Spanish Broadcasting System, Inc. (Exact Name of Registrant As Specified in Its Charter)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Public Notice >> Licensing and Management System Admin >>

REPORT NO. PN-1-200116-01 | PUBLISH DATE: 01/16/2020 Federal Communications Commission 445 12th Street SW PUBLIC NOTICE Washington, D.C. 20554 News media info. (202) 418-0500 APPLICATIONS File Number Purpose Service Call Sign Facility ID Station Type Channel/Freq. City, State Applicant or Licensee Status Date Status 0000097316 Renewal of FM WNRT 36195 Main 96.9 MANATI, PR LA VOZ EVANGELICA 01/14/2020 Received License DE PUERTO RICO, INC. Amendment 0000097397 Renewal of FM KHOM 6619 Main 100.9 SALEM, AR E-COMMUNICATIONS, 01/14/2020 Accepted License LLC For Filing 0000097418 Renewal of FM WMXI 54655 Main 98.1 LAUREL, MS EAGLE BROADCASTING 01/14/2020 Accepted License LLC For Filing 0000097117 Renewal of FM KUCA 69401 Main 91.3 CONWAY, AR University of Central 01/14/2020 Accepted License Arkansas Board of For Filing Trustees 0000097283 Renewal of AM WVLD 69647 Main 1450.0 VALDOSTA, GA SOUTHERN 01/14/2020 Received License COMMUNICATIONS, LLC Amendment 0000097371 Renewal of FM WESP 6891 Main 102.5 DOTHAN, AL ALABAMA MEDIA, LLC 01/14/2020 Received License Amendment 0000097146 Renewal of AM WCNN 56389 Main 680.0 NORTH ATLANTA DICKEY 01/14/2020 Received License , GA BROADCASTING Amendment COMPANY Page 1 of 17 REPORT NO. PN-1-200116-01 | PUBLISH DATE: 01/16/2020 Federal Communications Commission 445 12th Street SW PUBLIC NOTICE Washington, D.C. 20554 News media info. (202) 418-0500 APPLICATIONS File Number Purpose Service Call Sign Facility ID Station Type Channel/Freq. City, State Applicant or Licensee Status Date Status 0000097241 Renewal of AM WPBR 50333 Main 1340.0 LANTANA, FL PALM BEACH RADIO 01/14/2020 Received License GROUP LLC Amendment 0000097185 Renewal of AM WQSC 34590 Main 1340.0 CHARLESTON, KIRKMAN 01/14/2020 Received License SC BROADCASTING, INC. -

Draft Copy « License Modernization «

Approved by OMB (Office of Management and Budget) | OMB Control Number 3060-0113 (REFERENCE COPY - Not for submission) Broadcast Equal Employment Opportunity Program Report FRN: 0003736220 File Number: 0000082758 Submit Date: 09/30/2019 Call Sign: WODA Facility ID: 54471 City: BAYAMON State: PR Service: Full Power FM Purpose: EEO Report Status: Received Status Date: 09/30/2019 Filing Status: Active General Section Question Response Information Application Description Description of the application (255 characters max.) is EEO Program Report for all visible only to you and is not part of the submitted SBS Puerto Rico Stations application. It will be displayed in your Applications workspace. Attachments Are attachments (other than associated schedules) being Yes filed with this application? Licensee Name, Type and Contact Information Licensee Information Applicant Applicant Address Phone Email Type SPANISH BROADCASTING SYSTEM 7007 NW +1 (305) PJASPAR@SBSCORPORATE. Company HOLDING COMPANY, INC. 77TH AVE. 441-6901 COM Doing Business As: SPANISH BROADCASTING MIAMI, FL SYSTEM HOLDING COMPANY, INC. 33166 United States Contact Contact Name Address Phone Email Contact Type Representatives Nancy A Ory 2001 L Street, NW +1 (202) 416- NORY@LERMANSENTER. Legal Member Washington, DC 6791 COM Representative Lerman Senter 20036 PLLC United States Common Facility Identifier Call Sign City State Time Brokerage Agreement Stations 1890 WEGM SAN GERMAN PR No 53554 WNOD MAYAGUEZ PR No 54471 WODA BAYAMON PR No 32157 WMEG GUAYAMA PR No 8153 WIOB MAYAGUEZ PR -

Eeo Public File Report

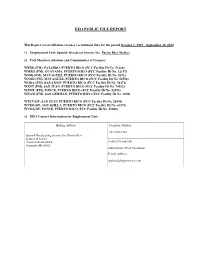

EEO PUBLIC FILE REPORT This Report covers full-time vacancy recruitment data for the period October 1, 2019 – September 30, 2020 1) Employment Unit: Spanish Broadcast System, Inc. Puerto Rico Market 2) Unit Members (Stations and Communities of License): WRXD (FM), FAJARDO, PUERTO RICO (FCC Facility ID No. 51428) WMEG (FM), GUAYAMA, PUERTO RICO (FCC Facility ID No. 32157) WIOB (FM), MAYAGUEZ, PUERTO RICO (FCC Facility ID No. 8153) WNOD (FM), MAYAGUEZ, PUERTO RICO (FCC Facility ID No. 53554) WODA (FM), BAYAMON, PUERTO RICO (FCC Facility ID No. 54471) WZNT (FM), SAN JUAN, PUERTO RICO (FCC Facility ID No. 74552) WZMT (FM), PONCE, PUERTO RICO (FCC Facility ID No. 53076) WEGM (FM), SAN GERMAN, PUERTO RICO (FCC Facility ID No. 1890) WTCV-DT, SAN JUAN, PUERTO RICO (FCC Facility ID No. 28954) WVEO-DT, AGUADILLA, PUERTO RICO (FCC Facility ID No. 61573) WVOZ-DT, PONCE, PUERTO RICO (FCC Facility ID No. 29000) 3) EEO Contact Information for Employment Unit: Mailing Address: Telephone Number: (787) 622-9700 Spanish Broadcasting System, Inc/ Puerto Rico Frances St Lot 42 Amelia Industrial Park Contact Person/Title: Guaynabo PR 00969 Sixto Pabón, VP of Operations E-mail Address: [email protected] 4) List all Full-Time Job Vacancies Filled by Each Station in the Employment Unit: Job Title Recruitment Source Referring Hire Promotions Producer Rehire 5) Job Title: Promotions Producer Referral Source(s) of Hiree: Rehire Name of Organization Contact Address Telephone # of Did Recruitment Interviewees Source Request Notified of Job Vacancy Person Number Referred Notification? (Yes or No) Referral/Rehire N/A N/A N/A 1 Yes 6) Total # of Interviewees / Referred: For the period from October 1, 2019 through September 30, 2020, this Employment Unit interviewed 1 interviewee for full-time job vacancies. -

Stations Monitored

Stations Monitored 10/01/2019 Format Call Letters Market Station Name Adult Contemporary WHBC-FM AKRON, OH MIX 94.1 Adult Contemporary WKDD-FM AKRON, OH 98.1 WKDD Adult Contemporary WRVE-FM ALBANY-SCHENECTADY-TROY, NY 99.5 THE RIVER Adult Contemporary WYJB-FM ALBANY-SCHENECTADY-TROY, NY B95.5 Adult Contemporary KDRF-FM ALBUQUERQUE, NM 103.3 eD FM Adult Contemporary KMGA-FM ALBUQUERQUE, NM 99.5 MAGIC FM Adult Contemporary KPEK-FM ALBUQUERQUE, NM 100.3 THE PEAK Adult Contemporary WLEV-FM ALLENTOWN-BETHLEHEM, PA 100.7 WLEV Adult Contemporary KMVN-FM ANCHORAGE, AK MOViN 105.7 Adult Contemporary KMXS-FM ANCHORAGE, AK MIX 103.1 Adult Contemporary WOXL-FS ASHEVILLE, NC MIX 96.5 Adult Contemporary WSB-FM ATLANTA, GA B98.5 Adult Contemporary WSTR-FM ATLANTA, GA STAR 94.1 Adult Contemporary WFPG-FM ATLANTIC CITY-CAPE MAY, NJ LITE ROCK 96.9 Adult Contemporary WSJO-FM ATLANTIC CITY-CAPE MAY, NJ SOJO 104.9 Adult Contemporary KAMX-FM AUSTIN, TX MIX 94.7 Adult Contemporary KBPA-FM AUSTIN, TX 103.5 BOB FM Adult Contemporary KKMJ-FM AUSTIN, TX MAJIC 95.5 Adult Contemporary WLIF-FM BALTIMORE, MD TODAY'S 101.9 Adult Contemporary WQSR-FM BALTIMORE, MD 102.7 JACK FM Adult Contemporary WWMX-FM BALTIMORE, MD MIX 106.5 Adult Contemporary KRVE-FM BATON ROUGE, LA 96.1 THE RIVER Adult Contemporary WMJY-FS BILOXI-GULFPORT-PASCAGOULA, MS MAGIC 93.7 Adult Contemporary WMJJ-FM BIRMINGHAM, AL MAGIC 96 Adult Contemporary KCIX-FM BOISE, ID MIX 106 Adult Contemporary KXLT-FM BOISE, ID LITE 107.9 Adult Contemporary WMJX-FM BOSTON, MA MAGIC 106.7 Adult Contemporary WWBX-FM -

Directorio De Medios De Puerto Rico

Directorio de Medios de Puerto Rico El Directorio más completo y mejor actualizado de Puerto Rico Agencias de noticias Agencia EFE, Cobian´s Plaza, Oficina 214 Santurce, PR, 00910, 787-723-6023 T, 787- 725-8651 F, [email protected]. CyberNews, Apartado Postal 12043, SJ, PR, 00914, 787-644-8418 T y 787-603-6653 T, cybernewspr.com, [email protected], [email protected]. Inter News Service, Apartado 9023025, San Juan, Puerto Rico 00902-3025. 787-368- 6353 T, [email protected], internewsservice.com Prensa Asociada - AP, Metro Office Park, Edif. 8, Calle 1, Suite 108, Guaynabo, PR 00968, 787-793-5833 T, 787-783-4425 F, [email protected] RMAsociadosPR.com, Calle 2-A10, Berwind Estates, Rio Piedras P.R. 00924, rmasociadospr.com, [email protected], [email protected] Diarios de circulación nacional El Nuevo Día, Apartado Postal 9067512, SJ, PR 00906-7512, 641-8000 (Cuadro), 641- 7600 (Redacción), 641-3924 F (Redacción), 641-3927 F (Por Dentro), endi.com, [email protected], [email protected] El Vocero, Apartado Postal 9067515, San Juan de PR 00906-7515, 721-2300 T, 787- 622-7483 y 787-725-8422 F, Escenario: 787-724-8438 F, vocero.com, [email protected] Primera Hora, Apartado 2009, Cataño, PR 00963-2009, 641-5454 T, 641-4472 F, primerahora.com, [email protected], [email protected] Puerto Rico Daily Sun, Urb. La Riviera, 943 de Diego Ave. Río Piedras, 00921, Apartado Postal 364302, San Juan, PR 00936-4302, 787-969-3477, 787-969-3479 y 787- 969-3480 T, 1-866-641-4557 y 787-749-4839 F, [email protected] Semanarios de circulación nacional Bandera Roja, Apartado 22699, Estación UPR, San Juan, Puerto Rico 00931-2699, 1 [email protected], [email protected], bandera.org [Mensual] Caribbean Business, Apartado Postal 12130, San Juan, PR 00914-0130, 728-3000 ext. -

Inside This Issue

News Serving DX’ers since 1933 Volume 82, No. 3● November 3, 2014● (ISSN 0737-1639) Inside this issue . 2 … AM Switch 19 … International DX Digest 23 … Space Weather Forecast 7 … Domestic DX Digest West 22 … Membership Report 23 … Unreported Stations 14 … Domestic DX Digest East 23 … Musings of the Members 24 … Back Page DX TEST: WSPO‐1390 Charleston SC will You’ll be greatly missed for your wit, wisdom, conduct a DX test on Monday, November 10, and patience, Ken. 2014, at 0000‐0100 ELT. The test will run at full Any club member in good standing may apply day power of 5 kW and will consist of distinctive to be a member of the NRC Board of Directors. audio clips, Morse code, and sweep tones. You’ll need to have Internet access and reliable e‐ Reception reports (including return postage) mail, plus a phone, as most of our may be sent to Mr. Bruce Roberts (KI4YST), communication is accomplished very quickly Director of Engineering, Apex Broadcasting, 2294 and not via snail mail. To apply, send a short Clements Ferry Rd., Charleston SC 29492. statement as to how long you’ve been a club Many thanks to J.D. Stephens for arranging member and why you wish to volunteer to the test and to Bruce Roberts at WSPO for become a BoD member to BoD chairman Paul making the test Swearingen: [email protected] by possible. (Via December 15. Thanks! Paul Brandon Jordan, RIP: Graham Maynard, a noted British MW IRCA/NRC DX DXer, passed away on October 6. -

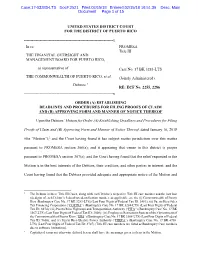

Case:17-03283-LTS Doc#:2521 Filed:02/15/18 Entered:02/15/18 16:51:39 Desc: Main Document Page 1 of 15

Case:17-03283-LTS Doc#:2521 Filed:02/15/18 Entered:02/15/18 16:51:39 Desc: Main Document Page 1 of 15 UNITED STATES DISTRICT COURT FOR THE DISTRICT OF PUERTO RICO --------------------------------------------------------------------x In re: PROMESA Title III THE FINANCIAL OVERSIGHT AND MANAGEMENT BOARD FOR PUERTO RICO, as representative of Case No. 17 BK 3283-LTS THE COMMONWEALTH OF PUERTO RICO, et al. (Jointly Administered) Debtors.1 RE: ECF No. 2255, 2286 --------------------------------------------------------------------x ORDER (A) ESTABLISHING DEADLINES AND PROCEDURES FOR FILING PROOFS OF CLAIM AND (B) APPROVING FORM AND MANNER OF NOTICE THEREOF Upon the Debtors’ Motion for Order (A) Establishing Deadlines and Procedures for Filing Proofs of Claim and (B) Approving Form and Manner of Notice Thereof, dated January 16, 2018 (the “Motion”);2 and the Court having found it has subject matter jurisdiction over this matter pursuant to PROMESA section 306(a); and it appearing that venue in this district is proper pursuant to PROMESA section 307(a); and the Court having found that the relief requested in the Motion is in the best interests of the Debtors, their creditors, and other parties in interest; and the Court having found that the Debtors provided adequate and appropriate notice of the Motion and 1 The Debtors in these Title III Cases, along with each Debtor’s respective Title III case number and the last four (4) digits of each Debtor’s federal tax identification number, as applicable, are the (i) Commonwealth of Puerto Rico (Bankruptcy Case No. 17 BK 3283-LTS) (Last Four Digits of Federal Tax ID: 3481); (ii) Puerto Rico Sales Tax Financing Corporation (“COFINA”) (Bankruptcy Case No. -

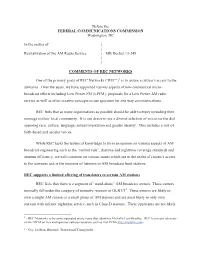

Revitalization of the AM Radio Service ) ) ) )

Before the FEDERAL COMMUNICATIONS COMMISSION Washington, DC In the matter of: ) ) Revitalization of the AM Radio Service ) MB Docket 13-249 ) ) COMMENTS OF REC NETWORKS One of the primary goals of REC Networks (“REC”)1 is to assure a citizen’s access to the airwaves. Over the years, we have supported various aspects of non-commercial micro- broadcast efforts including Low Power FM (LPFM), proposals for a Low Power AM radio service as well as other creative concepts to use spectrum for one way communications. REC feels that as many organizations as possible should be able to enjoy spreading their message to their local community. It is our desire to see a diverse selection of voices on the dial spanning race, culture, language, sexual orientation and gender identity. This includes a mix of faith-based and secular voices. While REC lacks the technical knowledge to form an opinion on various aspects of AM broadcast engineering such as the “ratchet rule”, daytime and nighttime coverage standards and antenna efficiency, we will comment on various issues which are in the realm of citizen’s access to the airwaves and in the interests of listeners to AM broadcast band stations. REC supports a limited offering of translators to certain AM stations REC feels that there is a segment of “stand-alone” AM broadcast owners. These owners normally fall under the category of minority, women or GLBT/T2. These owners are likely to own a single AM station or a small group of AM stations and are most likely to only own stations with inferior nighttime service, such as Class-D stations. -

Communications Status Report for Areas Impacted by Hurricane Maria October 23, 2017

Communications Status Report for Areas Impacted by Hurricane Maria October 23, 2017 The following is a report on the status of communications services in geographic areas impacted by Hurricane Maria as of October 23, 2017 at 11:00 AM EDT. This report incorporates network outage data submitted by communications providers to the Federal Communications Commission’s Disaster Information Reporting System (DIRS). DIRS is currently activated for all counties in Puerto Rico and the U.S. Virgin Islands. Note that the operational status of communications services during a disaster may evolve rapidly, and this report represents a snapshot in time. It should also be noted that some communications providers have not yet reported in DIRS, so outage information almost certainly is not complete. The following counties are in the geographic area that was covered by the DIRS activation as of this morning (the “disaster area”). Puerto Rico: Adjuntas, Aguada, Aguadilla, Aguas Buenas, Aibonito, Anasco, Arecibo, Arroyo, Barceloneta, Barranquitas, Bayamon, Cabo Rojo, Caguas, Camuy, Canovanas, Carolina, Catano, Cayey, Ceiba, Ciales, Cidra, Coamo, Comerio, Corozal, Culebra, Dorado, Fajardo, Florida, Guanica, Guayama, Guayanilla, Guaynabo, Gurabo, Hatillo, Hormigueros, Humacao, Isabela, Jayuya, Juana Diaz, Juncos, Lajas, Lares, Las Marias, Las Piedras, Loiza, Luquillo, Manati, Maricao, Maunabo, Mayaguez, Moca, Morovis, Naguabo, Naranjito, Orocovis, Patillas, Penuelas, Ponce, Quebradillas, Rincon, Rio Grande, Sabana Grande, Salinas, San German, San Juan, San Lorenzo, San Sebastian, Santa Isabel, Toa Alta, Toa Baja, Trujillo Alto, Utuado, Vega Alta, Vega Baja, Vieques, Villalba, Yabucoa and Yauco U.S. Virgin Islands: St. Croix, St. John, St. Thomas 911 Services The Public Safety and Homeland Security Bureau (PSHSB) learns the status of each Public Safety Answering Point (PSAP) through the filings of 911 Service Providers in DIRS, reporting to the FCC’s Public Safety Support Center (PSSC), coordination with state 911 Administrators, and, if necessary, from individual PSAPs. -

[email protected] • • 1.888

[email protected] • www.hispanicprwire.com • 1.888.776.0942 http://www.prnewswire.com/products-services/distribution/usmedia/multicultural-communications-2.html HISPANIC PR WIRE General National Media Points ¡Que Onda! Magazine ¡Qué Pasa! Magazine 20 De Mayo 4to Poder 809RD La Revista! AARP Segunda Juventud Acento Latino Magazine Acontecer Latino Actual Magazine Actualidad hispana Adelante Valle Agence France-Presse Agencia de Coberturas Comunitarias Agencia EFE AHAA Newsletter Ahora News Al Borde Al Día Alabama en Español Alaska en Español Alianza Metropolitan News Americas Quarterly Arizona en Español News Arkansas en Español News Armando F. Sanchez Podcast Program Asociación de la Prensa de Madrid Automóvil Panamericano Avance Hispano Ayuda Total Azteca América Banda Oriental Latinoamerica BBC Mundo BBC World Service Bell Gardens Sun Bienvenidos Press Birmingham Latino Bronx Latino Buenos Días Nebraska Café Fuerte California en Español News Cambalache Newspaper Caracol América Caribbean Business Carnetec [email protected] • www.hispanicprwire.com • 1.888.776.0942 http://www.prnewswire.com/products-services/distribution/usmedia/multicultural-communications-2.html Catalina Magazine Catholic Herald Magazine CENTRO Mi Diario Ch. 34 Univisión City Terrace Comet Claridad Clear Channel CNN en Español CNNExpansión CNY Latino Colorado en Español ColorLines Comenzando el Día Commerce Comet Con Alma y Corazón Conexiones International Conneticut en Español Constru-Guia al Dia CONTACTO Magazine Cosmopolitan for Latinas CRONICAS -

Complimentary SUMMER 1988

Complimentary SUMMER 1988 C H I C A G O L A N D Your Complete Guide to Local Radio Over 100 metropolitan, suburban and regional stations. Published by MEDIA TIES u Tms Requestse Business Box 2215 -W 8014 W. 27th Street Westmont, IL 60559 North Riverside, IL (312) 442 -4444 60546 CHICAGOLAND RADIO WAVES. Published by MediaTies. Copyright 1988 Media Ties. All rights reserved. Publisher S.J. Peters Executive Vice- President Gary Wilt Art Director Matt Cerra Photography /Operations Tom Kubaszak Media Coordinator Stephen Dynako Distribution Coordinator Paul Schultz Special thanks to Carrie Peters, Marie Smelhaus, Denise Stief, Marty Zivin, Rivian B. Sarwer, Wayne Magdziarz, Vera Wilt. AN INVITATION TO CHICAGOLAND RADIO WAVES Your complete free guide to local radio, published quarterly (as the seasons change) by S.J. Peters and Media Ties, North Riverside, Illinois. PREMISE Over 110 radio stations fill the dials across metropolitan, suburban and regional Chicagoland, offering a rich mix of programming suited to practically any interest, taste, culture, mood and need. Created and committed to advise consumers on the wide array of available radio listening choices, CHICAGOLAND RADIO WAVES provides this unique yet logical and carefully researched service free. Our editorial policy is to inform and entertain, not to criticize. As we embark upon our third issue, we're pleased to report intense reader/listener popularity, strong support from Chicagoland radio stations, and growing interest by the business community. The question: how to find out what's on the radio? The only answer is RADIO WAVES. CIRCULATION Each issue of Chicagoland Radio Waves is available at no cost through select retail outlets, community and business organizations, auto rental and service agencies, hotels, realtors, convention bureaus, radio stations, and at certain public and private events. -

530 CIAO BRAMPTON on ETHNIC AM 530 N43 35 20 W079 52 54 09-Feb

frequency callsign city format identification slogan latitude longitude last change in listing kHz d m s d m s (yy-mmm) 530 CIAO BRAMPTON ON ETHNIC AM 530 N43 35 20 W079 52 54 09-Feb 540 CBKO COAL HARBOUR BC VARIETY CBC RADIO ONE N50 36 4 W127 34 23 09-May 540 CBXQ # UCLUELET BC VARIETY CBC RADIO ONE N48 56 44 W125 33 7 16-Oct 540 CBYW WELLS BC VARIETY CBC RADIO ONE N53 6 25 W121 32 46 09-May 540 CBT GRAND FALLS NL VARIETY CBC RADIO ONE N48 57 3 W055 37 34 00-Jul 540 CBMM # SENNETERRE QC VARIETY CBC RADIO ONE N48 22 42 W077 13 28 18-Feb 540 CBK REGINA SK VARIETY CBC RADIO ONE N51 40 48 W105 26 49 00-Jul 540 WASG DAPHNE AL BLK GSPL/RELIGION N30 44 44 W088 5 40 17-Sep 540 KRXA CARMEL VALLEY CA SPANISH RELIGION EL SEMBRADOR RADIO N36 39 36 W121 32 29 14-Aug 540 KVIP REDDING CA RELIGION SRN VERY INSPIRING N40 37 25 W122 16 49 09-Dec 540 WFLF PINE HILLS FL TALK FOX NEWSRADIO 93.1 N28 22 52 W081 47 31 18-Oct 540 WDAK COLUMBUS GA NEWS/TALK FOX NEWSRADIO 540 N32 25 58 W084 57 2 13-Dec 540 KWMT FORT DODGE IA C&W FOX TRUE COUNTRY N42 29 45 W094 12 27 13-Dec 540 KMLB MONROE LA NEWS/TALK/SPORTS ABC NEWSTALK 105.7&540 N32 32 36 W092 10 45 19-Jan 540 WGOP POCOMOKE CITY MD EZL/OLDIES N38 3 11 W075 34 11 18-Oct 540 WXYG SAUK RAPIDS MN CLASSIC ROCK THE GOAT N45 36 18 W094 8 21 17-May 540 KNMX LAS VEGAS NM SPANISH VARIETY NBC K NEW MEXICO N35 34 25 W105 10 17 13-Nov 540 WBWD ISLIP NY SOUTH ASIAN BOLLY 540 N40 45 4 W073 12 52 18-Dec 540 WRGC SYLVA NC VARIETY NBC THE RIVER N35 23 35 W083 11 38 18-Jun 540 WETC # WENDELL-ZEBULON NC RELIGION EWTN DEVINE MERCY R.