Investing Strategically for Profitable Growth

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Company Profile

Company Profile Founded in 1806, Colgate-Palmolive is a $17.42 billion consumer products company that serves people around the world with well- known brands that make their lives healthier and more enjoyable. Colgate Brands Colgate provides oral care, personal care, home care and pet nutrition products under trusted brands such as: Colgate, Palmolive, Mennen, Softsoap, Irish Spring, Protex, Sorriso, Kolynos, Elmex, Tom’s of Maine, Ajax, Axion, Soupline, Suavitel, Hill’s Science Diet and Hill’s Prescription Diet. Operations Colgate operates in over 75 countries and sells products in over 200 countries and territories. 37,400 Colgate employees drive our success. Headquartered in New York City, Colgate operates through six divisions around the world: ® ® ® North America Latin America Europe/South Pacific Softsoap Blue- PMS 661 Silver- Foil Stamp Africa/Eurasia Asia Hill’s Pet Nutrition Six Divisions The Company has over 50 manufacturing and research facilities globally. The vast majority of Colgate products are manufactured in Colgate-owned facilities. 5 of 5854 Company Profile Business Strength Colgate Values Colgate’s success is linked to the Company’s values of Net Sales ($ millions) Caring, Global Teamwork and Continuous Improvement. 2009 $15,327 2010 $15,564 n 2011 $16,734 Caring 2012 $17,085 The Company cares about people: Colgate people, 2013 $17,420 customers, shareholders and business partners. Colgate is committed to act with compassion, integrity, honesty Dividends Paid(1) (per common share) and high ethics in all situations, to listen with respect 2009 $0.86 to others and to value differences. The Company is 2010 $1.02 also committed to protect the global environment, to 2011 $1.14 enhance the communities where Colgate people live 2012 $1.22 and work, and to be compliant with government laws 2013 $1.33 and regulations. -

COLGATE ULTRA BRITE® ADVANCED WHITENING ALL in ONE CLEAN MINT Drug Facts

COLGATE ULTRA BRITE ADVANCED WHITENING ALL IN ONE CLEAN MINT- sodium fluoride paste, dentifrice Colgate-Palmolive Company Disclaimer: Most OTC drugs are not reviewed and approved by FDA, however they may be marketed if they comply with applicable regulations and policies. FDA has not evaluated whether this product complies. ---------- COLGATE ULTRA BRITE® ADVANCED WHITENING ALL IN ONE CLEAN MINT Drug Facts Active ingredient Sodium fluoride 0.24% (0.15% w/v fluoride ion) Purpose Anticavity Use helps protect against cavities Warnings Keep out of reach of children under 6 years of age. If more than used for brushing is accidentally swallowed, get medical help or contact a Poison Control Center right away. Directions brush teeth thoroughly, preferably after adults and children 2 each meal or at least twice a day, or as years of age and older directed by a dentist or physician children 2 to 6 years use only a pea sized amount and supervise child's brushing and rinsing (to minimize swallowing) children under 2 years ask a dentist or physician Inactive ingredients sorbitol, water, hydrated silica, sodium lauryl sulfate, flavor, PEG-12, tetrasodium pyrophosphate, cocamidopropyl betaine, cellulose gum, sodium saccharin, xanthan gum, titanium dioxide Questions? 1-800-468-6502 Dist. by: COLGATE-PALMOLIVE COMPANY New York, NY 10022 PRINCIPAL DISPLAY PANEL - 170 g Tube Carton CLEAN MINT Ultra brite® ANTICAVITY FLUORIDE TOOTHPASTE WHITENS TEETH Advanced Whitening All in One Toothpaste® VALUE 30% MORE VS. 4.6 OZ SIZE NET WT 6.0 OZ (170 g) COLGATE ULTRA -

Presentation to Analysts

Colgate Palmolive India Ltd …….since 1937 Colgate Palmolive India Limited Slide 1 Disclaimer This Presentation and its related publication, release, webcast or communication (together the “Presentation”) is for general information purposes only. This Presentation does not solicit any action by Colgate-Palmolive (India) Limited (the “Company”) based on the material contained herein. Nothing in this Presentation is intended by the Company to be construed as legal, accounting, investment or tax saving advice. This Presentation includes statements that are, or may be deemed to be, “forward‐looking statements”(except for the historical information). These forward-looking statements appear in several places in the Presentation and are based on certain expectations, assumptions, anticipated developments and various other factors which are not limited to, risk and uncertainties regarding fluctuations in market share, earnings, market growth, intense competition and the pricing environment in the market, consumption level, ability to maintain and manage key business stakeholders and external factors having impact on the conduct of the business not limited to inflation, currency fluctuations, climatic changes, political and regulatory environment, Government policies and changes in international oil prices etc. The Company, therefore, in no way assures, represents, warrants, guaranty, undertake, express or imply, given that such statements, views, projections or forecasts are correct or that the objectives of the Company will be achieved as contained in the Presentation. The Company’s actual results of operations, financial condition, stability, liquidity, and the development of the industry / business sector in which the Company operates, may differ materially from those suggested by the forward‐looking statements contained in this Presentation. -

Cocamidopropyl Betaine

COCAMIDOPROPYL BETAINE Your patch test result indicates that you have a contact allergy to cocamidopropyl betaine. This contact allergy may cause your skin to react when it is exposed to this substance although it may take several days for the symptoms to appear. Typical symptoms include redness, swelling, itching and fluid-filled blisters. Where is cocamidopropyl betaine found? Cocamidopropyl betaine is used in personal care products like shampoos, hand soaps, and toothpastes, and in cosmetics as an emulsifying agent and thickener. It is also used in conditioners to reduce static cling. How can you avoid contact with cocamidopropyl betaine? Avoid products that list any of the following names in the ingredients: • 1-Propanaminium, N-(carboxymethyl)- N,N-dimethyl-3-((1-oxococonut)amino)-, hydroxide, inner salt • N-(2-Aminoethyl)-N-(2-(2- carboxyethoxy)ethyl) beta-alanine, norcoco acyl derivs., disodium salts • N-(Carboxymethyl)-N,N-dimethyl-3-((1- oxococonut)amino)-1-propanam- inium • Cocamidopropyl betaine • Cocamidopropyl dimethyl glycine • CAS RN: 61789-40-0 What are some products that may contain cocamidopropyl betaine? Anti-fungal: Shampoo/Conditioner: • Mycocide NS • Alberto VO5 Extra Body Shampoo • Alberto VO5 Herbal Escapes Moisturizing Shampoo Cosmetics: • Alberto VO5 Moisture Milks Nourishing Shampoo • Gillette Multi-Glide Shave Gel B,CPB • Alberto VO5 Normal Shampoo Hair Coloring Kits: • Aveeno Baby Wash & Shampoo • Clairol Natural Instincts Haircolor, Level 2, Hazelnut-20 • Charles Worthington Big Hair Full Volume Shampoo • -

Colgate Elects Stephen I. Sadove to Board of Directors

Colgate Elects Stephen I. Sadove To Board of Directors New York, New York, June 7, 2007... Colgate-Palmolive Company (NYSE:CL) announced today that Stephen I. Sadove, Chairman and Chief Executive Officer of Saks, Inc., has been elected to Colgate's Board of Directors. Mr. Sadove, 55, brings extensive business leadership experience and a strong marketing and consumer products background to the Colgate Board. He joined the management team of Saks as Vice Chairman in 2002 and was named Chief Operating Officer in 2004 and CEO in 2006. A member of the Saks Board of Directors since 1998, Mr. Sadove was elected Chairman in May. Mr. Sadove's strong consumer products experience began in 1975 at General Foods USA, where he held various positions of increasing responsibility, including Executive Vice President and General Manager of the Desserts Division. He joined Bristol- Myers Squibb Company in 1991 as President of Clairol in the United States and later gained additional responsibility for the consumer businesses in Canada, Europe, the Middle East, Africa, and Latin America. In 1996, he was named President of Bristol-Myers Squibb's worldwide beauty care business and was later named a senior vice president with additional responsibility for Mead Johnson Nutritionals. Mr. Sadove is a graduate of Hamilton College and holds an MBA with distinction from Harvard Business School. * * * About Colgate-Palmolive: Colgate-Palmolive is a leading global consumer products company, tightly focused on Oral Care, Personal Care, Home Care and Pet Nutrition. Colgate sells its products in over 200 countries and territories around the world under such internationally recognized brand names as Colgate, Palmolive, Mennen, Softsoap, Irish Spring, Protex, Sorriso, Kolynos, Elmex, Tom's of Maine, Ajax, Axion, Soupline, and Suavitel, as well as Hill's Science Diet and Hill's Prescription Diet. -

Executive Summary

_______________________________________Top Five Toothpaste Brands in Mumbai Executive Summary A day to day necessity of our life is toothpaste. We have variety of brands available in market. People use variety of toothpaste as per their requirement and as per their need, the main objective of using toothpaste is to keep our teeth healthy, 24 hours freshness and to avoid cavity so that we can enjoy our life as we want and we can enjoy variety of food. We have Colgate, Pepsodent, Close – up, Cibaca, Babool, Anchor, Ajanta, etc. The main objective behind making this project is to provide detail analysis of top 5 brand used in Mumbai, and to know most preferable toothpaste in south Mumbai. The top 5 brands used in Mumbai are COLGATE, PEPSODENT, CLOSE – UP, CIBACA, COLGATE FRESH ENERGY GEL. This project gives you brief introduction about Toothpaste Industry, History of Toothpaste, Industry Overview, Segments in the Industry. It includes primary and secondary information. The penetration levels of dentifrice in the country have been on an upward trend over the last few years driven by strong improvements in toothpaste penetration. In India, per capita toothpaste consumptiotion stood at 74g in 2005, which isis amongst the lowest in the world, compared to 350g and 300g in Malaysia and Vietnam respectively. Oral hygiene continues to be under aggressive competition, with sales increasing by a modest 3% in current value terms in 2006 to Rs. 2,400 crs. Toothpaste accounted for a whopping 83% of value sales. 11 _______________________________________Top Five Toothpaste Brands in Mumbai Industry analysts believe that the new threat will come from smaller players who have embraced a different kind of business model with a different value proposition. -

Fcc Terre Haute ~ Commissary List General Population Revised 04/01/13

FCC TERRE HAUTE ~ COMMISSARY LIST GENERAL POPULATION REVISED 04/01/13 NAME__________________________ REG#___________________UNIT/CELL_____________PHASE_______ INMATES ARE ALLOWED TO SHOP ONCE PER WEEK. NO REFUNDS OR EXCHANGES ON ANY ITEM. INMATES ARE RESPONSIBLE FOR FILLING OUT COMMISSARY LIST IN A LEGIBLE MANNER. ENSURE THE ITEM YOU MARK IS THE ITEM YOU WANT. UNDER NO CIRCUMSTANCES WILL ADJUSTMENTS BE MADE ON ITEMS NOT CLEARLY NUMBERED OR MARKED. INMATES MAY ONLY SHOP ON THEIR UNIT’S DESIGNATED SHOPPING DAY. SEE HOLIDAY MEMO ON TRULINCS FOR DESIGNATED SHOPPING ROTATION. PRICES SUBJECT TO CHANGE WITHOUT NOTICE. PRICE AMOUNT ITEM PRICE AMOUNT ITEM PRICE AMOUNT ITEM REQUESTED REQUESTED REQUESTED STAMPS & MISC. ICE CREAM DAIRY, FISH, MEAT CONT. ** LIMIT $9.20 WORTH OF STAMPS!** $1.85 VANILLA $1.05 BEEF STICK JACK LINKS $0.01 0.01 STAMP @ (SL) $1.85 STRAWBERRY $3.40 SWEET SUE CHICKEN $0.17 0.17 STAMP @ (SL) $1.85 BUTTER PECAN $2.05 HALAL BEEF SAUSAGE (h) $0.46 0.46 STAMP @ (SL) $2.10 CHOC. PEANUT BUTTER CHNK(k) $1.95 TACO MEAT (k)(v) $1.00 1.00 STAMP @ (SL) $1.95 ICE CREAM SNDWCH COOKIE(k) MICROWAVE,RICE $1.00 PHOTO TICKET (LIMIT 10) $3.50 PIZZA KIT $7.50 COPY CARD(LIMIT 3)@(L,SL) CANDY $1.05 VEL. MAC&CHEESE (k)(h) ELECTRONICS $2.25 SUGAR FREE LIFESAVERS $1.10 RICE, WHITE (k) $2.05 AA BATTERIES $0.85 BUTTERFINGER (k) $1.10 RICE, BROWN (k)(h) $2.05 AAA BATTERIES $0.80 HERSHEY BAR (k) $2.50 CR2016 WATCH BATTERY $1.30 TWIZZLERS (k) NUTS, SNACKS $2.50 CR2025 WATCH BATTERY $0.85 PLAIN M&M’S (k) $4.30 RAW ALMONDS (k) $69.20 MP-3 PLAYER $0.85 -

COLGATE® and MEIJER® RECYCLING CONTEST RETURNS Companies Partner with Terracycle® to Award Playground Made of Recycled Oral Care Waste

COLGATE® AND MEIJER® RECYCLING CONTEST RETURNS Companies Partner with TerraCycle® to Award Playground Made of Recycled Oral Care Waste TRENTON, N.J., (April X, 2018) –TerraCycle announces the fourth annual Recycled Playground Challenge, a contest with partners Colgate-Palmolive (“Colgate”) and Meijer, that encourages healthy habits among school children and their communities and awards a recycled playground to a winning school. Running April 22 - June 30, schools located throughout Michigan, Illinois, Indiana, Ohio, Kentucky and Wisconsin can join TerraCycle’s Oral Care Recycling Program, a free, national program run by Colgate and TerraCycle, and compete to win a new playground made completely of recycled mate- rial. Schools participating in the contest earn one ‘Playground Credit’ for each unit ("unit" defined as 0.02 lbs of used, post-consumer oral care products and packaging) of oral care waste, such as empty toothpaste tubes and floss containers, sent to TerraCycle within the timeframe. Additional Play- ground Credits are earned through online voting at www.meijer.com/colgate or www.terracycle.com/colgatemeijerplayground2018. Full set of rules for the 2018 “Recycled Playground Challenge” can be viewed at: www.terracycle.com/colgatemeijerplayground2018 The school that earns the most Playground Credits by June 30 will be announced as the winner of the grand prize playground in July 2018 before the playground installation in fall 2018. The first and second runner-up schools, as well as six honorable mention participants, will be awarded Mei- jer gift cards. Kettle Lake Elementary in Grand Rapids, Michigan was the winner of the 2017 Recy- cled Playground Challenge after earning a total of 81,697 Playground Credits. -

Q2 2021 End User Rebate Offer 4/1/2021 – 6/30/2021

Q2 2021 End User Rebate Offer 4/1/2021 – 6/30/2021 US06969A MX06813A US05981A 204917 NEW! NEW! US03563A US03574A US04206A US07326A US07327A PRODUCT CP SKU PACK DIST. REBATE ® Fabuloso Professional All Purpose Cleaner/Degreaser US06969A 4-1 gal/case $3.00 Lemon Fabuloso® All Purpose Cleaner, Lemon MX06813A 3-169 fl oz/case $3.00 Ajax® Ultra Professional Triple Action Dish Liquid US05981A 4-1 gal/case $3.00 Palmolive® Professional Original Dishwashing Liquid 204917 1-5 gal/case $4.00 Softsoap® Brand AB Hand Soap, Fresh Citrus US03563A 6/11.25 fl oz/case $1.50 Softsoap® Brand AB Hand Soap, White Tea US03574A 6/11.25 fl oz/case $1.50 Softsoap® Brand AB Hand Soap, Kitchen Fresh US04206A 6/11.25 fl oz/case $1.50 Softsoap® Brand AB Hand Soap, Sparkling Pear US07326A 6/11.25 fl oz/case $1.50 Softsoap® Brand AB Hand Soap, Clean and Protect US07327A 6/11.25 fl oz/case $1.50 IMPORTANT • Purchases must be made between 4/1/2021 and 6/30/2021 • Rebate Certificate must be redeemed by 7/31/2021 • Rebate redemption limit: NO LIMIT! • Rebate valid in U.S., Hawaii and Alaska www.colpalprofessional.com NEW! NEW! US06969A MX06813A US05981A 204917 US03563A US03574A US04206A US07326A US07327A END USER Q2 2021 REBATE CERTIFICATE # Cases Purchased SKU # Product Size Rebate per Case Total Rebate (no limit) Fabuloso® Professional All Purpose US06969A 4-1 gal/cs x $3.00 per case = Cleaner/Degreaser, Lemon MX06813A Fabuloso® All Purpose Cleaner, Lemon 4-1 gal/cs x $3.00 per case = US05981A Ajax® Ultra Professional Dish Liquid 4-1 gal/cs x $3.00 per case = 204917 -

Professional Products World Renown Brands for Powerful Results

Professional Products World Renown Brands for Powerful Results Visit our website: www.colgatecommercial.com 90054-1209 Taking steps to contribute to the environment. SCOURING CLEANSER - POWDER 7 Colgate-Palmolive is pleased to present its line of cleaning products that have been granted the EPA ‘Design for the SCOURING CLEANSER - CREME 8 Environment’ (DfE) seal. This seal is given to products that offer more positive environmental BATHROOM CLEANERS 9 characteristics than conventional ALL PURPOSE CLEANERS 10 cleaning formulations.* Look for the DfE logo throughout the catalog for products GLASS CLEANERS 15 included in the program. Visit our website — More are on the way. It’s another way MURPHY® OIL SOAP 16 that Colgate-Palmolive helps you www.colgatecommercial.com manage the risk by providing exceptional cleaning products AIR FRESHENER 17 that have been granted the DfE seal by the EPA. DISHWASHING LIQUIDS 18 Colgate Receives Recognition from the U.S. Environmental Protection Agency Colgate has been recognized by the U.S. Environmental Protection Agency (EPA) through their Design DISHWASHING POWDER 21 for the Environment Safer Detergent Stewardship Initiative (SDSI) program for our use of safer surfac- tants in personal care and home care products. Through the SDSI, the EPA’s Design for the Environment Program recognizes environmental leaders who voluntarily commit to the use of safer surfactants in Your Source For: detergents. Safer surfactants are surfactants that break down quickly to non-polluting compounds and DELIMER 21 help protect aquatic life in both fresh and salt water. Colgate is being recognized as a Champion, the highest level of recognition offered under SDSI. -

Valuación Del Capital Accionario De Colgate-Palmolive Company

Universidad de San Andrés Escuela de Negocios Maestría en Finanzas Valuación del Capital Accionario de Colgate-Palmolive Company Autor: Lucas Emiliano Reyna DNI: 32925170 Director de Tesis: Javier Epstein Buenos Aires, Julio de 2018 Universidad De San Andres Departamento De Finanzas Maestría En Finanzas Valuación del Capital Accionario de Colgate-Palmolive Company Autor: Lucas Emiliano Reyna Dni: 32.925.170 Director De Tesis: Javier Epstein Buenos Aires, Argentina - Julio De 2018 Resumen ejecutivo El presente trabajo tiene como objetivo realizar el ejercicio de valuación del capital accionario de la empresa Colgate-Palmolive Co. (NYSE:CL). A lo largo del informe, se realiza un análisis de la compañía desde el punto de vista operativo, económico y financiero, así como de las industrias en las cuales opera la empresa. En primer lugar, se describe el negocio de la compañía, los distintos segmentos de operaciones y la organización operativa. A continuación, se realiza un análisis de la industria y el posicionamiento de Colgate-Palmolive Co. dentro de la misma. En tercer lugar, se presenta un análisis financiero de compañía, dónde se estudian las ventas, las rentabilidad, y otros indicadores relevantes. Se incluye además una comparación con los principales competidores de industria. Seguidamente, se realiza el ejercicio de valuación del capital accionario de Colgate Palmolive Co. En este punto, se utiliza el método de Flujos de Fondos Descontados (DCF) para obtener el valor de la empresa (EV) y a partir del cual, sustrayendo la deuda y sumando la caja, se llega al valor del capital accionario (E). El valor obtenido en este ejercicio es 66.285 millones de dólares o 74,66 dólares por acción. -

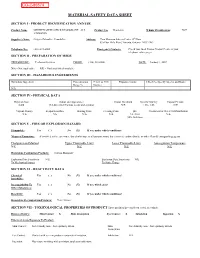

Material Safety Data Sheet

MATERIAL SAFETY DATA SHEET SECTION I - PRODUCT IDENTIFICATION AND USE Product Name MENNEN SPEED STICK DEODORANT - ALL Product Use Deodorant Whmis Classification: NCP VARIANTS Supplier’s Name Colgate-Palmolive Canada Inc. Address: Two Morneau Sobeco Centre, 6th Floor 895 Don Mills Road, Toronto, Ontario M3C 1W3 Telephone No.: (416) 421-6000 Emergency Contacts: Check your local Poison Control Centre in your telephone white pages. SECTION II - PREPARATION OF MSDS PREPARED BY: Technical Services PHONE: (416) 421-6000 DATE: January 1, 2007 N/A = Not Applicable; N/E = Not Established/Available SECTION III - HAZARDOUS INGREDIENTS Hazardous Ingredient Concentration C.A.S. or U.N. Exposure Limits LD50/LC50 Specify Species and Route Range % Number N/A SECTION IV - PHYSICAL DATA Physical State Odour and Appearance Odour Threshold Specific Gravity Vapour Pressure Solid Gel-like solid (Various scents and colours) N/E 1.00 - 1.05 N/E Vapour Density Evaporation Rate Boiling Point Freezing Point pH Coefficient of Water/Oil Distribution N/E N/E N/A N/A 9.0 - 10.0 N/A (10% Solution) SECTION V - FIRE OR EXPLOSION HAZARD Flammable: Yes ( ) No (X) If yes, under which conditions: Means of Extinction: If involved in fire, use water, dry alcohol type or all purpose foam, dry chemical, carbon dioxide or other Class B extinguishing agents. Flashpoint and Method Upper Flammable Limit Lower Flammable Limit Auto-ignition Temperature N/E N/E N/E N/E Hazardous Combustion Products: Carbon Monoxide Explosion Data Sensitivity N/E Explosion Data Sensitivity N/E To Mechanical Impact To Static Charge SECTION VI - REACTIVITY DATA Chemical Yes ( ) No (X) If yes, under which conditions? Instability: Incompatibility To Yes ( ) No (X) If yes, which ones? Other Substances: Reactivity: Yes ( ) No (X) If yes, under which conditions? Hazardous Decomposition Products: None known SECTION VII - TOXICOLOGICAL PROPERTIES OF PRODUCT These products have not been tested as a whole.