Review of the Bhiwandi Model

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Estate 5 BHK Brochure

4 & 5 BHK LUXURY HOMES Hiranandani Estate, Thane Hiranandani Estate, Off Ghodbunder Road, Thane (W) Call:(+91 22) 2586 6000 / 2545 8001 / 2545 8760 / 2545 8761 Corp. Off.: Olympia, Central Avenue, Hiranandani Business Park, Powai, Mumbai - 400 076. [email protected] • www.hiranandani.com Rodas Enclave-Leona, Royce-4 BHK & Basilius-5 BHK are mortgaged with HDFC Ltd. The No Objection Certificate (NOC)/permission of the mortgagee Bank would be provided for sale of flats/units/property, if required. Welcome to the Premium Hiranandani Living! ABUNDANTLY YOURS Standard apartment of Basilius building for reference purpose only. The furniture & fixtures shown in the above flat are not part of apartment amenities. EXTRAVAGANTLY, oering style with a rich sense of prestige, quality and opulence, heightened by the cascades of natural light and spacious living. Actual image shot at Rodas Enclave, Thane. LUXURIOUSLY, navigating the chasm between classic and contemporary design to complete the elaborated living. • Marble flooring in living, dining and bedrooms • Double glazed windows • French windows in living room • Large deck in living/dining with sliding balcony doors Standard apartment of Basilius building for reference purpose only. The furniture & fixtures shown in the above flat are not part of apartment amenities. CLASSICALLY, veering towards the modern and eclectic. Standard apartment of Basilius building for reference purpose only. The furniture & fixtures shown in the above flat are not part of apartment amenities. EXCLUSIVELY, meant for the discerning few! Here’s an access to gold class living that has been tastefully designed and thoughtfully serviced, oering only and only a ‘royal treatment’. • Air-conditioner in living, dining and bedrooms • Belgian wood laminate flooring in common bedroom • Space for walk–in wardrobe in apartments • Back up for selected light points in each flat Standard apartment of Basilius building for reference purpose only. -

Reg. No Name in Full Residential Address Gender Contact No

Reg. No Name in Full Residential Address Gender Contact No. Email id Remarks 20001 MUDKONDWAR SHRUTIKA HOSPITAL, TAHSIL Male 9420020369 [email protected] RENEWAL UP TO 26/04/2018 PRASHANT NAMDEORAO OFFICE ROAD, AT/P/TAL- GEORAI, 431127 BEED Maharashtra 20002 RADHIKA BABURAJ FLAT NO.10-E, ABAD MAINE Female 9886745848 / [email protected] RENEWAL UP TO 26/04/2018 PLAZA OPP.CMFRI, MARINE 8281300696 DRIVE, KOCHI, KERALA 682018 Kerela 20003 KULKARNI VAISHALI HARISH CHANDRA RESEARCH Female 0532 2274022 / [email protected] RENEWAL UP TO 26/04/2018 MADHUKAR INSTITUTE, CHHATNAG ROAD, 8874709114 JHUSI, ALLAHABAD 211019 ALLAHABAD Uttar Pradesh 20004 BICHU VAISHALI 6, KOLABA HOUSE, BPT OFFICENT Female 022 22182011 / NOT RENEW SHRIRANG QUARTERS, DUMYANE RD., 9819791683 COLABA 400005 MUMBAI Maharashtra 20005 DOSHI DOLLY MAHENDRA 7-A, PUTLIBAI BHAVAN, ZAVER Female 9892399719 [email protected] RENEWAL UP TO 26/04/2018 ROAD, MULUND (W) 400080 MUMBAI Maharashtra 20006 PRABHU SAYALI GAJANAN F1,CHINTAMANI PLAZA, KUDAL Female 02362 223223 / [email protected] RENEWAL UP TO 26/04/2018 OPP POLICE STATION,MAIN ROAD 9422434365 KUDAL 416520 SINDHUDURG Maharashtra 20007 RUKADIKAR WAHEEDA 385/B, ALISHAN BUILDING, Female 9890346988 DR.NAUSHAD.INAMDAR@GMA RENEWAL UP TO 26/04/2018 BABASAHEB MHAISAL VES, PANCHIL NAGAR, IL.COM MEHDHE PLOT- 13, MIRAJ 416410 SANGLI Maharashtra 20008 GHORPADE TEJAL A-7 / A-8, SHIVSHAKTI APT., Male 02312650525 / NOT RENEW CHANDRAHAS GIANT HOUSE, SARLAKSHAN 9226377667 PARK KOLHAPUR Maharashtra 20009 JAIN MAMTA -

SR NO First Name Middle Name Last Name Address Pincode Folio

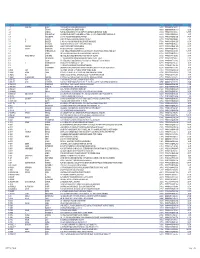

SR NO First Name Middle Name Last Name Address Pincode Folio Amount 1 A SPRAKASH REDDY 25 A D REGIMENT C/O 56 APO AMBALA CANTT 133001 0000IN30047642435822 22.50 2 A THYAGRAJ 19 JAYA CHEDANAGAR CHEMBUR MUMBAI 400089 0000000000VQA0017773 135.00 3 A SRINIVAS FLAT NO 305 BUILDING NO 30 VSNL STAFF QTRS OSHIWARA JOGESHWARI MUMBAI 400102 0000IN30047641828243 1,800.00 4 A PURUSHOTHAM C/O SREE KRISHNA MURTY & SON MEDICAL STORES 9 10 32 D S TEMPLE STREET WARANGAL AP 506002 0000IN30102220028476 90.00 5 A VASUNDHARA 29-19-70 II FLR DORNAKAL ROAD VIJAYAWADA 520002 0000000000VQA0034395 405.00 6 A H SRINIVAS H NO 2-220, NEAR S B H, MADHURANAGAR, KAKINADA, 533004 0000IN30226910944446 112.50 7 A R BASHEER D. NO. 10-24-1038 JUMMA MASJID ROAD, BUNDER MANGALORE 575001 0000000000VQA0032687 135.00 8 A NATARAJAN ANUGRAHA 9 SUBADRAL STREET TRIPLICANE CHENNAI 600005 0000000000VQA0042317 135.00 9 A GAYATHRI BHASKARAAN 48/B16 GIRIAPPA ROAD T NAGAR CHENNAI 600017 0000000000VQA0041978 135.00 10 A VATSALA BHASKARAN 48/B16 GIRIAPPA ROAD T NAGAR CHENNAI 600017 0000000000VQA0041977 135.00 11 A DHEENADAYALAN 14 AND 15 BALASUBRAMANI STREET GAJAVINAYAGA CITY, VENKATAPURAM CHENNAI, TAMILNADU 600053 0000IN30154914678295 1,350.00 12 A AYINAN NO 34 JEEVANANDAM STREET VINAYAKAPURAM AMBATTUR CHENNAI 600053 0000000000VQA0042517 135.00 13 A RAJASHANMUGA SUNDARAM NO 5 THELUNGU STREET ORATHANADU POST AND TK THANJAVUR 614625 0000IN30177414782892 180.00 14 A PALANICHAMY 1 / 28B ANNA COLONY KONAR CHATRAM MALLIYAMPATTU POST TRICHY 620102 0000IN30108022454737 112.50 15 A Vasanthi W/o G -

THE ERA of TRANSCENDENCE Ane-Dombivli a FACT-FILE on the GROWTH of NAVI MUMBAI on the GROWTH of NAVI a FACT-FILE

Redefining Real Estate www.marathonrealty.com THE ERA OF TRANSCENDENCE ane-Dombivli A FACT-FILE ON THE GROWTH OF NAVI MUMBAI ON THE GROWTH OF NAVI A FACT-FILE Corporate Address: 702 Marathon Max, Mulund-Goregaon Link Road, Mulund West, Mumbai - 400080 www.marathonrealty.com Today, nobody fails to mention Thane-Dombivli when the subject of discussion is growth of infrastructure in Mumbai and its peripheries. Belapur, Panvel, Dronagiri and even the areas beyond them are taking rapid strides towards development. It is almost astounding to see this transformation take place. This is a compilation of evidences offering a glimpse into the making of the future. 2 3 2 3 INDEX 01 THANE-DOMBIVLI – REALTY 02 INFRASTRUCTURE Why Kalyan-Dombivli will drive Mumbai’s realty market now ........................................................................................................................................08 Kalyan-Dombivli-Taloja metro under consideration: Devendra Fadnavis .....................................................................................................................20 What is special about Thane real estate ................................................................................................................................................................................11 TMT starts new service from Thane to Dombivli west - Infrastructure ..........................................................................................................................21 Thane: A residential destination in sync with -

Registered Importer of Hazardous Waste (Ferrous / Non Ferrous Metal Waste) Mentioned and Marked ** (Double Star) in Part-B of Sc

Registered Importer of Hazardous Waste (ferrous / Non ferrous Metal Waste) mentioned and marked ** (Double Star) in Part-B of Schedule-III of Hazardous Wastes (Management, Handling & Transboundry Movement) Rules, 2008 Sr. No Name & Address of the Import Material Storage Address Outward No Importer 1 M/s. MTC Business Pvt. S.No: 44 to 47, Ltd, Jawahar Industrial 301-302, Vartex Vikas, Estate, Vill: A-Wing, Kalamboli, Tal: BO/RO(HQ)/HW/Import/ Opp.Railway Station, Steel Scrap Khalapur, Dist: 2009/PA/B- 7563, Andheri (E), Mumbai- Raigad dt: 19/11/2009. 400069 Phone: (022) 26843024/25/26, Fax: (022) 26844681 Iron & Steel Scrap, 2 M/s. Karan Metals, Aluminum Scrap, Godown No: 1, BO/RO(HQ)/HW/Import/ Godown No: 1, Arihant Nickel Scrap, Arihant Compound, 2009/PA/B-7720, Compound, Vill: Val, Copper Scrap, Vill: Val, Anjur Phata, dt: 25/11/2009 Anjur Phata, Bhiwandi, Brass Scrap, Zinc Bhiwandi, Dist: Dist: Thane Dross, Zinc Scrap, Thane Magnesium Scrap & Tin Scrap Steel Scrap, 3 M/s. Linbeck Metal Aluminum Scrap, Survey No: 11/0, BO/RO(HQ)/HW/Import/ Trading (PTY) Ltd, Nickel Scrap, Brass 12/0, 16/2, Vill: 2009/PA/B-7751, Survey No: 11/0, 12/0, Scrap, Zinc, Bhokerpada, Old dt: 27/11/2009 16/2, Vill: Bhokerpada, Molybdenum, Mumbai-Pune Old Mumbai-Pune Vanadium, Cobalt Highway, Near L& T, Highway, Near L& T, Tal: & Titanium Tal: Panvel, Dist: Panvel, Dist: Raigad- Raigad-410206 410206 4 M/s. Sals Shipping Pvt. Khan Compound, BO/RO(HQ)/HW/Import/ Ltd, Khan Compound, Iron & Steel Scrap Opp. Irani Masjid, 2009/PA/B-7809, Opp. -

Of Human Vaccines, Recombinant Products and Veterinary Vaccine Issued from 30/04/2016 to 20/12/2016

Status of Registration Certificate (Form 41) of Human Vaccines, Recombinant Products and Veterinary Vaccine issued from 30/04/2016 to 20/12/2016 S. Firm Name of Formulation Registration No. Certificate No. & Validity HUMAN VACCINE 1. M/s. Prosper Channel Life Science India Pvt. Diphtheria, Tetanus and Acellular Pertussis SVH-16 Ltd.,B-244, Sector- 7, PalamExtn., New Delhi- Combined Vaccine, adsorbed Valid up to 110045, India. 23/06/2019 2. M/s. GlaxoSmithKline Pharmaceuticals Ltd., Measles, Mumps and Rubella Vaccine (live) SVH-7 Dr. Annie Besant Road, Mumbai, India IP in Vial Valid up to 25/12/2019 3. M/s Sanofi Pasteur India Pvt. Ltd.,Sanofi Diphtheria, Tetanus, Pertussis (acellular SV-1 House, CT Survey No. 117-B,L&T Business Component), Hepatitis B (r-DNA), Valid up to Park, Saki Vihar Road,Powai, Mumbai- Poliomyelitis (Inactivated) and Haemophilus 31/12/2017 400072, India. Influenzae type b conjugate vaccine (adsorbed).Suspension for Injection by Intramuscular route.Presentation:Single dose Pre-filled syringe&Single dose vial 4. M/s Sanofi Pasteur India Pvt. Ltd.,Sanofi Diphtheria, Tetanus, Pertussis (acellular SV-5 House, CT Survey No. 117-B,L&T Business Component), Hepatitis B (r-DNA), Valid up to Park, Saki Vihar Road,Powai, Mumbai- Poliomyelitis (Inactivated) and Haemophilus 31/12/2017 400072, India. Influenzae type b conjugate vaccine (adsorbed).Suspension for Injection by Intramuscular route.Presentation:Single dose Pre-filled syringe&Single dose vial 5. M/s Pusan Bioresearch Enterprizes,Unit 007, Rabies Vaccine, Human I.P. (Vero cell), Freeze SV-52 Chamber No. 06, Cabin No. 2, A.A. -

Job Description

JOB DESCRIPTION OPENING FOR: PROGRAM COORDINATOR NAME OF THE PROGRAM: MATERNAL AND NEWBORN HEALTH (MNH) ROLE REPORTS TO: ASSOCIATE PROGRAM DIRECTOR JOB LOCATION: BHIWANDI & ULHASNAGAR ABOUT THE PROGRAM SNEHA’s Maternal and Newborn Health program seeks to improve the quality of delivery of maternal and neonatal health care in urban slums by building an accountable healthcare system as well as to empower communities to be responsible for addressing women’s and newborns’ integrated health needs. THE PROFILE The Program Coordinator will be responsible for the overall planning and implementation of the intervention of the project; assist in the hiring, training and building capacity of team members, effective utilization of teams, monitoring and supervision of delegated work, communication with other contributors within the program for documentation and evaluation inputs. He/she will oversee and monitor collection of data, develop research design and analyse data. Incumbent will be required to liaise and network with partners, funders and stakeholders and continually consider how emerging knowledge can be transformed into policy or developed as a model. He/she will also be required to contribute to organizational level work and events. This position reports to the Associate Program Director and is based in Mumbai. RESPONSIBILITIES Strengthening partnership with different Municipal Corporation officials at various levels through meetings, interactions and continuous follow ups. Preparing plan of implementation with the Stakeholders. Executing and monitoring the project plan Monitoring the work plans and deliverables of program officers on daily basis. Organizing and conducting training programs for various levels of health care providers and ensuring the availability of skill trainers. -

CZMP of Mira Bhayandar Municipal Corporation in 1:25000 Scale

Centre for Earth Science Studies, Thiruvananthapuram CZMP of Mira Bhayandar Municipal Corporation in 1:25000 scale 1. Introduction The preparation of the CZMP for Mira Bhayandar Municipal Corporation has been undertaken as part of the CZMP preparation for the coastal zone of Thane and Sindhudurg districts. The approach and methodology followed are the same for all the Municipal Corporations, Municipal Councils and rural areas in the above districts. The damages to the coastal zone and the impact of coastal hazards to communities and properties, to a certain extent, can be controlled by regulating high impact activities in the coastal zone. It was with this objective the Coastal Regulation Zone (CRZ) Notification (MoEF, 2011; 1991) was introduced in the country. 1. 1 Coastal Zone Management Plans The CRZ provides a spatial planning framework for Coastal Zone Management Plans which provide setbacks around sensitive eco-zones restricting development and other activities close to it. Setbacks require specific reference lines and boundaries for its meaningful implementation. The High Tide Line (HTL) forms the cardinal reference line for determining the setbacks for CRZ. The 100, 200 and 500m CRZ lines landward from the HTL are the landward setback lines. The Low Tide Line (LTL) and the Territorial water boundary (12 NM) form the setback lines towards the sea. The Coastal Zone Management Plans are prepared in 2 scales: 1. CZMP consisting of CRZ maps in 1:25000 scale with Survey of toposheets as base maps 2. CZMP consisting of CRZ maps in 1:4000 scale with cadastral maps as base maps The major work components are: i. -

Containment Zone Boundaries Bhiwandi Nizampur City Municipal Corporation (BNCMC)

Containment Zone Boundaries Bhiwandi Nizampur City Municipal Corporation (BNCMC) Boundries Sr. No. Containment Zones East West North South Current Status Prabhag Samiti No. 1 1 VETAL PADA: NADI NAKA UPHC AREA Safiya Girls School Vanjarpatti Road Balacompound Naigaon Road Inactive 2 AWCHIT PADA: AWCHIT PADA UPHC AREA Ansar Mohalla Road Nasik Road Pentagaon Complex, Chavindra Aampada Road Inactive 3 NAIGAON: GAYATRI NAGAR UPHC AREA Gayatri Nagar Raod Vakil Compund Road Rikshaw Stand Ram Nagar - Baudh Vihar Road Gayatri Nagar Raod Active KIDWAI NAGAR: AWCHIT PADA UPHC 4 Kidwai Nagar Road Gayatri Nagar Road Gausiya Masjid, Shanti Nagar Road Naigaon Active AREA 5 NAIGAON: AWCHIT PADA UPHC AREA Kasim Pura - Kidwai Nagar Road ICICI ATM Naigaon - Awchit Pada Road Kasim Pura Active NEW AZAD NAGAR: GAYATRI NAGAR Alamgir Shaikh House to Medical Store 6 Alhera Masjid to Kadariya Masjid Alamgir Shaikh House toAlhera Masjid Medical Store to Kadariya Masjid Active UPHC AREA Road CHAVHAN COLONY: NADI NAKA UPHC Vetal Pada Arun Raut Bunglow 7 Garib Nawaz Hall to Court Road Naigaon Road Vanjar Patti Active AREA Gully 8 ASHOK NAGAR: NADI NAKA UPHC AREA Kalyan Road Wada Road Shanti Nagar Road Kalyan Road Active 9 AAM PADA:AWCHIT PADA UPHC AREA Vanjarpatti Road Aam Pada Road Khandu Pada Awchit Pada Road Active 10 KHANDU PADA:AWCHIT PADA UPHC AREA Vanjarpatti Road Naigaon - Bus Stand Road Maulana Azad Nagar Ansar Mohalla Market Active 11 VAFA CPMPLEX, AVACHIT PADA HP KIDVAIN NAGAR KIDVAI NAGAR ROAD GAYATRI NAGAR ROAD SHANTI NAGAR ROAD Active 12 AAMPADA, AVCHIT -

1 Maharashtra Vasai Dahanu 2 Palghar 3 Thane 4 Bhiwandi

Name of Institutes with Contact NHSRCL official for Training S.N. State District/ Tehsil Name Training Programme Available for enrolment (Duration) NHSRCL Project Office Address Details Coordination 1 Maharashtra Vasai Global Education Trust (GET) 1 Digital Marketing , L1 & L2 04 Months 1.Dy./ CPM/ - Sh.Deepak Kulsheta Project Office Adress - 2 Basic Computers and DTP with Photoshop 06 Months Mobile No. 9619138687 Adinath Villa ,Opp. Tashish Hotel, Vagulsar, 3 Basic Computers and Hardware and Networking 06 Months 2.Manager /Social Development - Sh. Arbind Mahim Road, Soni; Mobile No. 8700379928 Palghar -401404 4 Beautician Basic 03 Months Maharshtra Electrician Electricial with wireman and Electricial motor 5 03 Months rewinding 6 Automobile Technician ,Customar Service Advisor 04 Months 7 Hotel Managetment - Bartender 03 to 04 Months 8 MLT Medicial lab Techician 03 to 04 Months 9 Basic computer, advance web designing (L1 & L2) 03 to 04 Months 10 Basic computers, MS Office, Basic Accounts & Tally & GST 06 Months 11 Basic Computers and AutoCAD 03 to 04 Months 12 Basic Computers advance web designing (Level 1 & level 2) 06 Months Khadi Gram Udhog Multi Disciplinary 1 Carpentry 06 Months 1.Dy./ CPM/ - Sh.S. N. Tripati Training Centre , Dahanu , Agar Road, P.O 2 Electrical Wireman 03 Months Mobile No. 7704903656 Dahanu ,Dist- Palghar- 401601 3 Agarbati Making 01 Month Maharashtra , Phone no - 02528-222626, 2. AM /Social Development - Sh. Gopinath [email protected] 4 Candle Making Course 01 Month Korde 5 Palm Gur Technology 04 Months -

PROPERTY INSIGHTS India Quarter 1, 2021

PROPERTY INSIGHTS India Quarter 1, 2021 INDIA REAL ESTATE OVERVIEW Introduction Economy The Indian economy returned to growth in October - December 2020, following two consecutive quarters of contraction, thereby breaking out of the recession in the aftermath of the COVID-19 outbreak. Economic activity recovered significantly in the quarter with improvement in business sentiments and growth in several high frequency indicators on the back of the festive period that led to a gradual recovery in consumer demand. Real GDP expanded by 0.4% in October – December 2020, as compared to the 7.5% contraction in the previous quarter with manufacturing and construction sectors posting healthy growth. The construction sector recorded an expansion of 6.2%, as compared to the 7.2% contraction in the previous quarter while manufacturing output grew by 1.6%, reversing the 1.5% decline in July – September 2020. Electricity, gas and water supply continued to do well with a 7.3% expansion while the agricultural sector remained a crucial support for the economy, recording a growth of 3.9%, faster than the 3.0% expansion in the previous quarter. Parts of the services sector witnessed a recovery, thereby adding to the economic momentum. For instance, the finance, real estate and professional services segment registered a growth of 6.6% as compared to a 9.5% contraction in the previous quarter. The trade, hotels, transport and communications segment declined by 7.7%, slower than the 15.3% contraction in July – September 2020. Private consumption declined by 2.4%, a marginal recovery over the 11.3% contraction in the previous quarter. -

Mumbai Retail Guide

MUMBAI Cushman & Wakefield Global Cities Retail Guide Cushman & Wakefield | Mumbai | 2019 0 Mumbai serves as the financial capital of India and accounts for the highest GDP contribution in the country, currently standing at approximately 6.61%. Mumbai is the second most populated city in the country with a population of approximately 22 million. Mumbai’s retail market is characterised by smaller disorganised retailers or corner shops retailing various commodities ranging from food to clothes and other household items, as is the case across most cities and towns in India. Rapid economic growth and changing consumer preferences have transformed Mumbai’s retail market, with organised retail increasingly playing a much larger part. Over the years, several large organised developments have sprung up across the city, ranging from mass to premium and luxury. Several local and international luxury brands have opened stores in Mumbai and many consider the city a launch pad for their brand. The presence of Bollywood, one of the world’s leading movie industries, has fuelled the growth of organised retail in Mumbai, with many stars endorsing both local and global brands alike. Brands such as H&M, GAP, Sephora, Scotch & Soda, Muji, Massimo Dutti, Jo Malone, Longchamp, American Eagle, Armani Exchange, Hackett, Onitsuka Tiger, Hamley's, Simon Carter, Du Rhône Chocolatier, Bath & Body Works, Franck Muller, Hublot have all entered the Mumbai retail market. New entrants tend to open stores in malls first, within prominent retail developments, then subsequently establish a footprint on major streets. Luxury labels benefit from high-net-worth individuals (HNI) in Mumbai, many of whom travel abroad frequently and have high disposable incomes.