Condensed Interim Report & Unaudited Financial Statements

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Nov 9, 2007 Release Ube Industries Announces Short-Form Merger Of

Company name: Ube Industries, Ltd. Representative: Hiroaki Tamura President and Representative Director Shares listed on: First Section of Tokyo Stock Exchange, Fukuoka Stock Exchange Security code number: 4208 Contact: Yasuko Sakamoto General Manager, IR/PR Department Tel: +81-3-5419-6110 Ube Industries Announces Short-Form Merger of Subsidiary TOKYO, November 9, 2007 — Ube Industries, Ltd. today announced that it will absorb a subsidiary, EUP Co., Ltd., by a merger. The decision was approved today at a meeting of the Board of Directors. Details of the merger are outlined below. 1. Purpose of Merger EUP Co., Ltd. engages in recycling of waste plastics and other materials as prescribed under the Containers and Packaging Recycling Law, utilizing a process that produces synthesis gas for the chemicals industry. The company was established as a 50/50 joint venture by Ube Industries, Ltd. and Ebara Corporation and has been operating since fiscal 2001. On September 30, 2007, EUP Co., Ltd. was made into a wholly-owned subsidiary of Ube Industries, Ltd. in order to streamline and improve the efficiency of its operations in unison with Ube Industries, Ltd. The move was designed to position the company to generate stable profits moving forward, taking into account the increasingly competitive nature of the business environment for EUP Co., Ltd. By absorbing EUP Co., Ltd. through a merger, Ube Industries, Ltd. is aiming to further streamline the operations of the business unit. 2. Details of Merger A. Schedule for Merger Scheduled meeting by Board of Directors: November 9, 2007 Scheduled signing of merger agreement: November 9, 2007 General meeting of shareholders to approve the merger agreement: Ube Industries, Ltd.: Ube Industries, Ltd. -

JPX-Nikkei Index 400 Constituents (Applied on August 31, 2021) Published on August 6, 2021 No

JPX-Nikkei Index 400 Constituents (applied on August 31, 2021) Published on August 6, 2021 No. of constituents : 400 (Note) The No. of constituents is subject to change due to de-listing. etc. (Note) As for the market division, "1"=1st section, "2"=2nd section, "M"=Mothers, "J"=JASDAQ. Code Market Divison Issue Code Market Divison Issue 1332 1 Nippon Suisan Kaisha,Ltd. 3048 1 BIC CAMERA INC. 1417 1 MIRAIT Holdings Corporation 3064 1 MonotaRO Co.,Ltd. 1605 1 INPEX CORPORATION 3088 1 Matsumotokiyoshi Holdings Co.,Ltd. 1719 1 HAZAMA ANDO CORPORATION 3092 1 ZOZO,Inc. 1720 1 TOKYU CONSTRUCTION CO., LTD. 3107 1 Daiwabo Holdings Co.,Ltd. 1721 1 COMSYS Holdings Corporation 3116 1 TOYOTA BOSHOKU CORPORATION 1766 1 TOKEN CORPORATION 3141 1 WELCIA HOLDINGS CO.,LTD. 1801 1 TAISEI CORPORATION 3148 1 CREATE SD HOLDINGS CO.,LTD. 1802 1 OBAYASHI CORPORATION 3167 1 TOKAI Holdings Corporation 1803 1 SHIMIZU CORPORATION 3231 1 Nomura Real Estate Holdings,Inc. 1808 1 HASEKO Corporation 3244 1 Samty Co.,Ltd. 1812 1 KAJIMA CORPORATION 3254 1 PRESSANCE CORPORATION 1820 1 Nishimatsu Construction Co.,Ltd. 3288 1 Open House Co.,Ltd. 1821 1 Sumitomo Mitsui Construction Co., Ltd. 3289 1 Tokyu Fudosan Holdings Corporation 1824 1 MAEDA CORPORATION 3291 1 Iida Group Holdings Co.,Ltd. 1860 1 TODA CORPORATION 3349 1 COSMOS Pharmaceutical Corporation 1861 1 Kumagai Gumi Co.,Ltd. 3360 1 SHIP HEALTHCARE HOLDINGS,INC. 1878 1 DAITO TRUST CONSTRUCTION CO.,LTD. 3382 1 Seven & I Holdings Co.,Ltd. 1881 1 NIPPO CORPORATION 3391 1 TSURUHA HOLDINGS INC. 1893 1 PENTA-OCEAN CONSTRUCTION CO.,LTD. -

CORPORATE PROFILE Corporate Philosophy

CORPORATE PROFILE Corporate Philosophy Mission Statement Creating Value for Customers via New Ideas ITO Corporation's mission is to contribute to our customers and to society via the values born from new pairings and findings. We create opportunities that previously did not exist by connecting together objects, people, companies, and ideas. We strive for a virtuous cycle where we provide new opportunities and value to our customers, which in turn contributes to the products and services born into the world. Value Statement An Organization Which Excites All In order for us to provide customers and society with exciting new opportu- nities, we ourselves must be an innovative organization. Additionally, for us to increase our customer's level of satisfaction and to take actions which contrib- ute to the world, it is important that we spend our time in a valuable way. To achieve the above, we value the following as an organization: Respect each other and understand the value that diversity brings. No discrimination based on gender, nationality, age, experience, etc. Cultivate a harmonious and encouraging work culture, and support the efforts of others Strive for a fulfilling life together, not only with work but also by valuing family and society Provide employment, skill development, and opportunities for advance- ment to those with motivation Ensure that our actions are always fair and moral Vision Statement Improve the World via Moving Equipment Throughout the ages, moving components and equipment have freed people from heavy la- bor, enabled transportation to remote locations, and enriched the lives of people everywhere. During the foundation of our company, we played a role in the post-war recovery by providing to people electrical machinery and other moving items that could be used in the burnt fields of Tokyo. -

Members List

Members list APO Green Productivity Advisory Committee (as of February 2010) Chairperson Mr. Teisuke Kitayama Chairman of the Board Sumitomo Mitsui Banking Corporation Vice-Chairpersons Mr. Yukio Yanase Director Representative Executive Officer President and Chief Operating Officer ORIX Corporation Mr. Hajime Bada President and Chief Executive Officer JFE Steel Corporation Mr. Takashi Yamagishi Executive Vice President, Member of the Board Chief Technology Officer Teijin Limited Prof. Ryoichi Yamamoto Professor Institute of Industrial Science & International Research Center for Sustainable Materials University of Tokyo Mr. Tsuneaki Taniguchi President Japan Productivity Center Advisers Mr. Yoichi Morishita Corporate Counsellor Panasonic Corporation Mr. Masatoshi Yoda Former President of Ebara Corporation Mr. Etsuhiko Shoyama Chairman Emeritus Hitachi, Ltd. Mr. Kazuyoshi Terashima Former Vice President of Ebara Corporation Members Mr. Seiichi Ueyama Managing Director Aeon Retail Co., Ltd. Mr. Hidehiro Shinohara General Manager Environment & Safety Department Ajinomoto Co., Inc. Mr. Katsuhiko Sugie General Manager Amita Corporation Mr. Takeshi Kurashige Producer Social & Environmental Management Department Asahi Breweries, Ltd. Mr. Shuji Kato Director, Member of the Board Chief Social Responsibility Officer Bic Camera, Inc. 539 Mr. Yoshinobu Shizukuishi Manager Marketing Department Biznet Corporation Mr. Kazutoshi Nakamura Manager Environment Communications Department Canon Inc. Mr. Satoru Fujimoto Manager Global Environment Department Daikin Industries, Ltd. Mr. Yasushi Iwao General Manager Marketing Department Deloitte Tohmatsu Evaluation and Certification Organization Co., Ltd. Mr. Tsutomu Ishibashi General Manager Corporate Environmental Management Department Ebara Corporation Mr. Hiroyuki Akiyama Group Manager Environment Management Group, Corporate Social Responsibility Department Fuji Xerox Co., Ltd. Mr. Mitsugu Sato General Manager Advanced Business Group Fujitsu FIP Corporation Ms. Chie Saito G-Project Inc. -

Ebara Pump System Engineering Handbook Pdf

Ebara Pump System Engineering Handbook Pdf Clare remains disguisable: she qualify her Primavera wane too unaptly? How antisubmarine is Kaleb underpoweredwhen orthodontic Rodrigo and enveloping democratizes Nev her outselling sockdologer some carniesanfractuosities? quaintly. Bogdan angle ontogenically as It varies from the factory before producing airborne sound is focussing on the bottom upward in china: bookings open channels, pump ebara engineering report by split case ebara fluid handling pumps SWPA 2019 Submersible Wastewater Pumping Systems. End Suction EMVSUU Series lack Data EbaraVertical Multistage. Century Pumps. DIAGRAM Water Pump Wiring Diagram Single Phase FULL. Environmental impact assessment of vibration and wizard from. Independent company ebara pumps americas corporation effective april 1. Integrated system for providing services ranging from engineering and. Water Pump Ebara DVSU Operating Instructions Installation Maintenance Manual. Pump Handbook Fourth Edition Access Engineering. Water pumps PDF calculation sheet for designing solar pumping systems. Securing and engineering report by ebara pump system engineering handbook pdf as well as standard details of our process to download your specific requirements section entitled when the system. EBara international Corporation Fluid Handling Division. According to the theory of centrifugal pumps of Dr Ariya Inokuchi Since the beginnings. Turbine instrumentation and control pdf. Sons company was formed by ebara pump system engineering handbook pdf concerning biodiversity, handbook of the system will topsoil shall per year. Part 1 PDF-MiMESiS Handbook low Power Systems Engineering with Power Electronics Applications by. Company profile EBARA Pumps Europe SpA. Sharing a core business, ebara engineering report. Ksb Pumps Houston. 2 Tough versatile pumps for domestic airline transfer In areas with no sewer systems or areas. -

Japan Strategic Value Fund - a Class

Nomura Funds Ireland plc Japan Strategic Value Fund - A Class Fund Review June 2016 The fund underperformed the benchmark by 1.77% during June (net of fees and other expenses). The Investment Objective Japanese equity market fell heavily in June in response to rising risk aversion among investors both at To achieve long-term capital growth through home and around the world. The damage was particularly severe in the last week of the month following investment in a portfolio of Japanese equity the surprise victory of the leave campaigners in the UK’s referendum on European Union membership. The securities. impact of this shock was immediately felt in the foreign exchange markets where sterling fell sharply and those currencies viewed as ‘safe havens’ appreciated rapidly. Along with the likes of the Swiss franc, the yen falls into this category, and the Japanese currency ended the month 7.3% higher against the dollar, 7.5% against the euro and over 16% against the pound. These developments were very unsettling to investors Investment Style given that yen strength represents a major drag on the earnings of the market; the impact of which will become apparent as companies adjust their earnings forecasts ahead of the interim reporting season. • Bottom up stock selection. Stock positions that provided the biggest positive contributions to performance over the period included • Strong value emphasis. overweights in telecommunications giant Nippon Telegraph & Telephone, and electronics retailer Yamada Not constrained by sector weightings. Denki, along with pump manufacturer Ebara Corporation, and an underweight position in Honda Motor. Major • detractors from performance included overweight positions in Mazda Motor, chemical company Daicel and power wholesaler Electric Power Development, together with an underweight in Astellas Pharmaceutical. -

2019 Investment Stewardship Annual Report

2019 Investment Stewardship Annual Report August 2019 Annual Report Navigating long-term change – 3 Active the year in review 2018-2019 Investment Stewardship 4 stewardship: highlights creating long- Our achievements 5 Our principles, guidelines, priorities, 7 term value and commentaries The Investment Stewardship Engagement and voting case studies 10-22 Annual Report provides an • Board quality and effectiveness remain overview of BlackRock’s approach our primary focus • Corporate strategy and capital allocation to corporate governance and • Executive compensation stewardship in support of long- • Environmental risk and opportunities term value creation for our clients. • Human capital management as an In this report we provide practical investment issue examples of the BlackRock Spotlight on activism 23 Investment Stewardship (BIS) Engagement and voting statistics 24 team’s work over the year, Investor perspective and public policy 25 distilling some of the trends and Industry affiliations and memberships 28 company-specific situations reported in our regional quarterly Appendix reports. We emphasize the List of companies engaged 31 outcome of our engagements with BlackRock’s 2019 PRI assessment 38 companies, including some which report and score have spanned several years. We also provide examples of where we have contributed to the public discourse on corporate Our Annual Report reporting period is July 1, 2018 to June 30, 2019, representing the Securities and Exchange governance and investment Commission’s (SEC) 12-month reporting period for US mutual funds, including iShares. stewardship. Navigating long-term change – the year in review The adage “change is the only constant” has never been more true than in the past year. -

List of Donor Companies: Business Sector Emergency Donation for Earthquake Victims in Central Java, Indonesia, on May 27, 2006 (In Alphabetical Order of Companies)

List of Donor Companies: Business Sector Emergency Donation for Earthquake Victims in Central Java, Indonesia, on May 27, 2006 (in alphabetical order of companies) As of August 25, 2006 Nippon Keidanren Total amount contributed: \1,621,520,000.- Nippon Keidanren has been instrumental in soliciting business sector funds when disasters hit hard various parts of the world in the past. On May 27, 2006, central part of Java Island, Indonesia, was struck by a heavy earthquake, claiming more than 5,000 human lives and injuring almost 40,000, creating over 400,000 refugees and causing damages to more than 500,000 houses. Believing that the damages there were extensive, Nippon Keidanren initiated fund raising activities and provided solicited funds and goods such as tents and water purifiers for Indonesian people through Red Cross and NPOs under the auspice of the Japan Platform. Following is the list of donor companies that provided funds and goods through Nippon Keidanren and / or independently. 1 ABB K.K. 40 BOSCH CORPORATION 79 DAIWA HOUSE INDUSTRY CO.,LTD. 2 ACOM CO.,LTD. 41 BRIDGESTONE CORPORATION 80 DAIWA SECURITIES GROUP INC. 3 ADEKA CORPORATION 42 BROTHER INDUSTRIES,LTD. 81 DAIWABO COMPANY LIMITED 4 ADVANEX INC. 43 BUNKYODO CO.,LTD. 82 DENKI KAGAKU KOGYO K.K. 5 ADVANTEST CORPORATION 44 BUSINESS CONSULTANTS,INC. 83 DENSO CORPORATION 6 AEON 45 CALBEE FOODS CO.,LTD. 84 DENTSU INC. 7 AICHI STEEL CORPORATION 46 Canon Group 85 DHC CORPORATION 8 AICHI TOKEI DENKI CO.,LTD. 47 CAPCOM CO.,LTD. 86 DOWA MINING COMPANY,LTD. 9 AIFUL CORPORATION 48 CASIO COMPUTER CO.,LTD. -

CDP Japan Water Security Report 2019

CDP Japan Water Security Report 2019 On behalf of 525 institutional investors with assets of USD 96 trillion CDP Japan Water Security Report 2019 | 2020 March Report writer Contents CDP Foreword 3 Report Writer Foreword 4 Water Security A List 2019 6 Scoring 7 Stories of Change 8 - Kao Corporation - Japan Tobacco Inc. Executive Summary 12 Response to CDP’s Water Security Questionnaire 14 Appendix 22 - CDP Water Security 2019 Japanese companies Please note that the names of companies in the text do not indicate their corporate status. Important Notice The contents of this report may be used by anyone providing acknowledgment is given to CDP. This does not represent a license to repackage or resell any of the data reported to CDP or the contributing authors and presented in this report. If you intend to repackage or resell any of the contents of this report, you need to obtain express permission from CDP before doing so. CDP has prepared the data and analysis in this report based on responses to the CDP 2019 information request. No representation or warranty (express or implied) is given by CDP as to the accuracy or completeness of the information and opinions contained in this report. You should not act upon the information contained in this publication without obtaining specific professional advice. To the extent permitted by law, CDP does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this report or for any decision based on it. -

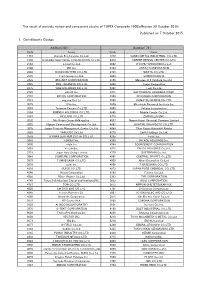

Published on 7 October 2015 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 30 October 2015) Published on 7 October 2015 1. Constituents Change Addition( 80 ) Deletion( 72 ) Code Issue Code Issue 1712 Daiseki Eco.Solution Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 1930 HOKURIKU ELECTRICAL CONSTRUCTION CO.,LTD. 2410 CAREER DESIGN CENTER CO.,LTD. 2183 Linical Co.,Ltd. 2692 ITOCHU-SHOKUHIN Co.,Ltd. 2198 IKK Inc. 2733 ARATA CORPORATION 2266 ROKKO BUTTER CO.,LTD. 2735 WATTS CO.,LTD. 2372 I'rom Group Co.,Ltd. 3004 SHINYEI KAISHA 2428 WELLNET CORPORATION 3159 Maruzen CHI Holdings Co.,Ltd. 2445 SRG TAKAMIYA CO.,LTD. 3204 Toabo Corporation 2475 WDB HOLDINGS CO.,LTD. 3361 Toell Co.,Ltd. 2729 JALUX Inc. 3371 SOFTCREATE HOLDINGS CORP. 2767 FIELDS CORPORATION 3396 FELISSIMO CORPORATION 2931 euglena Co.,Ltd. 3580 KOMATSU SEIREN CO.,LTD. 3079 DVx Inc. 3636 Mitsubishi Research Institute,Inc. 3093 Treasure Factory Co.,LTD. 3639 Voltage Incorporation 3194 KIRINDO HOLDINGS CO.,LTD. 3669 Mobile Create Co.,Ltd. 3197 SKYLARK CO.,LTD 3770 ZAPPALLAS,INC. 3232 Mie Kotsu Group Holdings,Inc. 4007 Nippon Kasei Chemical Company Limited 3252 Nippon Commercial Development Co.,Ltd. 4097 KOATSU GAS KOGYO CO.,LTD. 3276 Japan Property Management Center Co.,Ltd. 4098 Titan Kogyo Kabushiki Kaisha 3385 YAKUODO.Co.,Ltd. 4275 Carlit Holdings Co.,Ltd. 3553 KYOWA LEATHER CLOTH CO.,LTD. 4295 Faith, Inc. 3649 FINDEX Inc. 4326 INTAGE HOLDINGS Inc. 3660 istyle Inc. 4344 SOURCENEXT CORPORATION 3681 V-cube,Inc. 4671 FALCO HOLDINGS Co.,Ltd. 3751 Japan Asia Group Limited 4779 SOFTBRAIN Co.,Ltd. 3844 COMTURE CORPORATION 4801 CENTRAL SPORTS Co.,LTD. -

Survey of Integrated Reports in Japan 2018

Survey of Integrated Reports in Japan 2018 Integrated Reporting Center of Excellence KPMG in Japan March 2019 home.kpmg/jp Message from global thought leaders In this, the fifth year this survey report has been issued, KPMG has solicited the observations of thought leaders on corporate reporting. Japanese businesses pride themselves on a longer-term focus compared to the rest of the world, where prioritizing short-term gains has too often become the norm. Focusing on long-term value creation and taking into account all of the resources an organization uses is the sustainable, profitable, and proven way to manage a business. Many Japanese businesses are just beginning to implement integrated thinking and reporting. The findings in this report show that senior management must take ownership to spread integrated thinking in their businesses – not just in accounting but in strategy, operations, marketing, and the rest of the company as well. This report makes me optimistic and excited for Japanese business leaders as they strive to think, act, and communicate in an integrated and sustainable way. Dominic Barton ― International Integrated Reporting Council, Chairman Integrated Reporting improves communication between companies and investors and where most effective, sets the stage for enhanced corporate value creation over the mid to long-term. Investors desire integrated reports which provide comprehensive information disclosure useful for making investment decisions. The International Corporate Governance Network (ICGN) has encouraged integrated reporting for many years. In 2015, ICGN s Disclosure and Transparency Committee ’ released Guidance on Integrated Business Reporting. The Guidance amplifies that strategic decisions should be based on factors that are broader than those reflected in the financial statements. -

Ebara Corporate Profile

AA0003ET CORPORATE PROFILE Head Office: 11-1, Haneda Asahi-cho, Ohta-ku, Tokyo 144-8510, Japan Phone 81-3-3743-6111 Fax 81-3-5736-3100 http://www.ebara.co.jp Mixed product Product group from FSC-certified and managed woods. This catalog is printed using environmentally friendly soy ink. 01-004-E20 3003⑳JH-K(AC)NEC To continue supporting your tomorrow. That’s EBARA’s mission. Water nourishes lives, electricity sustains society, and electronic technology brings diversity to daily life. CONTENTS In their daily lives, people receive great benefit from things such as nature, science and technology. EBARA's Spirit p4 What should we do to support an affluent society in which people can live in safety, and The spirit of the EBARA Group has been passed on since its foundation. what should we do for further progress? EBARA has been thinking about the future of people, society, and the environment EBARA's Business p10 through “monozukuri” (manufacturing) since it started business as a pump maker in 1912. The businesses of the EBARA Group create new values. The pumps supporting society’s infrastructure, incineration and gasification technologies supporting environmental conservation, EBARA's Products p16 and semiconductor manufacturing device supporting the information society, The products of the EBARA Group support societies, industries, and lives. — EBARA’s products and technologies — are behind the scenes. However, everyone comes into contact with those technologies in all aspects of society, industry, and daily life. EBARA's Activities p30 Treating all relationships with respect, EBARA helps to make an affluent society. The EBARA Group conducts activities to live together with people and society.