2005-1167.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Notice of Special Meeting

BOARD OF DIRECTORS EAST BAY MUNICIPAL UTILITY DISTRICT 375 - 11th Street, Oakland, CA 94607 Office of the Secretary: (510) 287-0440 Notice of Special Meeting FY22 and FY23 Budget Workshop #2 Tuesday, March 23, 2021 9:00 a.m. **Virtual** At the call of President Doug A. Linney, the Board of Directors has scheduled a Budget Workshop for 9:00 a.m. on Tuesday, March 23, 2021. Due to COVID-19 and in accordance with the most recent Alameda County Health Order, and with the Governor’s Executive Order N-29-20 which suspends portions of the Brown Act, this meeting will be conducted by webinar or teleconference only. In compliance with said orders, a physical location will not be provided for this meeting. These measures will only apply during the period in which state or local public health officials have imposed or recommended social distancing. The Board will meet in workshop session to review the proposed Fiscal Year 2022 (FY22) and Fiscal Year 2023 biennial budget, rates, operating and capital priorities, and staffing; the proposed FY22 System Capacity Charge and FY22 Wastewater Capacity Fee; and will receive follow-up information from the January 26, 2021 Budget Workshop #1. Dated: March 18, 2021 _______________________________ Rischa S. Cole Secretary of the District W:\Board of Directors - Meeting Related Docs\Notices\Notices 2021\032321_FY22_FY23 Budget Workshop 2.docx This page is intentionally left blank. BOARD OF DIRECTORS EAST BAY MUNICIPAL UTILITY DISTRICT 375 - 11th Street, Oakland, CA 94607 Office of the Secretary: (510) 287-0440 AGENDA Special Meeting FY22 and FY23 Budget Workshop #2 Tuesday, March 23, 2021 9:00 a.m. -

Contra Costa County

Historical Distribution and Current Status of Steelhead/Rainbow Trout (Oncorhynchus mykiss) in Streams of the San Francisco Estuary, California Robert A. Leidy, Environmental Protection Agency, San Francisco, CA Gordon S. Becker, Center for Ecosystem Management and Restoration, Oakland, CA Brett N. Harvey, John Muir Institute of the Environment, University of California, Davis, CA This report should be cited as: Leidy, R.A., G.S. Becker, B.N. Harvey. 2005. Historical distribution and current status of steelhead/rainbow trout (Oncorhynchus mykiss) in streams of the San Francisco Estuary, California. Center for Ecosystem Management and Restoration, Oakland, CA. Center for Ecosystem Management and Restoration CONTRA COSTA COUNTY Marsh Creek Watershed Marsh Creek flows approximately 30 miles from the eastern slopes of Mt. Diablo to Suisun Bay in the northern San Francisco Estuary. Its watershed consists of about 100 square miles. The headwaters of Marsh Creek consist of numerous small, intermittent and perennial tributaries within the Black Hills. The creek drains to the northwest before abruptly turning east near Marsh Creek Springs. From Marsh Creek Springs, Marsh Creek flows in an easterly direction entering Marsh Creek Reservoir, constructed in the 1960s. The creek is largely channelized in the lower watershed, and includes a drop structure near the city of Brentwood that appears to be a complete passage barrier. Marsh Creek enters the Big Break area of the Sacramento-San Joaquin River Delta northeast of the city of Oakley. Marsh Creek No salmonids were observed by DFG during an April 1942 visual survey of Marsh Creek at two locations: 0.25 miles upstream from the mouth in a tidal reach, and in close proximity to a bridge four miles east of Byron (Curtis 1942). -

(Oncorhynchus Mykiss) in Streams of the San Francisco Estuary, California

Historical Distribution and Current Status of Steelhead/Rainbow Trout (Oncorhynchus mykiss) in Streams of the San Francisco Estuary, California Robert A. Leidy, Environmental Protection Agency, San Francisco, CA Gordon S. Becker, Center for Ecosystem Management and Restoration, Oakland, CA Brett N. Harvey, John Muir Institute of the Environment, University of California, Davis, CA This report should be cited as: Leidy, R.A., G.S. Becker, B.N. Harvey. 2005. Historical distribution and current status of steelhead/rainbow trout (Oncorhynchus mykiss) in streams of the San Francisco Estuary, California. Center for Ecosystem Management and Restoration, Oakland, CA. Center for Ecosystem Management and Restoration TABLE OF CONTENTS Forward p. 3 Introduction p. 5 Methods p. 7 Determining Historical Distribution and Current Status; Information Presented in the Report; Table Headings and Terms Defined; Mapping Methods Contra Costa County p. 13 Marsh Creek Watershed; Mt. Diablo Creek Watershed; Walnut Creek Watershed; Rodeo Creek Watershed; Refugio Creek Watershed; Pinole Creek Watershed; Garrity Creek Watershed; San Pablo Creek Watershed; Wildcat Creek Watershed; Cerrito Creek Watershed Contra Costa County Maps: Historical Status, Current Status p. 39 Alameda County p. 45 Codornices Creek Watershed; Strawberry Creek Watershed; Temescal Creek Watershed; Glen Echo Creek Watershed; Sausal Creek Watershed; Peralta Creek Watershed; Lion Creek Watershed; Arroyo Viejo Watershed; San Leandro Creek Watershed; San Lorenzo Creek Watershed; Alameda Creek Watershed; Laguna Creek (Arroyo de la Laguna) Watershed Alameda County Maps: Historical Status, Current Status p. 91 Santa Clara County p. 97 Coyote Creek Watershed; Guadalupe River Watershed; San Tomas Aquino Creek/Saratoga Creek Watershed; Calabazas Creek Watershed; Stevens Creek Watershed; Permanente Creek Watershed; Adobe Creek Watershed; Matadero Creek/Barron Creek Watershed Santa Clara County Maps: Historical Status, Current Status p. -

4.14-1 This Chapter Describes Potential

4.14 UTILITIES AND SERVICE SYSTEMS This chapter describes potential impacts from the proposed Project on utili- ties and services including sanitary wastewater, water supply, stormwater drainage, solid waste, and energy conservation. The following service provid- ers serve the Project site and surrounding area: Central Contra Costa Sani- tary District (wastewater), East Bay Municipal Utilities District (water), Cen- tral Contra Costa Solid Waste Authority (solid waste), and the Pacific Gas and Electric Company (electric and natural gas). Correspondence and infor- mation provided from these service providers are included in Appendix L of this Draft EIR. A. Wastewater The Central Contra Costa Sanitary District (CCCSD) provides wastewater collection and treatment service for the Project site. This section describes the existing conditions and potential impacts of the Project with regard to wastewater collection and treatment facilities. 1. Regulatory Framework a. Federal Regulations i. Clean Water Act The Federal Water Pollution Control Act of 1972, more commonly known as the Clean Water Act (CWA), regulates the discharge of pollutants into wa- tersheds throughout the nation. Under the CWA, the United States Envi- ronmental Protection Agency (EPA) implements pollution control programs and sets wastewater standards. ii. National Pollutant Discharge Elimination System (NPDES) The National Pollutant Discharge Elimination System (NPDES) permit pro- gram was established in the Clean Water Act to regulate municipal and indus- trial discharges to -

Regional in Nature March - April 2012 East Bay Regional Park District Activity Guide

Regional in Nature March - April 2012 East Bay Regional Park District Activity Guide www.ebparks.org Spring is wildfl ower season in the parks. A fi eld of owl’s clover covers Round Valley Regional Preserve near Brentwood. Look Photo: Mark Crumpler Crumpler Mark Photo: inside for guided wildfl ower hikes in the Regional Parks. Inside: Junior Lifeguards • page 4 Park’n It Summer Day Camp • page 5 Pole Walking • page 6 Fire Making and Cord Making at Coyote Hills • page 11 Kayaking Big Break • page 14 Tips for Choosing a Summer Day Camp, see page 2. Contents Aquatics/Jr. Lifeguards .........4 Signifi cant Addition to Wildcat Recreation Programs ...... 5-6 Ardenwood ................. 6-7, 10 Canyon Regional Park Black Diamond ...............7, 10 BY GENERAL MANAGER ROBERT E. DOYLE Botanic Garden ..................10 Wildcat Canyon Regional Park, with Like adjacent Wildcat Canyon, this passed by voters in 2008 to help Coyote Hills ...................10-11 its majestic hills, ridges, and peaks, is recently acquired land contains secure open space. We are fortunate Crab Cove ......................11-12 growing. The East Bay Regional Park a mix of oak woodlands and grassland to have these funds at this time so we District Board of Directors recently providing a natural habitat to precious can act quickly to make bargain land Sunol ..................................... 12 approved the purchase of 362 acres wildlife. At Park District staff purchases. We are also fortunate Tilden Nature Area ...........12 adjacent to Wildcat Canyon, making it recommendation, much of the to work with a number of partner the largest parcel acquired by the Park property will be held in land bank agencies with similar visions to make Other Regional Parks ...12-14 District in west Contra Costa County status until it can be made safe our Regional Park system the fi nest Volunteer Programs ..........14 in 35 years. -

Watershed and Recreation Rules and Regulations

WATERSHED AND RECREATION RULES AND REGULATIONS TABLE OF CONTENTS Pages I. General Provisions………………………………………………..……1 – 2 II. Definitions………………………………………………….…………. 3 – 8 III. General Rules………………………………………………………..... 9 IV. Access………………………………………..…………………….......10 – 11 V. Boating Regulations…………………………………………………....12 – 15 VI. Camping……………………………………………………………......16 – 17 VII. Commercial Uses………………………………………………………18 VIII. Dangerous Activities………………………………………………….. 19 IX. General Nuisance……………………………………………………... 20 – 21 X. Protection of Property and Resources……………………………….... 22 – 25 XI. Sanitation……………………………………………………………... 26 – 27 XII. Trails…………………………………………………………..……… 28 XIII. Vehicles…………………………………………………………...….. 29 - 31 XIV. Bicycles, Skateboards, Roller Skates, Roller Blades, Etc……………… 32 XV. Hunting………………………………………………………………..... 33 Watershed Rules & Regulations May 27, 2014 I. GENERAL PROVISIONS 1.01 The following Regulations shall apply to all persons except: A. They shall not apply to District Employees, concessionaires, or employees of District concessionaries acting within the scope of their authorized duties. B. They shall not apply to employees of Federal, State, County or Municipal governments acting within the scope of their authorized duties and with the knowledge of the District. C. They shall not apply to persons possessing District Land Use, Special Use, Property Entry or Watershed Entry Permits when such permits specifically suspend a section or sections of the regulations providing said permittees are in compliance with all conditions of the permit and all other regulations. D. They shall not apply to leaseholders where such use is expressly provided for in the terms and conditions of their lease. 1.02 District employees, concessionaires, and employees of District concessionaires shall abide by the laws of the State of California and all applicable county and municipal ordinances. 1.03 Special regulations enacted for an area or a subject do not preclude the application of general regulations unless expressly so indicated. -

CSA P-6 Zones and Patrol Beats

Index Map: P-6 Zones and Sheriff's Patrol Beats in Contra Costa County as of July 2014 Solano Solano }þ12 680 County ¨¦§ County }þ37 ¨¦§80 Suisun Sacramento Bay County San Pablo Bay ¨¦§780 2 5 ¨¦§80 }þ160 16 4 680 Pittsburg }þ4 ¨¦§ 1 }þ4 !( Pinole Hercules !( }þ4 Oakley!( San Martinez Joaquin 242 San 3 }þ Concord Antioch County Pablo Pleasant Hill ¨¦§580 Richmond Clayton 15 El 6 Brentwood Cerrito Walnut 4 Lafayette Creek 7 }þ }þ24 Orinda Contra 14 }þ4 Costa ¨¦§80 !( County 12 }þ24 J4 Moraga 10 567 13 P-6 Zone }þ 680 ¨¦§ 13 ¨¦§980 Danville Bay¨¦§80 Station ¨¦§580 8 11 £101 ¤ Valley Station Muir Station 880 San ¨¦§ Ramon Alameda County Delta StationSan Alameda 280 205 ¨¦§ Francisco County ¨¦§ City Police BayService 9 ¨¦§580 Sheriff Dispatch Only 580 238 ¨¦§ Sheriff Contract Patrol ¨¦§ Sheriff Patrol Beats as depicted on this map 101 represent primary beat patterns. Beats are ¤£Park Police Service 680 ¨¦§ variable based on staffing and budgets. This map was created by the Contra Costa County Department of Conservation and Development Map Created 04/23/2015 with data from the Contra Costa County GIS Program. Some base data, primarily City Limits, is derived from the by Contra Costa County Department of CA State Board of Equalization's tax rate areas. P-6 Zones are derived from tax data and do not represent Conservation and Development, GIS Group Miles legal boundaries. While obligated to use this data the County assumes no responsibility for its accuracy. 30 Muir Road, Martinez, CA 94553 This map contains copyrighted information and may not be altered. -

Ebmud East Bay Watershed Trail Info: Northern Trails

EBMUD EAST BAY WATERSHED TRAIL INFO: NORTHERN TRAILS TRAIL START END DISTANCE (mi) LEASHED DOGS HORSES BICYCLES SUN EXPOSURE DIFFICULTY Pinole Valley Pereira Trailhead Alhambra Valley and 6.66 one way No Yes Yes Mostly sun Difficult Multi-Use Castro Ranch intersection Pinole Ridge Pereira Trailhead Pinole Valley Multi-Use Trail at 2.96 one way No Yes No Mostly sun Difficult Fernandez Ranch Windmill Trail Old San Pablo San Pablo Boat Launch Kennedy Grove Connector Trail 3.4 one way Limited to Yes Yes Equal parts shade and sun Easy (partially paved) park hours Old San Pablo (unpaved) Watershed Headquarters San Pablo Boat Launch 1.4 one way No Yes No Mostly shade Easy Eagle’s Nest San Pablo Recreation Area Nimitz Way 0.83 one way No Yes Yes Mostly shade Difficult Inspiration Inspiration Point Staging Area Old San Pablo Trail 1.98 one way No Yes No Mostly sun Difficult Orinda Connector Bear Creek Rd Watershed Headquarters 0.6 one way No Yes No Full shade Moderate Hampton Hampton Rd Oursan Trail 0.67 one way Yes Yes No Mostly shade Moderate Oursan Briones Overlook Staging Area Bear Creek Staging Area 9.54 one way Yes Yes No Mostly sun Moderate Bear Creek Bear Creek Staging Area Briones Overlook Staging Area 3.81 one way No Yes No Full shade Moderate Skyline Lomas Cantadas Trailhead Sibley Park boundary 1.73 one way No Yes No Equal parts shade and sun Moderate De Laveaga De Laveaga Trailhead Skyline Gardens Trailhead 2.85 one way No Yes No Mostly sun Difficult TRAIL DESCRIPTIONS Pinole Valley Multi-Use: From the Pereira Trailhead, cross the creek and turn left (west) at the Orinda Connector: This trail is a short but important link between the City of Orinda and EBMUD’s trail junction. -

Briones ALHAMBRA Martinez 0 123 4 Mi to Benicia IRON to 680 Antioch Briones in 1906, the People’S Water Company Began HORSE

Welcome to Briones ALHAMBRA Martinez 0 123 4 Mi To Benicia IRON To 680 Antioch Briones In 1906, the People’s Water Company began HORSE Year opened: 1967 Acres: 6,256 AV. REG. purchasing land in the San Pablo and Bear Creek To I-80 & 4 C.C.CANAL TRAIL Highlights: hiking, biking, horseback riding, bird areas for watershed lands. The East Bay Municipal Richmond REG. TR. Regional Park watching, picnicking, archery range, group camping, North Utility District acquired People’s Water Company A 242 LH Martinez, Pleasant Hill, Lafayette wildflowers in season. A in 1916 and built San Pablo Dam in 1923. In 1957 M Did you know? From 1,483-foot Briones Peak, B D R VA A Contra Costa County and EBMUD agreed to a land AL LLE A H Y O R hikers can enjoy 360-degree views of the California AM E AV. BRA R LIE WILLOW conveyance that established a large open space park Z BL. PASS RD. V LOR Delta, Mount Diablo, Mount Tamalpais, and Las Y A TA in the Bear Creek watershed to be called Briones. B L E L GRAY- A E Trampas Regional Wilderness. • Naturalist John R Y SON In 1964, when portions of Contra Costa County C Briones RD. R Muir, a resident of nearby Martinez, hiked these Concord . were annexed to the East Bay Regional Park E . E Regional D D K hills in the late nineteenth century. R District, the County and the Park District agreed to Park R L TREAT BL. Pleasant O L Hill Fees: Check website. -

Final Municipal Service Review Volume Ii—Utility Services Agency Appendix

FINAL MUNICIPAL SERVICE REVIEW VOLUME II—UTILITY SERVICES AGENCY APPENDIX Report to the Alameda Local Agency Formation Commission Submitted to: Alameda LAFCo Lou Ann Texeira, Executive Officer 1221 Oak Street, Room 555 Oakland, CA 94612 (510) 271-5142 Submitted by: Burr Consulting Beverly Burr, Project Coordinator 612 N. Sepulveda Blvd, Suite 8 Los Angeles, CA 90049 (310) 889-0077 In association with Braitman & Associates CDM Cotton/Bridges/Associates Accepted on November 10, 2005 ALAMEDA LAFCO UTILITY MSR—AGENCY APPENDIX TABLE OF CONTENTS PREFACE .............................................................................................................................................................. VIII CHAPTER A-1: ALAMEDA COUNTY FLOOD CONTROL DISTRICT...........................................................1 AGENCY OVERVIEW ..................................................................................................................................................1 FLOOD CONTROL SERVICE ........................................................................................................................................5 CHAPTER A-2: ALAMEDA COUNTY RESOURCE CONSERVATION DISTRICT.....................................23 AGENCY OVERVIEW ................................................................................................................................................23 CONSERVATION SERVICES.......................................................................................................................................27 -

U N S U U S E U R a C S

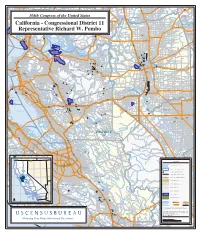

F S w a y Ione Band of Miwok TDSA c ( r S a t m H DISTRICT w e n y t o Napa 9 StHwy 84 9 StHwy 104 (Twin Cities Rd) 3 ) StH StHwy 121 w (Imola Ave) y 1 StHwy 88 1 3 AMADOR 108th Congress of the United States Sutter Slough Green Fairfield SACRAMENTO NAPA Cache Slough Valley Travis AFB Galt Suisun City Walnut Grove Dry Cr StHwy 12 StHwy 2 StH DISTRICT 20 wy 160 Hwy Dry Cr StHwy 12 (Rio V St 1 ista Rd) 22 0 Camanche Reservoir Sonoma Creek American Canyon StHwy 12 StHwy 99 Wallace Napa River 0 16 North Woodbridge y w H Lockeford t Rive S ne r m lu CALAVERAS Lodi Lake e k South Woodbridge o StHwy 37 (Sears Point Rd) Coast Guard Station Rio Vis M South Slough StHwy 12 80 680 Lodi ) d v l 9 B 2 Grizzly Bay StHwy 12 (Kettleman Ln) y a DISTRICT StHwy 12 w m SOLANO H o t n S o Vallejo 7 S ( Mare Island Sacramento River 5 Naval Complex 0 6 Concord 1 Benicia Naval y 780 Suisun Bay Weapons Sta w H t Honker Bay S Davis Lake San Pablo Bay Crockett Port Concord Weapons Sta Costa Carquinez Strait San Joaquin River West Ln Morada Bay Ln Bethel Mosher Slu Morada Rodeo Point StHwy 26 Clyde Island N Lower ) Linden d Lincoln Sacramento Rd R Vine o Bayview- o Village N Alturas Ave rl Hill te Montalvin Holiday a Mountain Pittsburg Dr (W 8 StRte 4 8 Hercules View Concord y Kermit Ln w Martinez Weapons Sta tH Tara StR Calaveras R S te Hills StRte 4 4 ( Pinole M Kentfield Rd 2 El a 4 Oakley i N el Dorado St S Pacheco 2 n t 80 Sobrante kn S W Alpine Ave e Antioch D t Country iv t e R ) r Rollingwood t August ti Anderson Ln Knightsen Club ng S C Empire Ave Brentwood -

To the Briones Regional Park Land Use-Development Plan

1994 AMENDMENT TO THE BRIONES REGIONAL PARK LAND USE-DEVELOPMENT PLAN Approved: December 6, 1994 Resolution No: 1994-12-305 East Bay Regional Park District Planning/Stewardship Department 2950 Peralta Oaks Court P.O. Box 5381 Oakland, CA 94605 (510) 635-0135 1994 AMENDMENT OF THE BRIONES REGIONAL PARK LAND USE-DEVELOPMENT PLAN TABLE OF CONTENTS Page # Introduction/Purpose ............................... 1 Land-Use Zoning for New Properties .................. .. 1 Background ................................... .. 1 Proposed Zoning .................................. 2 Master Plan Zoning Unit Percentages ................... 8 III. Specific Recreation Amendments .................... , .. 10 a. Designation of the Lafayette Ridge Recreation Unit with an Equestrian Day Camp .................. 10 b. Connection of the Lafayette Ridge Trail in Lafayette .... 17 c. Replacement of Special Event Camp Site at Corral Valley With a New Special Event Camp Site at Coyote Valley .. 18 . FIGURES 1. Land Use Zoning and Project Area Map ................. 3 2. Special Management and Resource Units of the Western Parcel . 5 3. Proposed Lafayette Ridge Recreation Unit with Equestrian Day Camp ......................... 11 4. Connection of the Lafayette Ridge Fire Trail .............. 19 5. Proposed Special Event Camp Site at Coyote Valley on Bear Creek Road . ..... :'. ·22 TABLES 1. EBRPD Resource Inventory Key - Special Units 9 APPENDIX A. Contra Costa County Public Works letter concerning Bear Creek Road (Coyote Valley Special Event Camp) 23 I. INTRODUCTION/PURPOSE The purpose of this amendment is to update the 1981 Briones Land use Development Plan (LUDP\EIR or "plan"). There are two major objectives to this effort. The first objective is to designate land use zones for the new acreage acquired since the LUDP. The amendment also establishes protective zoning for major creeks throughout the parkland.