Holocaust Era Insurance Restitution After Icheic

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Participants

JUNE 26–30, Prague • Andrzej Kremer, Delegation of Poland, Poland List of Participants • Andrzej Relidzynski, Delegation of Poland, Poland • Angeles Gutiérrez, Delegation of Spain, Spain • Aba Dunner, Conference of European Rabbis, • Angelika Enderlein, Bundesamt für zentrale United Kingdom Dienste und offene Vermögensfragen, Germany • Abraham Biderman, Delegation of USA, USA • Anghel Daniel, Delegation of Romania, Romania • Adam Brown, Kaldi Foundation, USA • Ann Lewis, Delegation of USA, USA • Adrianus Van den Berg, Delegation of • Anna Janištinová, Czech Republic the Netherlands, The Netherlands • Anna Lehmann, Commission for Looted Art in • Agnes Peresztegi, Commission for Art Recovery, Europe, Germany Hungary • Anna Rubin, Delegation of USA, USA • Aharon Mor, Delegation of Israel, Israel • Anne Georgeon-Liskenne, Direction des • Achilleas Antoniades, Delegation of Cyprus, Cyprus Archives du ministère des Affaires étrangères et • Aino Lepik von Wirén, Delegation of Estonia, européennes, France Estonia • Anne Rees, Delegation of United Kingdom, United • Alain Goldschläger, Delegation of Canada, Canada Kingdom • Alberto Senderey, American Jewish Joint • Anne Webber, Commission for Looted Art in Europe, Distribution Committee, Argentina United Kingdom • Aleksandar Heina, Delegation of Croatia, Croatia • Anne-Marie Revcolevschi, Delegation of France, • Aleksandar Necak, Federation of Jewish France Communities in Serbia, Serbia • Arda Scholte, Delegation of the Netherlands, The • Aleksandar Pejovic, Delegation of Monetenegro, Netherlands -

Me Israel Aestra JULU 3-QUGUSU 8 1979 Me Israel Assam Founoed Bu A.Z

me Israel Aestra JULU 3-QUGUSU 8 1979 me Israel Assam FOunoeD bu a.z. ppopes JULU 3-aUGUSB 8 1979 Member of the European Association of Music Festivals Executive Committee: Asher Ben-Natan, Chairman Honorary Presidium: ZEVULUN HAMMER - Minister of Education and Culture Menahem Avidom GIDEON PATT - Minister of Industry, Trade and Tourism Gary Bertini TEDDY KOLLEK - Mayor of Jerusalem Jacob Bistritzky Gideon Paz SHLOMO LAHAT - Mayor of Tel Aviv-Yafo Leah Porath Ya'acov Mishori Jacob Steinberger J. Bistritzky Director, the Israel Festival. Director, The Arthur Rubinstein International Piano Master Competition. Thirty years of professional activity in Artistic Advisor — Prof. Gary Bertini the field of culture and arts, as Director of the Department of International The Public Committee and Council: Cultural Relations in the Ministry of Gershon Achituv Culture and Arts, Warsaw; Director of the Menahem Avidom Polish Cultural Institute, Budapest: Yitzhak Avni Director of the Frédéric Chopin Institute, Warsaw. Mr. Bistritzky's work has Mordechai Bar On encompassed all aspects of the Asher Ben-Natan Finance Committee: development of culture, the arts and mass Gary Bertini Menahem Avidom, Chairman media: promotion, organization and Jacob Bistritzky Yigal Shaham management of international festivals and Abe Cohen Micha Tal competitions. Organizer of Chopin Sacha Daphna competitions in Warsaw and International Meir de-Shalit Chopin year 1960 under auspices of Walter Eytan Festival Staff: U.N.E.S.C.O. Shmuel Federmann Assistant Director: Ilana Parnes Yehuda Fickler Director of Finance: Isaac Levinbuk Daniel Gelmond Secretariat: Rivka Bar-Nahor, Paula Gluck Dr. Reuven Hecht Public Relations: Irit Mitelpunkt Dr. Paul J. -

MS 315 A1076 Papers of Clemens Nathan Scrapbooks Containing

1 MS 315 A1076 Papers of Clemens Nathan Scrapbooks containing newspaper cuttings, correspondence and photographs from Clemens Nathan’s work with the Anglo-Jewish Association (AJA) 1/1 Includes an obituary for Anatole Goldberg and information on 1961-2, 1971-82 the Jewish youth and Soviet Jews 1/2 Includes advertisements for public meetings, information on 1972-85 the Middle East, Soviet Jews, Nathan’s election as president of the Anglo-Jewish Association and a visit from Yehuda Avner, ambassador of the state of Israel 1/3 Including papers regarding public lectures on human rights 1983-5 issues and the Nazi war criminal Adolf Eichmann, the Middle East, human rights and an obituary for Leslie Prince 1/4 Including papers regarding the Anglo-Jewish Association 1985-7 (AJA) president’s visit to Israel, AJA dinner with speaker Timothy Renton MP, Minister of State for the Foreign and Commonwealth Office; Kurt Waldheim, president of Austria; accounts for 1983-4 and an obituary for Viscount Bearsted Papers regarding Nathan’s work with the Consultative Council of Jewish Organisations (CCJO) particularly human rights issues and printed email correspondence with George R.Wilkes of Gonville and Cauis Colleges, Cambridge during a period when Nathan was too ill to attend events and regarding the United Nations sub- commission on human right at Geneva. [The CCJO is a NGO (Non-Governmental Organisation) with consultative status II at UNESCO (the United National Education, Scientific and Cultural Organisation)] 2/1 Papers, including: Jan -Aug 1998 arrangements -

SFU Thesis Template Files

From Militant to Military: The Ambivalent Politics of Liberal Feminism in the American War on Terror by Amanda Liao B.A., McGill University, 2013 Extended Essay Submitted in Partial Fulfillment of the Requirements for the Degree of Master of Arts in the School of Communication (Dual Degree Program in Global Communication) Faculty of Communication, Art and Technology Amanda Liao 2015 SIMON FRASER UNIVERSITY Summer 2015 Approval Name: Amanda Liao Degree: Master of Arts (Communication) Title: From Militant to Military: The Ambivalent Politics of Liberal Feminism in the American War on Terror Supervisory Committee: Program Director: Yuezhi Zhao Professor Zoë Druick Senior Supervisor Associate Professor Jie Gu Senior Supervisor Associate Professor The Institute of Communication Studies Communication University of China Date Approved: August 07, 2015 ii Abstract The widespread use of feminist, human rights, and international development discourse for justifying military intervention is part of a long and storied tradition of imperial feminism – a tradition which is deeply embedded into the normative Western ideologies of neoliberalism and modernization. However, the narrative of feminism that has been appropriated by the US military in order to justify the war on terror is that of liberal feminism; it is a discourse of feminism that privileges a white, middle-class, Western audience. In other words, it is blind to the historically disproportionate experience of oppression faced by women of colour. On a global scale, liberal feminism undermines the agency of women’s movements in the global south by assuming the universality – as well as the superiority – of Western human rights discourse. This paper will examine how the liberal feminist discourse became a dominant narrative in the war on terror. -

Bank of Israel

BANK OF ISRAEL The Government and Finance Committee of the Knesset Jerusalem In accordance with sections 59 and 60 of the Bank of Israel Law, 57141954, I respectfully submit herewith the Annual Report of the Bank of Israel for the year 1975. The Report is based on material prepared by the Research Department of the Bank. Most of the statistical data in Parts One and Two were supplied by the Central Bureau of Statistics. Some of the statistical information on which the 1974 Report and the 1976 National Budget were based was recently revised, and consequently some of the data in this Report have also been revised, with the changes being of more than a mere technical nature. As in the two preceding years, developments in 1975 were not even. There were sharp fluctuations in the level of economic activity and in several major economic variables. This was due partly to exogenous factors, especially the slump and subsequent recovery of world trade, and partly to deliberate government policy and the public's response to the measures introduced. In 1975 the economy had to grapple with the balance of payments problem, which occupies a prominent place in this Report. The main conclusion emerging from an analysis of developments in 1975 is that the positive results of the government's actionthe curbing of private consumption, a slight contraction of the real import surplus, and some weakening of inf lationwere far from adequate, given the dimensions and gravity of the balance of payments situation. The crucial question facing the economy remains the checking of import growth, and even more, the rapid expansion of exports. -

A Plan for Allocating Successor Organization Resources

A Plan for Allocating Successor Organization Resources Report of the Planning Committee, Conference On Jewish Material Claims Against Germany June 28, 2000 25 Sivan 5760 1 Rabbi Israel Miller, President, Conference On Jewish Material Claims Against Germany 15 East 26 Street New York, New York Dear Israel, I am pleased to enclose A Plan for Allocating Successor Organization Resources, the report of the distinguished Planning Committee which I have had the honor of chairing. The Committee has completed a thoughtful ten-month process, carefully reviewing the issues and exploring a variety of options before coming to the conclusions contained in this document. We trust that you will bring these recommendations to the Board of Directors of the Claims Conference for review and action. Through this experience, I have become convinced that the work of the Claims Conference is not adequately understood or appreciated. I hope that this report and the results of this planning process will help dispel the confusion about the past and future achievements of the Claims Conference. No amount of money can compensate for the destruction of innocent human beings and thriving communities or the decimation of the Jewish people as a whole by the Nazis. We can try to use available resources - specifically the proceeds of the sale of communal and unclaimed property in the former East Germany - to respond to the most critical needs related to the consequences of the Shoah. This is what the enclosed Plan tries to accomplish. I want to thank the members of the Committee who came from near and far for their attendance and commitment, and for the high quality of their participation. -

Senate the Senate Met at 9:45 A.M

E PL UR UM IB N U U S Congressional Record United States th of America PROCEEDINGS AND DEBATES OF THE 108 CONGRESS, SECOND SESSION Vol. 150 WASHINGTON, TUESDAY, SEPTEMBER 14, 2004 No. 109 Senate The Senate met at 9:45 a.m. and was U.S. SENATE, ple to come in late. In order to finish called to order by the Honorable LIN- PRESIDENT PRO TEMPORE, the bill, especially as we want to pay COLN D. CHAFEE, a Senator from the Washington, DC, September 14, 2004. appropriate respect to the Jewish holi- State of Rhode Island. To the Senate: day tomorrow, I plead with our col- Under the provisions of rule I, paragraph 3, of the Standing Rules of the Senate, I hereby leagues that they come as soon as they PRAYER appoint the Honorable LINCOLN D. CHAFEE, a are notified there will be a vote. We The Chaplain, Dr. Barry C. Black, of- Senator from the State of Rhode Island, to give everyone a heads-up when there fered the following prayer: perform the duties of the Chair. will be a vote. Come and vote and leave Let us pray. TED STEVENS, and efficiently use that time. O Lord, our rock, hear our praise President pro tempore. Mr. REID. Will the Senator yield? today, for Your faithfulness endures to Mr. CHAFEE thereupon assumed the Mr. FRIST. I am happy to yield for a all generations. You hear our prayers. chair as Acting President pro tempore. question. Mr. REID. Mr. President, I am so Surround us with Your mercy. -

Oral History Ir.Terview with H. R. Haldeman R Conducted by Raymg~D H

Oral history ir.terview with H. R. Haldeman r conducted by RaymG~d H. Geselbracht in Mr. Haldeman's home in Santa Barbara, Califorrtia on April 12, 1988 RHG: Mr. Haldeman, yesterday we were talking about the first White House staff during this shakedowr. pet"icld. I noticed many entries [in Haldeman's Journall during this time about putting [John D.l Ehrl ichman in place as the domest ic pol icy pet"sclr... Or.e clf the thir.gs that surprised rne about this was that it was slclw in developing, and I would Judge from reading your Journal that the idea of using Ehrlichman was first suggested in a staff meeting. Then you had to sell the idea to the Presider.t ar.d maybe ever. Just as importar.t at least sell the idea tCI Ehrl ichmar•• I take it he thought about it for quite a long while. Could you describe that? HRH: I think your overall description is baSically accurate. The need came up very quickly, very early or., and hClw tCI deal wi th it. The need for somebc.dy in general control of clperat ions and procedures, and so forth, on the domestic side, as [Henryl Kissinger was on the foreign policy side, became almost immediately evident, even though we had not theoretically set up the structure with that thought in mind. The question of who it should be automatically rises quickly when that kind of problem arises. The only logical person, in looking back on it, and I'm sure it was the case at the time, was Ehrlichman, in the sense of his being knowledgeable and interested in domestic policy areas, first of all. -

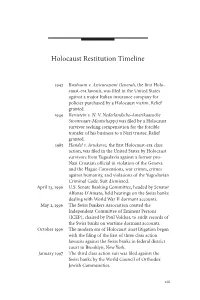

Holocaust Restitution Timeline

Holocaust Restitution Timeline 1942 Buxbaum v. Assicurazioni Generali, the first Holo- caust-era lawsuit, was filed in the United States against a major Italian insurance company for policies purchased by a Holocaust victim. Relief granted. 1949 Bernstein v. N. V. Nederlandsche-Amerikaansche Stoomvaart-Maatschappij was filed by a Holocaust survivor seeking compensation for the forcible transfer of his business to a Nazi trustee. Relief granted. 1985 Handel v. Artukovic, the first Holocaust-era class action, was filed in the United States by Holocaust survivors from Yugoslavia against a former pro- Nazi Croatian official in violation of the Geneva and the Hague Conventions, war crimes, crimes against humanity, and violations of the Yugoslavian Criminal Code. Suit dismissed. April 23, 1996 U.S. Senate Banking Committee, headed by Senator Alfonse D’Amato, held hearings on the Swiss banks dealing with World War II dormant accounts. May 2, 1996 The Swiss Bankers Association created the Independent Committee of Eminent Persons (ICEP), chaired by Paul Volcker, to audit records of the Swiss banks on wartime dormant accounts. October 1996 The modern era of Holocaust asset litigation began with the filing of the first of three class action lawsuits against the Swiss banks in federal district court in Brooklyn, New York. January 1997 The third class action suit was filed against the Swiss banks by the World Council of Orthodox Jewish Communities. xiii xiv Holocaust Restitution Timeline January 8, 1997 Christoph Meili discovered the Union Bank of Switzerland attempting to shred pre–World War II financial documents. March 25, 1997 French Prime Minister Alain Juppe created the Prime Minister’s Office Study Mission into the Looting of Jewish Assets in France (“Mattéoli Commission”) to study various forms of theft of Jewish property during World War II and the postwar efforts to remedy such theft. -

Henry Kissinger: the Emotional Statesman*

barbara keys Bernath Lecture Henry Kissinger: The Emotional Statesman* “That poor fellow is an emotional fellow,” a fretful Richard Nixon observed about Henry Kissinger on Christmas Eve 1971. The national security adviser had fallen into one of his typical postcrisis depressions, anguished over public criticism of his handling of the Indo-Pakistani War. In a long, meandering conversation with aide John Ehrlichman, Nixon covered many topics, but kept circling back to his “emotional” foreign policy adviser. “He’s the kind of fellow that could have an emotional collapse,” he remarked. Ehrlichman agreed. “We just have to get him some psychotherapy,” he told the president. Referring to Kissinger as “our major problem,” the two men recalled earlier episodes of Kissinger’s “impossible” behavior. They lamented his inability to shrug off criticism, his frequent mood swings, and his “emotional reactions.” Ehrlichman speculated that Nelson Rockefeller’s team had “had all kind of problems with him,” too. Nixon marveled at how “ludicrous” it was that he, the president— beset with enormous problems on a global scale—had to spend so much time “propping up this guy.” No one else, Nixon said, would have put up with “his little tantrums.”1 Kissinger’s temper tantrums, jealous rages, and depressions frequently frus- trated and bewildered the president and his staff. Kissinger habitually fell into a state of self-doubt when his actions produced public criticism. When his support for the Cambodian invasion elicited a media frenzy, for example, Kissinger’s second-in-command, Al Haig, went to Nixon with concerns about his boss’s “very emotional and very distraught” state.2 Journalists often found what William Safire called “Kissinger’s anguish—an emotion dramatized by the man’s ability to let suffering show in facial expressions and body *I am grateful to Frank Costigliola and TomSchwartz for comments on a draft of this essay, and to Frank for producing the scholarship that helped inspire this project. -

Arms Control-Public Diplomacy (06/06/1983-08/19/1983) Box: 11

Ronald Reagan Presidential Library Digital Library Collections This is a PDF of a folder from our textual collections. Collection: Executive Secretariat, NSC: Subject File Folder Title: Arms Control-Public Diplomacy (06/06/1983-08/19/1983) Box: 11 To see more digitized collections visit: https://www.reaganlibrary.gov/archives/digitized-textual-material To see all Ronald Reagan Presidential Library inventories visit: https://www.reaganlibrary.gov/archives/white-house-inventories Contact a reference archivist at: [email protected] Citation Guidelines: https://reaganlibrary.gov/archives/research- support/citation-guide National Archives Catalogue: https://catalog.archives.gov/ NSC/S PROFILE ~ ID 8303934 .. RECEIVED 07 JUN 83 19 TO CLARK FROM WICK, C DOCDATE 06 JUN 83 I • • DECLASSIFIED se Guidelines, August v,.-i~ "'-- NARA, Date_.,_..__,_..w._. KEYWORDS: PUBLIC DIPLOMACY ARMS CONTROL SUBJECT: STATUS RPT # 17 RE ARMS REDUCTION & SECURITY ISSUES 23 - 27 MAY ---------------------------------------- ·--- ---------------------------------- ACTION: ANY ACTION NECESSARY DUE: 10 JUN 83 STATUS S FILES FOR ACTION FOR CONCURRENCE FOR INFO RAYMOND LORD SIMS LINHARD LENCZOWSKI KRAEMER SOMMER DOBRIANSKY COMMENTS REF# LOG 8303605 NSCIFID ( J / ACTION OFFICER (S) ASSIGNED ACTION REQUIRED DUE COPIES TO _o/J_d" _ ytof<✓~ aclurn ~ lZ&cY7CV2/ ,., DISPATCH --- ----------- ------- W/ATTCH FILE tPA United States Office of the Director ·· Information Agency 3934 Washington, D. USIA ... ., 83 JUN 7 June 6, 1983 MEMJRANOOM FOR: The Honorable Lawrence s. Eagleburger Chairman, International Political Conmittee The Honorable Gerald B. Helman Chairman, PUblic Dip I cy Corrmittee /,,..\ FR<l-1: Charles z. 'Wick Director SUBJECT: Status Report No. 17 - Arms Reduction and Security Issues {Week of May 23-27) HIGHLIGHTS Norwegian Institute of Journalism Tour a success: A group of 15 mid-level journalists from the prestigious Norwegian Institute of Journalism participated in a USIA-arranged program in Washington on May 26 and 27 at the conclusion of a ronth-long visit to the U.S. -

By Any Other Name: How, When, and Why the US Government Has Made

By Any Other Name How, When, and Why the US Government Has Made Genocide Determinations By Todd F. Buchwald Adam Keith CONTENTS List of Acronyms ................................................................................. ix Introduction ........................................................................................... 1 Section 1 - Overview of US Practice and Process in Determining Whether Genocide Has Occurred ....................................................... 3 When Have Such Decisions Been Made? .................................. 3 The Nature of the Process ........................................................... 3 Cold War and Historical Cases .................................................... 5 Bosnia, Rwanda, and the 1990s ................................................... 7 Darfur and Thereafter .................................................................... 8 Section 2 - What Does the Word “Genocide” Actually Mean? ....... 10 Public Perceptions of the Word “Genocide” ........................... 10 A Legal Definition of the Word “Genocide” ............................. 10 Complications Presented by the Definition ...............................11 How Clear Must the Evidence Be in Order to Conclude that Genocide has Occurred? ................................................... 14 Section 3 - The Power and Importance of the Word “Genocide” .. 15 Genocide’s Unique Status .......................................................... 15 A Different Perspective ..............................................................