A Comparison of Accounting Fraud Before and After Sarbanes-Oxley Kayla Dowd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Loophole in Financial Accounting: a Detailed Analysis of Repo

The Journal of Applied Business Research – September/October 2011 Volume 27, Number 5 A Loophole In Financial Accounting: A Detailed Analysis Of Repo 105 Chun-Chia (Amy) Chang, Ph.D., San Francisco State University, USA Joanne Duke, Ph.D., San Francisco State University, USA Su-Jane Hsieh, Ph.D., San Francisco State University, USA ABSTRACT From 2000 to 2008, Lehman used repo transactions to hide billions of dollars on their statements. They also misrepresented the repo transactions as “secured borrowings” even though they actually recorded the transactions as sales. Valukas’ report in 2010 stimulated an extensive coverage of the repo transactions and spurred an array of studies addressing issues related to the collapse of financial institutions. Since the Repo 105 maneuver of Lehman provides a good example on how regulatory deficiencies can induce companies to obscure financial reporting and the importance of ethics in deterring these abuses, our study intends to examine repo transactions related accounting standards, illustrate how repo transactions can enhance a bank’s financial statements, and discuss the importance of business ethics in curtailing accounting irregularities. Keywords: Repo 105; creative accounting; business ethics INTRODUCTION n March 2010, the Wall Street Journal (WSJ hereafter) published a series of reports regarding a practice called Repo 105 that was employed by the Lehman Brothers Holdings Inc. to obscure approximately $50 billion of liabilities from investors.1 A “Repo” is a “repurchase agreement” that enables short-term Iborrowers to gain liquidity. During a repo transaction, a company “sells” assets to others with a repurchase agreement signed simultaneously at the time of the sale. -

Enron's Pawns

Enron’s Pawns How Public Institutions Bankrolled Enron’s Globalization Game byJim Vallette and Daphne Wysham Sustainable Energy and Economy Network Institute for Policy Studies March 22, 2002 About SEEN The Sustainable Energy and Economy Network, a project of the Institute for Policy Studies (Washington, DC), works in partnership with citizens groups nationally and globally on environment, human rights and development issues with a particular focus on energy, climate change, environmental justice, and economic issues, particularly as these play out in North/South relations. SEEN views these issues as inextricably linked to global security, and therefore applies a human security paradigm as a framework for guiding its work. The reliance of rich countries on fossil fuels fosters a climate of insecurity, and a rationale for large military budgets in the North. In the South, it often fosters or nurtures autocratic or dictatorial regimes and corruption, while exacerbating poverty and destroying subsistence cultures and sustainable livelihoods. A continued rapid consumption of fossil fuels also ensures catastrophic environmental consequences: Climate change is a serious, emerging threat to the stability of the planet's ecosystems, and a particular hazard to the world's poorest peo- ple. The threat of climate change also brings more urgency to the need to reorient energy-related investments, using them to provide abundant, clean, safe energy for human needs and sustainable livelihoods. SEEN views energy not as an issue that can be examined in isolation, but rather as a vital resource embedded in a development strategy that must simultaneously address other fundamentals, such as education, health care, public par- ticipation in decision-making, and economic opportunities for the poorest. -

A Case of Corporate Deceit: the Enron Way / 18 (7) 3-38

NEGOTIUM Revista Científica Electrónica Ciencias Gerenciales / Scientific e-journal of Management Science PPX 200502ZU1950/ ISSN 1856-1810 / By Fundación Unamuno / Venezuela / REDALYC, LATINDEX, CLASE, REVENCIT, IN-COM UAB, SERBILUZ / IBT-CCG UNAM, DIALNET, DOAJ, www.jinfo.lub.lu.se Yokohama National University Library / www.scu.edu.au / Google Scholar www.blackboard.ccn.ac.uk / www.rzblx1.uni-regensburg.de / www.bib.umontreal.ca / [+++] Cita / Citation: Amol Gore, Guruprasad Murthy (2011) A CASE OF CORPORATE DECEIT: THE ENRON WAY /www.revistanegotium.org.ve 18 (7) 3-38 A CASE OF CORPORATE DECEIT: THE ENRON WAY EL CASO ENRON. Amol Gore (1) and Guruprasad Murthy (2) VN BRIMS Institute of Research and Management Studies, India Abstract This case documents the evolution of ‘fraud culture’ at Enron Corporation and vividly explicates the downfall of this giant organization that has become a synonym for corporate deceit. The objectives of this case are to illustrate the impact of culture on established, rational management control procedures and emphasize the importance of resolute moral leadership as a crucial qualification for board membership in corporations that shape the society and affect the lives of millions of people. The data collection for this case has included various sources such as key electronic databases as well as secondary data available in the public domain. The case is prepared as an academic or teaching purpose case study that can be utilized to demonstrate the manner in which corruption creeps into an ambitious organization and paralyses the proven management control systems. Since the topic of corporate practices and fraud management is inherently interdisciplinary, the case would benefit candidates of many courses including Operations Management, Strategic Management, Accounting, Business Ethics and Corporate Law. -

Asset Sales Or Loans: the Case of Lehman Brothers' Repo 105S Chao

THE ACCOUNTING EDUCATORS’ JOURNAL Volume XXI 2011 pp. 79- 88 Asset Sales or Loans: The Case of Lehman Brothers’ Repo 105s Chao-Shin Liu University of Notre Dame Thomas F. Schaefer University of Notre Dame Abstract Lehman Brothers, Inc. was one of the very early casualties of the 2008-09 worldwide financial crisis becoming the largest bankruptcy of a U.S. financial institution. Prior to its demise, Lehman Brothers periodically employed an accounting technique known as Repo 105 for its financial reporting of certain transactions involving repurchase agreements. The Repo 105 accounting allowed Lehman to temporarily reduce its debt levels during periods that included financial statement preparation. The purpose of this case is to summarize the accounting for Lehman Brothers’ Repo 105 transactions, present some classroom discussion points, and provide student review questions related to accounting and financial reporting issues underlying the Repo 105 transactions. Background On September 15, 2008, Lehman Brothers, a former global financial services firm, became the largest firm at the time to declare bankruptcy in United States history. In several time periods prior to the bankruptcy, Lehman employed an accounting technique euphemistically referred to as either “Repo 105” or “Repo 108.”Although the role of these repurchase agreements in the bankruptcy is not completely clear, many argue that the technique enabled Lehman Brothers to hide large amounts of liabilities for the purpose of misinforming investors, business partners, and regulators. -

Sarbanes-Oxley and Corporate Greed Adria L

University of Connecticut OpenCommons@UConn Honors Scholar Theses Honors Scholar Program Spring 5-8-2011 Sarbanes-Oxley and Corporate Greed Adria L. Stigliano University of Connecticut - Storrs, [email protected] Follow this and additional works at: https://opencommons.uconn.edu/srhonors_theses Part of the Accounting Commons, and the Business Law, Public Responsibility, and Ethics Commons Recommended Citation Stigliano, Adria L., "Sarbanes-Oxley and Corporate Greed" (2011). Honors Scholar Theses. 207. https://opencommons.uconn.edu/srhonors_theses/207 Sarbanes-Oxley & Corporate Greed Adria L. Stigliano Spring 2011 Sarbanes-Oxley & Corporate Greed Adria L. Stigliano Spring 2011 Adria L. Stigliano Honors Thesis Spring 2011 Sarbanes-Oxley and Corporate Greed Sigmund Freud, the Austrian psychologist, believed that every human being is mentally born with a “clean slate”, known as Tabula rasa , where personality traits and character are built through experience and family morale. Other psychologists and neurologists believe individuals have an innate destiny to be either “good” or “bad” – a more fatalistic view on human life. Psychological theories are controversial, as it seems almost impossible to prove which theory is reality, but we find ourselves visiting these ideas when trust, ethics, reputation, and integrity are violated. The Sarbanes-Oxley Act is still a relatively new federal law set forth by the Securities Exchange Commission in 2002. Since its implementation, individuals have been wondering if Sarbanes-Oxley is effective enough and doing what it is meant to do – catch and prevent future accounting frauds and scandals. With the use of closer and stricter rules, the SOA is trying to prevent frauds with the use of a created Public Company Accounting Oversight Board. -

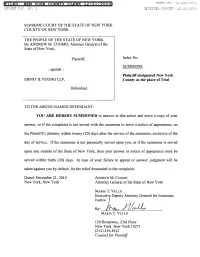

Filed: New York County Clerk 12/21/2010 Index No

FILED: NEW YORK COUNTY CLERK 12/21/2010 INDEX NO. 451586/2010 NYSCEF DOC. NO. 1 RECEIVED NYSCEF: 12/21/2010 SUPREME COURT OF TH:E STATE OF NEW YORK COUNTY OF NEW YORK THE PEOPLE OF THE STATE OF NEW YORK By ANDREW M. CUOMO, Attorney General ofthe State ofNew York, Plaintiff, Index No. SUMMONS - against- Plaintiff designated New York ERNST & YOUNG LLP, County as the place of Trial Defendant. TO THE ABOVE-NAMED DEFENDANT: YOU ARE HEREBY SUMMONED to answer in this action and serve a copy of your answer, or if the complaint is not served with the summons to serve a notice of appearance, on the Plaintiffs attorney within twenty (20) days after the service ofthe summons, exclusive of the day of service. If the summons is not personally served upon you, or if the summons is served upon you outside of the State of New York, then your answer or notice of appearance must be served within thirty (30) days. In case of your failure to appear or answer, judgment will be taken against you by default, for the relief demanded in the complaint. Dated: December 21,2010 ANDREW M. CUOMO New York, New York Attorney General ofthe State ofNew York MARIA T. VULLO Executive Deputy Attorney General for Economic JusticeL By: J1/A MARIA T. VULLO 120 Broadway, 23rd Floor New York, New York 10271 (212) 416-8521 Counselfor Plaintiff SUPREME COURT OF THE STATE OF NEW YORK COUNTY OF NEW YORK THE PEOPLE OF THE STATE OF NEW YORK By ANDREW M. CUOMO, Attorney General of the State of New York, Plaintiff, Index No. -

Enron: Market Exploitation and Correction

Financial Decisions, Spring 2002, Article 1. Enron: Market Exploitation And Correction Ronnie J. Clayton William Scroggins Christopher Westley1 Department of Finance, Economics and Accounting, Jacksonville State University Abstract This paper chronicles the rise and fall of Enron, Inc., the once powerful energy firm based in Houston, Texas. The history of the firm is reviewed, the November 2001 financial restatement is examined to show the impact of the failure to report the appropriate financial position for the firm, and reasons for the firm’s downfall are considered. While Enron’s decline may currently be considered a market failure, it is likely that the events surrounding the firm in 2001 will ultimately be considered a case in which the market worked to ferret out deception and poor judgment on the part of Enron’s management. I. Introduction Early in the year 2002 one could not escape the continuing publicity concerning the once powerful, now bankrupt, Enron, Inc. In a span of less than two months during the autumn of 2001, the firm fell from business idol to congressional doormat, or somewhat more importantly, from the new business model to a model of business greed and ultimate failure. Of course the fall of Enron did not occur in the few days of October and November 2001. The event that started it all was the 1993 formation, in partnership with the California Public Employees’ Retirement System (CalPERS), of the Joint Energy Development Investment Limited Partnership (JEDI).2 The ultimate failure was designed by JEDI and set into place in a galaxy not so far away and in a time not so long ago. -

Creative Accounting Practices Pdf

Creative accounting practices pdf Continue Euphemism, referring to unethical accounting practice Of Book Preparation, redirects here. For an episode of Black Books, see Cooking Books (Black Books episode). For the New York-tv cooking programme, watch the Cook Books Program (TV program). Part of the series onAccounting Historical Expenses Permanent Purchasing Power Office Tax Main Types Audit Budget Expenditures Forensic Fund State Office Social Tax Key Concepts Period Accrual Permanent Purchasing Power Economic Essence Fair Value Going Historical Concerns Historical Costs Compliance Principle Materiality Income Recognition Unit Account Selected Cash Account Cash Expenses Goods, Sold Amortization/Amortization of Equity Expenses Goodwill Passion principles Financial Reporting Annual Report Balance Sheet Cash Flow Income Office Discussion Notes to Financial Reporting Accountant Bank Reconciliation Of Debits and Loans Double Entry System FIFO and LIFO Journal Ledger / General Registry T Accounts Forensic Balance Audit Of Financial Firms Report by People and Organization Accountants Accounting Organizations but deviate from the spirit of these rules with questionable accounting ethics, in particular misrepresenting the results in favor of training, or the firm that hired the accountant. They are characterized by excessive complications and the use of new ways of characterizing income, assets or liabilities and the intention to influence readers with respect to interpretations desired by the authors. Sometimes the terms are also innovative or aggressive. Another common synonym is the preparation of books. Creative accounting is often used in tandem with outright financial fraud (including securities fraud), and the boundaries between them are blurred. Creative accounting techniques have been known since ancient times and appear all over the world in various forms. -

Classic Case Studies in Accounting Fraud”

“Classic Case Studies in Accounting Fraud” A thesis submitted to the Miami University Honors Program in partial fulfillment of the requirements for University Honors. by Justin Matthew Mock May 2004 Oxford, Ohio ABSTRACT “Classic Case Studies in Accounting Fraud” by Justin Matthew Mock Over the past several years, accounting fraud has dominated the headlines of mainstream news. While these recent cases all involve sums of money far in excess of any before, accounting fraud is certainly not a new phenomenon. Since the early days on Wall Street, fraud has consistently fooled the markets, investors, and auditors alike. In this thesis, an analysis of several cases of accounting fraud is conducted with background information, fraud logistics, and accounting and auditing violations all subject to study. This paper discusses specific cases of fraud and presents the issues that have been and must continue to be addressed as companies push the envelope of acceptable accounting standards. The discussion and findings demonstrate the ever-present potential for fraud in a variety of accounts, companies, industries, and time periods, while also having a powerful influence on an auditor’s work and preconceptions going forward. iii iv “Classic Case Studies in Accounting Fraud” by Justin Matthew Mock Approved by: _________________________, Advisor Dr. Phil Cottell _________________________, Reader Dr. Larry Rankin _________________________, Reader Mr. Jeffrey Vorholt Accepted by: __________________________, Director, University Honors Program v vi ACKNOWLEDGEMENTS “Classic Case Studies in Accounting Fraud” was completed under the direction of the Miami University Honors Program. The Honors Program provided financial support essential to the project’s research and successful completion. -

Annual Report

BERKSHIRE HATHAWAY INC. 2002 ANNUAL REPORT TABLE OF CONTENTS Business Activities.................................................... Inside Front Cover Corporate Performance vs. the S&P 500 ................................................ 2 Chairman's Letter*.................................................................................. 3 Selected Financial Data For The Past Five Years ..................................................................................24 Acquisition Criteria ................................................................................25 Independent Auditors' Report .................................................................25 Consolidated Financial Statements.........................................................26 Management's Discussion.......................................................................52 Owner's Manual......................................................................................68 Common Stock Data...............................................................................75 Major Operating Companies...................................................................76 Directors and Officers of the Company.........................Inside Back Cover *Copyright © 2003 By Warren E. Buffett All Rights Reserved Business Activities Berkshire Hathaway Inc. is a holding company owning subsidiaries engaged in a number of diverse business activities. The most important of these is the property and casualty insurance business conducted on both a direct and reinsurance basis -

Corporate Collapse and the Role of Audit Committees: a Case Study of Lehman Brothers

World Journal of Social Sciences Vol. 7. No. 1. March 2017. Pp. 19 – 29 Corporate Collapse and the Role of Audit Committees: A Case Study of Lehman Brothers Abdullahi Adamu Dodo* This paper examined the roles and effectiveness of Audit Committees (herein ACs) as provided by corporate governance codes, in relation to corporate failures, whether the failure is as a result of the ineffectiveness of the ACs. Given that the AC is perceived to be a means of strengthening the external financial reporting process and facilitating the detection and prevention of corporate misconducts and scandals. It is believed that many financial and governance failures experienced in the recent past could be detected much earlier, had ACs been discharging their duties effectively. Secondary sourced data were used to investigate the roles of AC in the case of Lehman Brother’s corporate failure. A qualitative case study method was employed to carry out the study, by identifying and evaluating specific areas of interaction between ACs and other parties which affect audit process. The finding shows that many corporate failures are associated with the ineffectiveness of ACs, and that ACs could have prevented the occurrence of several corporate failures if they were efficient. However, the ACs cannot be 100% blamed for the failures, this is because their effectiveness is subjected to so many factors, and lack of any one factor always renders the AC ineffective. Some of the findings are consistent, while others are contrary to previous empirical studies on effectiveness of ACs. The study exposed specifically the process involved in the conduct of ACs in an organization and this add to the current debate on the need for improvement in the roles played by the AC as public gatekeepers. -

Enron Scandal: the Fall of a Wall Street Darling

Enron Scandal: The Fall of a Wall Street Darling The story of Enron Corp. is the story of a company that reached dramatic heights, only to face a dizzying fall. Its collapse affected thousands of employees and shook Wall Street to its core. At Enron's peak, its shares were worth $90.75; when it declared bankruptcy on December 2, 2001, they were trading at $0.26. To this day, many wonder how such a powerful business, at the time one of the largest companies in the U.S, disintegrated almost overnight and how it managed to fool the regulators with fake holdings and off-the-books accounting for so long. Enron's Energy Origins Enron was formed in 1985, following a merger between Houston Natural Gas Co. and Omaha-based InterNorth Inc. Following the merger, Kenneth Lay, who had been the chief executive officer (CEO) of Houston Natural Gas, became Enron's CEO and chairman and quickly rebranded Enron into an energy trader and supplier. Deregulation of the energy markets allowed companies to place bets on future prices, and Enron was poised to take advantage. In 1990, Lay created the Enron Finance Corp. To head it, he appointed Jeffrey Skilling, whose work as a McKinsey & Co consultant had impressed Lay. Skilling was at the time one of the youngest partners at McKinsey. Why Enron Collapsed Skilling joined Enron at an auspicious time. The era's regulatory environment allowed Enron to flourish. At the end of the 1990s, the dot-com bubble was in full swing, and the Nasdaq hit 5,000.