Tax Incentives for Innovation in a Modern IP Ecosystem

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

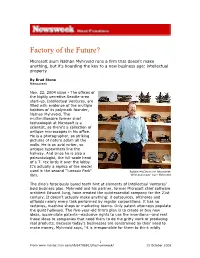

Factory of the Future?

Factory of the Future? Microsoft alum Nathan Myhrvold runs a firm that doesn't make anything, but it's hoarding the key to a new business age: intellectual property By Brad Stone Newsweek Nov. 22, 2004 issue - The offices of the highly secretive Seattle-area start-up, Intellectual Ventures, are filled with evidence of the multiple hobbies of its polymath founder, Nathan Myhrvold. The multimillionaire former chief technologist at Microsoft is a scientist, so there's a collection of antique microscopes in his office. He is a photographer, so striking pictures of nature adorn all the walls. He is an avid writer, so antique typewriters line the hallway. And since he is also a paleontologist, the full-scale head of a T. rex lords it over the lobby. It's actually a replica of the model used in the second "Jurassic Park" Robbie McClaran for Newsweek film. 'Wild and crazy' guy: Myhrvold The dino's ferociously bared teeth hint at elements of Intellectual Ventures' bold business plan. Myhrvold and his partner, former Microsoft chief software architect Edward Jung, have created the quintessential company for the 21st century. It doesn't actually make anything: it outsources, offshores and offloads nearly every task performed by regular corporations. It has no factories, machine shops or marketing teams. Only patent attorneys populate the quiet hallways. The five-year-old firm's plan is to create or buy new ideas, accumulate patents—exclusive rights to use the inventions—and rent those ideas to companies that need them to do the gritty work of producing real products. -

Some Facts of High-Tech Patenting

Some Facts of High-Tech Patenting Michael Webb Nick Short Nicholas Bloom Josh Lerner Working Paper 19-014 Some Facts of High-Tech Patenting Michael Webb Nick Short Stanford University Harvard Kennedy School Nicholas Bloom Josh Lerner Stanford University Harvard Business School Working Paper 19-014 Copyright © 2018 by Michael Webb, Nick Short, Nicholas Bloom, and Josh Lerner Working papers are in draft form. This working paper is distributed for purposes of comment and discussion only. It may not be reproduced without permission of the copyright holder. Copies of working papers are available from the author. Some Facts of High-Tech Patenting Michael Webb, Nick Short, Nicholas Bloom, and Josh Lerner NBER Working Paper No. 24793 July 2018 JEL No. L86,O34 ABSTRACT Patenting in software, cloud computing, and artificial intelligence has grown rapidly in recent years. Such patents are acquired primarily by large US technology firms such as IBM, Microsoft, Google, and HP, as well as by Japanese multinationals such as Sony, Canon, and Fujitsu. Chinese patenting in the US is small but growing rapidly, and world-leading for drone technology. Patenting in machine learning has seen exponential growth since 2010, although patenting in neural networks saw a strong burst of activity in the 1990s that has only recently been surpassed. In all technological fields, the number of patents per inventor has declined near-monotonically, except for large increases in inventor productivity in software and semiconductors in the late 1990s. In most high-tech fields, Japan is the only country outside the US with significant US patenting activity; however, whereas Japan played an important role in the burst of neural network patenting in the 1990s, it has not been involved in the current acceleration. -

THE DEFENSIVE PATENT PLAYBOOK James M

THE DEFENSIVE PATENT PLAYBOOK James M. Rice† Billionaire entrepreneur Naveen Jain wrote that “[s]uccess doesn’t necessarily come from breakthrough innovation but from flawless execution. A great strategy alone won’t win a game or a battle; the win comes from basic blocking and tackling.”1 Companies with innovative ideas must execute patent strategies effectively to navigate the current patent landscape. But in order to develop a defensive strategy, practitioners must appreciate the development of the defensive patent playbook. Article 1, Section 8, Clause 8 of the U.S. Constitution grants Congress the power to “promote the Progress of Science and useful Arts, by securing for limited Times to Authors and Inventors the exclusive Right to their respective Writings and Discoveries.”2 Congress attempts to promote technological progress by granting patent rights to inventors. Under the utilitarian theory of patent law, patent rights create economic incentives for inventors by providing exclusivity in exchange for public disclosure of technology.3 The exclusive right to make, use, import, and sell a technology incentivizes innovation by enabling inventors to recoup the costs of development and secure profits in the market.4 Despite the conventional theory, in the 1980s and early 1990s, numerous technology companies viewed patents as unnecessary and chose not to file for patents.5 In 1990, Microsoft had seven utility patents.6 Cisco © 2015 James M. Rice. † J.D. Candidate, 2016, University of California, Berkeley, School of Law. 1. Naveen Jain, 10 Secrets of Becoming a Successful Entrepreneur, INC. (Aug. 13, 2012), http://www.inc.com/naveen-jain/10-secrets-of-becoming-a-successful- entrepreneur.html. -

P106 - Word Count: 2,818

Brian Schnack ([email protected]) Garrett Thompson ([email protected]) Group: P106 - Word Count: 2,818 Patents and Technology The patent system was designed to promote intellectual innovation and to protect inventions from being stolen, allowing small companies to thrive if their ideas are new and innovative. The founding fathers thought it was so important to “promote the Progress of Science and useful Arts” that they wrote it directly into the U.S. Constitution (US Constitution, 8). However in recent years, with patents on programming algorithms and different electronic components, the patent system has started to inhibit innovation. The current methodology of the US patent system does not promote intellectual inventions in software and technology, but instead allows companies to abuse the patent system. Companies misuse the patent system to make money through lawsuits rather than innovation, hurting businesses and ultimately the consumer. Slowly, through the judicial court, things are beginning to shape up but the United States is still a long way away from a patent system that actually does promote intellectual innovation. One large company that uses the broken patent system to their advantage is Intellectual Ventures, a company that attempts to help small time inventors protect their intellectual property by buying their patents, a move they call investing in their inventions. Unfortunately, this is not how it usually plays out, and Intellectual Ventures ends up selling patents to companies who attempt to make money purely by suing other companies who are infringing on the patents that they just bought. Many companies that Intellectual Ventures sells patents to are not even companies, but individuals pretending to be a company who will then use those patents to sue actual companies to make quick and easy money. -

Patents & Legal Expenditures

Patents & Legal Expenditures Christopher J. Ryan, Jr. & Brian L. Frye* I. INTRODUCTION ................................................................................................ 577 A. A Brief History of University Patents ................................................. 578 B. The Origin of University Patents ........................................................ 578 C. University Patenting as a Function of Patent Policy Incentives ........ 580 D. The Business of University Patenting and Technology Transfer ....... 581 E. Trends in Patent Litigation ................................................................. 584 II. DATA AND ANALYSIS .................................................................................... 588 III. CONCLUSION ................................................................................................. 591 I. INTRODUCTION Universities are engines of innovation. To encourage further innovation, the federal government and charitable foundations give universities grants in order to enable university researchers to produce the inventions and discoveries that will continue to fuel our knowledge economy. Among other things, the Bayh-Dole Act of 1980 was supposed to encourage additional innovation by enabling universities to patent inventions and discoveries produced using federal funds and to license those patents to private companies, rather than turning their patent rights over to the government. The Bayh-Dole Act unquestionably encouraged universities to patent inventions and license their patents. -

How Valuable Is Your Patent, Really?

1 2 3 4 • These are factors that go beyond the usual realm of a patent prosecution counsel • broad claims • well supported by spec • clean prosecution history • Timely issuance • Can the patent stand alone as an asset? à How much is the patent worth in the market place? 5 • Life after AIA • Presumption of validity at the district court level is no longer there • Parallel proceedings at PTAB • High rate of IPR institution and claim cancellation (especially at the outset of AIA) • While the application of AIA rules and new processes are being hashed out, presumption of validity is definitely gone. • Case law is always evolving – Pendulum still swinging • Gottschalk v. Benson • Parker v. Flook • Diamond v. Diehr • State Street Bank v. Signature Financial Group • In re Bilski • Alice Corp. v. CLS Bank International • DDR Holdings v. Hotels.com (one patent held as patentable! • Enfish v. Microsoft • Certain PTAB decisions being designated precedential 6 http://www.ncsl.org/research/financial-services-and-commerce/2016-patent-troll- legislation.aspx http://www.law360.com/articles/836578/the-post-aia-battleground-for-patent- challenges http://www.finnegan.com/resources/articles/articlesdetail.aspx?news=3aad1da2- 08a9-4f14-a147-611b1e39ff75 ITC: Availability of Cease and Desist orders and Limited or General Exclusion Orders; speedy proceedings “anti-patent troll” — i.e., entities that have made a business out of directly challenging patents via IPR for financial gain (“...IPR process is being misused by hedge fund companies whose motive isn't -

Intellectual Ventures Comments

INTELLECTUAL VENTURES" July 3, 2018 By Mail & Email ([email protected]) The Honorable Andrew lancu Under Secretary of Commerce for Intellectual Property Director of the United States Patent and Trademark Office United States Patent & Trademark Office Mail Stop Patent Board P.O. Box 1450 Alexandria, VA 22313-1450 Attention Vice Chief Administrative Patent Judges Michael Tierney or Jacqueline Wright Bonilla, PTAB Notice of Proposed Rulemaking 2018. Dear Under Secretary lancu: Intellectual Ventures Management LLC ("Intellectual Ventures") thanks the Director for the opportunity to present its views on the United States Patent & Trademark Office ("Office") Notice of Proposed Rulemak ing entitled "Changes to the Claim Construction Standard for Interpreting Claims in Trial Proceedings Be fore the Patent Trial and Appeal Board" as published in the May 9, 2018 issue of the Federal Register, 83 Fed. Reg. 21,221 ("Notice"). Intellectual Ventures urges the Office to adopt the rules proposed in the Notice. About Intellectual Ventures Intellectual Ventures fosters conception, development, and investment in inventions. It was co-founded by Dr. Nathan Myhrvold, who is also its Chief Executive Officer. Dr. Myhrvold was previously the Chief Tech nology Officer of Microsoft, and he holds a doctorate in theoretical and mathematical physics and a mas ter's degree in mathematical economics from Princeton University, as well as a master's degree in geo physics and space physics and a bachelor's degree in mathematics from the University of California at Los Angeles. He was a postdoctoral fellow in the quantum physics laboratory of Dr. Stephen Hawking at Cambridge University. And he is a named inventor on hundreds of issued patents. -

The Opinion in Support of the Decision Being Entered Today Was

[email protected] Paper No. 18 571-272-7822 Entered: July 23, 2018 UNITED STATES PATENT AND TRADEMARK OFFICE ____________ BEFORE THE PATENT TRIAL AND APPEAL BOARD ____________ EBAY INC. and PAYPAL, INC., Petitioner, v. XPRT VENTURES, LLC, Patent Owner. ____________ Case CBM2017-00027 Patent 7,483,856 B2 ____________ Before JAMESON LEE, KEVIN F. TURNER, and MICHAEL R. ZECHER, Administrative Patent Judges. ZECHER, Administrative Patent Judge. FINAL WRITTEN DECISION Covered Business Method Patent Review 35 U.S.C. § 328(a) and 37 C.F.R. § 42.73 CBM2017-00027 Patent 7,483,856 B2 I. INTRODUCTION eBay Inc. and PayPal, Inc. (collectively, “Petitioner”), filed a Petition requesting a review under the transitional program for covered business method patents of claims 1, 5, 6, 8, 34, 35, 45, and 48 (“challenged claims”) of U.S. Patent No. 7,483,856 B2 (Ex. 1001, “’856 patent”). Paper 1 (“Pet.”). Patent Owner, XPRT Ventures, LLC (“Patent Owner”), did not file a Preliminary Response. We preliminarily determined that the information presented in the Petition established that the ’856 patent qualifies as a covered business method patent that is eligible for review, and that it was more likely than not that the challenged claims are unpatentable under 35 U.S.C. § 101. Paper 8. Pursuant to 35 U.S.C. § 324 and § 18(a) of the Leahy-Smith America Invents Act (“AIA”), Pub. L. No. 112-29, 125 Stat. 284, 329–31 (2011), we instituted a covered business method patent review as to all of the challenged claims. Id. Patent Owner filed a Response to the Petition (Paper 13 (“PO Resp.”)), and Petitioner filed a Reply (Paper 14 (“Pet. -

CPI Antitrust Chronicle January 2015 (2)

CPI Antitrust Chronicle January 2015 (2) Intellectual Ventures v. Capital One: Can Antitrust Law and Economics Get Us Past the Trolls? Michelle D. Miller (WilmerHale) & Janusz A. Ordover (New York University) www.competitionpolicyinternational.com Competition Policy International, Inc. 2015© Copying, reprinting, or distributing this article is forbidden by anyone other than the publisher or author. CPI Antitrust Chronicle January 2015 (2) Intellectual Ventures v. Capital One: Can Antitrust Law and Economics Get Us Past the Trolls? Michelle D. Miller & Janusz A. Ordover1 I. INTRODUCTION Patent trolls are currently under intense scrutiny by lawmakers, regulators, academics, and industry players. The term “patent troll” generally refers to patent owners that do not make or sell products, and instead focus on licensing and litigation to monetize their acquired patents. These entities are also known as “patent assertion entities” (PAEs)2, and in this paper, we use the terms interchangeably. Infringement suits brought by trolls have exploded over the last few years—in 2012 patent trolls accounted for 62 percent of all patent infringement suits,3 and recent studies estimate that trolls imposed direct costs of $29 billion in 2011.4 And these costs appear to be deterring investment in new businesses and technologies—one study estimated that venture capital funding was $8.1 billion lower over a five-year period than it would have been without PAE enforcement.5 Although most commentators have concluded that many patent troll business models lead to market inefficiencies, it is not clear what can be done in the short term to address the wide variety of concerns that troll activities raise.6 Various legislative solutions have been suggested 1 Michelle Miller is a partner in the Antitrust and Competition Group of WilmerHale. -

Intermediaries for the IP Market Working Paper

Intermediaries for the IP market Andrei Hagiu David Yoffie Working Paper 12-023 October 12, 2011 Copyright © 2011 by Andrei Hagiu and David Yoffie Working papers are in draft form. This working paper is distributed for purposes of comment and discussion only. It may not be reproduced without permission of the copyright holder. Copies of working papers are available from the author. Intermediaries for the IP market1 Andrei Hagiu and David Yoffie2 Introduction Some assets are traded in liquid markets with the help of many, thriving intermediaries: houses and apartments, financial products, books, DVDs, electronics and all sorts of collectibles. Intellectual property (IP) in general and patents in particular are not among those assets. In fact, one could argue that the market for patents is one of the last large and inefficient markets in the economy. There are some obvious reasons for why the patent market is highly illiquid: IP is the ultimate intangible asset and extremely hard to value. Moreover, there are very high search and transaction costs on both sides of the market (inventors or patent owners and operating companies or patent users/buyers) and the risk of litigation makes all potential participants even more cautious. Despite these difficulties, there could be attractive opportunities to create intermediation mechanisms to match patent creators with patent users and facilitate transactions between them, thereby allowing each side to specialize in what they do best (creators to innovate; users to build products based on the IP embedded in the corresponding patents). And indeed, during the last 5- 10 years a variety of novel and intriguing intermediaries has emerged, all using different business models while attempting to bring more liquidity to the patent market. -

View Report 2015 Annual Report

2015 Annual Report © Invent Now, Inc. United States Patent and Trademark Office Partnership The United States Patent and Trademark Office CIC is the only competition in the country where Letter from the CEO (USPTO) is a founding partner of NIHF and student finalists are judged by a panel of NIHF In 2015, we continued to implement our vision to be the Hall What distinguishes our organization from all others is our Invent Now Mission continues to support our programs and national Inductees and USPTO officials for feedback, of Fame that pays it forward by spreading our mission to core, the National Inventors Hall of Fame, and our relationship outreach to inspire innovation in America. brainstorming, and encouragement on advancing inspire innovation in America. Big talk backed up by decisive with the United States Patent and Trademark Office (USPTO), their innovation and intellectual property protection. action last year: 123,000 K-12 students, led by 8,000 of our a founding partner. The USPTO, the ultimate purveyor of We inspire innovation Through decades of collaboration, the USPTO’s nation’s best teachers from 1,500 outstanding school districts, intellectual property, is home to the National Inventors Hall of investment has propelled Camp Invention, Club Finally, the National Inventors Hall of Fame museum were immersed in our programming from Camp Invention and Fame Museum, which is worth a trip to Alexandria, VA, just in America. Invention, and Invention Project to be the largest is located on the USPTO headquarters campus Club Invention (pages 3-6) to Invention Project (pages 7-8) outside Washington, DC. -

Geopiracy: the Case Against Geoengineering I Geopiracy: the Case Against Geoengineering

“We cannot solve our problems with the same thinking we used when we created them.” Albert Einstein “We already are inadvertently changing the climate. So why not advertently try to counterbalance it?” Michael MacCracken, Climate Institute, USA About the cover ETC Group gratefully acknowledges the financial support of SwedBio The cover is an adaptation of The (Sweden), HKH Foundation (USA), Scream by Edvard Munch, painted in CS Fund (USA), Christensen Fund 1893, shown on the right. Munch (USA), Heinrich Böll Foundation painted several versions of this image (Germany), the Lillian Goldman over the years, which reflected his Charitable Trust (USA), Oxfam Novib feeling of "a great unending scream (Netherlands), and the Norwegian piercing through nature." One theory is Forum for Environment and that the red sky was inspired by the Development. ETC Group is solely eruption of Krakatoa, a volcano that responsible for the views expressed in cooled the Earth by spewing sulphur this document. into the sky, which blocked the sun. Geoengineers seek to artificially Copy-edited by Leila Marshy reproduce this process. Design by Shtig (.net) Geopiracy: The Case Against Acknowledgements Geoengineering is ETC Group We also thank the Beehive Collective Communiqué # 103 ETC Group is grateful to Almuth for artwork and all the participants of First published October 2010 Ernsting of Biofuelwatch, Niclas the HOME campaign for their ongoing Second edition November 2010 Hällström of the Swedish Society for participation and support as well as the Conservation of Nature (that Leila Marshy and Shtig for good- All ETC Group publications are published Retooling the Planet from humoured patience and professionalism available free of charge on our website: which some of this material is drawn).