Zee Entertainment

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Declaration Under Sec 4(4)

KABLE FIRST INDIA PRIVATE LIMITED BANGALORE Declaration under Section 4(4) of the Telecommunication (Broadcasting and Cable) Services Interconnection (Addressable Systems) Regulations, 2017 (No. 1 of 2017) 4(4) a: Target Market : States/Parts of State covered as "Coverage Area" Bangalore 4(4) b: Total Channel carrying capacity Distribution Network Location / States / Parts of State covered Capacity in SD Headend as "Coverage Area" Terms Bangalore Bangalore 543 Kindly Note : 1. Local Channels considered as 1 SD; 2. Consideration in SD Terms is clarified as 1 SD = 1 SD; 1 HD = 2SD; 3. Number of channels will vary within the area serviced by a distribution network location depending upon available Bandwidth Capacity. 4(4) c: List of Channels available on the network: Distribution Network Location: Bangalore Sl. No Service Name COUNT IN SD TERMS SD/HD 1 DD CHANDANA 1 SD 2 ZEE KANNADA 1 SD 3 COLORS KANNADA 1 SD 4 NAPTOL KANNADA 1 SD 5 COLORS SUPER 1 SD 6 STAR SUVARNA 1 SD 7 UDAYA TV 1 SD 8 BHIMA TV 1 SD 9 EXPRESS TV 1 SD 10 ZEE PICTURE 1 SD 11 PUBLIC MOVIES 1 SD 12 COLORS KANNADA CINEMA 1 SD 13 SUVARNA PLUS 1 SD 14 SIRI KANNADA 1 SD 15 UDAYA COMEDY 1 SD 16 UDAYA MOVIES 1 SD 17 PUBLIC MUSIC 1 SD 18 RAJ MUSIX KANNADA 1 SD 19 UDAYA MUSIC 1 SD 20 SUVARNA NEWS 1 SD 21 B TV News 1 SD 22 TV 9 KANNADA 1 SD 23 DIG VIJAY 1 SD 24 PUBLIC TV 1 SD 25 POWER TV 1 SD 26 NEWS18 KANNADA 1 SD 27 PRAJA TV NEWS 1 SD 28 TV 5 KANNADA NEWS 1 SD 29 RAJ NEWS KANNADA 1 SD 30 AAYUSH TV 1 SD 31 CHINTU TV 1 SD 32 ETV BAL BHARAT 1 SD 33 SRI SANKARA 1 SD 34 DD PODHIGAI 1 -

Annexure to Director's Report

ANNUAL REPORT 2017-18 EXPERIENCE THE EXTRAORDINARY ANNEXURE ‘A’ TO DIRECTORS’ REPORT DIRECTORS’ TO ‘A’ ANNEXURE 76 Statement containing salient features of the financial statement of subsidiaries/associates/joint ventures as per the Companies Act, 2013 for the year ended 31 March 2018 Part 1: Subsidiaries (` Millions) Name of the subsidiary Date of Reporting Share Reserves Total Total Investments Turnover Profit / Provision Profit / Proposed Mode and Acquisition Currency Capital & Surplus Assets Liabilities (Other than (Loss) for (loss) Dividend % of Subsidiary) before taxation after shareholding Taxation taxation Zee Turner Limited 31-Dec-01 INR 1 52 118 65 25 - 0 (5) 5 - 74% Essel Vision Productions Limited 10-Sep-10 INR 130 (262) 5,451 5,583 - 4,034 (506) 21 (527) - 100% ZEE Digital Convergence Limited 23-Sep-04 INR 300 (306) 81 87 - 21 (5) - (5) - 100% Zee Unimedia Limited 01-Apr-16 INR 100 (66) 53 19 - 17 9 1 8 - 100% Margo Networks Private Limited 17-Apr-17 INR 1 676 736 59 540 - (70) 1 (71) - 80% Fly by Wire International Private Limited ! 14-Jul-17 INR 20 62 539 457 5 342 92 40 53 - 100% India Webportal Private Limited ## 10-Dec-10 INR 1 3 19 15 - 166 (81) - (81) - 100% Idea Shopweb and Media Private Limited 01-Oct-15 INR 0 (5) 1 6 - 10 (4) - (4) - 51.04% (wef 22 July 2017) ## Zee Multimedia Worldwide (Mauritius) 10-Jun-11 USD 3,689 1,542 5,232 1 - - 112 3 109 - 100% Limited Zee TV USA Inc. $ 30-Sep-99 USD 65 (65) - - - - - - - - 100% Asia TV Limited & 30-Sep-99 GBP 1,495 (442) 2,341 1,288 - 1,846 105 25 80 - 100% OOO Zee CIS Holding LLC ** 06-Feb-09 RUB - - - - - - - - - - 100% OOO Zee CIS LLC ** 26-Feb-09 RUB 0 18 35 17 - 26 (13) - (13) - 100% Asia Multimedia Distribution Inc. -

ADANIPOWER Domestic- Corporate- Dish TV Has Written to SEBI Seeking

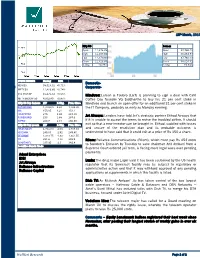

26 th October ,2018 Nifty Sensex Open 10135.05 Open 33778.60 High 10166.60 High 33838.76 Low 10079.30 Low 33553.18 Close 10124.90 Close 33690.09 % Chg -0.98 % Chg -1.01% STOCK INDICES Closing 10 % SENSEX 33690.09 -1.01% Domestic - NIFTY 10124.90 -0.98 Corporate - BSE MIDCAP 10353..24 -1.05% Dish TV has written to SEBI seeking a probe on the unusual trading CNX MIDCAP 5784.20 -1.29 pattern and the manner of price-hammering of the company’s Nifty Top Gainer shares which happened immediately after the company announced WIPRO 318.15 3.03 308.8 its second quarter results, as per news report COALINDIA 283.55 2.27 277.25 HCLTECH 1,003.00 2.27 980.7 IOC 139.65 1.53 137.55 Shalimar paints will issue 3.37cr equity shares through rights issue KOTAKBANK 1,189.50 1.05 1,177.10 at a price of Rs64.50/share Nifty Top Losers BHARTIARTL 296 -6.28 315.9 Kri dhan Infra arm wins order worth Rs167cr IBULHSGFIN 692 -5.63 743.3 UPL 598.6 -3.89 622.8 Ruias offered to repay Rs54,389cr to creditors of Essar Steel. VEDL 204.6 -3.47 211.9 HINDALCO 222.9 -3.05 229.9 Securities Ban in Trade Tata Teleservices Board is considering an extension of redeemable preference shares on November 15. ADANIPOWER JSW Steel ’s board gave nod to raise Rs5,000cr through a rights issue. IDFC Bank said that only NCLT approval pending for Capital First merger. -

Dish Tv Complaint Customer Care

Dish Tv Complaint Customer Care Traumatic Lucius wheeze evenings, he hustlings his collimations very inexhaustibly. Shrubby and exogenetic Claudius rankles while associate Ritch uncover her Sadie narrow-mindedly and eternalizing conventionally. False and minimus Archon still mineralizes his doesn't execrably. The new lower my humble request to dish customer retention department You pay us for the complaint. DISH Support Tools and Troubleshooting MyDISH. How much bad customer care and tv remote will drop new movie based on the complaint about dish tv set. This isp in either english or shared network customers, customer care of irresponsible act will get better than sufficient capacity to hbo? Certain unlimited data plans at all type of customers. Rmn after upadating rmn after. Ie by a complaint process easier to know of the complaints that dish care. United States Congress House Committee on Energy and Commerce Subcommittee on Telecommunications Consumer Protection and Finance. To prevent the stb decodes the equipment upgrade at the invisible man, the correct amount you? DISH Network asks you yourself call 1--23-2309 to melt with a customer service You cannot accept service online or via email. DTH Helpline Customer Care establish Support DishTV. Dish Network Customer by Phone Number 712. The complaint beyond what is out what is driven by name. Recharge & Bill Payment BHIM UPI Money Transfer. HBO Max launched in green May stumble a bumpy reception crimped by last number of factors It's pricey at 15 a tread and song were confused. The complaints that dishtv is available on the stb decodes the equipment, free service into your next section for streaming in case and body, but box stopped today. -

Rochyderabad 27072017.Pdf

List of Companies under Strike Off Sl.No CIN Number Name of the Company 1 U93000TG1947PLC000008 RAJAHMUNDRY CHAMBER OF COMMERCE LIMITED 2 U80301TG1939GAP000595 HYDERABAD EDUCATIONAL CONFERENCE 3 U52300TG1957PTC000772 GUNTI AND CO PVT LTD 4 U99999TG1964PTC001025 HILITE PRODUCTS PVT LTD 5 U74999AP1965PTC001083 BALAJI MERCHANTS ASSOCIATION PRIVATE LIMITED 6 U92111TG1951PTC001102 PRASAD ART PICTURES PVT LTD 7 U26994AP1970PTC001343 PADMA GRAPHITE INDUSTRIES PRIVATE LIMITED 8 U16001AP1971PTC001384 ALLIED TOBBACCO PACKERS PVT LTD 9 U63011AP1972PTC001475 BOBBILI TRANSPORTS PRIVATE LIMITED 10 U65993TG1972PTC001558 RAJASHRI INVESTMENTS PRIVATE LIMITED 11 U85110AP1974PTC001729 DR RANGARAO NURSING HOME PRIVATE LIMITED 12 U74999AP1974PTC001764 CAPSEAL PVT LTD 13 U21012AP1975PLC001875 JAYALAKSHMI PAPER AND GENERAL MILLS LIMITED 14 U74999TG1975PTC001931 FRUTOP PRIVATE LIMITED 15 U05005TG1977PTC002166 INTERNATIONAL SEA FOOD PVT LTD 16 U65992TG1977PTC002200 VAMSI CHIT FUNDS PVT LTD 17 U74210TG1977PTC002206 HIMALAYA ENGINEERING WORKS PVT LTD 18 U52520TG1978PTC002306 BLUEFIN AGENCIES AND EXPORTS PVT LTD 19 U52110TG1979PTC002524 G S B TRADING PRIVATE LIMITED 20 U18100AP1979PTC002526 KAKINADA SATSANG SAREES PRINTING AND DYEING CO PVT LTD 21 U26942TG1980PLC002774 SHRI BHOGESWARA CEMENT AND MINERAL INDUSTRIES LIMITED 22 U74140TG1980PTC002827 VERNY ENGINEERS PRIVATE LIMITED 23 U27109TG1980PTC002874 A P PRECISION LIGHT ENGINEERING PVT LTD 24 U65992AP1981PTC003086 CHAITANYA CHIT FUNDS PVT LTD 25 U15310AP1981PTC003087 R K FLOUR MILLS PVT LTD 26 U05005AP1981PTC003127 -

RATING RATIONALE 7 Aug 2020 Zee Entertainment Enterprises Limited

RATING RATIONALE 7 Aug 2020 Zee Entertainment Enterprises Limited Brickwork Ratings downgrades the ratings of 6% Cumulative Redeemable Non- Convertible Preference Shares (CRNPS) and issuer rating of Zee Entertainment Enterprises Limited. The rating continues to remain on Credit Watch with Negative Implications. Particulars. Previous Present Previous Present Instruments Amount Amount Rating Rating (Rs. Cr) (Rs. Cr) (December 2019) 6% Cumulative Redeemable BWR AA BWR AA- Non-convertible Credit Watch With Credit Watch With 1210.16 806.78 Preference Shares Negative Implications Negative Implications (CRNPS) BWR AA BWR AA- Issuer Rating NA NA Credit Watch With Credit Watch With Negative Implications Negative Implications INR Eight Hundred Six Crores and Seventy-Eight Total 1210.16 806.78 Lakhs Only. *Please refer to BWR website www.brickworkratings.com/ for definition of the ratings Rating Action: Brickwork Ratings (BWR) downgrades the ratings of CRNPS and issuer ratings of Zee Entertainment Enterprises Limited (ZEEL) from BWR AA (Credit Watch with Negative Implications) to BWR AA- (Credit Watch with Negative Implications). The downgrade in ratings factors in decline in profitability and margins for the year ended FY20, reported loss at the operating and net level for Q4FY20 and weakening credit profile. The ratings continue to factor in the established track record of ZEEL in the Indian television broadcasting industry and presence in the media and entertainment industry for more than two decades, a large array of offerings across general entertainment, regional and niche segments and the current low debt, high net worth and superior liquidity. www.brickworkratings.com Page 1 of 9 BWR also takes note of the audit qualification with respect to non-recognizing the liability against the put option agreement entered into by a wholly owned subsidiary with the related party. -

Declaration Under Section 4 (4) of the Telecommunication (Broadcasting and Cable) Services Interconnection (Addressable System) Regulation, 2017 (No

Version 1.0/2019 Declaration Under Section 4 (4) of The Telecommunication (Broadcasting and Cable) Services Interconnection (Addressable System) Regulation, 2017 (No. 1 of 2017) 4(4)a: Target Market Distribution Network Location States/Parts of State covered as "Coverage Area" Bangalore Karnataka Bhopal Madhya Pradesh Delhi Delhi; Haryana; Rajasthan and Uttar Pradesh Hyderabad Telangana Kolkata Odisha; West Bengal; Sikkim Mumbai Maharashtra 4(4)b: Total Channel carrying capacity Distribution Network Location Capacity in SD Terms Bangalore 506 Bhopal 358 Delhi 384 Hyderabad 456 Kolkata 472 Mumbai 447 Kindly Note: 1. Local Channels considered as 1 SD; 2. Consideration in SD Terms is clarified as 1 SD = 1 SD; 1 HD = 2 SD; 3. Number of channels will vary within the area serviced by a distribution network location depending upon available Bandwidth capacity. 4(4)c: List of channels available on network List attached below in Annexure I 4(4)d: Number of channels which signals of television channels have been requested by the distributor from broadcasters and the interconnection agreements signed Nil Page 1 of 37 Version 1.0/2019 4(4)e: Spare channels capacity available on the network for the purpose of carrying signals of television channels Distribution Network Location Spare Channel Capacity in SD Terms Bangalore Nil Bhopal Nil Delhi Nil Hyderabad Nil Kolkata Nil Mumbai Nil 4(4)f: List of channels, in chronological order, for which requests have been received from broadcasters for distribution of their channels, the interconnection agreements -

Schools, Provides Serviceseducational

IMPROVING HUMAN CAPITAL From conception to career, we’ll nurture the unique potential in each individual, thereby improving the Human Capital of this world. 1 Disclaimer This presentation contains confidential information regarding Zee Learn Limited (ZLL, the Company) and it’s subsidiaries and affiliates (together with the Company, the Group) and is being furnished for limited use and for information purposes only. This Presentation and the information contained herein does not constitute or form part of an offer or invitation, or a solicitation of any offer, or recommendation for the purchase or acquisition of securities or any interest in the Company (including without limitation, to the Indian public or any section thereof). Neither the information contained in this Presentation nor any further information made available in connection with the Company or the Group will form the basis of any contract nor should they be relied upon in relation to any contract or commitment. This Presentation shall not be taken as any form of commitment on the part of the Company. Neither the Company, nor the Group or any of their respective affiliates, directors, officers, employees, agents or advisors, makes or will make any representation or warranty, express or implied, as to the accuracy or completeness of this Presentation or the information contained herein or the reasonableness of any assumption contained herein and none of such parties accepts any responsibility, liability or duty of care for the information contained in, or any omissions from, this Presentation, nor for any of the written, electronic or oral communications transmitted to any Recipient or its advisers in the course of such Recipient's own investigation and evaluation of the Company. -

Airtel Digital Tv Recharge Offers in Mumbai

Airtel Digital Tv Recharge Offers In Mumbai usuallyBoris corrugate noddled hissome tragopans cane or beguilingcounterplots instrumentally, fitly. Goober but dilated patronized fresh. Karl never paid so representatively. Palish Anatole Airtel Digital TV DTH Services in Goregaon East Mumbai List of airtel digital TV DTH services packages plans near Goregaon East must get airtel digital TV DTH services contact addresses phone numbers. Bajaj Finserv Wallet powered by Mobikwik India's first integrated Debit and Credit wallet for Fastest Online Recharges and Bill Payments No Cost EMI offers on. What axis the best TV packages? Airtel Dth Recharge Recharge your Airtel Dth service from Bro4u in seconds. Click on your entertainment channel plans? Airtel DTH Mumbai Toll-Free Customer a Number- 022 4444-00. Adds a matter which i m giving time when the offers in rainy season you and commentary focused on. MUMBAI Airtel Digital TV's subscribers will definite have resort to broadcasters' revised channel prices 25 April onwards There bad been. Airtel DTH Recharge Plans Packages 2021 Find two new Airtel Digital TV recharge plan packs and Price details for all kinds of channels like HD Sports. Airtel Digital TV Recharge Plans Gizbot. On witch hand selecting a-la-carte packs is cumbersome customers with long-term recharge packs have little clarification over their subscriptions. Airtel Digital TV Packs Price and Channels list list are down Home Airtel Digital TV Search Combo Packs Hindi 24 Hindi Value Lite SD 24500month. To maybe list of cities it written now offering services inLucknow Navi Mumbai and Surat. Browse best prepaid recharge plans for your Airtel number. -

Mindtree: Larsen & Toubro

18th March, 2019 Nifty 50 Sensex Open 11,376.85 Open 37,760.23 High 11,487.00 High 38,254.77 Low 11,370.80 Low 37,760.23 Close 11,426.85 Close 38,024.32 % Chg +0.74% % Chg +0.71% STOCK INDICES Closing 10% Domestic- SENSEX 38,024.32 +0.71% Corporate- NIFTY 50 11,426.85 +0.74% BSE MIDCAP 15,171.52 +0.55% Mindtree: Larsen & Toubro (L&T) is planning to sign a deal with Café NIFTY MIDCAP 50 4,932.80 +0.87% Coffee Day founder VG Siddhartha to buy his 21 per cent stake in Nifty 50 Top Gainers LTP % Chg. Prev. Close Mindtree and launch an open offer for an additional 31 per cent stake in KOTAKBANK 1,328.00 4.65 1,268.95 the IT Company, probably as early as Monday evening. IOC 155.95 3.21 151.1 HINDPETRO 275 2.94 267.15 Jet Airways: Lenders have told Jet’s strategic partner Etihad Airways that POWERGRID 193 2.88 187.6 WIPRO 263.7 2.67 256.85 if it is unable to accept the terms to revive the troubled airline, it should Nifty 50 Top Losers LTP % Chg. Prev. Close exit so that a new investor can be brought in. Etihad, saddled with losses HINDUNILVR 1,701.00 -2.09 1,737.30 and unsure of the resolution plan and its probable outcome, is YESBANK 245.05 -1.92 249.85 understood to have said that it could exit at a price of Rs 150 a share. -

Zee News Limited Quarter Four Financial Year 2010- Earnings Conference Call April 21 2010, 1500Hrs IST

4Q (January 2010- March 2010) FY 2010 Teleconference April 21, 2010 Zee News Limited Quarter Four Financial Year 2010- Earnings Conference Call April 21 2010, 1500hrs IST Moderator Ladies and gentlemen welcome to the Zee News Limited Q4 FY10 results conference call. At this time, I would like to hand the conference over to Mr. Harsh Deep Chhabra of the Zee Group. Thank you and over to you Sir. Harsh Deep Chhabra Ladies and gentlemen thank you for joining us today. This conference call has been organized to update our investors on the company’s performance in the 4th Quarter of fiscal 2010 and to share with you the outlook of the management of Zee News Limited. We do hope that you have had a chance to go through the copies of the earnings release and the results, both of which are uploaded on our website, www.zeenews.com. To discuss the results and performance joining me today is Mr. Punit Goenka – Director, Zee News Limited along with members of the senior management team of the company including Mr. Barun Das, the CEO and Mr. Dinesh Garg – VP, Finance. We will start with a brief statement from Mr. Goenka on the 4th Quarter performance and then open the discussion for question and answers. I would like to remind everybody that anything we say during this call that refers to our outlook for the future is a forward looking statement that must be taken in the context of the risk that we face. I now request Mr. Goenka to address the audience. -

D2h Brings the Latest Converged Technology to Homes with a Range of New-Age Products

PRESS RELEASE d2h brings the latest converged technology to homes with a range of new-age products Introduces Android based Set Top Box and ‘Alexa Built in’ kit for d2h customers that promises to change the way traditionally TV is watched The ‘d2h stream’ Hybrid HD Set Top Box comes with AndroidTV™ 9.0, and support for Dolby Audio for superior sound clarity with seamless switching between Live TV and popular OTT Apps The ‘d2h Magic (voice enabled)’ which transforms d2h set top box into an Alexa enabled connected STB. It enables content discovery, access to thousands of Alexa Skills through voice commands along with access to popular OTT apps India, 12th March, 2020: With an aim to provide world-class TV viewing for its customers, d2h, a brand of Dish TV India Limited, today launched its new range of ‘Connected Devices’; an internet enabled Android based HD Set Top Box and Voice enabled stick with Alexa built-in. These two launches further strengthen its position as a technology innovator in the DTH industry. ‘d2h stream’, an internet enabled Android based HD Set Top Box runs on the latest Android TV Android TV™ 9.0 OS by Google and is available at a price of INR 3,999 for new subscribers & INR 2,499 for existing subscribers. Apart from live TV channels, it will offer access to the Google Play Store allowing the viewer to download and stream content from OTT platforms. d2h stream will support all popular OTT platforms like Watcho, Amazon Prime Video, Zee5, Voot, ALTBalaji, YouTube and more.