person who you authorize to use the Account. The words “we”, “us” and “our” refer to NCMIC Finance Corporation, an Iowa Corporation. 1. USE OF ACCOUNT. YOU AGREE TO USE THE ACCOUNT AND CARD(S) ISSUED FOR THE ACCOUNT TO MAKE PURCHASES OR LEASE GOODS OR SERVICES FOR COMMERCIAL OR BUSINESS PURPOSES ONLY (AND NOT FOR PERSONAL, FAMILY OR HOUSEHOLD USE) from any person who accepts the Card(s) (“Purchases”). -

Consumer Credit Card Disclosure Effective October 1, 2017

Consumer Credit Card Disclosure Effective October 1, 2017 VISA Platinum Tier I, Tier II, Tier III, Student VISA Free CU Rewards • No Annual Fee Important information about your credit card contract & your billing rights KEEP THIS NOTICE FOR FUTURE USE Visa Credit Card AGREEMENT & REGULATIONS These regulations are effective October 1, 2017, and are subject to change. In these regulations the words “you” and “your” mean each and all of those who applied for the card. “Card” means your VISA credit card issued by Altra Federal Credit Union. “We,” “us,” and “our” means Altra Federal Credit Union. 1. Responsibility. If you apply for and receive a personal card from us, you agree to these regulations and you agree to maintain membership in good standing at Altra Federal Credit Union. You agree to use the card for personal charges. You also agree to repay all debts, advances, and any Finance Charge or any other fees or charges arising from the use of the card and the card account. For example, you are responsible for charges made by yourself, your spouse, and minor children. You are also responsible for charges made by anyone else to whom you give the card, and this responsibility continues until you recover and return the card to us. Except to the extent allowed by law, you cannot disclaim responsibility by notifying us. Your responsibility continues even though an agreement, divorce decree, or other court judgment which we are not a party to may direct you or one of the other persons responsible to pay the account. Any person using the card shall be jointly responsible with you for charges he or she makes, and if that person signs the application and receives a copy of these regulations, he or she is also responsible for all charges on the account, including yours. -

Citadel Cash Rewards Mastercard® Agreements & Disclosures

Citadel Cash Rewards MasterCard® Agreements & Disclosures Interest Rates and Interest Charges Annual Percentage Rate (APR) for 11.74-17.99% based upon your creditworthiness. Purchases The APR will vary with the market based on the Prime Rate. APR for Balance Transfers and for Cash 11.74-17.99% based upon your creditworthiness. Advances The APR will vary with the market based on the Prime Rate. How to Avoid Paying Interest Your due date is 25 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month. Interest is charged on cash advances and balance transfers from the date the advance is made. For Credit Card Tips From The To learn more about factors to consider when applying for or using a credit card, visit the Federal Reserve Board website of the Federal Reserve Board at http://www.federalreserve.gov/creditcard Fees Transaction Fees Cash Advance Fee 3% of amount advanced ($10 minimum, $100 maximum) Foreign Transaction Fee 1.1% of transaction amount in U.S. dollars. Penalty Fees Late Fee $25.00 Returned Check Fee $25.00 How We Will Calculate Your Balance: We use a method called the “Average Daily Balance (including new purchases).” Billing Rights: Information on your rights to dispute transactions and how to exercise those rights is provided in your account agreement. The information about the costs of the card described is accurate as of 4/17. This information may have changed after that date. To find out what may have changed, call us at (800) 666-0191. -

AUTOMATED TELLER MACHINE (Athl) NETWORK EVOLUTION in AMERICAN RETAIL BANKING: WHAT DRIVES IT?

AUTOMATED TELLER MACHINE (AThl) NETWORK EVOLUTION IN AMERICAN RETAIL BANKING: WHAT DRIVES IT? Robert J. Kauffiiian Leollard N.Stern School of Busivless New 'r'osk Universit,y Re\\. %sk, Net.\' York 10003 Mary Beth Tlieisen J,eorr;~rd n'. Stcr~iSchool of B~~sincss New \'orl; University New York, NY 10006 C'e~~terfor Rcseai.clt 011 Irlfor~i~ntion Systclns lnfoornlation Systen~sI)epar%ment 1,eojrarcl K.Stelm Sclrool of' Busir~ess New York ITuiversity Working Paper Series STERN IS-91-2 Center for Digital Economy Research Stem School of Business Working Paper IS-91-02 Center for Digital Economy Research Stem School of Business IVorking Paper IS-91-02 AUTOMATED TELLER MACHINE (ATM) NETWORK EVOLUTION IN AMERICAN RETAIL BANKING: WHAT DRIVES IT? ABSTRACT The organization of automated teller machine (ATM) and electronic banking services in the United States has undergone significant structural changes in the past two or three years that raise questions about the long term prospects for the retail banking industry, the nature of network competition, ATM service pricing, and what role ATMs will play in the development of an interstate banking system. In this paper we investigate ways that banks use ATM services and membership in ATM networks as strategic marketing tools. We also examine how the changes in the size, number, and ownership of ATM networks (from banks or groups of banks to independent operators) have impacted the structure of ATM deployment in the retail banking industry. Finally, we consider how movement toward market saturation is changing how the public values electronic banking services, and what this means for bankers. -

EMF Implementing EMV at The

Implementing EMV®at the ATM: Requirements and Recommendations for the U.S. ATM Community Version 2.0 Date: June 2015 Implementing EMV at the ATM: Requirements and Recommendations for the U.S. ATM Community About the EMV Migration Forum The EMV Migration Forum is a cross-industry body focused on supporting the EMV implementation steps required for global and regional payment networks, issuers, processors, merchants, and consumers to help ensure a successful introduction of more secure EMV chip technology in the United States. The focus of the Forum is to address topics that require some level of industry cooperation and/or coordination to migrate successfully to EMV technology in the United States. For more information on the EMV Migration Forum, please visit http://www.emv- connection.com/emv-migration-forum/. EMV is a trademark owned by EMVCo LLC. Copyright ©2015 EMV Migration Forum and Smart Card Alliance. All rights reserved. The EMV Migration Forum has used best efforts to ensure, but cannot guarantee, that the information described in this document is accurate as of the publication date. The EMV Migration Forum disclaims all warranties as to the accuracy, completeness or adequacy of information in this document. Comments or recommendations for edits or additions to this document should be submitted to: ATM- [email protected]. __________________________________________________________________________________ Page 2 Implementing EMV at the ATM: Requirements and Recommendations for the U.S. ATM Community TABLE OF CONTENTS -

Mastercard Frequently Asked Questions Platinum Class Credit Cards

Mastercard® Frequently Asked Questions Platinum Class Credit Cards How do I activate my Mastercard credit card? You can activate your card and select your Personal Identification Number (PIN) by calling 1-866-839-3492. For enhanced security, RBFCU credit cards are PIN-preferred and your PIN may be required to complete transactions at select merchants. After you activate your card, you can manage your account through your Online Banking account and/or the RBFCU Mobile app. You can: • View transactions • Enroll in paperless statements • Set up automatic payments • Request Balance Transfers and Cash Advances • Report a lost or stolen card • Dispute transactions Click here to learn more about managing your card online. How do I change my PIN? Over the phone by calling 1-866-297-3413. There may be situations when you are unable to set your PIN through the automated system. In this instance, please visit an RBFCU ATM to manually set your PIN. Can I use my card in my mobile wallet? Yes, our Mastercard credit cards are compatible with PayPal, Apple Pay®, Samsung Pay, FitbitPay™ and Garmin FitPay™. Click here for more information on mobile payments. You can also enroll in Mastercard Click to Pay which offers online, password-free checkout. You can learn more by clicking here. How do I add an authorized user? Please call our Member Service Center at 1-800-580-3300 to provide the necessary information in order to qualify an authorized user. All non-business Mastercard account authorized users must be members of the credit union. Click here to learn more about authorized users. -

TENDER DOCUMENT for Switching Services & RUPAY Card Functioning in up Cooperative Bank Ltd

TENDER DOCUMENT' for Switching services and RUPAY card functioning TENDER DOCUMENT FOR Switching Services & RUPAY Card functioning in UP Cooperative Bank Ltd. Tender Document No: COOP BANK/ THE INFORMATION PROVIDED BY THE BIDDERS IN RESPONSE TO THIS TENDER DOCUMENT WILL BECOME THE PROPERTY OF UTTAR PRADESH COOPERATIVE BANK LTD. () AND WILL NOT BE RETURNED. RESERVES THE RIGHT TO AMEND, RESCIND OR REISSUE THIS TENDER DOCUMENT AND ALL AMENDMENTS WILL BE ADVISED TO THE BIDDERS AND SUCH AMENDMENTS WILL BE BINDING ON THEM. (THIS DOCUMENT SHOULD NOT BE REUSED OR COPIED OR USED EITHER PARTIALLY OR FULLY IN ANY FORM) Page 1 of 33 TENDER DOCUMENT' for Switching services and RUPAY card functioning ‘TENDER DOCUMENT’ for selection of ATM / EFT switch vendor Critical Information Summary 1) The TENDER DOCUMENT is posted on website www.upcbl.in. UPCB reserves the right to change the vendor requirements. However, any such changes will be posted on web site. 2) Bidders are advised to study the tender document carefully. Submission of bids shall be deemed to have been done after careful study and examination of the tender document with full understanding of its implications. 3) Any clarifications from bidder or any change in requirement will be posted on UPCB website. Hence before submitting bids, bidder must ensure that such clarifications / changes have been considered by them. UPCB will not have any responsibility in case some omission is done by any bidder. 4) In case of any clarification required by UPCB to assist in the examination, evaluation and comparison of bids, UPCB may, at its discretion, ask the bidder for clarification. -

Chapter 1 Introduction

CHAPTER 1 INTRODUCTION Globally, banking system is working continuously from many years. Paper money or cash has been leading payment mechanism worldwide for the centuries. The measure works of a bank to deposits an amount of a customer and returns it to him when he needs. During deposits and withdrawal of the amount bank may use this money for itself as to given loans to other customers who wants to avail it. There are so many types of loan like home loan, agricultural loan, personnel loan, loan for industries and business houses etc. Banks give a particular interest for the depositors on his money and take a certain interest from loan account holder. There are very fast changes occur in the traditional banking operation system. Before a decade ago a bank was involved only with customers when they were at premises of bank. But during this new time a bank provides many more services to the customer’s at their doorsteps. The entire system of banking has changed drastically. In banking system there are two most frequent and important services- one is to deposit cash in the account and second to withdraw cash from the account. Both the service provided to a customer during a time in which banks are open and officials present at that time. Here in this work our main concern is about the withdrawal service provided by the bank. Banks normally provide this cash through teller counters. Only in the past century paper money or cash faced competition from mainly cheques, debit and credit cards. Previously this whole process was thoroughly manual and nowadays it is automatic. -

Synchrony Bank Rates and Fees Table Gap Inc. Visa® Card Account Agreement Pricing Information

FR833282333_GAP INC. VISA® CREDIT CARD T&C-DC 19838E PDF 3/16 SYNCHRONY BANK RATES AND FEES TABLE GAP INC. VISA® CARD ACCOUNT AGREEMENT PRICING INFORMATION Interest Rates and Interest Charges Annual The APR for purchases is the prime rate plus 21.74% Percentage This APR will vary with the market based on the Prime Rate. Rate (APR) for Purchases APR for The APR for cash advances is the prime rate plus 23.74%. Cash Advances This APR will vary with the market based on the Prime Rate. Paying Interest Your due date is at least 23 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month. We will begin charging interest on cash advances on the transaction date. Minimum If you are charged interest, the charge will be no less than $1.50. Interest Charge Fees Transaction Fees • Cash Advance Either $10 or 4% of the amount of each cash advance, whichever is greater. • Foreign 3% of each transaction. Transaction Penalty Fees • Late Payment Up to $37 How We Will Calculate Your Balance: We use a method called “daily balance”. See your credit card account agreement below for more details. SECTION II: RATES, FEES AND PAYMENT INFORMATION GAP INC. VISA CARD ACCOUNT AGREEMENT How Interest is Calculated Your Interest We use a daily rate to calculate the interest on the balance on your account each day. The daily rate is the applicable APR times 1/365. Rate Interest will be imposed in amounts or at rates not in excess of those permitted by applicable law. -

![Switch Interface Gateway Oracle FLEXCUBE Universal Banking Release 11.80.02.0.0 CN Cluster Oracle Part Number E64368-01 [January] [2016]](https://docslib.b-cdn.net/cover/9682/switch-interface-gateway-oracle-flexcube-universal-banking-release-11-80-02-0-0-cn-cluster-oracle-part-number-e64368-01-january-2016-929682.webp)

Switch Interface Gateway Oracle FLEXCUBE Universal Banking Release 11.80.02.0.0 CN Cluster Oracle Part Number E64368-01 [January] [2016]

Switch Interface Gateway Oracle FLEXCUBE Universal Banking Release 11.80.02.0.0 CN Cluster Oracle Part Number E64368-01 [January] [2016] Switch Interface Gateway Table of Contents 1. ABOUT THIS MANUAL ................................................................................................................................ 1-1 1.1 INTRODUCTION ........................................................................................................................................... 1-1 1.2 AUDIENCE .................................................................................................................................................. 1-1 1.3 ABBREVIATIONS ......................................................................................................................................... 1-1 1.4 ORGANIZATION .......................................................................................................................................... 1-2 1.4.2 Related Documents ............................................................................................................................ 1-2 1.5 GLOSSARY OF ICONS .................................................................................................................................. 1-3 2. SWITCH INTERFACE GATEWAY ............................................................................................................ 2-1 2.1 INTRODUCTION .......................................................................................................................................... -

Synchrony Bank Section I: Rates and Fees Table Paypal Cashback Mastercard® Account Agreement Pricing Information

FR833282333_PAYPAL CASHBACK MASTERCARD T&C DC PDF WF3305322M, WF3305322N, WF3305322P 6/2021 SYNCHRONY BANK SECTION I: RATES AND FEES TABLE PAYPAL CASHBACK MASTERCARD® ACCOUNT AGREEMENT PRICING INFORMATION Interest Rates and Interest Charges The APR for purchases is the prime rate plus (i) 16.74% for Account Type 1, or (ii) 20.74% for Account Annual Percentage Type 2, or (iii) 23.74% for Account Type 3. Rate (APR) for Rates are determined when you open your account, based on your creditworthiness and other factors. Purchases These rates will vary with the market based on the Prime Rate. APR for Cash The APR for cash advances is the prime rate plus 23.74%. Advances This APR will vary with the market based on the Prime Rate. Paying Interest Your due date is at least 23 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month. We will begin charging interest on cash advances on the transaction date. Minimum If you are charged interest, the charge will be no less than $2.00. Interest Charge Fees Transaction Fees • Cash Advance Either $10 or 5% of the amount of each cash advance, whichever is greater. • Foreign Transaction 3% of each transaction. Penalty Fees • Late Payment Up to $40. • Returned Payment $29 How We Will Calculate Your Balance: We use a method called “daily balance.” See your credit card account agreement below for more details. 1 SECTION II: RATES, FEES AND PAYMENT INFORMATION PAYPAL CASHBACK MASTERCARD® ACCOUNT AGREEMENT How Interest is Calculated Your Interest Rate We use a daily rate to calculate the interest on the balance on your account each day. -

Postdoc Fellow RES/07/01

Coercing Consensus: Unintended success of the Octopus electronic payment system For PISTA 2008 Dr Lucia Leung-Sea SIU ([email protected]) Department of Sociology and Social Policy, Lingnan University Hong Kong, China ABSTRACT 1. INTRODUCTION This paper contrasts the success and failure of two In the world of plastic payment, credit cards and debit cards electronic payment systems in Hong Kong, Octopus and are the two major categories that have attained mature Mondex, during 1996-2002. The case illustrates the new development. Each has developed its own system of properties of electronic currencies, and provides insights for verification, settlement and security, spanning a globalized product designers and regulators. Mondex was endowed hierarchical framework of trust and settlement [19]. with the full legal status of money, launched by a mammoth However, demands for an electronic payment tool suitable banking group, with Mondex cards were given away for for small payments in the range of US$0.5 – US$5 remain free to consumers. Yet the Mondex system went into largely unfulfilled in most parts of the world. For every day oblivion within five years. Octopus started as a modest applications such as buying a coffee, a morning newspaper, stored value transport ticket that required a deposit. It ended paying for a bus ride, or feeding a parking meter, both up as a city-wide multipurpose payment card used by 95% merchants and consumers find it cumbersome to handle of the adult population. The system has saved significant exact change in coins. Yet the transaction costs of credit transaction costs from the handling of coins, generating cards and debit cards are formidable for these applications.