US Hispanic Media and Communications Monthly Feb 2006, Issue 3

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Impact of Corporate Newsroom Culture on News Workers & Community Reporting

Portland State University PDXScholar Dissertations and Theses Dissertations and Theses Spring 6-5-2018 News Work: the Impact of Corporate Newsroom Culture on News Workers & Community Reporting Carey Lynne Higgins-Dobney Portland State University Follow this and additional works at: https://pdxscholar.library.pdx.edu/open_access_etds Part of the Broadcast and Video Studies Commons, Journalism Studies Commons, and the Mass Communication Commons Let us know how access to this document benefits ou.y Recommended Citation Higgins-Dobney, Carey Lynne, "News Work: the Impact of Corporate Newsroom Culture on News Workers & Community Reporting" (2018). Dissertations and Theses. Paper 4410. https://doi.org/10.15760/etd.6307 This Dissertation is brought to you for free and open access. It has been accepted for inclusion in Dissertations and Theses by an authorized administrator of PDXScholar. Please contact us if we can make this document more accessible: [email protected]. News Work: The Impact of Corporate Newsroom Culture on News Workers & Community Reporting by Carey Lynne Higgins-Dobney A dissertation submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Urban Studies Dissertation Committee: Gerald Sussman, Chair Greg Schrock Priya Kapoor José Padín Portland State University 2018 © 2018 Carey Lynne Higgins-Dobney News Work i Abstract By virtue of their broadcast licenses, local television stations in the United States are bound to serve in the public interest of their community audiences. As federal regulations of those stations loosen and fewer owners increase their holdings across the country, however, local community needs are subjugated by corporate fiduciary responsibilities. Business practices reveal rampant consolidation of ownership, newsroom job description convergence, skilled human labor replaced by computer automation, and economically-driven downsizings, all in the name of profit. -

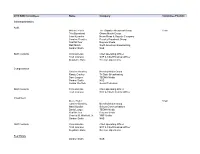

2019 Committees Roster.Xlsx

2019 NAB Committees Name Company Committee Position Joint Committees Audit Michael Fiorile The Dispatch Broadcast Group Chair Trila Bumstead Ohana Media Group John Kueneke News-Press & Gazette Company Caroline Beasley Beasley Broadcast Group Paul McTear Raycom Media Matt Mnich North American Broadcasting Gordon Smith NAB Staff Contacts Chris Ornelas Chief Operating Officer Trish Johnson SVP & Chief Financial Officer Stephanie Bone Director, Operations Compensation Caroline Beasley Beasley Media Group Randy Gravley Tri State Broadcasting Dave Lougee TEGNA Media Gordon Smith NAB Jordan Wertlieb Hearst Television Staff Contacts Chris Ornelas Chief Operating Officer Trish Johnson SVP & Chief Financial Officer Investment Steve Fisher Chair Caroline Beasley Beasley Media Group Marci Burdick Schurz Communications David Lougee TEGNA Media Paul McTear Raycom Media Charles M. Warfield, Jr. YMF Media Gordon Smith NAB Staff Contacts Chris Ornelas Chief Operating Officer Trish Johnson SVP & Chief Financial Officer Stephanie Bone Director, Operations Real Estate Gordon Smith NAB 2019 NAB Committees Name Company Committee Position Caroline Beasley Beasley Media Group Michael Fiorile The Dispatch Broadcast Group Paul Karpowicz Meredith Corporation Charles M. Warfield, Jr. YMF Media Staff Contact Steve Newberry EVP, Strategic Planning and Industry Affairs Bylaws Committee Darrell Brown Bonneville International Corp. Susan Fox The Walt Disney Company Kathy Clements Tribune Broadcasting Company John Zimmer Zimmer Radio of Mid-Missouri, Inc. Carolyn Becker Riverfront Broadcasting LLC Collin Jones Cumulus Media Inc. Caroline Beasley Beasley Media Group Randy Gravley Tri State Communications Inc Jordan Wertlieb Hearst Television Inc. Staff Contact Rick Kaplan General Counsel and EVP, Legal and Regulatory Affairs Dues Committee Tom Walker Mid-West Family Broadcasting Dave Santrella Salem Media Group Joe DiScipio Fox Television Stations, LLC Ralph Oakley Quincy Media, Inc. -

530 CIAO BRAMPTON on ETHNIC AM 530 N43 35 20 W079 52 54 09-Feb

frequency callsign city format identification slogan latitude longitude last change in listing kHz d m s d m s (yy-mmm) 530 CIAO BRAMPTON ON ETHNIC AM 530 N43 35 20 W079 52 54 09-Feb 540 CBKO COAL HARBOUR BC VARIETY CBC RADIO ONE N50 36 4 W127 34 23 09-May 540 CBXQ # UCLUELET BC VARIETY CBC RADIO ONE N48 56 44 W125 33 7 16-Oct 540 CBYW WELLS BC VARIETY CBC RADIO ONE N53 6 25 W121 32 46 09-May 540 CBT GRAND FALLS NL VARIETY CBC RADIO ONE N48 57 3 W055 37 34 00-Jul 540 CBMM # SENNETERRE QC VARIETY CBC RADIO ONE N48 22 42 W077 13 28 18-Feb 540 CBK REGINA SK VARIETY CBC RADIO ONE N51 40 48 W105 26 49 00-Jul 540 WASG DAPHNE AL BLK GSPL/RELIGION N30 44 44 W088 5 40 17-Sep 540 KRXA CARMEL VALLEY CA SPANISH RELIGION EL SEMBRADOR RADIO N36 39 36 W121 32 29 14-Aug 540 KVIP REDDING CA RELIGION SRN VERY INSPIRING N40 37 25 W122 16 49 09-Dec 540 WFLF PINE HILLS FL TALK FOX NEWSRADIO 93.1 N28 22 52 W081 47 31 18-Oct 540 WDAK COLUMBUS GA NEWS/TALK FOX NEWSRADIO 540 N32 25 58 W084 57 2 13-Dec 540 KWMT FORT DODGE IA C&W FOX TRUE COUNTRY N42 29 45 W094 12 27 13-Dec 540 KMLB MONROE LA NEWS/TALK/SPORTS ABC NEWSTALK 105.7&540 N32 32 36 W092 10 45 19-Jan 540 WGOP POCOMOKE CITY MD EZL/OLDIES N38 3 11 W075 34 11 18-Oct 540 WXYG SAUK RAPIDS MN CLASSIC ROCK THE GOAT N45 36 18 W094 8 21 17-May 540 KNMX LAS VEGAS NM SPANISH VARIETY NBC K NEW MEXICO N35 34 25 W105 10 17 13-Nov 540 WBWD ISLIP NY SOUTH ASIAN BOLLY 540 N40 45 4 W073 12 52 18-Dec 540 WRGC SYLVA NC VARIETY NBC THE RIVER N35 23 35 W083 11 38 18-Jun 540 WETC # WENDELL-ZEBULON NC RELIGION EWTN DEVINE MERCY R. -

Exhibit 2181

Exhibit 2181 Case 1:18-cv-04420-LLS Document 131 Filed 03/23/20 Page 1 of 4 Electronically Filed Docket: 19-CRB-0005-WR (2021-2025) Filing Date: 08/24/2020 10:54:36 AM EDT NAB Trial Ex. 2181.1 Exhibit 2181 Case 1:18-cv-04420-LLS Document 131 Filed 03/23/20 Page 2 of 4 NAB Trial Ex. 2181.2 Exhibit 2181 Case 1:18-cv-04420-LLS Document 131 Filed 03/23/20 Page 3 of 4 NAB Trial Ex. 2181.3 Exhibit 2181 Case 1:18-cv-04420-LLS Document 131 Filed 03/23/20 Page 4 of 4 NAB Trial Ex. 2181.4 Exhibit 2181 Case 1:18-cv-04420-LLS Document 132 Filed 03/23/20 Page 1 of 1 NAB Trial Ex. 2181.5 Exhibit 2181 Case 1:18-cv-04420-LLS Document 133 Filed 04/15/20 Page 1 of 4 ATARA MILLER Partner 55 Hudson Yards | New York, NY 10001-2163 T: 212.530.5421 [email protected] | milbank.com April 15, 2020 VIA ECF Honorable Louis L. Stanton Daniel Patrick Moynihan United States Courthouse 500 Pearl St. New York, NY 10007-1312 Re: Radio Music License Comm., Inc. v. Broad. Music, Inc., 18 Civ. 4420 (LLS) Dear Judge Stanton: We write on behalf of Respondent Broadcast Music, Inc. (“BMI”) to update the Court on the status of BMI’s efforts to implement its agreement with the Radio Music License Committee, Inc. (“RMLC”) and to request that the Court unseal the Exhibits attached to the Order (see Dkt. -

Scanned Document

Before the FEDERAL COMMUNICATIONS COMMISSION Washington, DC 20554 In the Matter of ) ) Expanding the Economic and Innovation ) Opportunities of Spectrum Through Incentive ) GN Docket No. 12-268 Auctions ) COMMENTS OF BAHAKEL COMMUNICATIONS, LTD. Bahakel Communications, Ltd. ("Bahakel"), by its attorneys, hereby submits its comments in response to the Notice ofProposed Rulemaking C'NPRM') released by the Federal Communications Commission ("FCC") in the above-referenced proceeding. 1 Bahakel, through subsidiaries, owns six full-power television stations and six radio stations mainly in the Southeast, and it has been serving local communities for over half a century. The NPRM seeks comment on the FCC's implementation of the Middle Class Tax Relief and Jobs Creation Act of 2012 (the "Spectrum Act").2 The NPRM raises scores of proposals, two of which concern Bahakel and on which it comments. First, the NPRM proposes to protect in any repack or reconfiguration of allotments only faci lities that were licensed, or for which an application for license to cover facilities was already on file with the Commission, as of February 22, 20 12.3 This proposal exceeds the requirements of the Spectrum Act. If implemented, it would represent agency action that is arbitrary and capricious, unfair, and contrary to the public interest for those stations that, at great expense, 1 Expanding the Economic and innovation Opportunities ofSpectrum Through incentive Auctions, Notice ofProposed Rulemaldng, GN Docket No. 12-268, released Oct. 2, 2012. 2 Middle Class Tax Relief and Job Creation Act of2012, Pub. L. No. 112-96, 126 Stat 156 (2012). 3 NPRMat ~98 . have completed construction of facilities that had been the subject of applications pending before the Spectrum Act's enactment but may not have been licensed by that date. -

Licensing and Management System

Approved by OMB (Office of Management and Budget) 3060-0010 September 2019 (REFERENCE COPY - Not for submission) Commercial Broadcast Stations Biennial Ownership Report (FCC Form 323) File Number: 0000103093 Submit Date: 2020-01-30 FRN: 0020019436 Purpose: Commercial Broadcast Stations Biennial Ownership Report Status: Received Status Date: 01/30/2020 Filing Status: Active Section I - General Information 1. Respondent FRN Entity Name 0005008289 Bahakel Communications, Ltd. Street City (and Country if non U.S. State ("NA" if non-U.S. Zip Address address) address) Code Phone Email c/o Charlotte NC 28205 +1 (704) 372- bposton@bahakel. Beverly 4434 com Poston One Televsion Place 2. Contact Name Organization Representative M. Anne Swanson Wilkinson Barker Knauer, LLP Street City (and Country if non U.S. Zip Address address) State Code Phone Email 1800 M Washington DC 20036 +1 (202) 383- aswanson@wbklaw. Street, NW 3342 com Suite 800N Not Applicable 3. Application Filing Fee 4. Nature of (a) Provide the following information about the Respondent: Respondent Relationship to stations/permits Entity required to file a Form 323 because it holds an attributable interest in one or more Licensees Nature of Respondent For-profit corporation (b) Provide the following information about this report: Purpose Biennial "As of" date 10/01/2019 When filing a biennial ownership report or validating and resubmitting a prior biennial ownership report, this date must be Oct. 1 of the year in which this report is filed. 5. Licensee(s) and Station(s) Respondent is filing this report to cover the following Licensee(s) and station(s): Licensee/Permittee Name FRN Tennessee Broadcasting Partners 0003828696 Fac. -

TV Channel 5-6 Radio Proposal

Before the Federal Communications Commission Washington, D.C. 20554 In the Matter of ) ) Promoting Diversification of Ownership ) MB Docket No 07-294 in the Broadcasting Services ) ) 2006 Quadrennial Regulatory Review – Review of ) MB Docket No. 06-121 the Commission’s Broadcast Ownership Rules and ) Other Rules Adopted Pursuant to Section 202 of ) the Telecommunications Act of 1996 ) ) 2002 Biennial Regulatory Review – Review of ) MB Docket No. 02-277 the Commission’s Broadcast Ownership Rules and ) Other Rules Adopted Pursuant to Section 202 of ) the Telecommunications Act of 1996 ) ) Cross-Ownership of Broadcast Stations and ) MM Docket No. 01-235 Newspapers ) ) Rules and Policies Concerning Multiple Ownership ) MM Docket No. 01-317 of Radio Broadcast Stations in Local Markets ) ) Definition of Radio Markets ) MM Docket No. 00-244 ) Ways to Further Section 257 Mandate and To Build ) MB Docket No. 04-228 on Earlier Studies ) To: Office of the Secretary Attention: The Commission BROADCAST MAXIMIZATION COMMITTEE John J. Mullaney Mark Lipp Paul H. Reynolds Bert Goldman Joseph Davis, P.E. Clarence Beverage Laura Mizrahi Lee Reynolds Alex Welsh SUMMARY The Broadcast Maximization Committee (“BMC”), composed of primarily of several consulting engineers and other representatives of the broadcast industry, offers a comprehensive proposal for the use of Channels 5 and 6 in response to the Commission’s solicitation of such plans. BMC proposes to (1) relocate the LPFM service to a portion of this spectrum space; (2) expand the NCE service into the adjacent portion of this band; and (3) provide for the conversion and migration of all AM stations into the remaining portion of the band over an extended period of time and with digital transmissions only. -

ABC Affiliates Nor Did the Notice Include Any of the Complaints

No. 10-1293 In the Supreme Court of the United States -------------------------------------------------- FEDERAL COMMUNICATIONS COMMISSION ET AL., Petitioners, v. FOX TELEVISION STATIONS, INC. ET AL., Respondents. FEDERAL COMMUNICATIONS COMMISSION ET AL., Petitioners, v. ABC, INC. ET AL., Respondents. On Petition For A Writ Of Certiorari To The United States Court Of Appeals For The Second Circuit -------------------------------------------------- BRIEF IN OPPOSITION OF RESPONDENTS ABC TELEVISION AFFILIATES ASSOCIATION ET AL. Wade H. Hargrove Counsel of Record Mark J. Prak David Kushner Julia C. Ambrose BROOKS, PIERCE, MCLENDON, HUMPHREY & LEONARD, LLP 150 Fayetteville Street Suite 1600 Raleigh, N.C. 27601 919.839.0300 May 23, 2011 [email protected] [Additional Respondents Listed on Inside Cover] THE LEX GROUPDC 1825 K Street, N.W. Suite 103 Washington, D.C. 20006 (202) 955-0001 (800) 856-4419 Fax: (202) 955-0022 www.thelexgroup.com Additional Respondents Joining in Brief in Opposition Citadel Communications, LLC, WKRN, G.P., Young Broadcasting of Green Bay, Inc., WKOW Television, Inc., WSIL-TV, Inc., Cedar Rapids Television Company, Centex Television Limited Partnership, Channel 12 of Beaumont, Inc., Duhamel Broadcasting Enterprises, Gray Television Licensee, Inc., KATC Communications, Inc., KATV, LLC, KDNL Licensee, LLC, KETV Hearst-Argyle Television, Inc., KLTV/KTRE License Subsidiary, LLC, KSTP-TV, LLC, KSWO Television Company, Inc., KTBS, Inc., KTUL, LLC, KVUE Television, Inc., McGraw-Hill Broadcasting Company, Inc., -

Broadcast Market Research TV Households

Broadcast Market Research TVHouseholds Everyindustryneedsameasureofthesizeofitsmarketplaceandtheradioandtelevisionindustriesare noexceptions. TELEVISION - U.S. AmajorsourceofsuchmediamarketdataintheUnitedStatesisNielsenMediaResearch(NMR),and oneofthemeasurementsittakesannuallyisTVHouseholds(TVHH).Ahomewithoneoperable TV/monitorisaTVHH,andNielsenisabletoextrapolateits“NationalUniverseEstimates”fromCensus BureaupopulationdatacombinedwiththisexpressionofTVpenetration. WithUsfromDayOne Theadventofbroadcastadvertising,inJuly1941,wascoincidentalwiththedawnofcommercial television,andwithintenyearsmarketresearchinthenewmediumwasinfullswing. SincetheFederalCommunicationsCommission(FCC)allowedthosefirstTVads—forSunOil,Lever Bros.,Procter&GambleandtheBulovaWatchCompany—reliableaudiencemeasurementhasbeen necessaryformarketerstotargettheircampaigns.TheproliferationofdevicesforviewingTVcontent andthecontinualevolutionofconsumerbehaviorhavemadethetaskmoreimportant—andmore challenging—thanever. Nevertheless,whiletherealityof“TVEverywhere”hasundeniablycomplicatedtheworkofaudience measurement,theuseofonerudimentarygaugepersists—thenumberofhouseholdswithaset,TVHH. NielsenMediaResearch IntheUnitedStates,NielsenMediaResearch(NMR)istheauthoritativesourcefortelevisionaudience measurement(TAM).BestͲknownforitsratingssystem,whichhasdeterminedthefatesofmany televisionprograms,NMRalsotracksthenumberofhouseholdsinaDesignatedMarketArea(DMA) thatownaTV. PublishedannuallybeforethestartofthenewTVseasoninSeptember,theseUniverseEstimates, representingpotentialregionalaudiences,areusedbyadvertiserstoplaneffectivecampaigns. -

Freq Call State Location U D N C Distance Bearing

AM BAND RADIO STATIONS COMPILED FROM FCC CDBS DATABASE AS OF FEB 6, 2012 POWER FREQ CALL STATE LOCATION UDNCDISTANCE BEARING NOTES 540 WASG AL DAPHNE 2500 18 1107 103 540 KRXA CA CARMEL VALLEY 10000 500 848 278 540 KVIP CA REDDING 2500 14 923 295 540 WFLF FL PINE HILLS 50000 46000 1523 102 540 WDAK GA COLUMBUS 4000 37 1241 94 540 KWMT IA FORT DODGE 5000 170 790 51 540 KMLB LA MONROE 5000 1000 838 101 540 WGOP MD POCOMOKE CITY 500 243 1694 75 540 WXYG MN SAUK RAPIDS 250 250 922 39 540 WETC NC WENDELL-ZEBULON 4000 500 1554 81 540 KNMX NM LAS VEGAS 5000 19 67 109 540 WLIE NY ISLIP 2500 219 1812 69 540 WWCS PA CANONSBURG 5000 500 1446 70 540 WYNN SC FLORENCE 250 165 1497 86 540 WKFN TN CLARKSVILLE 4000 54 1056 81 540 KDFT TX FERRIS 1000 248 602 110 540 KYAH UT DELTA 1000 13 415 306 540 WGTH VA RICHLANDS 1000 97 1360 79 540 WAUK WI JACKSON 400 400 1090 56 550 KTZN AK ANCHORAGE 3099 5000 2565 326 550 KFYI AZ PHOENIX 5000 1000 366 243 550 KUZZ CA BAKERSFIELD 5000 5000 709 270 550 KLLV CO BREEN 1799 132 312 550 KRAI CO CRAIG 5000 500 327 348 550 WAYR FL ORANGE PARK 5000 64 1471 98 550 WDUN GA GAINESVILLE 10000 2500 1273 88 550 KMVI HI WAILUKU 5000 3181 265 550 KFRM KS SALINA 5000 109 531 60 550 KTRS MO ST. LOUIS 5000 5000 907 73 550 KBOW MT BUTTE 5000 1000 767 336 550 WIOZ NC PINEHURST 1000 259 1504 84 550 WAME NC STATESVILLE 500 52 1420 82 550 KFYR ND BISMARCK 5000 5000 812 19 550 WGR NY BUFFALO 5000 5000 1533 63 550 WKRC OH CINCINNATI 5000 1000 1214 73 550 KOAC OR CORVALLIS 5000 5000 1071 309 550 WPAB PR PONCE 5000 5000 2712 106 550 WBZS RI -

Rules and ) Other Rules Adopted Pursuant to Section 202 of ) the Telecommunications Act of 1996 ) ) 2010 Quadrennial Regulatory Review – Review of ) MB Docket No

Federal Communications Commission FCC 14-28 Before the Federal Communications Commission Washington, D.C. 20554 In the Matter of ) ) 2014 Quadrennial Regulatory Review – Review of ) MB Docket No. 14-50 the Commission’s Broadcast Ownership Rules and ) Other Rules Adopted Pursuant to Section 202 of ) the Telecommunications Act of 1996 ) ) 2010 Quadrennial Regulatory Review – Review of ) MB Docket No. 09-182 the Commission’s Broadcast Ownership Rules and ) Other Rules Adopted Pursuant to Section 202 of ) the Telecommunications Act of 1996 ) ) Promoting Diversification of Ownership ) MB Docket No. 07-294 In the Broadcasting Services ) ) Rules and Policies Concerning ) MB Docket No. 04-256 Attribution of Joint Sales Agreements ) In Local Television Markets ) ) FURTHER NOTICE OF PROPOSED RULEMAKING AND REPORT AND ORDER Adopted: March 31, 2014 Released: April 15, 2014 Comment Date: [45 days after publication in the Federal Register] Reply Comment Date: [75 days after publication in the Federal Register] By the Commission: Chairman Wheeler and Commissioners Clyburn and Rosenworcel issuing separate statements; Commissioners Pai and O’Rielly dissenting and issuing separate statements. TABLE OF CONTENTS Heading Paragraph # I. INTRODUCTION.................................................................................................................................. 1 II. BACKGROUND.................................................................................................................................... 9 III. MEDIA OWNERSHIP RULES.......................................................................................................... -

Five Things You Should Know About Apple

LEAD-IN ADVERTISING PROGRAMMING STREAMING Five Things You Should Know About Apple TV+ Silicon Valley’s largest innovator unveils a video strategy amid a hodgepodge of new services By Daniel Frankel and Mike Farrell EARLY A DOZEN YEARS after the introduction of the iPhone, Apple CEO Tim Cook took the stage in Cupertino, NCalifornia, March 25, trumpeting a new era in which the first U.S. company to ever reach a trillion-dollar valuation would focus on services, not gadgets. “For decades, Apple has been creat- ANALYSIS ing world-class hardware and world- class software,” Cook said. “We’ve also been creating a world-class collection of world-class services. and that’s what today is all about.” After announcing a Spotify-like service for newspapers and magazines that expands on its News app, a subscription streaming platform for video games and a new credit-card business, Apple got to the reveal the world had been waiting for — the intro- duction of a newly reinvented and significantly expanded streaming video platform that would rival those of Netflix and Amazon. Instead of the typical hushed awe in the audience, though, what followed was a lot of head-scratching. Sure, the star power was out in force at the Steve Jobs Theater, with Steven Spielberg, Jennifer Aniston, Reese selection of services — HBO Go, Hulu, Oprah Winfrey and a Witherspoon, Steve Carell and Oprah Winfrey among Amazon Prime Video and CBS All Access, crowd full of Hollywood A-listers joined Apple the big names touting original series projects for Apple’s just to name a few — and watches and pays CEO Tim Cook (l.) new subscription VOD service, Apple TV+.