The Rise and Fall of Neoliberal Capitalism

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Azimuth Corporation Employee Handbook

Azimuth Corporation Employee Handbook ABOUT THIS HANDBOOK/DISCLAIMER This Employee Handbook is designed to acquaint you with Azimuth Corporation and to provide employees with an overview of the policies, procedures and management practices affecting employment with our company. Unless otherwise stated, these policies and practices apply to all Azimuth employees as of the date of this Employee Handbook, and those that may begin after its effective date. This Employee Handbook outlines the programs developed by Azimuth for the benefit of its employees, and the employee's responsibility to Azimuth and its customers. Each employee should read, understand and comply with the provisions of this handbook. Please take the necessary time to read it. Please contact your Supervisor and/or the Human Resources Department if you require additional information. Neither this handbook nor any other verbal or written communication by a management representative is, nor should it be considered to be, an agreement, contract of employment, express or implied, or a promise of treatment in any particular manner in any given situation, nor does it confer any contractual rights whatsoever. This Employee Handbook does not constitute a contract of employment between Azimuth and its employees, whether expressed or implied. The handbook, nor any portion of it, does not preempt the doctrine of employment-at-will. Azimuth Corporation adheres to the policy of employment at will, which permits the Company or the employee to end the employment relationship at any time, for any reason, with or without cause or notice. Many matters covered by this handbook, such as benefit plan descriptions, are also described in separate Company documents. -

Merchants and the Origins of Capitalism

Merchants and the Origins of Capitalism Sophus A. Reinert Robert Fredona Working Paper 18-021 Merchants and the Origins of Capitalism Sophus A. Reinert Harvard Business School Robert Fredona Harvard Business School Working Paper 18-021 Copyright © 2017 by Sophus A. Reinert and Robert Fredona Working papers are in draft form. This working paper is distributed for purposes of comment and discussion only. It may not be reproduced without permission of the copyright holder. Copies of working papers are available from the author. Merchants and the Origins of Capitalism Sophus A. Reinert and Robert Fredona ABSTRACT: N.S.B. Gras, the father of Business History in the United States, argued that the era of mercantile capitalism was defined by the figure of the “sedentary merchant,” who managed his business from home, using correspondence and intermediaries, in contrast to the earlier “traveling merchant,” who accompanied his own goods to trade fairs. Taking this concept as its point of departure, this essay focuses on the predominantly Italian merchants who controlled the long‐distance East‐West trade of the Mediterranean during the Middle Ages and Renaissance. Until the opening of the Atlantic trade, the Mediterranean was Europe’s most important commercial zone and its trade enriched European civilization and its merchants developed the most important premodern mercantile innovations, from maritime insurance contracts and partnership agreements to the bill of exchange and double‐entry bookkeeping. Emerging from literate and numerate cultures, these merchants left behind an abundance of records that allows us to understand how their companies, especially the largest of them, were organized and managed. -

Capacity Utilization, Inflation and Monetary Policy

Capacity Utilization, Inflation and Monetary Policy: Classicals, post-Keynesians and the New Keynesian Consensus Peter Kriesler and Marc Lavoie1 Abstract The paper looks at the adjustment process towards long run equilibrium within Marxian models, defined in terms of normal rates of capacity utilization. The model is reduced to three essential equations: an IS equation, a Phillips curve equation and an central bank reaction function. It is shown that long run convergence depends on the specific inflation (Phillips curve) equation, and on the central bank setting a zero inflationary target. When these conditions are relaxed, the results are shown to accord more closely with post-Keynesian results. The Marxian model is then contrasted with New Consensus models, which only varies in its inflation/Phillips curve equation. Post-Keynesian criticisms of both the IS and the Phillips curve equation are considered, and suggestions for a post-Keynesian alternative are made. Keywords: monetary policy, central bank, inflation, capacity utilization, post-Keynesian, New- Keynesian JEL classification: E12, E40, E52, E58 In an extremely interesting paper, Duménil and Lévy (Duménil and Lévy 1999) explore the adjustment mechanism of an economy towards a long run equilibrium with capacity utilization at normal levels − a fully adjusted position as the Sraffians would call it, or a classical long-term equilibrium as Duménil and Lévy have it. Short run equilibrium within their model is of the Keynes/Kalecki type, with variability in levels of capacity utilization. One distinctive feature of their model is that it is not the forces of competition which push the economy to a fully adjusted position, but rather aspects of the macro economy coupled with the behaviour of the central bank. -

COMMENTARY to PROFESSOR MURRAY Phil Reed*

COMMENTARY TO PROFESSOR MURRAY Phil Reed* In his article, Professor Murray provides an excellent response to the Business Roundtable’s (BRT) Statement on the Purpose of a Corporation, and outlines the ways that an interested corporation could implement governance changes to reflect the statement. Reactions to the Business Roundtable’s statement, as described by Professor Murray, could be grouped into one of three categories – optimistic praise, supportive pessimism, and blunt opposition. As Professor Murray has done an excellent job of addressing the second category of reactions, supportive pessimism, it falls upon me to address the blunt opposition. I think, however, that there are two modes of opposition to the BRT’s statement. The first mode of opposition is that the signatories of the statement are being insincere in endorsing a commitment to stakeholders, rather than shareholders. The second is opposition to stakeholder theory in the first place. In that view, the BRT should not have issued the statement at all. The sincerity of a signed statement can be readily determined by the behavior of one who signed it. Soon after signing the Business Roundtable’s statement, Amazon-owned Whole Foods made the decision to cut health benefits for part-time workers.1 This move did not do much to inspire confidence in the statement, to put it lightly.2 To the extent that * Phil Reed is a third-year law student at the University of Tennessee College of Law and is scheduled to graduate in May 2020. 1 Bob Bryan, Amazon-Owned Whole Foods’ Decision to Drop Health Benefits for Hundreds of Part-Time Workers Reveals How Promises to Workers Like CEO Jeff Bezos’ Recent Pledge are Worthless, BUS. -

The Fair Labor Standards Act of 1938, As Amended

The Fair LaboR Standards Act Of 1938, As Amended U.S. DepaRtment of LaboR Wage and Hour Division WH Publication 1318 Revised May 2011 material contained in this publication is in the public domain and may be reproduced fully or partially, without permission of the Federal Government. Source credit is requested but not required. Permission is required only to reproduce any copyrighted material contained herein. This material may be contained in an alternative Format (Large Print, Braille, or Diskette), upon request by calling: (202) 693-0675. Toll-free help line: 1-866-187-9243 (1-866-4-USWAGE) TTY TDD* phone: 1-877-889-5627 *Telecommunications Device for the Deaf. Internet: www.wagehour.dol.gov The Fair Labor Standards Act of 1938, as amended 29 U.S.C. 201, et seq. To Provide for the establishment of fair labor standards in emPloyments in and affecting interstate commerce, and for other Purposes. Be it enacted by the Senate and House of Representatives of the United States of America in Congress assembled, That this Act may be cited as the “Fair Labor Standards Act of 1938”. § 201. Short title This chapter may be cited as the “Fair Labor Standards Act of 1938”. § 202. Congressional finding and declaration of Policy (a) The Congress finds that the existence, in industries engaged in commerce or in the Production of goods for commerce, of labor conditions detrimental to the maintenance of the minimum standard of living necessary for health, efficiency, and general well-being of workers (1) causes commerce and the channels and instrumentalities of commerce to be used to sPread and Perpetuate such labor conditions among the workers of the several States; (2) burdens commerce and the free flow of goods in commerce; (3) constitutes an unfair method of competition in commerce; (4) leads to labor disputes burdening and obstructing commerce and the free flow of goods in commerce; and (5) interferes with the orderly and fair marketing of goods in commerce. -

489.108 Name. 1. the Name of a Limited Liability Company Must Contain the Words “Limited Liability Company” Or “Limited Company” Or the Abbreviation “L

1 REVISED UNIFORM LIMITED LIABILITY COMPANY ACT, §489.108 489.108 Name. 1. The name of a limited liability company must contain the words “limited liability company” or “limited company” or the abbreviation “L. L. C.”, “LLC”, “L. C.”, or “LC”. “Limited” may be abbreviated as “Ltd.”, and “company” may be abbreviated as “Co.”. 2. Unless authorized by subsection 3, the name of a limited liability company must be distinguishable in the records of the secretary of state from all of the following: a. The name of each person that is not an individual and that is incorporated, organized, or authorized to transact business in this state. b. Each name reserved under section 489.109. 3. A limited liability company may apply to the secretary of state for authorization to use a name that does not comply with subsection 2. The secretary of state shall authorize use of the name applied for if either of the following applies: a. The present user, registrant, or owner of the noncomplying name consents in a signed record to the use and submits an undertaking in a form satisfactory to the secretary of state to change the noncomplying name to a name that complies with subsection 2 and is distinguishable in the records of the secretary of state from the name applied for. b. The applicant delivers to the secretary of state a certified copy of the final judgment of a court establishing the applicant’s right to use in this state the name applied for. 4. A limited liability company may use the name, including the fictitious name, of another entity that is used in this state if the other entity is formed under the law of this state or is authorized to transact business in this state and the proposed user limited liability company meets any of the following conditions: a. -

Citigroup Inc.; Rule 14A-8 No-Action Letter

*** FISMA & OMB Memorandum M-07-16 ENCLOSURE 1 THE PROPOSAL AND RELATED CORRESPONDENCE (IF ANY) ENCLOSURE 2 STATEMENT OF INTENT TO EXCLUDE STOCKHOLDER PROPOSAL The Proposal requests that the Company’s Board of Directors (the “Board”) conduct a comprehensive review of Citigroup’s governance documents, making recommendations to the shareholders on specifically how the “Purpose of a Corporation” signed by our Chief Executive Officer can be fully implemented by board and management, and recommending amendments to governance documents such as the bylaws, Company’s Articles of Incorporation, or Committee Charters to fulfill the new statement of purpose. The Proponent does not reproduce, or really even try to describe, the “Purpose of a Corporation” that is the subject of his Proposal. The Company believes the Proponent is referring to the Statement of the Purpose of a Corporation issued by the Business Roundtable (the “Statement”), which was signed by the chief executive officers of 181 companies, including the Company’s Chief Executive Officer (the “CEO”). The Statement reduces to writing the signatory companies’ commitment to all of their stakeholders, specifically in five areas: (1) “delivering value to the company’s customers”; (2) “investing in our employees”; (3) “dealing fairly and ethically with our suppliers”; (4) “supporting the communities in which we work”; and (5) “generating long- term value for shareholders, who provide the capital that allows companies to invest, grow and innovate.”1 A copy of the Statement is attached hereto as Enclosure 3. THE PROPOSAL MAY BE EXCLUDED BECAUSE IT IS VAGUE AND MISLEADING. The Proposal may be excluded pursuant to Rule 14a-8(i)(3) because the Proposal is vague and misleading.2 The Proposal is vague because stockholders cannot understand the action requested by the Proposal without referring to materials outside the Proposal. -

Employment and Capacity Utilization Over the Business Cycle

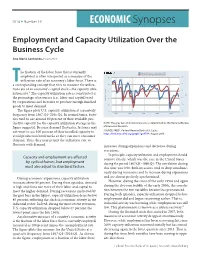

2016 n Number 19 ECONOMIC Synopses Employment and Capacity Utilization Over the Business Cycle Ana Maria Santacreu, Economist he fraction of the labor force that is currently Capacity Utilization: Total Industry (left) 100-Civilian Unemployment Rate (right) 98 employed is often interpreted as a measure of the 90 utilization rate of an economy’s labor force. There is 96 T 85 a corresponding concept that tries to measure the utiliza- tion rate of an economy’s capital stock—the capacity utili- 94 80 zation rate.1 The capacity utilization rate is constructed as 100-% 92 the percentage of resources (i.e., labor and capital) used 75 Percent of Capacity by corporations and factories to produce enough finished 90 goods to meet demand. 70 88 The figure plots U.S. capacity utilization at a quarterly 65 frequency from 1967:Q1–2016:Q1. In normal times, facto- 1970 1980 1990 2000 2010 ries tend to use around 80 percent of their available pro- fred.stlouisfed.org myf.red/g/6ZXZ ductive capacity (as the capacity utilization average in the NOTE: The gray bars indicate recessions as determined by the National Bureau figure suggests). Because demand fluctuates, factories may of Economic Research. SOURCE: FRED®, Federal Reserve Bank of St. Louis; not want to use 100 percent of their installed capacity to https://fred.stlouisfed.org/graph/?g=6TA4; August 2016. avoid production bottlenecks so they can meet consumer demand. Thus, they may permit the utilization rate to fluctuate with demand. increases during expansions and decreases during recessions. In principle, capacity utilization and employment should Capacity and employment are affected comove closely, which was the case in the United States by cyclical factors, but employment during the period 1967:Q1–1990:Q1. -

Shareholder Capitalism a System in Crisis New Economics Foundation Shareholder Capitalism

SHAREHOLDER CAPITALISM A SYSTEM IN CRISIS NEW ECONOMICS FOUNDATION SHAREHOLDER CAPITALISM SUMMARY Our current, highly financialised, form of shareholder capitalism is not Shareholder capitalism just failing to provide new capital for – a system driven by investment, it is actively undermining the ability of listed companies to the interests of reinvest their own profits. The stock shareholder-backed market has become a vehicle for and market-fixated extracting value from companies, not companies – is broken. for injecting it. No wonder that Andy Haldane, Chief Economist of the Bank of England, recently suggested that shareholder capitalism is ‘eating itself.’1 Corporate governance has become dominated by the need to maximise short-term shareholder returns. At the same time, financial markets have grown more complex, highly intermediated, and similarly short- termist, with shares increasingly seen as paper assets to be traded rather than long-term investments in sound businesses. This kind of trading is a zero-sum game with no new wealth, let alone social value, created. For one person to win, another must lose – and increasingly, the only real winners appear to be the army of financial intermediaries who control and perpetuate the merry-go- round. There is nothing natural or inevitable about the shareholder-owned corporation as it currently exists. Like all economic institutions, it is a product of political and economic choices which can and should be remade if they no longer serve our economy, society, or environment. Here’s the impact -

Outline of a Business Plan Plan Summary Company And

APPENDIX B OUTLINE OF A BUSINESS PLAN A business plan is a description of your proposed or existing business and should include information on the business' products or services, markets, marketing strategies, manufacturing procedures, ownership, management structure, needs (organizational, personnel and financial) and projections. A well-prepared business plan serves two important functions. First, it is a basic management tool that helps guide the future direction of your company. Second, it is a mandatory document if you plan to seek business financing. How much detail should your business plan contain and in what order? What will help make it effective in communicating your proposed or existing company's strengths and potential? The purpose of this section of the handbook is to help you answer such questions. Not all plans need to be alike. Some sections of this outline may be more applicable to your company than others. You should make every effort to tailor your plan to your company's specific set of circumstances. PLAN SUMMARY A well-written business plan summary allows prospective lenders and investors to quickly decide if they want to examine the entire plan in detail. Therefore, your objective in the plan summary is to convince them to study the plan further. Although a plan summary appears first, it should be the last part you write. The summary should briefly highlight the key elements of your business plan and include the following points: - A brief history of your business or business concept; - A description of your products or services with emphasis on their distinguishing features, the market needs they will meet, the market potential and assessment of the competition: - How the products will be made, or services performed; - An outline of your management team's experience and talent; - A summary of your financial projections; and - How much money you are seeking, in what form, for what purpose and how it will be repaid. -

Privatization of Public Social Services a Background Paper Demetra Smith Nightingale, Nancy M

Privatization of Public Social Services A Background Paper Demetra Smith Nightingale, Nancy M. Pindus This paper was prepared at the Urban Institute for U.S. Department of Labor, Office of the Assistant Secretary for Document date: October 15, 1997 Policy, under DOL Contract No. J-9-M-5-0048, #15. Released online: October 15, 1997 Opinions expressed are those of the authors and do not necessarily represent the positions of DOL, the Urban Institute or its sponsors. The views expressed are those of the author and do not necessarily reflect those of the Urban Institute, its board, its sponsors, or other authors in the series 1. Introduction The purposes of the paper are to provide a general overview of the extent of privatization of public services in the areas of social services, welfare, and employment; rationales for privatizing service delivery, and evidence of effectiveness or problems. Examples are included to highlight specific types of privatization and actual operational experience. The paper is not intended to be a comprehensive treatment of the overall subject of privatization, but rather a brief review of issues and experiences specifically related to the delivery of employment and training, welfare, and social services. The key points that are drawn from a review of the literature are: There is no single definition of privatization. Privatization covers a broad range of methods and models, including contracting out for services, voucher programs, and even the sale of public assets to the private sector. But for the purposes of this paper, privatization refers to the provision of publicly-funded services and activities by non-governmental entities. -

Imbalance Game 2.0: a Tale of Two Productivities

NEW THINKING Imbalance Game 2.0: A Tale of Two Productivities Michael Craig, CFA Vice President & Director Haining Zha, CFA Vice President September 2017 Almost nine years after the financial crisis, the global economy remains mired in low growth. Low productivity growth is certainly a key contributing factor, but our research shows that current productivity measures don’t tell the whole story. In this article, we propose a fundamental change to how people should examine productivity: we believe the supply and demand sides should be viewed separately to obtain more robust insights. Taking this approach allows us to differentiate supply-side progress from demand-side malaise and shows that the economy may be more promising than commonly thought. In addition, it highlights large supply-side divergences within and across different sectors of the economy, which are not reflected in the aggregate productivity measure – potentially leading to a distorted economic picture. Viewing productivity through this new lens, we believe that: • Nominal economic growth will remain low • Inflation will remain subdued • Interest rates will stay lower for longer • Technology-driven progress and persistent supply-side divergence will create investment risks and opportunities in equity markets In the investment world, economic growth is a big deal. We believe investment returns across asset classes can ultimately be traced back to one source: economic growth. Occasionally, asset prices can deviate from fundamentals, but over the long term, the relationship between returns and growth is very strong. That’s why it is critical to have a better understanding of the low growth phenomenon and key contributing factors, such as productivity.