Building Simpler Insurance Products to Better Protect Customers 02

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Auto –Accidents - What Is “No-Fault” Insurance?

AUTO –ACCIDENTS - WHAT IS “NO-FAULT” INSURANCE? If you are injured in a car accident who pays your medical bills? Believe it or not, your medical insurance carrier does not have the primary responsibility to pay your medical bills for injuries sustained in an automobile accident - The applicable automobile insurance carrier does. But remember, if your injuries or above a certain threshold you can still sue the person who cause your injuries for money damages above what the applicable automobile insurance carrier provides. In New York State each automobile insurance policy must provide coverage known as Personal Injury Protection (“PIP”) and typically referred to a “No-Fault” insurance. Medical bills, some or all of the injured party’s lost wages and other expenses are paid from this portion of the policy, whether or not the injured party caused the accident. So if were in a car accident driving your own vehicle and you are injured as a result of another person's negligence, the no-fault portion of your automobile insurance policy will cover your medical bills to the extent that you have coverage. If your coverage runs out other insurance will kick in. The New York State Insurance Law, requires that all automobile insurance policies issued in this state contain a Personal Injury Protection (“PIP”) or “No-Fault” endorsement with a minimum of $50,000.00 in coverage. Generally speaking, this coverage extends to the driver and passengers in a covered vehicle, as well as to a pedestrian struck by the covered vehicle. The coverage “kicks in” regardless of fault in connection with an accident; under most circumstances, a covered individual will be afforded certain enumerated benefits regardless of that individual’s fault in connection with the happening of the accident. -

Understanding Home and Renters Insurance

Understanding Home and Renters Insurance With multiple types of home and renters insurance and varying degrees of coverage available, it can be a challenge to know what’s right for you. However, carrying adequate insurance is one of the best ways to protect your assets. By paying for home or renters insurance now, you’ll have the coverage you need if something happens in the future. What is home insurance? A home insurance policy provides protection for your home’s physical structure and belongings in the event of damage caused by a disaster or loss of property from theft. Additionally, most home insurance policies also cover your own personal liability for harm caused to other people or property at your home or by members of your household. For instance, if a visitor to your home were to fall down your stairs, your home insurance policy may cover medical expenses. However, home insurance policies don’t cover earthquakes or floods — those are typically covered through separate policies or riders. Make sure your coverage is adequate for your current location and update accordingly when you PCS. Did you know? Most home insurance policies have an occupancy clause stating that your home can’t be unoccupied for longer than a certain period of time. If you deploy and leave your home ? vacant, your policy could become void, so check requirements with your provider. What is renters insurance? If you rent or sublet, renters insurance protects your personal property within your home from damage caused by disaster or theft. Renters insurance policies also protect against personal liability claims, but exclude injuries caused by the structure of the home. -

Employment Practices Liability Insurance Program EPLI

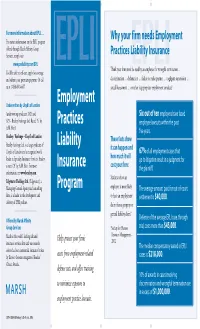

B5848_EPLI 2/14/06 2:49 PM Page 1 For more information about EPLI … Why your firm needs Employment For instant information on the EPLI program offered through Marsh Affinity Group Services, simply visit Practices Liability Insurance www.proliablity.com/EPLI Think your firm won’t be sued by an employee for wrongful termination … You’ll be able to self-rate, apply for coverage EPLI EPLI and submit your premium payment. Or call discrimination … defamation … failure to make partner … negligent supervision … us at 1-888-601-6667. sexual harassment … or other inappropriate employment conduct? Underwritten by Lloyd’s of London Employment (underwriting syndicates 2623 and Six out of ten employers have faced 623 – Beazley Furlonge Ltd. Rated “A” by Practices employee lawsuits within the past A.M. Best) five years. Beazley / Furlonge – Lloyd’s of London These facts show Beazley Furlonge Ltd. is a large syndicate of Liability it can happen and Lloyd’s of London and a recognized world 67% of all employment cases that leader in Specialty Insurance Services. Beazley how much it will go to litigation result in a judgment for is rated “A” by A.M. Best. For more Insurance cost your firm: the plaintiff. information, see www.beazley.com. Statistics show an Edgewater Holdings Ltd. (Edgewater), a Managing General Agency and consulting Program employer is more likely The average amount paid for out-of-court firm, is a leader in the development and to have an employment settlement is $40,000. delivery of EPLI policies. claim than a property or general liability claim.* Offered by Marsh Affinity Defense of the average EPLI case, through Group Services *Society for Human trial, costs more than $45,000. -

AUTOMOBILE INSURANCE TOOLKIT Automobile Insurance Toolkit

Florida Department of Financial Services AUTOMOBILE INSURANCE TOOLKIT Automobile Insurance Toolkit Insurance coverage is an integral part of a solid financial foundation. Insurance can help us recover financially after illness, accidents, natural disasters or even the death of a loved one. There are a wide variety of insurance products available and choosing the correct type and amount of coverage can be a challenge. This toolkit provides information to assist you with insuring your automobile and tips for settling an automobile insurance claim. TABLE OF CONTENTS Click a title or page number to navigate to a section. 01 Coverages & Minimum Requirements - 4 Coverage Descriptions - 5 Insurance Requirements for Special Cases - 8 02 Underwriting Guidelines - 11 Underwriting Factors That Cannot Affect Your Ability to Purchase Insurance - 11 Underwriting Factors That Affect Your Insurance Policy Premium - 12 Other Factors Affecting Your Premiums - 13 Shopping for Auto Insurance - 13 03 Automobile Claims - 14 Actions to Take Before and After an Auto Accident - 14 Disputing Claim Settlements - 16 04 Shopping for Coverage Checklist - 17 01 Coverages & Minimum Requirements In Florida, vehicle owners may be required to The second type of auto insurance is outlined in the purchase two types of auto insurance. Florida Financial Responsibility Law. It requires drivers The first type of auto insurance is outlined in the who have caused accidents involving bodily injury/death Florida Motor Vehicle No-Fault Law (s. 627.736, Florida or received certain citations, to purchase bodily injury Statutes). It requires every person who registers a liability (BI) coverage with minimum limits of $10,000 vehicle in Florida to provide proof they have personal per person and $20,000 per accident, referred to as injury protection (PIP) and property damage liability split limits. -

What You Need to Know

What AutoAuto you InsuranceInsurance need to know A consumer information publication The Minnesota Department of Commerce has prepared this guide to help you better understand auto insurance. It gives you information on shopping for insurance, the different types of coverage, and a basic understanding of “no fault” coverage. The Minnesota Department of Commerce regulates insurance agents, agencies, adjusters, and companies operating in Minnesota. If they are licensed to do business in the State, they are responsible for adhering to the laws and rules that govern the industry. This guide does not list all of these regulations. If you have a question about your insurance, please contact the Department’s Consumer Response Team at 651-296-2488, or toll free 800-657-3602. Duplication of this guide is encouraged. Please feel free to copy this information and share it with others. Department of Commerce Auto Insurance can protect you from the financial costs of an accident or injury, provided you have the proper coverage. Yet many people are unclear about what their insurance policy cov- ers until it is too late. They may have difficulties settling a claim or face rate increases or termination of coverage. Auto Insurance I s ... Protection. Insurance is a way of transferring risk for a loss among a certain group of people. You, and others, pay premiums to an insurance company to be reimbursed if you have an acci- dent. The amount you can collect and under what circumstances are outlined in your policy. Required. Under most circumstances, a licensed vehicle in the state of Minnesota must have liability, personal injury protection, uninsured motorist, and underinsured motorist coverage. -

Consumers Guide to Auto Insurance

CONSUMERS GUIDE TO AUTO INSURANCE PRESENTED TO YOU BY THE DEPARTMENT OF BUSINESS REGULATION INSURANCE DIVISION 1511 PONTIAC AVENUE, BLDG 69-2 CRANSTON, RI 02920 TELEPHONE 401-462-9520 www.dbr.ri.gov Elizabeth Kelleher Dwyer Superintendent of Insurance TABLE OF CONTENTS Introduction………………………………………………………………1 Underwriting and Rating………………………………………………...1 What is meant by underwriting and how is it accomplished…………..1 How are rates and premium charges determined in Rhode Island……1 What factors are considered in ratemaking……………………………. 2 What discounts are used in determining final premium cost…………..3 Rhode Island Automobile Insurance Plan…………………..…………..4 Regulation of Rates……………………………………………………….4 The Tort System…………………………………………………………..4 Liability Coverages………………………………………………………..5 Coverages Other Than Liability…………………………………………5 Physical Damage to the Automobile……………………………………..6 Other Optional Coverages………………………………………………..6 The No-Fault System……………….……………………………………..7 Smart Shopping……………………………………………………………7 Shop for True Comparison………………………………………………..8 Consumer Protection Available...…………………………………………8 What to Do if You are in an Automobile Accident………………………9 Your State Insurance Department………………………………….........9 Auto Insurance Buyer’s Worksheet…………………………………….10 Introduction Auto insurance is an expensive purchase for most Americans, and is especially expensive for Rhode Islanders. Yet consumers rarely comparison-shop for auto insurance as they might for other products and services. Auto insurance companies vary substantially both in price and service to policyholders, so it pays to shop around and compare different insurance companies. This guide to buying auto insurance was developed to help you become a more knowledgeable policyholder and to get the combination of price and service best suited to your needs. It provides information on how to shop for coverage and how insurance premiums are determined. You will also find an Auto Insurance Buyer’s Worksheet in the guide to help you compare premium prices among insurers. -

Tax Risk Insurance: Taking It Captive

taxnotes federal ■ Volume 171, Number 4 April 26, 2021 Tax Risk Insurance: Taking It Captive by Ken Brewer and Albert Liguori Reprinted from Tax Notes Federal, April 26, 2021, p. 549 For more Tax Notes content, please visit www.taxnotes.com. © 2021 Tax Analysts. All rights reserved. Analysts does not claim copyright in any public domain or third party content. TAX PRACTICE tax notes federal Tax Risk Insurance: Taking It Captive by Ken Brewer and Albert Liguori is to explore the U.S. tax implications of that meeting. Behold: captive tax risk insurance!3 In our experiences, the use of tax risk insurance has been most prevalent in the mergers and acquisitions context. But as we mentioned in our last article, we have seen it becoming more common in the context of large corporate groups seeking to manage their global tax risks, regardless of whether they are related to M&A.4 In either context, the use of tax risk insurance lends itself to captive arrangements, for the same reasons that have caused captive arrangements to be desirable for other types of insurance risks. Ken Brewer is a senior adviser and Captive Insurance and the U.S. Tax Implications international tax practitioner with Alvarez & Thereof Marsal Taxand LLC in Miami, and Albert Liguori is a managing director in the firm’s New As an alternative to traditional insurance York office. The authors send special thanks to protection, which is obtained from one or more of Brian Pedersen, managing director at Alvarez & the many underwriters offering that coverage to Marsal Taxand, for his contributions and the public, captive insurance is obtained from a review. -

Auto Insurance and How Those Terms Affect Your Coverage

Arkansas Insurance Department AUTOMOBILE INSURANCE Asa Hutchinson Allen Kerr Governor Commissioner A Message From The Commissioner The Arkansas Insurance Department takes very seriously its mission of “consumer protection.” We believe part of that mission is accomplished when consumers are equipped to make informed decisions. We believe informed decisions are made through the accumulation and evaluation of relevant information. This booklet is designed to provide basic information about automobile insurance. Its purpose is to help you understand terms used in the purchase of auto insurance and how those terms affect your coverage. If you have questions or need additional information, please contact our Consumer Services Division at: Phone: (501) 371-2640; 1-800-852-5494 Fax: (501) 371-2749 Email: [email protected] Web site: www.insurance.arkansas.gov Mission Statement The primary mission of the State Insurance Department shall be consumer protection through insurer insolvency and market conduct regulation, and fraud prosecution and deterrence. 1 Coverages Provided by Automobile Insurance The automobile insurance policy is comprised of several separate types of coverages: COLLISION, COMPREHENSIVE, LIABILITY, PERSONAL INJURY PROTECTION, UNINSURED MOTORIST, UNDERINSURED MOTORIST and other coverages. You are required by law to purchase liability protection only. All others are voluntary unless required by a lienholder. LIABILITY Under Legislation passed in 1987 and 1999, it is unlawful for any person to operate a motor vehicle within this state unless the vehicle is insured with the minimum amount of liability coverage: $25,000 for bodily injury or death of one person in any one accident; $50,000 for bodily injury or death of two or more persons in any one accident and $25,000 for damage to or destruction of the property of others. -

Overwhelmed an Overview of Factors That Impact Upon Insurance Disclosure Comprehension, Comparability and Decision Making, September 2018

Overwhelmed An overview of factors that impact upon insurance disclosure comprehension, comparability and decision making, September 2018 Monash University and the Financial Rights Legal Centre, with the support of funding from the Victorian Fire Services Levy Monitor have produced a report titled: (In)effective Disclosure: A study of consumers purchasing home and contents insurance1. The experimental study aimed at examining how the newly introduced requirement for providing a Key Fact Sheet (KFS) for home and contents insurance enhances consumer perceptions and decision outcomes. The study in particular examined how: (i) consumers engage with the KFS and/or Product Disclosure Statement (PDS) at the point of sale; (ii) consumers perceive the information provided by the KFS and/or PDS; and (iii) the obtaining of this information and knowledge leads to perceptible changes in consumer decision-making behaviour. The study tested engagement, comprehension and behaviour of consumers in a specifically designed, experimentally controlled environment that nevertheless reflected the insurance purchasing process, albeit a simplified version. The study limited the number of parameters to ensure that the participant respondents were, in a sense, given the best chance to select the best PDS or KFS. For example, all tested policies were equally priced. Policies were non-branded to control for the effect of brand names. PDSs were reduced in size to 20 pages each rather than the usual 80 plus pages. KFSs also closely matched the legislated requirements but the number of covered events was reduced. The decision to essentially simplify the KFS and PDS and control for as many factors as possible, was made to ensure that the findings were obtained in as optimized a purchasing and decision-making context as possible. -

The Insurability of Claims for Restitution

ARTICLE 1 (FRENCH) (DO NOT DELETE) 5/22/16 9:34 PM THE INSURABILITY OF CLAIMS FOR RESTITUTION Christopher C. French* Does and should a wrongdoer’s liability insurance cover an aggrieved party’s claim for restitution (e.g., a claim for the disgorgement of ill-gotten gains)? This article answers those questions. It does so by first answering the question of whether claims for restitution are covered under the terms of liability insurance policies. Then, after concluding that they are, it addresses the question of whether claims for restitution should be insurable as a matter of public policy and insurance law theory. There are long- standing legal and equitable principles that, on the one hand, dictate that a wrongdoer should not be allowed to benefit from its wrongdoing, which the wrongdoer would if insurance were allowed to cover claims for restitution. On the other hand, there are competing public policies that favor enforcing contracts and compensating innocent victims. If a claim for restitution is covered by the terms of an insurance policy, but such claims are viewed as uninsurable as a matter of public policy, then policyholders would have paid millions of dollars in premiums for policies that provide illusory coverage and thousands of innocent victims with billions of dollars of claims would not receive compensation. In analyzing these issues, this article does so by using two common examples where the insurability of claims for restitution are regularly implicated—intellectual property infringement claims under Commercial General Liability insurance policies (CGL policies) and shareholder fraud claims under Directors and Officers liability insurance policies (D&O policies). -

10 Things You Should Know About Purchasing Home Insurance

10 Things You Should Know About Purchasing Home Insurance 1. You Need Home Insurance Homeowners need to purchase home insurance to protect their homes and personal property. Tenants need insurance to protect their furniture and other personal property. Everyone needs protection against liability for accidents that injure other people or damage their property. 2. Decide How Much Coverage You Need The better your coverage, the less you will have to pay out of your own pocket if disaster strikes. In some cases, your lender decides how much coverage you need and may require you to buy a policy that covers at least the amount of the mortgage. It is important to note that the amount of coverage you buy for your house, contents and personal property will affect the price you pay. 3. Compare Deductibles The deductible is the amount you have to pay out of pocket on each claim and applies only to coverage on your house and personal property. Make sure when choosing a policy that you are comfortable paying the deductible if you make a claim. Remember, a policy with a $100 deductible will cost more than one with a $250 deductible. Higher deductibles may be available at a reduced price. 4. Replacement Cost or Actual Cash Value? You have the option to choose to insure your home and belongings for either replacement cost or actual cash value. Replacement cost is the amount it would take to replace or rebuild your home or repair damages with materials of similar kind and quality, without deducting for depreciation. It is important to insure your home for at least 80 percent of its replacement value. -

UNDERSTANDING INSURANCE Participant Guide

MINDYOUR FINANCES UNDERSTANDING INSURANCE Participant Guide INCHARGE DEBT SOLUTIONS • WWW.INCHARGE.ORG 01 AN OLD STORY. It was a common practice for ancient caravans to split up goods and take different routes to the delivery point. In this way, the risk of losing the full cargo to thieves was lessened. During the 12th and 13th centuries, artisans in Europe worked in guilds. They’d pay money into the guilds and if their shop burned down (common because most dwellings were made of wood), the guild would help them rebuild. If they were injured or killed, the guilds would pay for the care of their widows and children. A NEW STORY. Gloria was a 65-year old widow. She worked hard all her life in the tourism industry. She started as a waitress at the age of 15, and for the next fifty years worked many jobs, with very little time off. She worked as a waitress, a maid, and a hostess in a large hotel. Gloria had just retired. With a paid off home, she was looking forward to a mortgage-free retirement. One January morning, the wiring in her walls caught fire. When she returned from running errands, her home was nearly gone. She didn’t know it at the time, but her dog had escaped into a neighbor’s backyard. At 65, Gloria didn’t have the time or the strength to start over. QUESTIONS: What can Gloria do? Do you agree with this statement? Insurance is great to have, if you can afford it. 02 INCHARGE DEBT SOLUTIONS • WWW.INCHARGE.ORG LIFE IS RISKY.