WMWRIGLEY AR2004.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Magic's Kingdom

BROOKLYN’S REAL NEWSPAPERS Including The Brooklyn Heights Paper, Carroll Gardens-Cobble Hill Paper, DUMBO Paper and the Downtown News Published every Saturday — online all the time — by Brooklyn Paper Publications Inc, 55 Washington St, Suite 624, Brooklyn NY 11201. Phone 718-834-9350 • www.BrooklynPapers.com • © 2005 Brooklyn Paper Publications • 16 pages •Vol.28, No. 21 BWN • Saturday, May 21, 2005 • FREE Magic’s BORO’S BEACON kingdom Our 9-11 memorial dedicated in Ridge NBA Hall-of-Famer buys By Jotham Sederstrom The Brooklyn Papers On a breezy, sun-filled day eerily reminiscent of the September morning when two commercial jets were flown into the World Williamsburgh Bank tower Trade Center towers, several hundred people, many of whom wit- nessed the destruction from the 69th Street Pier in Bay Ridge, returned to that dock for the unveiling of Brooklyn’s first-ever By Jess Wisloski borough-wide memorial to victims of those attacks. The Brooklyn Papers Fire and police boats quietly circled Monday morning as, one-by-one, He conquered the NBA, he’s a giant in the officials involved with the Brooklyn Remembers memorial project stepped retail franchising field and now Earvin behind a podium and carefully reflected on the attacks of Sept. 11, 2001. A “Magic” Johnson towers above Brooklyn with light fog blurred an otherwise clear view of Lower Manhattan. his latest purchase — the Williamsburgh Sav- “You can understand what a perfect place this is for a memorial. Just ings Bank tower. look around you,” said Mayor Michael Bloomberg during the May 16 cer- An investment fund led by the NBA Hall-of- emony, adding later, “We saw blazing towers go down. -

+1-516-204-7793 Product Catalog

MVP TRADING CO., INC. PRODUCT CATALOG - 2015 TEL: +1-516-204-7793 UNITS CATEGORY UNIT UPC DESCRIPTION PER CASE ACNE AIDS 724742007614 ALBA ACNE FACE/BDY WASH 8 OZ 6 ACNE AIDS 724742007638 ALBA DEEP CLEAN ACNE WASH 6 OZ 6 ACNE AIDS 724742007607 ALBA PORE ACNE WASH 6 OZ 6 ACNE AIDS 654749453872 AVALON BALANCING TONER 8.5 OZ 6 ACNE AIDS 724742003623 AVALON HONEY MANGO GEL 12OZ 12 ACNE AIDS 839977008012 CLEARASIL .65OZ ADULT CARE CRM 24 ACNE AIDS 839977005356 CLEARASIL 6.5OZ HYDRA O/F SENS 12 ACNE AIDS 39977005343 CLEARASIL 6.5OZ HYDRA O/F WASH 12 ACNE AIDS 839977009200 CLEARASIL ULT D/P CLN PADS 90'S 6 ACNE AIDS 839977005325 CLEARASIL ULT RAP ACT GEL 6.78Z 6 ACNE AIDS 839977009095 CLEARASIL ULT VANISH CREAM 1 OZ 24 ACNE AIDS 839977005073 CLEARASIL ULT WSH/MASK 6.78 OZ 6 ACNE AIDS 839977009224 CLEARASIL ULTRA FACE WASH 6.78Z 12 ACNE AIDS 381370035664 CLN & CLR CLEAR TCH SHEETS 50CT 24 ACNE AIDS 381370033424 CLN & CLR DLY PORE CLNSER 5.5OZ 24 ACNE AIDS 381371020805 CLN & CLR MORN BRST FACE CLNS 8 24 ACNE AIDS 381371020829 CLN & CLR MORN BRST FC SCRB 5Z 24 ACNE AIDS 381371157648 CLN & CLR NT RLX DP CLN FACE 8Z 24 ACNE AIDS 381370033875 CLN & CLR SENS FACIAL CLNR 8 OZ 24 ACNE AIDS 381370039914 CLN & CLR.75OZ ADV ACNE TRTMNT 24 ACNE AIDS 70501116906 NEUT #1169 CLR-PORE OIL CNT 8OZ 24 ACNE AIDS 70501153666 NEUT #15366 OIL-FR ACNE WSH 6OZ 12 ACNE AIDS 70501020036 NEUT #2003 4.2Z RAZ/DEF D/SCRUB 12 ACNE AIDS 70501020135 NEUT #2013 MEN MD LOTION SPF20 12 ACNE AIDS 70501023549 NEUT #2354 ADV ACNE THERAPY SYS 12 ACNE AIDS 70501027004 NEUT #270 ALCOHOL-FR -

Campbell Wholesale Company, Inc. Order Book 6849 E

Campbell Wholesale Company, Inc. Order Book 6849 E. 13th 1104 W. Broadway Tulsa, Oklahoma 74112 Muskogee, Oklahoma 74401 1(800) 722-2359 1(888) 516-2997 (918) 836-8774 (918) 682-6608 Fax: (918) 832-5689 Fax: (918) 686-8182 Customer No.: ________________________________________________ Customer Name: _____________________________________________ Date: _________________________________________________________ Written By: ___________________________________________________ ITEM NO. QTY. DESCRIPTION ITEM NO. QTY. DESCRIPTION _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ _______________________________________ -

Master Candy List

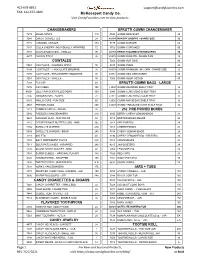

412-678-8851 [email protected] FAX: 412-673-4406 McKeesport Candy Co. Visit CandyFavorites.com to view products. CHANGEMAKERS EFRUTTI GUMMI CHANGEMAKER 7272 ANGEL MINTS 110 4090 GUMMI BRACELET 40 7248 CANDY CIGARETTES 24 42134 BAKERY SHOPPE - SHARE SIZE 12 7171 CARAMEL CREAMS 170 7177 GUMMI BURGER 60 7347 CELLA CHERRY- INDIVIDUALLY WRAPPED 72 3752 GUMMI CUPCAKES 60 7173 CHARLSTON CHEW - VANILLA 96 42133 EFRUTTI GUMMI CHEESECAKES 30 4277 CHICKO STICK 36 40078 GUMMI DONUTS - SHARE SIZE 12 COWTALES 7262 GUMMI HOT DOG 60 5067 COWTALES - CARAMEL APPLE 36 4105 GUMMI PIZZA 48 5304 COWTALES - CHOCOLATE BROWNIE 36 40079 GUMMI RAINBOW UNICORN - SHARE SIZE 12 7270 COWTALES - STRAWBERRY SMOOTHIE 36 63151 GUMMI SEA CREATURES 60 7263 COWTALES - VANILLA 36 7266 GUMMI SOUR GECKO 40 7269 FUN DIP 48 EFRUTTI GUMMI BAGS - LARGE 7275 ICE CUBES 100 43030 GUMMIUNIVERSE SHELF TRAY 12 46001 JOLLY RANCHER FILLED POPS 100 6943 GUMMI LUNCH BAG SHELF TRAY 12 7286 JUNIOR MINTS - BOXES 72 42111 GUMMI LUNCH BAG SOUR TRAY 12 5443 MALLO CUPS - FUN SIZE 60 42008 GUMMI MOVIE BAG SHELF TRAY 12 4848 PRETZEL RODS 450 43203 GUMMI TREASURE HUNT SHELF TRAY 12 7313 PUMPKIN SEEDS - INDIAN 36 25¢ PRE-PRICED BOXES 5040 RAZZLES CHANGEMAKERS 240 3395 BERRY CHEWY LEMONHEADS 24 4423 RAIN-BLO GUM - MINI PACKS 48 4018 BOSTON BAKED BEANS 24 7215 REESE PEANUT BUTTER CUPS - MINI 105 7912 APPLEHEADS 24 7156 SATELLITE WAFERS 240 7913 CHERRYHEADS 24 5089 SATELLITE WAFERS - SOUR 240 5154 CHEWY LEMONHEADS 24 7318 SIXLETS 48 3396 CHEWY LEMONHEADS - REDRIFIC 24 7154 SOFT PEPPERMINT PUFFS -

Gum * Bubble/Kids/Novelty Types- (0200) Gum * Mini Packs

PAGE : 1 SOLD TO CUST NO. DATE : _______________ GUM * BUBBLE/KIDS/NOVELTY TYPES- (0200) 360959 TRIDENT GUM S/F ISLAND BERRY 12/BX 530324 AIRHEAD GUM BL RASPBERRY 14PC 12/BX 360906 TRIDENT GUM S/F MINT BLISS 12/BX 530320 AIRHEAD GUM CHERRY 14 PC 12/BOX 360913 TRIDENT GUM S/F MINT SW TWST 12/BOX 530322 AIRHEAD GUM WATERMELON 14 PC 12/BOX 360951 TRIDENT GUM S/F ORIGINAL 12/BOX 350250 BIG LEAGUE CHEW GRAPE 12/BOX 361003 TRIDENT GUM S/F PASSION FRT 12/BOX 350202 BIG LEAGUE CHEW GIRL 12/BOX 360919 TRIDENT GUM S/F PEPPERMINT 12/BOX 350200 BIG LEAGUE CHEW ORIGINAL 12/BOX 360901 TRIDENT GUM S/F SPEARMINT 12/BOX 350170 BIG LEAGUE CHEW SOUR APPLE 12/BOX 360911 TRIDENT GUM S/F TROPIC TWIST 12/BX 350160 BIG LEAGUE CHEW WATERMELON 12/BOX 360957 TRIDENT GUM S/F WINTERGREEN 12/BOX 350174 BIG LEAGUE CHEW 5-BALL GRAPE 18/BOX 360962 TRIDENT GUM S/F WTR/MLN TWIST 12/BX 350176 BIG LEAGUE CHEW 5-BALL ORIG 18/BX 361031 TRIDENT LAYERS CHERRY + LIME 12/BX 750300 BUBBLE TAPE BUBBLE GUM 24/BOX 361026 TRIDENT LAYERS GRAPE+LEMONADE 12/BX 350400 BUBBLE YUM REGULAR 18/BOX 361020 TRIDENT LAYERS SBERRY/CITRUS 12/BX 350778 BUBBLICIOUS BUBBLE GUM 18/BOX 361035 TRIDENT LAYERS W-MELON/TROPIC 12/BX 350710 BUBBLICIOUS GONZO GRAPE 18/BOX 326001 WRIG "5" ASCENT PTP 10/BX 350900 BUBBLICIOUS S/BERRY SPLASH 18/BOX 326010 WRIG "5" COBALT PTP 10/BX 350950 BUBBLICIOUS WATERMELON 18/BOX 327040 WRIG "5" PRISM WATERMELON PTP 10/BX 351030 HUBBA BUBBA MAX SB/WM 18/BOX 326020 WRIG "5" RAIN PTP 10/BX 351015 HUBBA BUBBA ORIGINAL 18/BOX 328005 WRIG "5" REACT MINT PTP 10/BX 351452 RAINBLO -

Candy, Gum, & Snacks

PAGE : 1 SOLD TO CUST NO. DATE : _______________ GUM * BUBBLE/KIDS/NOVELTY TYPES- (0200) 360957 TRIDENT GUM S/F WINTERGREEN 12/BOX 530324 AIRHEAD GUM BL RASPBERRY 14PC 12/BX 360962 TRIDENT GUM S/F WTR/MLN TWIST 12/BX 530322 AIRHEAD GUM WATERMELON 14 PC 12/BOX 361020 TRIDENT LAYERS SBERRY/CITRUS 12/BX 350250 BIG LEAGUE CHEW GRAPE 12/BOX 361035 TRIDENT LAYERS W-MELON/TROPIC 12/BX 350200 BIG LEAGUE CHEW ORIGINAL 12/BOX 326001 WRIG "5" ASCENT PTP 10/BX 350170 BIG LEAGUE CHEW SOUR APPLE 12/BOX 326010 WRIG "5" COBALT PTP 10/BX 350160 BIG LEAGUE CHEW WATERMELON 12/BOX 327040 WRIG "5" PRISM WATERMELON PTP 10/BX 350176 BIG LEAGUE CHEW 5-BALL ORIG 18/BX 326020 WRIG "5" RAIN PTP 10/BX 350400 BUBBLE YUM REGULAR 18/BOX 328005 WRIG "5" REACT MINT PTP 10/BX 350778 BUBBLICIOUS BUBBLE GUM 18/BOX 328014 WRIG "5" RPM MINT PTP 10/BX 350950 BUBBLICIOUS WATERMELON 18/BOX 327030 WRIG "5" SOUR STRAWBERRY PTP 10/BX 750301 HUBBA BUBBA BUBBLE TAPE 6/BOX 326017 WRIG "5" SWEET MINT MAZE 10/BX 351030 HUBBA BUBBA MAX SB/WM 18/BOX 372032 WRIG EXTRA CINNAMON 10/BOX 351015 HUBBA BUBBA ORIGINAL 18/BOX 373050 WRIG EXTRA CLASSIC BGUM SLIM 10/BOX 351452 RAINBLO TUBE B/GUM 24CT 373040 WRIG EXTRA PEPPERMINT SLIM 10/BOX 354000 SUPER BUBBLE APPLE 300/BOX 372035 WRIG EXTRA POLAR ICE SLIM 10/BOX 353810 SUPER BUBBLE ASST TUB 300/BOX 373044 WRIG EXTRA SMOOTH MINT 10/BOX 353852 SUPER BUBBLE FRUIT 300/TUB 372030 WRIG EXTRA SPEARMINT SLIM 10/BOX 350065 TOPPS BAZOOKA BUBBLE GUM 12/BX 373062 WRIG EXTRA WATERMELON FRTSENS 10/BX 350069 TOPPS BAZOOKA MINI WALLET 12 CT 372028 WRIG EXTRA WINTERFRESH -

1451741361075.Pdf

q i Credits Table of Contents Author: Peter C. Spahn Characters 2 Artwork: Rick Hershey, Jon Gibbons Crime 13 Special Thanks To: Brett M. Bernstein, Mark Miami Nights Tips and Optional Rules 17 Bruno, Alex Hunter, Justin D. Jacobson, Sean Miami Nights Stories 22 Petroff The 1980s 28 Miami 33 Based on the game Vice Squad: 80s Police Episodes 48 Adventures by Mark Bruno and Precis The Deal (sample adventure) 65 Intermedia Character Templates 73 Character Sheet 80 Charts 81 Miami Nights 80s Trivia 83 Vice Squad: Miami Nights is © 2007 by Peter C. Spahn. genreDiversion is a trademark of Precis Intermedia and is used here under license. All rights reserved. No part of this book may be reproduced in any form, except where noted (one copy may be printed for personal use only). WWW.PIGAMES.NET MIAMI NIGHTS Vice Squad: Miami Nights is a genreDiversion add-on that chatting up the ladies and solving crimes, or a corrupt cop focuses on crime in 1980s Miami. Uphold the law as beat looking for the next big bribe. cops, bust drug dealers as vice squad detectives, make the Miami Nights takes you to the crime-ridden streets of streets safe as part of an anti-gang unit, join a S.W.A.T team to Miami where anything is possible. The game is set in 1985, take on heavy-hitters, or play IAD and fight corruption in the however, if you think of something from the late 80s that you department. If law and order are not your thing, play a mafia want to include, feel free to drop it in. -

2021 Virtual Trade Show March 1 - 31, 2021

2021 VIRTUAL TRADE SHOW MARCH 1 - 31, 2021 To Log On To The Show to Place Your Order, Go To: www.tradeshoweasy.com - or - www.gemstatedist.com/trade-show.html HOW TO LOG ON: Username: gem21 - Account # (or chain #) Password: gem21 Index Albanese Confectionary 3 Kind Healthy Snacks 18 American Snuff Co. 3 Kraft Heinz Co. 18 Bazooka Candy Brands 4 Lil Drug Store 19 Blue Diamond Growers 4 Link Industry, Inc 19 Bug Juice International 5 Living Essentials 20 Campbell’s Snacks 5 Mars Wrigley Confections 20 Candy Treasures 6 McCain Foods 21 Casper’s Ice Cream Inc. 6 Mondelez Global 21 Charms Candy Inc. 7 Moringa America 22 Darigold (Up) 7 Nestle Professional 22 Deep River Snacks 8 One Brands, LLC 23 Deli Express 8 Orion/Landmark (Dot) 23 Dr. Pepper Snapple 9 Pearson Candy Company 24 Evans Food Group 9 Pepperidge Farm Inc. 24 F’REAL (Dot) 10 Portland Bee Balm 25 Ferrara Candy Company 10 Quest Nutrition 25 Ferrara Snack 11 Reliva LLC 26 Ferrero USA, Inc. 11 RJ Reynolds 26 Ford Gum 11 Ruby Jewel 27 Foreign Candy Co 12 Ruiz Foods 27 Fun Factory 12 Santa Fe Natural Tobacco 28 General Mills, Inc. 13 Schuster Products 28 Giant Snacks, LLC 13 Smokey Mountain Chew Inc. 29 Grinds LLC. 15 Storck USA, LP 29 Hershey Foods USA 14 Taste of Nature 30 Hostess 15 The Quaker Oats Co. (Spitz) 30 Jack Link’s (Dot) 16 Tootsie Roll Industries 31 JTM Foods 16 Van Holten’s 31 Just Born Inc. 17 Warren Distribution, Inc. 32 Kellogg/Keebler 17 www.gemstatedist.com PAGE 2 • GEM STATE DISTRIBUTORS ALBANESE CONFECTIONARY GUMMI BEARS 1/Each 36 Oz. -

Candy/Gum/Food Items

CANDY/GUM/FOOD ITEMS DESCRIPTION SKU FLC VENDOR NIP ALMOND JOY CANDY BAR KING SZ #5220 CTN/18 893719 751 HERSHEY CHOCOLA 19.71 ALMOND JOY CANDY BARS #0320 CTN OF 36 618033 751 HERSHEY CHOCOLA 22.27 ALTOIDS CINNAMON 1.76 OZ CTN/12 126342 751 DOT FOODS INC 15.77 ALTOIDS PEPPERMINT 1.76 OZ CTN/12 126284 751 DOT FOODS INC 15.77 ALTOIDS SMALLS SF PEPPERMINT CTN/9 698316 751 DOT FOODS INC 6.86 ALTOIDS SMALLS SF WINTERGREEN CTN/9 698340 751 DOT FOODS INC 6.86 ALTOIDS WINTERGREEN 1.76 OZ CTN/12 126276 751 DOT FOODS INC 15.77 ANDES CREME DE MENTHE C/MAKER CTN/72 #12068 777714 751 THE WARRELL COR 15.40 ATOMIC FIREBALLS 5 OZ CS/12 893107 751 TASTE OF NATURE 8.62 BABY RUTH CANDY BAR CTN/24 #01588 875823 751 NESTLE USA INC 14.91 BABY RUTH KING SIZE 2PC BAR CTN/18 825018 751 NESTLE USA INC 19.80 BARNUMS ANIMAL CRACKERS CS/24 #00379 044115 093 MONDELEZ GLOBAL 32.37 BEAR NAKED ENERGY BAR CHOC/CHIP P/B 2 OZ CT/8 119347 093 DOT FOODS INC 7.79 BEAR NAKED ENERGY BAR PEANUT BUTTER 2 OZ CT/8 119354 093 DOT FOODS INC 7.79 BIG LEAGUE CHEW GRAPE CTN/12 #20191 875674 751 THE WARRELL COR 13.42 BIG LEAGUE CHEW OUT HERE ORIGNINAL CT12 20181 875518 751 THE WARRELL COR 13.42 BIT O HONEY 3.5 OZ CS/12 892992 751 TASTE OF NATURE 8.62 BLACK PEPPER 4 OZ 104927 093 JR WATKINS 2.40 BREATH SAVERS PEPPERMINT CTN OF 24 397851 751 HERSHEY CHOCOLA 12.41 BREATH SAVERS WINTERGREEN CTN OF 24 397877 751 HERSHEY CHOCOLA 12.41 BUBBLE GUM STICKS CTN/24 #26983 875682 751 THE WARRELL COR 17.49 BUBBLE YUM REGULAR GUM CTN/18 397653 751 HERSHEY CHOCOLA 7.12 BUBBLICIOUS BUBBLE GUM BX/18 724583 -

Water Rates Jump Durant a 'Rebel with a Cause'

Spott'fored by SUBSCRIBE NOW Grosse Pointe 'Mlb Amu to I Yacht Club GREAT LAKES (313)343-5578 New boats ali sizes/Vmtage Cars, $14.50 OFF THE NEWSSTAND PRICE BOATING FESTIVAL Boats, & Motorcycles/Displays by the Ford House and the M ay 18-20, 2012 Dossin Museum (see page 6 for details) Space Donated by n ? m i l Open In fhe MOTOR ViilAGe G rosse Pointe New s VO L 73, NO. 20,38 PAGES MAY 17,2012 ONE DOLLAR (DELIVERY 7 U) One of America's great community newspapers since 1940 GROSSE POINTE, MICHIGAN Complete news coverage of all the Pointes SAVE with the Grosse Pointe News! Water rates jump By Brad Lindberg StaffW riter W eek ahead GROSSE POINTE FARMS — Water conservation is the main 13 14 15 16 17 18 19 cause of a 19 percent water rate increase. 20 21 22 23 24 25 26 “There’s several factors that came into play,” said John Lamerato, Grosse Pointe Farms THURSDAY, MAY 17 finance director. ♦ The Friends of Grosse The main one is decreased Pointe Pubiic library hold consumption. a book sale from noon to Farms water customers are us 8 p.m. at the Woods HI give ing less water. Consumption is 20 branch, 20680 Mack. percent less since the mid*1990s. ♦ Grosse Pointe Woods “That is a significant drop in and Mack Avenue you a flower the sale of water,” said Business Association hold Councilman Louis Theros, chair sidewalk sales during The 38th annual Beautification man of the finance committee. business hours. Advisory Commission Flower Sale in The overall decrease this year Grosse Pointe Woods brought out is projected to exceed 2.5 per FRIDAY, MAY 18 flower lovers to buy blossoms In con cent, from 68.6- to 66.75-million ♦ Grosse Pointe Theatre tainers, flats and hanging baskets. -

Spring/Summer 2021

760 S. Delsea Drive, PO Box 1447 Vineland, New Jersey 08362-1447 Visit us on the web at: www.ljzucca.com PHONE 856-692-7425 TOLL FREE # 1-800-552-2639 FAX # 800-443-2067 ORDER CATALOG - SPRING/SUMMER 2021 Orders MUST be placed by 3:00 p.m. the day before your scheduled delivery day Customer Number Customer Name Day of delivery Street Address Date of delivery City Taken by ITEM# QTY DESCRIPTION ****ONLINE ORDERING NOW AVAILABLE FOR DELIVERED ORDERS**** Please contact Customer Service for details X 0 A To order catalogs use item number 803205 1-800-934-3968 www.wecard.org Office Hours: 7:00 am - 4:00 pm Monday - Friday Showroom Hours: 8:00 am - noon, 1:00 pm - 4:00 pm Monday - Thursday 8:00 am - noon, 1:00 pm - 3:00 pm Friday RETURN POLICY If an item is received with LESS than the guaranteed shelf life and you believe you will not sell it before the expiration date: Contact our office within 72 hours with the invoice number, item number, quantity, and the code on the received item. The following items may be returned for credit ONLY IF PURCHASED FROM L J ZUCCA in the last 14 days and in original packaging, un-opened, and never stickered. BATTERIES GROCERIES (Case) and (Each) CANDY, GUM, MINTS FULL BOXES PAPER PRODUCTS CIGARETTE PAPERS PLAYING CARDS CIGARETTE TUBES PIPES GLOVES SPORT & TRADING CARDS Credit for the following product categories is divided into four sections FULL CREDIT RESTRICTIONS ANY "NEW" CANDY, NOVELTY, GUM, SNACK ITEM Within 60 days of our initial release CIGARS PACKS KETTLE CHIPS MEAT SNACKS NABISCO CRACKERS & COOKIES TOBACCO CREDIT WITH RESTRICTIONS RESTRICTIONS: BEVERAGE'S If received with LESS than 30 days shelf life CANDY, GUM, CRACKERS OR COOKIES If received with LESS than 30 days shelf life CANDY - HOLIDAY If returned 30 days BEFORE the Holiday CIGAR FULL BOXES Full Boxes, original packaging, un-opened, and never stickered. -

Candy by Decade

Candy From The Candy From 1900’s – 1920’s The 1970’s Abba Zaba Candy by Decade In addition to the candy Baby Ruth Candy From from the prior decades, BB Bat Suckers Candy From someone born in the Beeman’s Gum Continued The 1930’s The 1950’s In addition to the candy 1970’s would also Bit-O-Honey 1900’s – 1920’s In addition to the candy remember these: Black Jack Gum from the prior decades, Life Savers Pep-O-Mint Candy From from the prior decades, Big Red Gum Black Licorice Mary Janes someone born in the 1930’s would also The 1940’s someone born in the Botan Rice Candy Butternger Milk Duds 1950’s would also Candy From Candy Cigarettes remember these: In addition to the candy Bottlecaps Milky Way from the prior decades, remember these: The 1960’s Candy Corn 3 Musketeers Bubble Yum Mounds someone born in the In addition to the candy Bubblicious Caramel Creams Moon Pie 5th Avenue 100 Grand Bar from the prior decades, Cella Cherries 1940’s would also Atomic Fireballs Charms Blow Pops Mountain Bar Big Cherry remember these: someone born in the Charms Boston Baked Beans Big Hunk Freshen Up Gum Mr. Goodbar 1960’s would also Gobstoppers Charms Sour Balls Necco Wafers Candy Buttons Almond Joy Black Licorice Pipes remember these: Charleston Chew Chick-O-Stick Bazooka Bubble Gum Black Tay Gold Mine Gum Snow Caps Banana Splits Hershey’s Special Dark Cherry Cocktail Nut Goodie Chunky Chocolate Cigarettes Candy Necklaces Cherry Mash El Bubble Gum Cigars Cigarettes - Bubble Gum Candy Watches Jelly Belly Jelly Beans Oh Henry! C.