Downtown Tampa Parking Survey Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Towards Trash Free Waters: Quantifying Potential Aquatic Trash Recovery in the Hillsborough River Watershed

Towards Trash Free Waters: Quantifying Potential Aquatic Trash Recovery in the Hillsborough River Watershed Prepared for Nestlé Waters North America October 27, 2015 Prepared by Timothy G. Townsend (Principal Investigator) Max J. Krause Sarah A. Gustitus Jeremy Toms University of Florida Gainesville, FL 32611 i Executive Summary Despite advances in solid waste management and increased awareness of the negative environmental consequences of pollution, littering is still common in the US. Littering can be the result of carelessness, accidents, or intentional actions, but the effect is the same. In recent years, concerned citizens have increased their attention to litter in the Hillsborough River Watershed (HRW). The University of Florida (UF) research team collaborated with local municipalities and non-government organizations (NGOs) to quantify and map the quantity of collected litter within the HRW. Because much of the storm water within the HRW drains into the Hillsborough River, all of the litter within the watershed has the potential to become aquatic trash (PAT). The PAT that was collected in roadside and park cleanups before it made its way into the Tampa Bay or the Gulf of Mexico (recovered PAT) was cataloged into a database and mapped using ESRI ArcGIS software. Concentrations of recovered PAT were reported as pounds per acre for 1,015 cleanup events at 168 unique sites within the HRW from 2008-2014, shown in Figure E1. Additionally, educational campaigns such as storm drain markings and field visits by the WaterVentures mobile lab were mapped to identify where residents could be expected to have increased awareness of the negative issues associated with littering. -

Tampa Bay Next Presentation

Welcome East Tampa Area Community Working Group September 25, 2018 Tina Fischer Collaborative Labs, St. Petersburg College Tonight’s Agenda • Open House Area (6:00 - ongoing) – Information about related studies, projects, etc. • Presentation (6:30 - 7:00) – SEIS Update – Overview of Downtown Interchange Design Options • Roundtable Discussions (7:00 - 8:00) – Dive into details and provide input with 2 sessions • Closing Comments/Announcements (8:00 - 8:10) Real Time Record • Comprehensive meeting notes and graphics - available next week • Presentation and Graphic Displays – available tomorrow • Posted on TampaBayNext.com TampaBayNext.com (813) 975-NEXT [email protected] TampaBayNext @TampaBayNext Your input matters. Your ideas help shape the Tampa Bay Next program. Now on to our presentation Chloe Coney Richard Moss, P.E. Sen. Darryl Rouson Alice Price/Jeff Novotny Supplemental Environmental Impact Statement (SEIS) Update FDOT District Seven Interstate OverviewModernization I-275 @ I-4 - Highlighted in Orange North W S Small Group Meetings to date Old Seminole Heights Westshore Palms – May 3 SE Seminole Heights North Bon Air – Jun 14 Tampa Heights V.M. Ybor Tampa Heights – Jun 26 East Tampa Oakford Park – Jul 9 Comm. East Tampa Comm. Partnership – Jul 10 Partnership Encore! – Jul 10 Ridgewood Park SE Seminole Heights – Jul 17 Ridgewood Park – Jul 24 North Bon Air College Hill Old Seminole Heights – Aug 9 Civic Assoc. Corporation to Develop Comm. – Aug 17 Trio at Encore! – Aug 21 Jackson College Hill Civic Assoc. – Aug 23 Heights V.M. Ybor Neighborhood Assoc. – 9/5 Ybor Chamber/Hist Ybor/East Ybor/Gary– 9/11 Encore! Hist Jackson Heights Neighborhood Assoc. -

Florida Department of Education

THE FOLLOWING CHANGES ARE FOR FISCAL YEAR 06-07 FLORIDA DEPARTMENT OF EDUCATION Implementation Date: DOE INFORMATION DATA BASE REQUIREMENTS Fiscal Year 2001-02 VOLUME I: AUTOMATED STUDENT INFORMATION SYSTEM July 1, 2001 AUTOMATED STUDENT DATA ELEMENTS Element Name: Prior School/Location: District/County Definition/Domain A two-character code which identifies the district/county in which a student was enrolled in school prior to enrolling in the current school. See Appendix C for district numbers. CODE DEFINITION 01 – 69, 71-75, 78 & 79 State assigned number for school district or other agency 99 Other than a Florida school Note: District 70 was used to report the Eckerd Challenge Program prior to 1993-94. Length: 2 Grades and Programs Requiring This Data Element: * Format: Numeric All Program Grades PK-12 Compatibility Requirement: Compatible Use Types: State Reporting Formats Requiring This Data Element: State Report Prior School Status/Student Attendance DB9 55x Local Accountability F.A.S.T.E.R. Data Element Number: 163126 Reported in Survey Periods: 1 2 3 4 5 9 Revised: 12/06 Volume I Effective: 7/06 Page Number: 222-1 FLORIDA DEPARTMENT OF EDUCATION Implementation Date: DOE INFORMATION DATA BASE REQUIREMENTS Fiscal Year 2006-07 VOLUME I: AUTOMATED STUDENT INFORMATION SYSTEM July 1, 2006 AUTOMATED STUDENT DATA ELEMENTS APPENDIX W TITLE I SUPPLEMENTAL EDUCATIONAL SERVICES SCHOOLS – 2006-07 TI SES TI SES District School School Name District School School Name ALACHUA 0021 CHARLES W. DUVAL ELEM SCHOOL BREVARD 3061 HARBOR CITY ELEMENTARY ALACHUA 0031 J. J. FINLEY ELEMENTARY SCHOOL SCHOOL ALACHUA 0071 LAKE FOREST ELEMENTARY BREVARD 4031 MILA ELEMENTARY SCHOOL SCHOOL BREVARD 4101 GARDENDALE ELEMENTARY ALACHUA 0083 ANCHOR SCHOOL MAGNET SCHOOL ALACHUA 0101 W. -

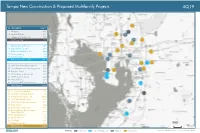

Tampa New Construction & Proposed Multifamily Projects

Tampa New Construction & Proposed Multifamily Projects 4Q19 ID PROPERTY UNITS 1 Wildgrass 321 3 Union on Fletcher 217 5 Harbour at Westshore, The 192 Total Lease Up 730 15 Bowery Bayside Phase II 589 16 Tapestry Town Center 287 17 Pointe on Westshore, The 444 28 Victory Landing 69 29 Belmont Glen 75 Total Under Construction 1,464 36 Westshore Plaza Redevelopment 500 37 Leisey Road Mixed Used Development 380 38 Progress Village 291 39 Grand Cypress Apartments 324 43 MetWest International 424 44 Waverly Terrace 214 45 University Mall Redevelopment 100 Total Planned 2,233 69 3011 West Gandy Blvd 80 74 Westshore Crossing Phase II 72 76 Village at Crosstown, The 3,000 83 3015 North Rocky Point 180 84 6370 North Nebraska Avenue 114 85 Kirby Street 100 86 Bowels Road Mixed-Use 101 87 Bruce B Downs Blvd & Tampa Palms Blvd West 252 88 Brandon Preserve 200 89 Lemon Avenue 88 90 City Edge 120 117 NoHo Residential 218 Total Prospective 4,525 2 mi Source: Yardi Matrix LEGEND Lease-Up Under Construction Planned Prospective Tampa New Construction & Proposed Multifamily Projects 4Q19 ID PROPERTY UNITS 4 Central on Orange Lake, The 85 6 Main Street Landing 80 13 Sawgrass Creek Phase II 143 Total Lease Up 308 20 Meres Crossing 236 21 Haven at Hunter's Lake, The 241 Total Under Construction 477 54 Bexley North - Parcel 5 Phase 1 208 55 Cypress Town Center 230 56 Enclave at Wesley Chapel 142 57 Trinity Pines Preserve Townhomes 60 58 Spring Center 750 Total Planned 1,390 108 Arbours at Saddle Oaks 264 109 Lexington Oaks Plaza 200 110 Trillium Blvd 160 111 -

Hillsborough County Trails, Paths & Bicycle Guide

Get Inspired to Bike! to Inspired Get Davis Island Trail Island Davis at the Suncoast Trail and other local trails. local other and Trail Suncoast the at 200 feet. This system will soon be available available be soon will system This feet. 200 used bicycle paths. bicycle used Yellow numbered decals are placed every every placed are decals numbered Yellow trick-skating maneuvers on heavily heavily on maneuvers trick-skating rules as bicyclists. Do not perform perform not Do bicyclists. as rules their location within one of these trails. trails. these of one within location their costs; and improved quality of life. of quality improved and costs; Skaters should follow the same travel travel same the follow should Skaters • Greenway can easily tell first responders responders first tell easily can Greenway and other chronic diseases; lower health care care health lower diseases; chronic other and Tampa Bay Trail and Town ‘N Country Country ‘N Town and Trail Bay Tampa safely on the left. left. the on safely reduced risk of coronary heart disease, stroke, stroke, disease, heart coronary of risk reduced Number System. Trail users at the Upper Upper the at users Trail System. Number when approaching others, then pass pass then others, approaching when way. benefits for people of all ages, including including ages, all of people for benefits counties to implement a 911 Station Station 911 a implement to counties Sound your bell or call out a warning warning a out call or bell your Sound • Pedestrians always have the right-of- the have always Pedestrians • Regular bicycling carries many health health many carries bicycling Regular Hillsborough County is one of the first first the of one is County Hillsborough Signal to Other Cyclists Other to Signal pedestrians. -

Transforming Tampa's Tomorrow

TRANSFORMING TAMPA’S TOMORROW Blueprint for Tampa’s Future Recommended Operating and Capital Budget Part 2 Fiscal Year 2020 October 1, 2019 through September 30, 2020 Recommended Operating and Capital Budget TRANSFORMING TAMPA’S TOMORROW Blueprint for Tampa’s Future Fiscal Year 2020 October 1, 2019 through September 30, 2020 Jane Castor, Mayor Sonya C. Little, Chief Financial Officer Michael D. Perry, Budget Officer ii Table of Contents Part 2 - FY2020 Recommended Operating and Capital Budget FY2020 – FY2024 Capital Improvement Overview . 1 FY2020–FY2024 Capital Improvement Overview . 2 Council District 4 Map . 14 Council District 5 Map . 17 Council District 6 Map . 20 Council District 7 Map . 23 Capital Improvement Program Summaries . 25 Capital Improvement Projects Funded Projects Summary . 26 Capital Improvement Projects Funding Source Summary . 31 Community Investment Tax FY2020-FY2024 . 32 Operational Impacts of Capital Improvement Projects . 33 Capital Improvements Section (CIS) Schedule . 38 Capital Project Detail . 47 Convention Center . 47 Facility Management . 49 Fire Rescue . 70 Golf Courses . 74 Non-Departmental . 78 Parking . 81 Parks and Recreation . 95 Solid Waste . 122 Technology & Innovation . 132 Tampa Police Department . 138 Transportation . 140 Stormwater . 216 Wastewater . 280 Water . 354 Debt . 409 Overview . 410 Summary of City-issued Debt . 410 Primary Types of Debt . 410 Bond Covenants . 411 Continuing Disclosure . 411 Total Principal Debt Composition of City Issued Debt . 412 Principal Outstanding Debt (Governmental & Enterprise) . 413 Rating Agency Analysis . 414 Principal Debt Composition . 416 Governmental Bonds . 416 Governmental Loans . 418 Enterprise Bonds . 419 Enterprise State Revolving Loans . 420 FY2020 Debt Service Schedule . 421 Governmental Debt Service . 421 Enterprise Debt Service . 422 Index . -

The Tampa Center City Plan Connecting Our Neighborhoods and Our River for Our Future

The Tampa Center City Plan Connecting Our Neighborhoods and Our River for Our Future The Tampa Center City Plan Connecting Our Neighborhoods and Our River for Our Future NOvembeR 2012 Prepared for: City of Tampa IMAGE PLACEHOLDER Prepared by: AECOM 150 North Orange Avenue Orlando, Florida 32801 407 843 6552 AECOM Project No. : 60250712 AECOM Contact : [email protected] In Collaboration With: Parsons Brinckerhoff The Leytham Group ChappellRoberts Blackmon Roberts Group MindMixer Crossroads Engineering Fowler White Boggs PA Stephanie Ferrell FAIA Architect Martin Stone Consulting, LLC © AeCOm Technical Services 2012 This document has been prepared by AeCOm on behalf of the City of Tampa, Florida. This project was made possible through a Sustainable Communities Challenge Grant provided by the U.S. Department of Housing and Urban Development. Participation List City Team Workshop Participants bob buckhorn - Mayor Chris Ahern Duncan broyd David Crawley bruce earhart bob mcDonaugh - Economic Development Administrator Art Akins Rod brylawski Nelson Crawley Shannon edge Thomas Snelling - Planning & Development Director Catherine Coyle - Planning Manager Adjoa Akofio-Swah bob buckhorn Darryl Creighton Diane egner Randy Goers - Project Manager beth Alden Arnold buckley Jim Crews Chris elmore J.J. Alexander benjamin buckley Laura Crews michael english Consultant Team Albert Alfonso michelle buckley Daryl Croi maggie enncking Robert Allen Davis burdick Andrea Cullen James evans AECOM ChappellRoberts Joseph Alvarez Andy bushnell Wence Cunnigham -

National Register of Historic Places JUN23 Multiple Property

NPS Form 10-900-b . OMB No. 1024-0018 {Jan. 1987) United States Department of the Interior National Park Service National Register of Historic Places JUN23 Multiple Property Documentation Form NATIONAL REGISTER This form is for use in documenting multiple property groups relating to one or several historic contexts. See instructions in Guidelines for Completing National Register Forms (National Register Bulletin 16). Complete each item by marking "x" in the appropriate box or by entering the requested information. For additional space use continuation sheets (Form 10-900-a). Type all entries. A. Name of Multiple Property Listing Mediterranean Revival Style Buildings of Davis Islands_______________ B. Associated Historic Contexts Architecture and Real Estate Development in Central and South Florida from the Boom Period to the Great Depression, 1920-1955___________ C. Geographical Data______________________________________________ The nominated properties are all located on the larger of the two islands that form the Davis Islands Subdivision, which is surrounded by the waters of Hillsborough Bay and Seddon Channel. (See Continuation Sheet for U1M List) See continuation sheet D. Certification As the designated authority under the National Historic Preservation Act of 1966, as amended, I hereby certify that this documentation form meets the National Register) documentation standards and sets forth requirements for the listing of related prap^ftfps consistent with theJ<lationalXegister criteria. This submission meets the procedural and professional forth in 36/£FR P^ftt60-affof^the Secretary^ the Interior's Standards for Planning and Evaluation. 16. 1Q8Q Signature of cei^jjyifig official /^ Date _____State Historic PreservatJrarf'Officer________________________ State or Federal agency and bureau I, hereby, certify that this multiple property documentation form has been approved by the National Register as a basis for euating related properties for listing in the National Register. -

TAMPA HISTORICAL SOCIETY 1977-78 M Rs

Sunland Tribune Volume 4 Article 1 1978 Full Issue Sunland Tribune Follow this and additional works at: http://scholarcommons.usf.edu/sunlandtribune Recommended Citation Tribune, Sunland (1978) "Full Issue," Sunland Tribune: Vol. 4 , Article 1. Available at: http://scholarcommons.usf.edu/sunlandtribune/vol4/iss1/1 This Full Issue is brought to you for free and open access by Scholar Commons. It has been accepted for inclusion in Sunland Tribune by an authorized editor of Scholar Commons. For more information, please contact [email protected]. THE SUNLAND TRIBUNE On Our Cover Volume IV Number 1 November, 1978 Old post card depicts Gordon Keller Journal of the Memorial Hospital, a "permanent TAMPA monument" to the memory of City HISTORICAL SOCIETY Treasurer and merchant Gordon Tampa, Florida Keller. HAMPTON DUNN Editor -Photo from HAMPTON DUNN COLLECTION Officers DR. L. GLENN WESTFALL 7DEOHRI&RQWHQWV President MRS. DAVID McCLAIN GORDON WHO? GORDON KELLER 2 Vice President By Hampton Dunn MRS. MARTHA TURNER Corresponding Secretary TAMPA HEIGHTS: MRS. THOMAS MURPHY TAMPA'S FIRST RESIDENTIAL SUBURB 6 Recording Secretary By Marston C. Leonard MRS. DONN GREGORY Treasurer FAMOUS CHART RECOVERED 11 Board of Directors I REMEMBER AUNT KATE 12 Mrs. A. M. Barrow Dr. James W. Covington By Lula Joughin Dovi Hampton Dunn Mrs. James L. Ferman Mrs. Joanne Frasier THE STORY OF DAVIS ISLANDS 1924-1926 16 Mrs. Thomas L. Giddens By Dr. James W. Covington Mrs. Donn Gregory Mrs. John R. Himes Mrs. Samuel 1. Latimer, Jr. DR. HOWELL TYSON LYKES Marston C. (Bob) Leonard Mrs. David McClain FOUNDER OF AN EMPIRE 30 Mrs. Thomas Murphy By James M. -

Tampa Early Lighting and Transportation Arsenio M

Sunland Tribune Volume 17 Article 7 2018 Tampa Early Lighting and Transportation Arsenio M. Sanchez Follow this and additional works at: http://scholarcommons.usf.edu/sunlandtribune Recommended Citation Sanchez, Arsenio M. (2018) "Tampa Early Lighting and Transportation," Sunland Tribune: Vol. 17 , Article 7. Available at: http://scholarcommons.usf.edu/sunlandtribune/vol17/iss1/7 This Article is brought to you for free and open access by Scholar Commons. It has been accepted for inclusion in Sunland Tribune by an authorized editor of Scholar Commons. For more information, please contact [email protected]. TAMPA EARLY LIGHTING AND TRANSPORTATION By ARSENIO M. SANCHEZ An early Tampa Electric Company (not the After signing the contract the electric present Co.) was organized on January 29, company became expansion-minded. More 1887. powerful generators were needed; and to obtain money to buy them, the company was About three months later the company reorganized, becoming Tampa Light & brought the first Electric lights to the city of Power Company, with Solon B. Turman as Tampa. A small Westinghouse generator President. was brought in and two arc lights were erected, one at the corner of Franklin and Tampa had to wait for its lights, however. Washington Streets; and one in front of the An epidemic of yellow fever struck the city, brand new "Dry Goods Palace." bringing progress to a halt; and the new electric light system was not installed until Tampa's first "light show" took place May of 1888. A power plant was built at the Monday, April 28, 1887. Word got around corner of Tampa and Cass Streets. -

Historic Preservation Challenge Grant Past Awards

Appendix “K” HISTORIC PRESERVATION CHALLENGE GRANT PAST AWARDS 2012 HERITAGE TOURISM PROJECT ALLOCATIONS 2012 FIRST ROUND Grantee: American Institute of Architects (AIA) Project: “Past Forward Tampa Bay/Tampa Bay Times in Education” Award: $10,000 Status: Completed The allocation was for the production of Past Forward Tampa Bay, a newspaper insert distributed to all eighth grade students at Hillsborough County schools (approximate circulation 16,300); inserted into all Hillsborough County home delivery and single copy (retail) copies of the Tampa Bay Times on a Sunday (approximate circulation 115,000); inserted into all Hillsborough County copies of tbt* on a Friday (approximate circulation 68,000); and distributed via partner organizations throughout Hillsborough County during the Republican National Convention (RNC). Copies of the publication were distributed to visitor bureaus and AIA Florida chapters throughout the state after the RNC. The County was recognized in the publication for its support. Grantee: Friends of Henry B. Plant Park Project: “Plant Park Cell Phone Tour” Award: $10,000 Status: Completed The allocation was for the development of a cell phone tour through Plant Park, which linked the Park, H.B. Plant Museum and the University of Tampa. A QR code for each stop on the walk was installed on architecturally designed stones placed in the gardens. The tour provides 20 stations of historical and botanical information in English and Spanish along with a brochure. www.friendsofplantpark.com/take-the-tour Grantee: Friends of Public Art, Inc. Project: “Tampa Cultural & Heritage Walking Tour” Award: $2,000 Status: Declined by Agency The allocation was for the website development with a digitized brochure of the Tampa Cultural and Heritage Walking Tour that would feature public art, historic architecture and historic significant events that shaped the City of Tampa, The tour would highlight walkable routes throughout sections of Downtown, including the Channel District and Ybor City. -

Virtual Workshop of the Livable Roadways Committee Call to Order

Virtual Workshop of the Livable Roadways Committee Wednesday, May 19, 2021, 9:00 – 11:00 a.m. Call to Order The County Center and Plan Hillsborough offices are closed to the public in response to the COVID-19 pandemic. Members of the public may access this meeting and participate via the GoToWebinar link below, or by phoning in. Technical support during the meeting may be obtained by contacting Jason Krzyzanowski at (813) 272-5940 or [email protected]. To view presentations and participate from your computer, tablet or smartphone, go to: https://attendee.gotowebinar.com/register/3258942983704569359. Register in advance to receive your personalized link which can be saved to your calendar. Dial in LISTEN-ONLY MODE: (415) 655-0060-4212 Access Code 670-174-100 Public comments are welcome and may be given in person at this teleconference meeting by logging into the website above and clicking the “raise hand” button. Comments may also be provided before the start of the meeting: • by leaving a voice message at (813) 273-3774 ext. 6. • by e-mailing [email protected] • by visiting the event posted on the TPO Facebook page. Written comments will be read into the record, if brief, and provided in full to the committee members. I. Public Comment - 3 minutes per speaker, please II. Approval of Minutes – April 21, 2021 III. Discussion Items- As this is a non-voting workshop, members are asked to individually identify any concerns or objections to these items. A. Transportation Improvement Program Update (Johnny Wong, TPO Staff) B. McIntosh Road PD&E Study Advance Notification (Allison Yeh, TPO Staff) C.