Criteria for Dutch and Belgian Supermarket Chains for Potato

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Sustainable Journey of Retailer Brands

MARCA BY BOLOGNA FIERE 2020 THE SUSTAINABLE JOURNEY OF RETAILER BRANDS ITALY, Bologna | January 16th, 2020 THE SUSTAINABLE JOURNEY OF RETAILER BRANDS THE DUTCH CASE KOEN DE JONG THE UNITED STATES CASE THE FRENCH CASE THE DUTCH MARKET Retailer market shares - 2019 21.0% Coop 3.7 Deen 2.1 -0,1 % Dirk 3.7 Dekamarkt 1.7 -0,1 % Hoogvliet-0,4 % 2.1 Jan Linders 1.1 35.7% +0,2 % 25.8% Plus 6.4 = Poisz 1.0 -0,3 % Spar 1.2 + 0,3 % = others 3.7 0 1.8 3.5 5.3 7 10.7% 6.8% Sources: Nielsen/Distrifood/RABO/IPLC 2019 THE DUTCH MARKET Retailer market shares - 2019 21.0% Coop 3.7 Deen 2.1 -0,1 % Dirk 3.7 Dekamarkt 1.7 -0,1 % Hoogvliet-0,4 % 2.1 Jan Linders 1.1 35.7% +0,2 % 25.8% Plus 6.4 = Poisz 1.0 -0,3 % Spar 1.2 + 0,3 % = others 3.7 0 1.8 3.5 5.3 7 10.7% 6.8% Estimate private Label value share: 43% (including Aldi and Lidl) Turnover €38,3bn Sources: Nielsen/Distrifood/RABO/IPLC 2019 THE RETAILER BRAND IN THE NETHERLANDS Further consolidation of retail landscape ▸ Amazing growth of Jumbo: 4.9% to 21% market share in past 10 years ▸ Market share retailer brands: 27,3% (including discounters: 43%) ▸ Retail consolidation has intensified competition ▸ Professional players place private label and sustainability central in their strategy THE ALBERT HEIJN CASE Why addresssing sustainability is important Store image perception Retail brand Shopper loyalty Retail brand Retail brand choice quality perception purchase intention to the store Retail brand price perception Source: Price premium for food brands, Journal of Product & Brand Management, 2014 THE ALBERT -

Global Vs. Local-The Hungarian Retail Wars

Journal of Business and Retail Management Research (JBRMR) October 2015 Global Vs. Local-The Hungarian Retail Wars Charles S. Mayer Reza M. Bakhshandeh Central European University, Budapest, Hungary Key Words MNE’s, SME’s, Hungary, FMCG Retailing, Cooperatives, Rivalry Abstract In this paper we explore the impact of the ivasion of large global retailers into the Hungarian FMCG space. As well as giving the historical evolution of the market, we also show a recipe on how the local SME’s can cope with the foreign competition. “If you can’t beat them, at least emulate them well.” 1. Introduction Our research started with a casual observation. There seemed to be too many FMCG (Fast Moving Consumer Goods) stores in Hungary, compared to the population size, and the purchasing power. What was the reason for this proliferation, and what outcomes could be expected from it? Would the winners necessarily be the MNE’s, and the losers the local SME’S? These were the questions that focused our research for this paper. With the opening of the CEE to the West, large multinational retailers moved quickly into the region. This was particularly true for the extended food retailing sector (FMCG’s). Hungary, being very central, and having had good economic relations with the West in the past, was one of the more attractive markets to enter. We will follow the entry of one such multinational, Delhaize (Match), in detail. At the same time, we will note how two independent local chains, CBA and COOP were able to respond to the threat of the invasion of the multinationals. -

Trade for Development Centre - BTC (Belgian Development Agency)

Trade for Development Centre - BTC (Belgian Development Agency) 1 Trade for Development Centre - BTC (Belgian Development Agency) Author: Facts Figures Future, http://www.3xf.nl Managing Editor: Carl Michiels © BTC, Belgian Development Agency, 2011. All rights reserved. The content of this publication may be reproduced after permission has been obtained from BTC and provided that the source is acknowledged. This publication of the Trade for Development Centre does not necessarily represent the views of BTC. Photo courtesy: © iStockphoto/Mediaphotos Cover: © CTB Josiane Droeghag 2 Trade for Development Centre - BTC (Belgian Development Agency) ......................................................................................................................................... 3 ............................................................................................................................ 4 .................................................................................................................... 5 1.1 Consumption .................................................................................................................... 5 1.2 Imports .............................................................................................................................. 5 1.3 Supplying markets ........................................................................................................... 5 1.4 Exports ............................................................................................................................. -

Datecdec Situation Du Projet Projet Decis Cdec Recours

'$7(&'(& 6,78$7,21 352-(7 '(&,6 5(&2856 '$7(&1(& '(&,6 &1(& '8352-(7 &'(& Extension de 3200 m² la surface de vente du magasin BRIE COMTE ROBERT – ZAC du LEROY MERLIN à BRIE COMTE ROBERT Tuboeuf -ZAC du Tuboeuf, rue de la Butte au Berger- selon la DXWRULVDWLRQ répartition suivante : PðH[WpULHXUV (par le libre accès de la clientèle dans la cour de matériaux agrandie de 323 m²) et PðSRXUOHPDJDVLQ (la surface couverte passera de 5800 m² à 6200 m², la surface extérieure sera de 2800 m² , la surface de show room de 195 m² est inchangée ) La surface de vente globale passera donc de 5995 à 9195 m² (SA LEROY MERLIN France) PROVINS , 15-17 avenue du Extension de 651 m² la surface de vente du magasin Maréchal de Lattre de Tassigny INTERMARCHE (2499 m² après extension) DXWRULVDWLRQ (SA PROVINS DISTRIBUTION (PRODIS) ) PROVINS -3, avenue de la Voulzie Extension de de 300 m² la surface de vente (1000 m² (partie de l’ex local BUT) après extension) du magasin d’équipement de la personne à l’enseigne DEFI MODE DXWRULVDWLRQ (SA JMP EXPANSION) MAREUIL LES MEAUX, lieudit Création d’un ensemble de trois magasins d’une surface de la Hayette, 79, rue des Montaubans vente totale de 1880 m² comprenant un magasin à (ancien site JARDILAND) l’enseigne MAXI TOYS (jeux et jouets) de 800 m², un DXWRULVDWLRQ magasin à l’enseigne AUBERT (puériculture et layette) de 550 m² et un magasin à l’enseigne CASA (arts de la table et décoration) de 530 m² (Sarl PAGESTIM) '$7(&'(& 6,78$7,21 352-(7 '(&,6 5(&2856 '$7(&1(& '(&,6 &1(& '8352-(7 &'(& extension de 290 m² la surface de vente (1440 m² après DAMMARIE LES LYS extension) du magasin de meubles FLY –Rue A. -

Producer/Retailer Contractual Relationships in the Fishing Sector : Food Quality, Procurement and Prices Stéphane Gouin, Erwan Charles, Jean-Pierre Boude

Producer/retailer Contractual Relationships in the fishing sector : food quality, procurement and prices Stéphane Gouin, Erwan Charles, Jean-Pierre Boude, . European Association of Fisheries Economists To cite this version: Stéphane Gouin, Erwan Charles, Jean-Pierre Boude, . European Association of Fisheries Economists. Producer/retailer Contractual Relationships in the fishing sector : food quality, procurement and prices. 16th Annual Conference of the European Association of Fisheries Economists, European Association of Fisheries Economists (EAFE). FRA., Apr 2004, Roma, Italy. 15 p. hal-02311416 HAL Id: hal-02311416 https://hal.archives-ouvertes.fr/hal-02311416 Submitted on 7 Jun 2020 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. Distributed under a Creative Commons Attribution - NonCommercial - NoDerivatives| 4.0 International License t XVIth Annual EAFE Conference, Roma, April 5-7th 2004 I EAFE, Romu, April 5-7th 2004 Producer/retailer Contractual Relationships in the fTshing sector : food quality, procurement and prices Gouin 5., Charles 8., Boude fP. Agrocampus Rennes Département d'Economie Rurale et Gestion 65, rue de Saint Brieuc CS 84215 F 35042 Rennes cedex gouin@agrocampus-rennes. fr boude@agrocampus-rennes. fr and *CEDEM Université de Bretagne Occidentale 12, rue de Kergoat BP 816 29285 Brest cedex erwan. -

Healthier, Tastier Food

HEALTHIER, TASTIER FOOD. NB: FOR OPTIMUM NAVIGATION, PLEASE DOWNLOAD AND VIEW THIS PDF IN ADOBE ACROBAT. ANNUAL REPORT 2021 CONTENTS STRATEGIC REPORT 2 Our purpose Our business today 10 At a glance 12 Chair’s statement 14 Chief Executive’s review 20 Our world 22 Our business model 24 Our strategy 26 Key performance indicators Review of the year 32 Food & Beverage Solutions 36 Primary Products 40 Innovation and Commercial Development 42 Global Operations 44 Chief Financial Officer’s introduction 46 Group financial review 50 Our people 53 Equity, diversity and inclusion 54 Community involvement 56 Environment, health and safety 66 Task Force on Climate-related Financial Disclosures 68 Risk Report GOVERNANCE 80 Board of Directors 84 Executive Committee 86 Corporate governance 101 Nominations Committee Report 104 Audit Committee Report 110 Directors’ Remuneration Report 129 Directors’ Report 131 Directors’ statement of responsibilities FINANCIAL STATEMENTS 134 Independent Auditor’s Report to the members of Tate & Lyle PLC 142 Consolidated income statement 143 Consolidated statement of comprehensive income 144 Consolidated statement of financial position 145 Consolidated statement of cash flows 146 Consolidated statement of changes in equity Tate & Lyle is a global 147 Notes to the consolidated financial statements provider of ingredients 194 Parent Company financial statements and solutions for the USEFUL INFORMATION 202 Group five-year summary 204 Additional information food, beverage and 205 Information for investors 207 Glossary industrial markets. 208 Definitions/explanatory notes DOWNLOAD THE FULL ANNUAL REPORT 2021 Download at www.tateandlyle.com STRATEGIC REPORT NB: FOR OPTIMUM NAVIGATION, PLEASE DOWNLOAD AND VIEW THIS PDF IN ADOBE ACROBAT. -

Romania: Retail Food Sector

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 2/6/2017 GAIN Report Number: RO1703 Romania Post: Bucharest Retail Food Sector Report Categories: Retail Foods Approved By: Russ Nicely Prepared By: Ioana Stoenescu Report Highlights: Over the last three years, Romania has seen strong positive growth, with encouraging developments in the economic and policy areas, becoming one of the most attractive markets in Southeastern Europe. After just a few notable events during 2015, the Romanian retail market experienced remarkable growth in 2016 reaching 2,000 stores operated by international retailers. As modern retail systems grow, exports of U.S. processed and high value foods to Romania will continue to expand. In 2015 U.S. agri- food exports to Romania increased by 45 percent from U.S. $96 million to U.S. $139 million over the last year. Romania's food sector is expected to be among the regional best performers during the next five years, with promising market prospects for U.S. exporters such as tree nuts, distilled spirits and wines. General Information: I. MARKET SUMMARY General Information Romania has been a member of the EU since 2007 and a member of NATO since 2004. Within the 28 EU countries, Romania has the seventh largest population, with 19.5 million inhabitants. Romania is presently a market with outstanding potential, a strategic location, and an increasingly solid business climate. Although there is the need for an exporter to evaluate the market in order to assess the business opportunities, exporting to Romania is steadily becoming less challenging than in previous years in terms of the predictability of the business environment. -

More Sustainable Food

MORE SUSTAINABLE FOOD: FRUIT AND VEGETABLES AT THE SUPERMARKET Consumers, JULY 2018 Consumers Association More sustainable food: fruit and vegetables at the supermarket 1 CONTENT Resume 4 preface 6 1 study Design 7 1.1 Research questions 7 1.2 Definition / scope 8 1.2.1 Selection supermarkets 8 1.2.2 Selection of case studies 8 1.2.3 Scope of the study 9 1.2.4 Definition and explanation term sustainable 10 1.3 Research Methods 10 1.3.1 Research supermarket policy 10 1.3.2 Consumer research 12 1.3.3 Research case studies 12 2 Results 13 2.1 Sustainability initiatives fruits and vegetables incl. Marks 13 2.1.1 Sustainability labels fruit and vegetables 13 2.1.2 Sustainability Initiatives fruit and vegetables 17 2.1.3 Sustainability Themes 18 2.1.4 International perspective 22 2.2 Supermarket Policy sustainability fruit and vegetables 25 2.2.1 Purchasing Organization Fruit & Vegetables 25 2.2.2 Sustainability generally Fruit & Vegetables 27 2.2.3 Environment: Ambition & Policy and Implementation & monitoring 32 2.2.4 Social: Ambition & Policy and Implementation & monitoring 40 2.2.5 Training & Support 47 2.2.6 Seasonal Products 49 2.2.7 Food waste 50 2.2.8 Final questions: challenges and responsibilities of supermarkets 54 2.2.9 Summary of results by supermarket chain 55 2.3 consumer research 57 2.3.1 The concept of sustainability 57 2.3.2 Purchase of vegetables and fruits 58 2.3.3 Consumers sustainability in fruit and vegetables 59 2.4 Results of case studies 61 2.4.1 Strawberry 63 2.4.2 Banana 72 2.4.3 Paprika 82 2.4.4 Green Bean 89 Consumers -

Social Media Use by Dutch Supermarket Chains

Social media use by Dutch supermarket chains A digital marketing analysis on brand loyalty Thomas Dijkman 11026057 August 21st, 2018 Supervisor: Dick Heinhuis 2nd Examiner: Tom van Engers Bachelor thesis Information Science Faculty of Science University of Amsterdam ABSTRACT Social media have grown from being entertaining communication platforms into powerful business tools for marketing, promotion and customer service. Consequently, businesses have had to make changes in their marketing strategies to take advantage of the opportunities created by this new social ecosystem. Brand loyalty, which is one of the main goals of marketing efforts, is influenced by social media through different factors like trust and feelings of community. This thesis assesses the efforts made by Dutch supermarket chains on social media to test the effect of social media on their perceived brand loyalty. The factors that stimulate brand loyalty that were found in an extensive literature review were challenged through field research to test their effect on Dutch supermarket brands. The findings of this research show that there is no significant effect of social media efforts on brand loyalty in the case of Dutch supermarket chains. On the contrary, present research confirms that there are unexplored opportunities for Dutch supermarket chains to use social media to increase brand loyalty. From these findings, a general discussion and conclusion are offered, as well as directions for further research. 2 Table of contents 1 Introduction………………………………………………………………………………………………………… 5 1.1 Research objectives……………………………………………………………………………………… 6 1.2 Relevance……………………………………………………………………………………………………. 6 1.2.1 Academic relevance………………………………………………………………………………. 6 1.2.2 Managerial relevance…………………………………………………………………………….. 7 1.3 Research question and subquestions………………………………………………………………. 8 1.4 The Dutch supermarket industry……………………………………………………………………. -

Retail Food Sector Retail Foods France

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 9/13/2012 GAIN Report Number: FR9608 France Retail Foods Retail Food Sector Approved By: Lashonda McLeod Agricultural Attaché Prepared By: Laurent J. Journo Ag Marketing Specialist Report Highlights: In 2011, consumers spent approximately 13 percent of their budget on food and beverage purchases. Approximately 70 percent of household food purchases were made in hyper/supermarkets, and hard discounters. As a result of the economic situation in France, consumers are now paying more attention to prices. This situation is likely to continue in 2012 and 2013. Post: Paris Author Defined: Average exchange rate used in this report, unless otherwise specified: Calendar Year 2009: US Dollar 1 = 0.72 Euros Calendar Year 2010: US Dollar 1 = 0.75 Euros Calendar Year 2011: US Dollar 1 = 0.72 Euros (Source: The Federal Bank of New York and/or the International Monetary Fund) SECTION I. MARKET SUMMARY France’s retail distribution network is diverse and sophisticated. The food retail sector is generally comprised of six types of establishments: hypermarkets, supermarkets, hard discounters, convenience, gourmet centers in department stores, and traditional outlets. (See definition Section C of this report). In 2011, sales within the first five categories represented 75 percent of the country’s retail food market, and traditional outlets, which include neighborhood and specialized food stores, represented 25 percent of the market. In 2011, the overall retail food sales in France were valued at $323.6 billion, a 3 percent increase over 2010, due to price increases. -

DEMO Competitive Analysis Retail

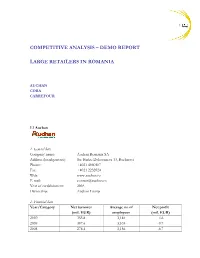

COMPETITIVE ANALYSIS – DEMO REPORT LARGE RETAILERS IN ROMANIA AUCHAN CORA CARREFOUR 1.1 Auchan 1. General data Company name: Auchan Romania SA Address (headquarters): Str. Barbu Delavrancea 13, Bucharest Phone: +4021 4080107 Fax: +4021 2232024 Web: www.auchan.ro E-mail: [email protected] Year of establishment: 2005 Ownership: Auchan Group 2. Financial data Year/Category Net turnover Average no of Net profit (mil. EUR) employees (mil. EUR) 2010 355.8 3,184 -4.6 2009 307.6 3,103 -9.7 2008 278.4 3,156 -6.7 A FRD Center Market Entry Services Demo Publication www.market-entry.ro 3. Key persons Name Position Contact details Mr. Patrick Espasa General Director Email: [email protected] Mr. Tiberiu Danetiu Marketing Director Email: [email protected] Ms. Mariana Dragan Communication Manager Email: [email protected] Tel: +4 021 4080294 4. Brief profile Auchan Romania is part of the French Group Auchan. Auchan opened its first hypermarket on the Romanian market in 2006. This store is located in Bucharest (in the Titan area) and has the surface of over 16,000 sqm. The store records a daily traffic of 30,000 – 45,000 persons and registers the biggest sales in the Auchan network in Romania. At present, Auchan has nine hypermarkets in Romania, located in Bucharest (two stores – in the Titan and Militari areas), Pitesti, Targu Mures, Cluj Napoca, Suceava, Timisoara, Constanta and Craiova. The Auchan hypermarket in Cluj Napoca was opened in November 2007, with an investment of 40 million EUR. The store is located in the Iulius Mall, has the surface of some 10,000 sqm and offers over 45,000 products. -

Nederlanders & Fairtrade 2013

Het kopen van fairtrade levensmiddelen kan gezien worden als een invulling van mondiaal burgerschap en als een uiting van betrokkenheid bij de wereld en bij internationale samenwerking. Daarom onderzoekt NCDO sinds 2007 jaarlijks het aankoopgedrag van fairtrade levensmiddelen in Nederland. Dit rapport beschrijft het daadwerkelijke fairtrade aankoopgedrag van Nederlanders in 2013, de achtergronden van de kopers en trends daarin. 2013 NEDERLANDERS & FAIRTRADE Hoeveel huishoudens in Nederland kochten in 2013 fairtrade levensmid- delen? Welke fairtrade levensmiddelen werden vooral gekocht? Wie zijn de voornaamste kopers van fairtrade levensmiddelen? En waar worden fairtrade levensmiddelen gekocht? Deze vragen worden in deze publicatie beantwoord. Deze publicatie is onderdeel van een nieuwe reeks onderzoekspublicaties van NCDO, die met onderzoek, trainingen en andere activiteiten het publiek bewustzijn over internationale samenwerking en het belang van Nederland om op dit terrein actief te zijn bevordert. NEDERLANDERS & FAIRTRADE 2013 ONDERZOEK NAAR AANKOOPGEDRAG BIJ FAIRTRADE LEVENSMIDDELEN ONDERZOEKSREEKS 22 Dit kennisdossier is een uitgave van NCDO, mei 2014 1 ONDERZOEKSREEKS 22 - NEDERLANDERS & FAIRTRADE 2013 NCDO is het Nederlandse kennis- en adviescentrum voor burgerschap en internationale samenwerking. NCDO voert onderzoek uit, geeft trainingen en stimuleert de meningsvorming over mondiale thema’s door publicaties te verzorgen en de discussie op gang te brengen. NCDO werkt daarbij samen met overheid en politiek, maatschappelijke organisaties, bedrijfsleven en wetenschap. Heeft u vragen of opmerkingen over dit onderzoek of wilt u op de hoogte worden gehouden van nieuw onderzoek, neem dan contact op met NCDO via [email protected]. Foto omslag: Werry Crone/Hollandse Hoogte ISBN: 978-90-74612-54-8 Amsterdam, mei 2014 NCDO is het centrum voor mondiaal burgerschap.