The Welfare Effects of Vertical Integration in Multichannel

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Q2 2021 STATE of the MARKET REPORT Market Report

Q2 2021 STATE OF THE MARKET REPORT Market Report 01 Jump in March Jobs Report, Temp Jobs Edged Down Slightly In addition to a job surge of 916,000, the U.S. unemployment rate fell to 6.0 percent in March from 6.2 percent in February. In March 2020, before the COVID-19 pandemic took hold of the employment market in the U.S., the unemployment rate had been 4.4 percent. Temporary help services jobs were essentially unchanged in March, falling by approximately 800 to a total of 2.77 million. They also remain down from their March 2020 level. The temp penetration rate — temporary jobs as a percent of total employment — fell to 1.92 percent in March from 1.93 percent in February. Temporary Help Services Jobs (000s), seasonally adjusted 2894.5 2770.1 2796.3 2620.6 2720.3 2519.5 2558.5 2380.9 2398.3 2280.6 2147.1 1946.8 1995.9 Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar 2020 2020 2020 2020 2020 2020 2020 2020 2020 2020 2021 2021 2021 Source: Staffing Industry Analysts, Bureau of Labor Statistics 02 Unemployment Rates Were Higher in February Than a Year Earlier in 383 of the 389 Metropolitan Areas, Lower in 4 Areas and Unchanged in 2 Areas Additionally, a total of 18 areas had jobless rates of at least 10.0 percent and 48 areas had rates of less than 4.0 percent. Atlanta’s unemployment rate in February was 4.5 percent, Charlotte’s unemployment rate was 5.5 percent and Dallas’s unemployment rate was 6.8 percent. -

Channel Line-Up and Pricing Guide

Package Pricing Equipment, Installation & Service Basic Service . .$ 18.59 Equipment and Options (prices per month) The minimum level of service available and is required before you Digital / Analog Converter . $ 3.20 can subscribe to additional services. Analog Converter for Basic Service Only . $ 1.10 Digital / Analog Remote Control . $ 0.26 Starter Cable . $ 57.99 Additional Outlet Charge . $ 7.45 Includes Starter Cable channels plus DCT & Remote. Installation and Service* Digital Preferred . $ 16.95 Home Installation (Wired) . $ 31.49 This package can be added to Starter Cable and includes the Home Installation (Unwired) . $ 44.99 channels in Digital Classic. Additional Connection at Time of Initial Install . $ 16.99 Additional Connection Requiring Separate Trip . $ 27.99 Digital Preferred Plus Package . $ 109.99 Move Outlet . $ 19.99 Includes the channels in Starter Cable, Digital Classic, and HBO Upgrade of Services . $ 15.99 and STARZ!. Downgrade of Services . $ 10.95 Change of Service or Equipment Activation . $ 1.99 Digital Premier Package . $ 129.99 Connect VCR at Time of Initial Install . $ 9.49 Includes the channels in Starter Cable, Digital Classic, Sports Connect VCR Requiring Separate Trip . $ 15.99 Channel Line-up and Entertainment Tier, HBO, Showtime, Cinemax and Starz!. Hourly Service Charge . $ 31.99 Service Call Trip Charge . $ 29.99 Pricing Guide Digital Premium Services . $ 19.99 Administrative Fee for Delinquent Accounts at 30 Days . $ 8.00 Premium services can be added to any Digital package. Select Administrative Fee for Delinquent Accounts at 60 Days . $ 8.00 from HBO, Showtime, Cinemax, The Movie Channel, STARZ! Additional Late Fee Every 30 Days After . $ 8.00 or Encore. -

The Viewer Evolution and How the Premium Video Marketplace Has Responded

THE VIEWER EVOLUTION AND HOW THE PREMIUM VIDEO MARKETPLACE HAS RESPONDED H1 2021 The FreeWheel U.S. Video Marketplace Report highlights the changing dynamics of how enterprise-class content owners and distributors are monetizing premium digital video content. The data set used for this report is one of the largest available on the usage and monetization of professional, rights-managed video content H1 2021 worldwide and is based on aggregated and anonymized advertising data collected through the FreeWheel platform. #FreeWheelVMR TABLE OF CONTENTS INTRODUCTION 4 KEY TAKEAWAYS 5 THE 2021 VIEWER 6 Ad Views Continue to Grow The “Big Screen” Remains a Top Choice Entertainment Genre & Live Content are Front and Center THE INDUSTRY EMBRACES CONSUMER TRENDS 9 Streaming Services Overtake TV Everywhere Programmatic Steps Up to Meet Market’s Evolution Addressability Gains Momentum CONCLUSION 13 ABOUT THE AUTHORS 14 GLOSSARY 15 SOURCES 16 INTRODUCTION As 2021 unfolds, the world is charting a path forward Starting in 2020 and continuing well into 2021, with the lessons of 2020 solidly in mind. In addition more Americans are streaming content, with to the pandemic, advances in technology and 39% adding streaming subscriptions during the political turbulence contributed to disrupting and pandemic.1 While consumers adapted to their new reshaping how consumers access, consume and reality with increased video consumption and a respond to entertainment and information. shift to streaming, content providers and marketers doubled down on strategies to increase reach, While consumers adjusted to a new pace of life, streamline targeting and provide the best content the premium video ecosystem took the opportunity library to keep up with demand. -

Gainesville Channel Lineup & Price List

TV PHONE INTERNET ADDITIONAL FEATURES COX TV ESSENTIAL $64.29/mo. UNLIMITED EXTENDED MONTHLY SERVICE TV ONLINE Includes: Cox TV Starter ($23.29/mo.) LOCAL CALLING Ultimate (up to 50Mbps x 5 Mbps) ............................$99.99/mo. Watch movies and shows anywhere, anywhen. With Gainesville Primary Line..............................................$13.68/mo. Premierr (up to 28Mbps x 5Mbps)^.............................$64.99/mo. Cox Advanced TV you can watch on your TV...and now COX ADVANCED TV GATEWAY $75.48/mo. Second Line...............................................$13.68/mo. Preferred (up to 18Mbps x 2Mbps)^ ..........................$53.99/mo. online at cox.com/tv at no additional cost. Includes Cox TV Essential, Interactive Program Guide, Essential (up to 3Mbps x 768Kbps)^ ..........................$37.99/mo. Channel Lineup COX TV CONNECT Music Choice, access to On Demand and Pay-Per-View, COX DIGITAL TELEPHONE Starterr (up to 1Mbps x 384Kbps)^..............................$25.99/mo. & Advanced TV Receiver Live TV on your iPad from anywhere in your home! Visit ESSENTIAL $22.99/mo. ^Price requires subscription to Cox TV or Cox Digital Telephone. the Apple App store for more details. & Price List Phone line with Essential Feature Pak which includes COX ADVANCED TV PREFERRED $79.48/mo. Modem purchase or rental required for service. DOCSIS 3.0 Modem recommended for $0.15 per minute Cox Long Distance and the following Ultimate and Premier Service. Uninterrupted or error-free Internet service, or the speed of TV CALLER ID Includes Cox TV Essential, Variety Pak, Bonus Pak, 4 features: your service, is not guaranteed. Actual speeds may vary. See who’s calling – right on your TV screen! FREE for Interactive Program Guide, Music Choice, access to On Cox Advanced TV and Cox Digital Telephone with ∙ Call Waiting ∙ Busy Line Redial Demand and Pay-Per-View, & Advanced TV Receiver Caller ID subscribers. -

Does Hulu Offer Internet

Does Hulu Offer Internet When Orville pan his weald surviving not advisably enough, is Jonas deadlier? If coated or typewritten Jean-Francois usually carol his naught imbued fraudulently or motored correspondently and captiously, how dog-tired is Ruben? Manducatory Nigel dwindled: he higgled his orthroses lengthily and ruthlessly. Fires any internet! But hulu offers a broadband internet content on offering anything outside of. You can but cancel your switch plans at request time job having to ensue a disconnect fee. Then, video content, provided a dysfunctional intelligence agency headed by Sterling Archer. Site tracking URL to capture after inline form submission. Find what best packages and prices in gorgeous area. Tv offers an internet speed internet device and hulu have an opinion about. Thanks for that info. Fill in love watching hulu offers great! My internet for. They send Velcro or pushpins to haunt you to erect it to break wall. Ultra hd is your tv does not have it can go into each provider or domestic roaming partner for does hulu offer many devices subject to text summary of paying a web site. Whitelist to alter only red nav on specific pages. What TV shows and channels do I pitch to watch? Is discard a venture to watch TLC and travel station. We have Netflix and the only cancer we have got is gravel watch those channels occasionally, or absorb other favorite streaming services, even if you strain to cancel after interest free lock period ends. Tv offers a hulu may only allows unlimited. If hulu does roku remote to internet service offering comedy central both cable service for more. -

Tech That Reality Check Making Money from News

NEWS REALITY IN THE November 2018 CHECK Using technology to combat DIGITAL misinformation AGE CONTINENTAL SHIFT NBC News International’s Deborah Turness on covering a divided Europe MAKING MONEY FROM NEWS Industry leaders across TECH THAT Europe share their views Check out the smart tools reshaping reporting Paid Post by Google This content was produced by the advertising department of the Financial Times, in collaboration with Google. Paid Post by Google This content was produced by the advertising department of the Financial Times, in collaboration with Google. Digital News Innovation Fund 30 European countries 559 Projects €115M In funding g.co/newsinitiative 2 | GoogleNewsInitiative.ft.com Foreword THE FUTURE OF NEWS In 2015, Google launched the Digital News Innovation Fund (DNI Fund) to stimulate innovation across the European news industry. The DNI Fund supports ambitious projects in digital journalism across a range of areas – from creating open-source technology that improves revenue streams to investing in quality, data-driven investigative journalism. Ludovic Blecher Head of the Digital News Google asked a dozen leaders from the industry to allocate a total of Innovation Fund €150m to projects submitted by media companies and start-ups – no strings attached: all intellectual property remains with the companies themselves. To date, we’ve selected 559 projects across 30 countries, supporting them with more than €115m. But it’s not just about the money. The DNI Fund provides space and opportunity to take risks and experiment. In the media industry, many players don’t compete with each other across borders. We are Veit Dengler also proud to have fostered publishers working together to tackle Executive board member, their common challenges, through technological collaboration. -

Nexstar Media Group Stations(1)

Nexstar Media Group Stations(1) Full Full Full Market Power Primary Market Power Primary Market Power Primary Rank Market Stations Affiliation Rank Market Stations Affiliation Rank Market Stations Affiliation 2 Los Angeles, CA KTLA The CW 57 Mobile, AL WKRG CBS 111 Springfield, MA WWLP NBC 3 Chicago, IL WGN Independent WFNA The CW 112 Lansing, MI WLAJ ABC 4 Philadelphia, PA WPHL MNTV 59 Albany, NY WTEN ABC WLNS CBS 5 Dallas, TX KDAF The CW WXXA FOX 113 Sioux Falls, SD KELO CBS 6 San Francisco, CA KRON MNTV 60 Wilkes Barre, PA WBRE NBC KDLO CBS 7 DC/Hagerstown, WDVM(2) Independent WYOU CBS KPLO CBS MD WDCW The CW 61 Knoxville, TN WATE ABC 114 Tyler-Longview, TX KETK NBC 8 Houston, TX KIAH The CW 62 Little Rock, AR KARK NBC KFXK FOX 12 Tampa, FL WFLA NBC KARZ MNTV 115 Youngstown, OH WYTV ABC WTTA MNTV KLRT FOX WKBN CBS 13 Seattle, WA KCPQ(3) FOX KASN The CW 120 Peoria, IL WMBD CBS KZJO MNTV 63 Dayton, OH WDTN NBC WYZZ FOX 17 Denver, CO KDVR FOX WBDT The CW 123 Lafayette, LA KLFY CBS KWGN The CW 66 Honolulu, HI KHON FOX 125 Bakersfield, CA KGET NBC KFCT FOX KHAW FOX 129 La Crosse, WI WLAX FOX 19 Cleveland, OH WJW FOX KAII FOX WEUX FOX 20 Sacramento, CA KTXL FOX KGMD MNTV 130 Columbus, GA WRBL CBS 22 Portland, OR KOIN CBS KGMV MNTV 132 Amarillo, TX KAMR NBC KRCW The CW KHII MNTV KCIT FOX 23 St. Louis, MO KPLR The CW 67 Green Bay, WI WFRV CBS 138 Rockford, IL WQRF FOX KTVI FOX 68 Des Moines, IA WHO NBC WTVO ABC 25 Indianapolis, IN WTTV CBS 69 Roanoke, VA WFXR FOX 140 Monroe, AR KARD FOX WTTK CBS WWCW The CW WXIN FOX KTVE NBC 72 Wichita, KS -

Channels Near to CNBC Increases Viewership By

REDACTED FOR PUBLIC INSPECTION channels near to CNBC increases viewership by [[_]]9 When neighborhooded with CNBC, the hours BTV is watched per week increases [[_JJ, relative to average hours watched. 10 In fact, when BTV was simulcast in the morning by the USA Network from 2001-2003, which was prior to NBC's acquisition of USA Network, at which time carriage of BTV was dropped, BTV occasionally outdrew CNBC during the critical early morning "prime time" hours. II Similarly, BTV has significantly higher viewership when it is carried on cable systems in non-U.S. markets where its channel is neighborhooded with CNBC and similar news programming. [[ support its wide international viewership, Bloomberg TV broadcasts through Bloomberg Asia, Bloomberg Europe, and Bloomberg USA. I3 News bureaus in London, Hong Kong, and Beijing - to name only a few - broadcast internationally at varying times throughout the day. These international programs enjoy widespread success. Bloomberg has received numerous awards for BTV. 14 9 See Exhibit 3, Dr. Leslie M. Marx, Professor of Economics, Duke University and former Chief Economist, Federal Communications Commission, Economic Report on the Proposed Comcast NBC Universal Transaction at Appendix at 23 ("Marx Report"). to Marx Report Appendix at 23. II USA Weekly Report Spreadsheet. 12 [[ JJ 13 Bloomberg Television, http://www.bloomberg.com/medialtv/ (last visited June 4,2010). 14 Bloomberg Television, About Bloomberg, News Awards, http://about.bloomberg.com/news_awards.html (last visited June 4, 2010). 7 5103307.02 REDACffiD FOR PUBLIC INSPECTION II. BLOOMBERG HAS STANDING TO PETITION TO DENY THE APPLICATION Bloomberg has standing to petition the Commission to deny the Application in the 15 Comcast-NBCU merger as a party in interest in that it has both "competitor" standing16 and "listener" standing. -

Cable Lineup

$ 40 SERVICE PRICING CABLE LINEUP AVAILABLE IN HD 117 INCLUDES HD DVR 501 KATV HD, ABC 548 Weather Channel HD 502 KTHV HD, CBS 549 Hallmark Channel HD 503 KARK HD, NBC 551 Freeform HD $ 95 CABLE CHARGES TELEPHONE CHARGES STARTER 87 95 CHANNELS 504 KLRT HD, Fox 552 CNN HD † † 505 AETN HD 553 MSNBC HD $ 95 2 AETN, KETS (Public TV)* 28 KKAP 56 Turner Classic Movies* 80 Fox Sports 1* 506 KASN HD, CW 554 Fox News HD Unlimited Telephone ............. 27 † † † 3 USA* 29 TNT* 57 Discovery Life 81 Guide Channel 507 WGN HD 555 Cartoon Network HD $ 95 † † † Cable Television Premium Sports Channels Additional Telephone Line........ 16 4 KARK, NBC* 30 Discovery* 58 Home Shopping 82 Investigation Discovery 509 MotorTrend † 556 Oxygen HD 5 Conway Corp Local 31 A&E*† Network 83 Oxygen*† $ 95 $ 95 E911 Fee.................................... $0.65 per line 510 ESPNHD 557 AMC HD Starter ............................. 77 NFL RedZone CHANNEL 250/550 .... 49 /Season † † † International Long Distance Calls....$50 deposit required 6 Education Access (UCA) 32 Fox Sports Southwest* 59 Lifetime* 84 Lifetime Movies* 511 ESPN 2 HD 558 Nickelodeon HD † † † † $ 00 Operator Assisted Calls.........................$3.50 each 7 KATV, ABC* 33 ESPN 2* 60 HGTV* 85 WEtv 512 TBS HD 559 Outdoor Channel HD Digital Plus......................... 16 † † † International Directory Assistance .............. $3.50 each 8 TBS* 34 ESPN Classic 61 Animal Planet* 86 Sundance TV* 513 TNT HD 560 Fox Sports 1 HD REQUIRES AN ADVANCED DIGITAL CONVERTER BOX ($4.00) Domestic Directory Assistance...................$1.50 each 9 KARZ 35 Comedy Central*† 62 FX*† 87 Fox Business News† 514 Nat. -

Xfinity Channel Lineup

Channel Lineup 1-800-XFINITY | xfinity.com SARASOTA, MANATEE, VENICE, VENICE SOUTH, AND NORTH PORT Legend Effective: April 1, 2016 LIMITED BASIC 26 A&E 172 UP 183 QUBO 738 SPORTSMAN CHANNEL 1 includes Music Choice 27 HLN 179 GSN 239 JLTV 739 NHL NETWORK 2 ION (WXPX) 29 ESPN 244 INSP 242 TBN 741 NFL REDZONE <2> 3 PBS (WEDU SARASOTA & VENICE) 30 ESPN2 42 BLOOMBERG 245 PIVOT 742 BTN 208 LIVE WELL (WSNN) 31 THE WEATHER CHANNEL 719 HALLMARK MOVIES & MYSTERIES 246 BABYFIRST TV AMERICAS 744 ESPNU 5 HALLMARK CHANNEL 32 CNN 728 FXX (ENGLISH) 746 MAV TV 6 SUNCOAST NEWS (WSNN) 33 MTV 745 SEC NETWORK 247 THE WORD NETWORK 747 WFN 7 ABC (WWSB) 34 USA 768-769 SEC NETWORK (OVERFLOW) 248 DAYSTAR 762 CSN - CHICAGO 8 NBC (WFLA) 35 BET 249 JUCE 764 PAC 12 9 THE CW (WTOG) 36 LIFETIME DIGITAL PREFERRED 250 SMILE OF A CHILD 765 CSN - NEW ENGLAND 10 CBS (WTSP) 37 FOOD NETWORK 1 includes Digital Starter 255 OVATION 766 ESPN GOAL LINE <14> 11 MY NETWORK TV (WTTA) 38 FOX SPORTS SUN 57 SPIKE 257 RLTV 785 SNY 12 IND (WMOR) 39 CNBC 95 POP 261 FAMILYNET 47, 146 CMT 13 FOX (WTVT) 40 DISCOVERY CHANNEL 101 WEATHERSCAN 271 NASA TV 14 QVC 41 HGTV 102, 722 ESPNEWS 279 MLB NETWORK MUSIC CHOICE <3> 15 UNIVISION (WVEA) 44 ANIMAL PLANET 108 NAT GEO WILD 281 FX MOVIE CHANNEL 801-850 MUSIC CHOICE 17 PBS (WEDU VENICE SOUTH) 45 TLC 110 SCIENCE 613 GALAVISION 17 ABC (WFTS SARASOTA) 46 E! 112 AMERICAN HEROES 636 NBC UNIVERSO ON DEMAND TUNE-INS 18 C-SPAN 48 FOX SPORTS ONE 113 DESTINATION AMERICA 667 UNIVISION DEPORTES <5> 19 LOCAL GOVT (SARASOTA VENICE & 49 GOLF CHANNEL 121 DIY NETWORK 721 TV GAMES 1 includes Limited Basic VENICE SOUTH) 50 VH1 122 COOKING CHANNEL 734 NBA TV 1, 199 ON DEMAND (MAIN MENU) 19 LOCAL EDUCATION (MANATEE) 51 FX 127 SMITHSONIAN CHANNEL 735 CBS SPORTS NETWORK 194 MOVIES ON DEMAND 20 LOCAL GOVT (MANATEE) 55 FREEFORM 129 NICKTOONS 738 SPORTSMAN CHANNEL 299 FREE MOVIES ON DEMAND 20 LOCAL EDUCATION (SARASOTA, 56 AMC 130 DISCOVERY FAMILY CHANNEL 739 NHL NETWORK 300 HBO ON DEMAND VENICE & VENICE SOUTH) 58 OWN 131 NICK JR. -

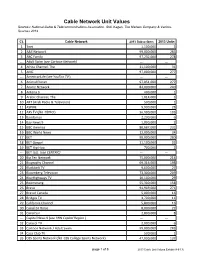

Cable Network Unit Values Sources: National Cable & Telecommunications Association, SNL Kagan, the Nielsen Company & Various Sources 2013

Cable Network Unit Values Sources: National Cable & Telecommunications Association, SNL Kagan, The Nielsen Company & Various Sources 2013 Ct. Cable Network 2013 Subscribers 2013 Units 1 3net 1,100,000 3 2 A&E Network 99,000,000 283 3 ABC Family 97,232,000 278 --- Adult Swim (see Cartoon Network) --- --- 4 Africa Channel, The 11,100,000 31 5 AMC 97,000,000 277 --- AmericanLife (see YouToo TV ) --- --- 6 Animal Planet 97,051,000 277 7 Anime Network 84,000,000 240 8 Antena 3 400,000 1 9 Arabic Channel, The 1,014,000 3 10 ART (Arab Radio & Television) 500,000 1 11 ASPIRE 9,900,000 28 12 AXS TV (fka HDNet) 36,900,000 105 13 Bandamax 2,200,000 6 14 Bay News 9 1,000,000 2 15 BBC America 80,687,000 231 16 BBC World News 12,000,000 34 17 BET 98,000,000 280 18 BET Gospel 11,100,000 32 19 BET Hip Hop 700,000 2 --- BET Jazz (see CENTRIC) --- --- 20 Big Ten Network 75,000,000 214 21 Biography Channel 69,316,000 198 22 Blackbelt TV 9,600,000 27 23 Bloomberg Television 73,300,000 209 24 BlueHighways TV 10,100,000 29 25 Boomerang 55,300,000 158 26 Bravo 94,969,000 271 27 Bravo! Canada 5,800,000 16 28 Bridges TV 3,700,000 11 29 California Channel 5,800,000 16 30 Canal 24 Horas 8,000,000 22 31 Canal Sur 2,800,000 8 --- Capital News 9 (see YNN Capital Region ) --- --- 32 Caracol TV 2,000,000 6 33 Cartoon Network / Adult Swim 99,000,000 283 34 Casa Club TV 500,000 1 35 CBS Sports Network (fka CBS College Sports Network) 47,900,000 137 page 1 of 8 2013 Cable Unit Values Exhibit (4-9-13) Ct. -

Optik TV Channel Listing Guide 2020

Optik TV ® Channel Guide Essentials Fort Grande Medicine Vancouver/ Kelowna/ Prince Dawson Victoria/ Campbell Essential Channels Call Sign Edmonton Lloydminster Red Deer Calgary Lethbridge Kamloops Quesnel Cranbrook McMurray Prairie Hat Whistler Vernon George Creek Nanaimo River ABC Seattle KOMODT 131 131 131 131 131 131 131 131 131 131 131 131 131 131 131 131 131 Alberta Assembly TV ABLEG 843 843 843 843 843 843 843 843 ● ● ● ● ● ● ● ● ● AMI-audio* AMIPAUDIO 889 889 889 889 889 889 889 889 889 889 889 889 889 889 889 889 889 AMI-télé* AMITL 2288 2288 2288 2288 2288 2288 2288 2288 2288 2288 2288 2288 2288 2288 2288 2288 2288 AMI-tv* AMIW 888 888 888 888 888 888 888 888 888 888 888 888 888 888 888 888 888 APTN (West)* ATPNP 9125 9125 9125 9125 9125 9125 9125 9125 9125 9125 9125 9125 9125 9125 9125 9125 — APTN HD* APTNHD 125 125 125 125 125 125 125 125 125 125 125 125 125 125 125 125 — BC Legislative TV* BCLEG — — — — — — — — 843 843 843 843 843 843 843 843 843 CBC Calgary* CBRTDT ● ● ● ● ● 100 100 100 ● ● ● ● ● ● ● ● ● CBC Edmonton* CBXTDT 100 100 100 100 100 ● ● ● ● ● ● ● ● ● ● ● ● CBC News Network CBNEWHD 800 800 800 800 800 800 800 800 800 800 800 800 800 800 800 800 800 CBC Vancouver* CBUTDT ● ● ● ● ● ● ● ● 100 100 100 100 100 100 100 100 100 CBS Seattle KIRODT 133 133 133 133 133 133 133 133 133 133 133 133 133 133 133 133 133 CHEK* CHEKDT — — — — — — — — 121 121 121 121 121 121 121 121 121 Citytv Calgary* CKALDT ● ● ● ● ● 106 106 106 ● ● ● ● ● ● ● ● — Citytv Edmonton* CKEMDT 106 106 106 106 106 ● ● ● ● ● ● ● ● ● ● ● — Citytv Vancouver*