Who Says Elephants Can't Dance BIZ

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sep 19 New Tobacco Products.Ppt

9/20/13 New Products Old Tricks The Problem What’s the Problem with New Products? New tobacco products are designed to: – Draw in new and youth users – Keep smokers smoking – Circumvent regulations and taxation 1 9/20/13 Increased youth smokeless tobacco use TOLL OF OTHER TOBACCO USE National Youth Smoking and Smokeless Tobacco Use 1997 - 2011 2003-2009: -11.0% 2003-2011: -17.4% 2003-2009: -9.2% 2003-2011: -8.7% 2003-2009: +36.4% 2003-2011: +16.4% 2003-2009: +32.8% 2003-2011: +14.9% Source: CDC, Youth Risk Behavior Surveillance Survey. 2 9/20/13 Most popular snuff brands among 12-17 year olds 1999-2011 2011 Top 3 Most Popular Moist Snuff Brands among 12-17 year olds 1. Grizzly (Reynolds American, via American Snuff Company) 2. Skoal (Altria, via UST) 3. Copenhagen (Altria, via UST) Source: 2011 NSDUH Source: Analysis of NHSDA, NSDUH data Health Harms of Other Tobacco Use Smokeless Tobacco It [smokeless • Cancer, including oral cancer tobacco] is not a safe and pancreatic cancer substitute for smoking cigarettes. • Gum disease -- U.S. Surgeon General, 1986 • Nicotine addiction Cigar Use • Cancer of the oral cavity, larynx, esophagus and lung 3 9/20/13 Brand development, Acquisitions Over Time WHERE IS THE INDUSTRY HEADED? Companies under in 1989 ( ) 4 9/20/13 Companies under in 2013 (28.5% economic interest) Tobacco Brands in 2013 Non-Tobacco Products 5 9/20/13 Companies under RJR Nabisco in 1989 Companies under in 2013 (formerly Conwood Company) B&W no longer exists as a separate company. -

Who Says Elephants Can't Dance?: Leading a Great Enterprise Through

Who Says Elephants Can't Dance? Leading a Great Enterprise Through Dramatic Change Louis V. Gerstner, Jr. This book is dedicated to the thousands of IBMers who never gave up on their company, their colleagues, and themselves. They are the real heroes of the reinvention of IBM. Contents Foreword vii Introduction 1 PART I-GRABBING HOLD 7 1 The Courtship 9 2 The Announcement 18 3 Drinking from a Fire Hose 29 4 Out to the Field 41 5 Operation Bear Hug 49 6 Stop the Bleeding (and Hold the Vision) 56 7 Creating the Leadership Team 73 8 Creating a Global Enterprise 83 9 Reviving the Brand 88 10 Resetting the Corporate Compensation Philosophy 93 11 Back on the Beach 103 PART II-STRATEGY 111 12 A Brief History of IBM 113 13 Making the Big Bets 121 14 ServicesÐthe Key to Integration 128 15 Building the World's Already Biggest Software Business 136 16 Opening the Company Store 146 17 Unstacking the Stack and Focusing the Portfolio 153 18 The Emergence of e-business 165 19 Reflections on Strategy 176 PART III-CULTURE 179 20 On Corporate Culture 181 21 An Inside-Out World 189 22 Leading by Principles 200 PART IV-LESSONS LEARNED 217 23 FocusÐYou Have to Know (and Love) Your Business 219 24 ExecutionÐStrategy Goes Only So Far 229 25 Leadership Is Personal 235 26 Elephants Can Dance 242 27 IBMÐa Farewell 253 APPENDICES 259 Appendix AÐThe Future of e-business 261 Appendix BÐFinancial Overview 277 Index 287 ABOUT THE AUTHOR CREDITS COVER COPYRIGHT ABOUT THE PUBLISHER Foreword have never said to myself, ªGee, I think I want to write a I book.º I am not a book writer. -

Private Equity

Private Equity: Accomplishments and Challenges by Greg Brown, University of North Carolina; Bob Harris, University of Virginia; Steve Kaplan, University of Chicago; Tim Jenkinson, University of Oxford; and David Robinson, Duke University ince the 1980s, there has been an ongoing discussion about the role of private S equity (PE) in the economy. As investors have flocked to the asset class, voices critical of the negative social impact of PE have grown louder. In this article, we examine what is known from the academic literature about the effects of private equity on corporate productivity, the returns for investors, and possible broader economic and social consequences. We catalogue what we believe to be strong evidence of the overall benefits of PE-backed companies and investors in private equity, as well as spillovers in the form of broader gains in economic productivity. We also describe apparent instances of PE shortcomings in some specific industries where negative social impacts can be measured in some way. In our view, private equity is “capitalism in high gear” and, Back to the 1980s as such, subject to most of the same debates concerning Our account of private equity begins at the end of the 1980s, economic and social conditions in a free enterprise system. when hostile takeovers and other often highly leveraged While some argue that the 2020 version of capitalism transactions, including a relative newcomer called the lever- (as practiced in the U.S. and much of the world) is inef- aged buyout (or LBO), came under fierce attack in both the fective in coping with current social needs, much of the press and conventional business circles. -

RJR Nabisco: a Case Study of a Complox Lovoragod Buyout

by Allen Michel and Israel Shaked RJR Nabisco: A Case Study of a Complox Lovoragod Buyout Several features of RJR Nabisco made it a particularly attractive LBO candidate. Its operations exhibited moderate and consistent growth, required little capital investment and carried low debt levels. Its problems—a declining return on assets and falling inventory turnover—appeared fixable. And it offered significant break-up value. Valuing RJR's equity at the time of the LBO requires detailed knowledge of the company's operations and extensive number crunching. The analysis is obviously quite dependent on the assumptions made about cash flow in the post-LBO period, as well as the long-term, steady-state growth rate. Nevertheless, the figures suggest that, even assuming a high, 5 per cent level of steady-state growth, RJR's cash flows would have to grow at a rate of at least 18 per cent per year to justify KKR's bid of $109 per share. RJR's board played a prominent role in the bidding process. By setting the bidding rules, the board successfully minimized the possibility of collusion and thus increased potential gains to stakeholders. The decision to accept KKR's offer over RJR management's higher bid appears to reflect the board's concern for employees and existing shareholders. OTH THE POPULAR press and the aca- move, introducing four brands simultaneously. demic press have devoted extensive cov- The strategy worked well. Among the new Berage to leveraged buyouts, but neither brands was Camel, a name brand that changed has devoted much attention to analyzing the the company's history. -

)%A:**********A*AA******A;.**** ************ Reproductions Supplied by EDRS Are the Best That Can Be Made from the Original Document

DOCUMENT RESUME ED 380 227 PS 023 077 AUTHOR Galinsky, Ellen; And Others TITLE Employers, Families, and Education: Promoting Faalily Involvement in Learning. Building Community Partnerships for Learning. INSTITUTION Families and Work Inst., New York, NY. SPONS AGENCY Department of Education, Washington, DC. REPORT NO ED-0US95-5 PUB DATE Jan 95 NOTE 41p.; Commissioned for the Family Involvement Partnership for Learning. PUB TYPE Reports Descriptive (141) EDRS PRICE MF01/PCO2 Plus Postage. DESCRIPTORS *Community Cooperation; Early Childhood Education; Employed Parents; Employer Employee Relationship; Employer Supported Day Care; Family Involvement; Family Programs; Family School Relationship; *Parent Participation; Parent Student Relationship; Partnerships in Education; Program Descriptions; Program Improvement; School Age Day Care; *School Business Relationship; *School Community Relationship; School Policy IDENTIFIERS Family Involvement Partnership for Learning ABSTRACT Intended to highlight the importance of including families and members of the broader community in children's learning, this report discusses the role of businesses and employers in helping partners and family members be more involved in children's learning. The introduction, "Making Family Involvement in Learning a Goal" notes the three major ways that employers are promoting home-school-workplace partnerships:(1) by promoting and instituting programs and policies that encourage employees to get involved in their children's education.;(2) by developing and maintaining programs and policies to improve child care and schools in their communities; and (3) by assisting schools and child care centers in the development of programs and policies that promote family involvement. The first part of the report presents articles describing in greater detail the specific efforts of employers in these three areas. -

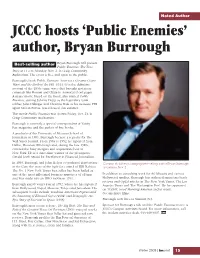

JCCC Hosts 'Public Enemies' Author, Bryan Burrough

Noted Author JCCC hosts ‘Public Enemies’ author, Bryan Burrough Best-selling author Bryan Burrough will present Public Enemies: The True Story at 11 a.m. Monday, Nov. 2, in Craig Community Auditorium. The event is free and open to the public. Burrough’s book Public Enemies: America’s Greatest Crime Wave and the Birth of the FBI, 1933-34 is the definitive account of the 1930s crime wave that brought notorious criminals like Bonnie and Clyde to America’s front pages. A major movie based on the book, also named Public Enemies, starring Johnny Depp as the legendary bank robber John Dillinger and Christian Bale as his nemesis, FBI agent Melvin Purvis, was released this summer. The movie Public Enemies was shown Friday, Oct. 23, in Craig Community Auditorium. Burrough is currently a special correspondent at Vanity Fair magazine and the author of five books. A graduate of the University of Missouri School of Journalism in 1983, Burrough became a reporter for The Wall Street Journal. From 1983 to 1992, he reported from Dallas, Houston, Pittsburgh and, during the late 1980s, covered the busy mergers and acquisitions beat in New York. He is a three-time winner of the prestigious Gerald Loeb Award for Excellence in Financial Journalism. In 1990, Burrough and John Helyar co-authored Barbarians Campus Activities is bringing best-selling author Bryan Burrough at the Gate, the story of the fight for control of RJR Nabisco. to campus Nov. 2. The No. 1 New York Times best-seller has been hailed as one of the most influential business narratives of all time In addition to consulting work for 60 Minutes and various and was made into an HBO movie in 1993. -

Private Equity Deals Picking up Steam

The Star Online: Printer Friendly Article Page 1 of 8 The Star Online > Business Saturday June 23, 2012 Private equity deals picking up steam By TEE LIN SAY [email protected] Value of deals in Malaysia comprised 50% of South-East Asia's total last year EVERY investing asset class has its defining deal. In the world of private equity (PE), its defining deal has got to be United States-based Kohlberg Kravis Roberts & Co's (KKR) takeover of RJR Nabisco in 1988 for US$31.3bil (RM97.03mil). That was the largest leverage buyout in history for the next 17 years. RJR Nabisco was formed in 1985 by the merger of Nabisco Brands and RJ Reynolds Tobacco Company. Nabisco was a producer of food products such as Oreo cookies, Ritz crackers, Del Monte fruit and vegetables and Snickers chocolate. RJ produced Winston , Camel and Salem cigarettes. No link there between food and fags. KKR made a hostile takeover bid of RJR Nabisco. During the ferocious battle that followed, the board along with KKR and other bidders progressively increased their bids to outdo each other. KKR subsequently won with its bid of US$31.1bil. Due to tobacco legislation, RJ Reynolds was subsequently spun out of RJR Nabisco. Today, Nabisco is owned by Kraft Foods . The RJR Nabisco leverage buyout was considered as the unsurpassed example of corporate greed. Time magazine featured RJR Nabisco president and CEO Ross Johnson on the cover of their December 1988 issue with the headline, “A Game of Greed: This man could pocket US$100mil from the largest corporate takeover in history. -

Safeguarding Investment Grade Bonds in the Event of a Leveraged Buyout: Legislation Or Contract?

Washington and Lee Law Review Volume 47 | Issue 3 Article 6 Summer 6-1-1990 Safeguarding Investment Grade Bonds In The Event Of A Leveraged Buyout: Legislation Or Contract? Follow this and additional works at: https://scholarlycommons.law.wlu.edu/wlulr Part of the Securities Law Commons Recommended Citation Safeguarding Investment Grade Bonds In The Event Of A Leveraged Buyout: Legislation Or Contract?, 47 Wash. & Lee L. Rev. 613 (1990), https://scholarlycommons.law.wlu.edu/wlulr/vol47/iss3/6 This Note is brought to you for free and open access by the Washington and Lee Law Review at Washington & Lee University School of Law Scholarly Commons. It has been accepted for inclusion in Washington and Lee Law Review by an authorized editor of Washington & Lee University School of Law Scholarly Commons. For more information, please contact [email protected]. SAFEGUARDING INVESTMENT GRADE BONDS IN THE EVENT OF A LEVERAGED BUYOUT: LEGISLATION OR CONTRACT? Prior to the takeover frenzy of the 1980s,' holders of investment grade bonds2 held relatively safe investments.' The phenomenon of leveraged buyouts (LBOs), however, has undermined the security of investment grade bonds. 4 Because a post-LBO company (surviving company) assumes a mas- sive amount of debt in addition to its pre-LBO (pre-existing) debt, the surviving company's ability to pay off all its pre-existing debt becomes more uncertain. 5 Despite this increased uncertainty, the pre-existing bondholders do not receive any additional return on their investment.6 The bonds of the pre-existing bondholders, thus, lose value by becoming riskier investments that still produce the same returns as before the LBO.7 Metropolitan Life Insurance Co. -

BURROUGH Would Say That We Hadn’T Already Said in Our Journal Stories,” Says Burrough

for The Wall Street Journal. When the two of them began pitching a book on the RJR Nabisco saga, “every publisher wanted to know what the book BURROUGH would say that we hadn’t already said in our Journal stories,” says Burrough. Only one publisher, Harper Collins, offered the two a contract, for $150,000. Minus their agent’s on “BARBARIANS” cut and distributed in installments split between the authors, that amount was just enough to allow Author bryan burrough discusses how his Burrough and Helyar to take some time off from and John Helyar’s masterpiece on the RJR Nabisco The Wall Street Journal. takeover changed the way deals are done Burrough, 27 at the time, had been covering Wall Street for only four months, “and I only wrote for t the barnes & noble bookstore on the Wall Street Journal because it was the best job New York’s Fifth Avenue, thousands I got offered out of college, not because I had any of titles cram the shelves of business interest in business. My interest was much more in books, suggesting that it won’t be easy true crime.” A to find a 28-year-old tome about an Neither Burrough nor Helyar had ever written a ’80s-era takeover. Does Barnes & Noble even carry book. “We started working on it on January 2nd and Barbarians at the Gate any longer? we turned it in over Labor Day. For those months, The title clearly rings a bell with the young man it was a seven-day-a-week, 16-hour-days thing. -

Lou Gerstner – Active Coper!

Lou Gerstner – Active Coper! By Leslie Pratch Some CEOs cope with whatever life presents; more than that, they grab opportunities. They learn from experience, face problems rather than avoid them, overcomes obstacles rather than giving up or blaming others. They consider others’ interests and the interests of society, as well as their own. They seize opportunities that others miss. They seek out multiple perspectives, in order to avoid own blind spots. These are active coping behaviors. Lou Gerstner is a model of active coping. CEOs for your portfolio companies should be too. Lou Gerstner began his career at McKinsey in 1965, where he became one of the youngest partners in the history of the firm. In 1973, he went to American Express. During his 10 years at American Express, he grew its business from 8.6 million to 30.7 million cardholders and produced 18% annual profit growth. In 1989, he became CEO of RJR Nabisco. There, he unified two separate cultures that had been brought together through the merger of RJR Tobacco and Nabisco Brands. KKR had purchased RJR Nabisco in 1988 in a leverage buyout that left the company with $25 billion debt. In four years, Gerstner reduced the debt to $14 billion, sold off $6 billion of non-core assets, and cut general expenses. In 1993, he was hired by IBM as the once world-class company was approaching failure. Most people believed that only smaller firms could nimbly adapt in the rapidly changing technology industry, and IBM’s board expected Gerstner to break IBM up. Instead, Gerstner kept the company together and revitalized it. -

1 Rj Reynolds Tobacco Co. Rj Reynolds Industries, Inc. Rjr Nabisco Inc. Rjr Nabisco Holdings Corp. Rj Reynolds Tobacco Holdings

RJ REYNOLDS TOBACCO CO. RJ REYNOLDS INDUSTRIES, INC. RJR NABISCO INC. RJR NABISCO HOLDINGS CORP. RJ REYNOLDS TOBACCO HOLDINGS, INC. REYNOLDS AMERICAN INC. A STOCK HISTORY – SEQUENCE OF EVENTS DATE EVENT 1899 RJ Reynolds Tobacco Co. Common Stock originally issued. (CUSIP: Unknown) November 1914 Shareholders received one (1) share of RJ Reynolds Tobacco Co. 7% Series Preferred Stock (CUSIP: Unknown) for every four (4) shares of Common Stock held. The 7% Series Preferred Stock originated with this distribution which was effective January 2, 1915. February 1917 Shareholders received one (1) share of 7% Series Preferred Stock for every four (4) shares of Common Stock held. May 1917 Shareholders received one (1) share of 7% Series Preferred Stock for every two (2) shares of Common Stock held. 1917 During the year, the Company’s charter was amended to allow two (2) types of Common Stock – Class A and Class B. (CUSIP’s are unknown.) All outstanding shares of the former “Common Stock” were designated Class A. April 1, 1918 Shareholders of Class A Common Stock were offered, for $100 per share, one share of Class B Common Stock for every four (4) shares of Class A held. This was the original issue date of the Class B security. July 1, 1918 Shareholders of Class A Common Stock were offered, for $100 per share, one share of Class B Common Stock for every two (2) shares of Class A held. November 1919 Shareholders of Class A Common Stock were offered, for $100 per share, one share of 7% Series Preferred Stock for every two (2) shares of Class A or Class B held. -

Who Says Elephants Can't Dance?

Who Says Elephants Can't Dance? Leading a Great Enterprise Through Dramatic Change Louis V. Gerstner, Jr. This book is dedicated to the thousands of IBMers who never gave up on their company, their colleagues, and themselves. They are the real heroes of the reinvention of IBM. Contents Foreword vii Introduction 1 PART I-GRABBING HOLD 7 1 The Courtship 9 2 The Announcement 18 3 Drinking from a Fire Hose 29 4 Out to the Field 41 5 Operation Bear Hug 49 6 Stop the Bleeding (and Hold the Vision) 56 7 Creating the Leadership Team 73 8 Creating a Global Enterprise 83 9 Reviving the Brand 88 10 Resetting the Corporate Compensation Philosophy 93 11 Back on the Beach 103 PART II-STRATEGY 111 12 A Brief History of IBM 113 13 Making the Big Bets 121 14 ServicesÐthe Key to Integration 128 15 Building the World's Already Biggest Software Business 136 16 Opening the Company Store 146 17 Unstacking the Stack and Focusing the Portfolio 153 18 The Emergence of e-business 165 19 Reflections on Strategy 176 PART III-CULTURE 179 20 On Corporate Culture 181 21 An Inside-Out World 189 22 Leading by Principles 200 PART IV-LESSONS LEARNED 217 23 FocusÐYou Have to Know (and Love) Your Business 219 24 ExecutionÐStrategy Goes Only So Far 229 25 Leadership Is Personal 235 26 Elephants Can Dance 242 27 IBMÐa Farewell 253 APPENDICES 259 Appendix AÐThe Future of e-business 261 Appendix BÐFinancial Overview 277 Index 287 ABOUT THE AUTHOR CREDITS COVER COPYRIGHT ABOUT THE PUBLISHER Foreword have never said to myself, ªGee, I think I want to write a I book.º I am not a book writer.