2008 Series C-1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sep 02 1992 Ubraries the New York World Trade Center: a Performance Study

THE NEW YORK WORLD TRADE CENTER: A PERFORMANCE STUDY by Andrew F. Fusscas B.S. Business Administration University of California, Berkeley 1987 Submitted to the Department of Urban Studies and Planning in Partial Fulfillment of the Requirements for the degree of MASTER OF SCIENCE in Real Estate at the Massachusetts Institute of Technology September, 1992 *Andrew F. Fusscas, 1992 All rights reserved. The author hereby grants to MIT permission to reproduce and to distribute publicly copies of this thesis document in whole or in part. Signature of author............ - - - - -r--v-1 . - - . - L - - - - Department of Urban Studies and Planning July 31, 1992 Certified by ................ Lawrence Bacow Department of Urban Studies and Planning Thesis Supervisor Accepted by................ Lawrence Bacow Chairman Interdepartmental Degree Program in Real Estate Development MASSACHUSETTS INSTITUTE OF TECHNOLOGY SEP 02 1992 UBRARIES THE NEW YORK WORLD TRADE CENTER: A PERFORMANCE STUDY by Andrew F. Fusscas Submitted to the Department of Urban Studies and Planning, in partial fulfillment of the Degree of Master of Science in Real Estate ABSTRACT This thesis represents a study of the New York World Trade Center. It was written in conjunction with four other papers studying World Trade Centers (WTCs) sites in Taipei, Amsterdam, Curacao and Portland (Oregon). These sites represent a cross-section of the various trade and economic environments that World Trade Centers operate in around the globe. Each of these studies examines the extent to which the owner/developer, the tenants and other regional public and private concerns have benefitted through their involvement with these highly specialized real estate developments. The New York World Trade Center is unique from all other World Trade Centers in several respects. -

General Info.Indd

General Information • Landmarks Beyond the obvious crowd-pleasers, New York City landmarks Guggenheim (Map 17) is one of New York’s most unique are super-subjective. One person’s favorite cobblestoned and distinctive buildings (apparently there’s some art alley is some developer’s idea of prime real estate. Bits of old inside, too). The Cathedral of St. John the Divine (Map New York disappear to differing amounts of fanfare and 18) has a very medieval vibe and is the world’s largest make room for whatever it is we’ll be romanticizing in the unfinished cathedral—a much cooler destination than the future. Ain’t that the circle of life? The landmarks discussed eternally crowded St. Patrick’s Cathedral (Map 12). are highly idiosyncratic choices, and this list is by no means complete or even logical, but we’ve included an array of places, from world famous to little known, all worth visiting. Great Public Buildings Once upon a time, the city felt that public buildings should inspire civic pride through great architecture. Coolest Skyscrapers Head downtown to view City Hall (Map 3) (1812), Most visitors to New York go to the top of the Empire State Tweed Courthouse (Map 3) (1881), Jefferson Market Building (Map 9), but it’s far more familiar to New Yorkers Courthouse (Map 5) (1877—now a library), the Municipal from afar—as a directional guide, or as a tip-off to obscure Building (Map 3) (1914), and a host of other court- holidays (orange & white means it’s time to celebrate houses built in the early 20th century. -

TM 3.1 Inventory of Affected Businesses

N E W Y O R K M E T R O P O L I T A N T R A N S P O R T A T I O N C O U N C I L D E M O G R A P H I C A N D S O C I O E C O N O M I C F O R E C A S T I N G POST SEPTEMBER 11TH IMPACTS T E C H N I C A L M E M O R A N D U M NO. 3.1 INVENTORY OF AFFECTED BUSINESSES: THEIR CHARACTERISTICS AND AFTERMATH This study is funded by a matching grant from the Federal Highway Administration, under NYSDOT PIN PT 1949911. PRIME CONSULTANT: URBANOMICS 115 5TH AVENUE 3RD FLOOR NEW YORK, NEW YORK 10003 The preparation of this report was financed in part through funds from the Federal Highway Administration and FTA. This document is disseminated under the sponsorship of the U.S. Department of Transportation in the interest of information exchange. The contents of this report reflect the views of the author who is responsible for the facts and the accuracy of the data presented herein. The contents do no necessarily reflect the official views or policies of the Federal Highway Administration, FTA, nor of the New York Metropolitan Transportation Council. This report does not constitute a standard, specification or regulation. T E C H N I C A L M E M O R A N D U M NO. -

THE VERIZON TELEPHONE COMPANIES TARIFF F.C.C. NO. 21 1St Revised Page 4-1 Cancels Original Page 4-1

THE VERIZON TELEPHONE COMPANIES TARIFF F.C.C. NO. 21 1st Revised Page 4-1 Cancels Original Page 4-1 SPECIAL CONSTRUCTION (D)(x) (S)(y) 4. Verizon New York Inc. Special Construction Cases 4.1 Charges for the State of Connecticut (Company Code 5131) 4.1.1 Special Construction Cases Prior to May 25, 1984 The following cases are subject to the regulations specified in 2.1 through 2.8 preceding, with the following exception. When the initial liability period expires, an annual underutilization charge applies to the difference between 70% of the number of original specially constructed facilities and the number of facilities in service at filed tariff rates at that time. For purposes of determining the underutilization charge, any facilities subject to minimum period monthly charges are considered to be in service at filed tariff rates. There are no special construction cases prior to May 24, 1984 for the State of Connecticut. (S)(y) (D)(x) (x) Filed under authority of Special Permission No. 02-053 of the Federal Communications Commission. (y) Reissued material filed under TR 169, to become effective on April 13, 2002. (TR 176) Issued: April 11, 2002 Effective: April 13, 2002 Vice President, Federal Regulatory 1300 I Street, NW, Washington, D.C. 20005 THE VERIZON TELEPHONE COMPANIES TARIFF F.C.C. NO. 21 8th Revised Page 4-2 Cancels 7th Revised Page 4-2 SPECIAL CONSTRUCTION 4. Verizon New York Inc. Special Construction Cases (Cont'd) 4.1 Charges for the State of Connecticut (Company Code 5131) (Cont'd) 4.1.2 Charges to Provide Permanent Facilities Customer: Greenwich Capital Markets ID# 2003-264110 Description: Special Construction of facilities to provide fiber based telecommunications services at 600 Steamboat Road, Greenwich, CT 06830. -

The Case of New York City's Financial District

INFORMATION TECHNOWGY AND WORLD CITY RESTRUCTURING: THE CASE OF NEW YORK CITY'S FINANCIAL DISTRICT by Travis R. Longcore A thesis submitted to the Faculty of the University of Delaware in partial fulfillment of the requirements for the degree of Honors Bachelor of Arts in Geography May 1993 Copyright 1993 Travis R. Longcore All Rights Reserved INFORMATION TECHNOWGY AND WORLD CITY RESTRUCTURING: THE CASE OF NEW YORK CITY'S FINANCIAL DISTRICT by Travis R. Longcore Approved: Peter W. Rees, Ph.D. Professor in charge of thesis on behalf of the Advisory Committee Approved: Robert Warren, Ph.D. Committee Member from the College of Urban Affairs Approved: Francis X. Tannian, Ph.D. Committee Member from the University Honors Program Approved: Robert F. Brown, Ph.D. Director, University Honors Program "Staccato signals of constant information, A loose affiliation of millionaires and billionaires and baby, These are the days of miracle and wonder. This is a long distance call. " Paul Simon, Graceland iii ACKNOWLEDGEMENTS The author would like to recognize and thank Dr. Peter Rees for his guidance on this project. Without the patient hours of discussion, insightful editorial comments, and firm schedule, this thesis would have never reached completion. The author also thanks the University Honors Program, the Undergraduate Research Program and the Department of Geography at the University of Delaware for their financial support. Many thanks are due to the Water Resources Agency for New Castle County for the use of their automated mapping system. IV TABLE OF CONTENTS LIST OFTABLES .................................... viii LIST OF FIGURES ix ABSTRACT ....................................... .. x Chapter 1 THE CITY IN A WORLD ECONOMY ................... -

Manhattan Office Market

Manhattan Offi ce Market 1 ST QUARTER 2016 REPORT A NEWS RECAP AND MARKET SNAPSHOT Pictured: 915 Broadway Looking Ahead Finance Department’s Tentative Assessment Roll Takes High Retail Rents into Account Consumers are not the only ones attracted by the luxury offerings along the city’s prime 5th Avenue retail corridor between 48th and 59th Streets where activity has raised retail rents. The city’s Department of Finance is getting in on the action, prompting the agency to increase tax assessments on some of the high-profi le properties. A tentative tax roll released last month for the 2016-2017 tax year brings the total market value of New York City’s real estate to over $1 trillion — reportedly for the fi rst time. The overall taxable assessed values for the city would increase 8.10%. Brooklyn’s assessed values accounted for the sharpest rise of 9.83% from FY 2015/2016, followed by Manhattan’s 8.47% increase. Although some properties along the 5th Avenue corridor had a reduction in valuations the properties were primarily offi ce, not retail according to a reported analysis of the tentative tax roll details. Building owners have the opportunity to appeal the increase; but an unexpected rise in market value — and hence real estate taxes, will negatively impact the building’s bottom line and value. Typically tenants incur the burden of most of the tax increases from the time the lease is signed, and the landlord pays the taxes that existed before the signing; but in some cases the tenant increase in capped, leaving the burden of the additional expense on the landlord. -

Daily Referrals 7-19-2021

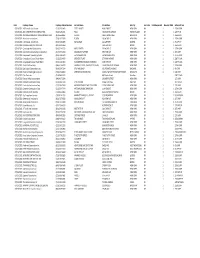

Date Employer Name Employer Phone Number Job Site Name Site Address Site City Site State Total Requested Number Filled Referred From 07/19/2021 A O F Installation Srvs Inc (212) 633‐2400 ESTEE LAUDER 40 W 23RD ST NEW YORK NY 1 1 157W CARP 07/19/2021 ABC CONSTRUCTION CONTRACTING (718) 729‐2501 R024 750 DURANT AVENUE STATEN ISLAND NY 1 1 2287 FC SI 07/19/2021 ADVANCED CONSTRUCTION EQUIPMENT CORP (914) 665‐8383 PS 197K 1599 E 22ND STREET BROOKLYN NY 1 1 1556 SCAFF 07/19/2021 Ashnu International Inc. (718) 267‐7590 PS 87M 160 W 78TH ST NEW YORK NY 1 1 157W CARP 07/19/2021 C D S Mestel Constr Corp (516) 739‐1865 AA HANGAR LGA AIRPORT QUEENS NY 1 1 45 APP‐CP 07/19/2021 CARLITOS CONTRACTING CORP (929) 499‐5654 150 E 149TH ST BRONX NY 1 1 1556 SCAFF 07/19/2021 Cavanaugh Wall Solutions Inc. (610) 524‐5353 MTA THEATER 254 W 54TH ST NEW YORK NY 1 1 157W CARP 07/19/2021 Commodore Construction Corporation (914) 297‐3000 MILLENIUM PARTNERS 399 PARK AVE NEW YORK NY 1 1 157 CARP 07/19/2021 Component Assembly Systems (914) 738‐5400 550 WASHINGTON 550 WASHINGTON ST NEW YORK NY 1 1 157W CARP 07/19/2021 Consolidated Carpet Trade Wkrm (212) 226‐4600 SPENCER STUART 277 PARK AVENUE NEW YORK NY 1 1 2287 FC MA 07/19/2021 Consolidated Carpet Trade Wkrm (212) 226‐4600 GUGGENHEIM MUSEUM ROTUNDA 1071 5TH AVE NEW YORK NY 1 1 2287 FC MA 07/19/2021 Curtis Partition Corp (646) 315‐6700 LINCOLN CENTER ‐ DAVID GEFFEN HALL 10 LINCOLN CENTER PLAZA NEW YORK NY 4 2 157W CARP 07/19/2021 Dgc Capital Contracting Corp. -

Manhattan Office Market

Manhattan Offi ce Market 2 ND QUARTER 2015 REPORT A NEWS RECAP AND MARKET SNAPSHOT Pictured: 1001 Avenue of the Americas Looking Ahead Partnership for New York City: New York’s Future as the World Financial Capital The report released in June concluded that while New York City remains the preferred location of global fi nancial companies to establish their headquarters, there is a growing trend to relocate jobs and business operations to lower cost, more business-friendly locations that are beyond the city’s border. A comprehensive survey was conducted in collaboration with Gerson Lehrman Group (GRG), intending to better understand how the fi nancial industry is evolving; and what measures are required to solidify New York’s competitive advantage as a global fi nancial center. Collected data represents an overview of the responses from 50-fi rm respondents that included large banks, insurance companies and asset managers, private equity fi rms, hedge funds, and fi nancial technology (FinTech) startups; and represent about 1/3rd of the total industry employment in the city. Additionally, observations were included from 8-real estate fi rms that were surveyed; along with interviews from other related experts in the fi eld. Financial Industry – an economic snapshot • Contributes 20% of the city’s economic output, representing twice that of the next top-grossing industry. • Accounts for nearly 1/3rd of the city’s private sector payroll, despite accounting for only 8%, or about 310,000 of the city’s private sector jobs in 2013; of which 23,000 jobs are high-technology in the areas of software, data processing and network management. -

Major Projects Update

EMPLOYMENT & OFFICE RETAIL TOURISM & HOSPITALITY RESIDENTIAL MAJOR PROJECTS UPDATE ALLIANCE FOR DOWNTOWN NEW YORK LOWER MANHATTAN REAL ESTATE MARKET OVERVIEW Q2 2016 COMMERCIAL OFFICE MARKET Lower Manhattan’s commercial market sent mixed signals through the second quarter of 2016, echoing trends also seen in other Private Sector Employment submarkets. Office leasing was on par with activity last year but still below the historical average, and news of new major tenant Total Private relocations remained quiet. Despite this, there were clear areas 232,200 Sector Workers of strength. The vacancy rate is currently below 10 percent, and key Lower Manhattan companies committed to stay or expand Additional Workers in new locations south of Chambers Street. The arrival of new 5,100 Year Over Year commercial tenants and the opening of hotels and retail has pushed Lower Manhattan’s private sector employment to grow, workers or 2% growth year over year. The employment expansion reaching a new post-2001 peak of more than 232,000 employees cuts across all the key sectors that have been fueling Lower 1 as of the end of 2015. Manhattan’s economy and leasing activity. EMPLOYMENT The hotel, retail and restaurant sectors added the largest share of employees to Lower Manhattan over the course of 2015. These Private sector employment climbed to nearly 232,200 employees as industries grew by more than 2,000 employees or 10%. More than of the end of 2015, marking the sixth consecutive year of growth and 58 stores and restaurants were added to the retail market, including the highest point since Lower Manhattan had 236,700 private sector Brookfield Places’ offerings as well as three hotels with over 433 rooms.2 employees at the end of 2001. -

Magnum, CIM Take $390M for Verizon Building Condo Conversion

The Insider’s Weekly Guide to the Commercial Mortgage Industry In This Issue 1 Magnum, CIM Take $390M for Verizon Building Condo Conversion 1 HFZ Scores $185M From Mexican Bank to Revamp South Beach Hotel 3 Steiner’s Brooklyn Residential Tower Gets $390M Construction Loan 4 Now Is Not Prime Time on the CMBS Channel 5 FHA and HUD to Undergo Further Revamp, Fannie Mae Unfazed 6 Chetrit Closes on $191.9M Purchase of Hotel Carter With $150M From Athene Annuity 7 Bancorp Provides 80 Percent LTC Acquisition Loan to Blue Rock And Partner “Though underwriting has clearly loosened up since the financial crisis, there is still a floor on how aggressive lenders will be” —Drew Anderman From Q&A on page 12 Magnum, CIM Take $390M HFZ Scores $185M for Verizon Building From Mexican Bank Condo Conversion to Revamp South Beach Hotel HFZ Capital refinanced The Shore Club, A partnership of Ben Shaoul and Los been rebranded as 100 Barclay Street. a luxury hotel in Miami’s South Beach neigh- Angeles-based CIM Group closed on a $390 The units will be built in the top 22 floors of borhood, Mortgage Observer Weekly has ex- million loan they will use to convert a Lower the 31-story building, which sits at the corner clusively learned. With the $185 Manhattan office building into of Vesey Street about a block from 1 World MOW million provided by Banco MOW fancy condominiums, Trade Center. EXCLUSIVE Inbursa, the Mexican bank run EXCLUSIVE Mortgage Observer The three-year loan is Libor-based, by Carlos Slim, the hotel will Weekly has learned. -

Lower Manhattan Real Estate Market Review Q1 2019

COMMERCIAL OFFICE RETAIL TOURISM & HOSPITALITY RESIDENTIAL MAJOR PROJECTS UPDATE ALLIANCE FOR DOWNTOWN NEW YORK LOWER MANHATTAN REAL ESTATE MARKET REVIEW Q1 2019 Private-Sector Employment Exceeds Levels Not Seen Since September 2001 Lower Manhattan Year to Date Leasing Activity, Almost eighteen years after September 11, 2001, private-sector 2015 - 2018 employment in Lower Manhattan has rebounded past immediate Source: CBRE pre-9/11 levels, fulfilling the promise to rebuild the neighborhood and reanimate its role as a vibrant and essential commercial district for the city, the state and the nation. According to the latest data from the New York State Department of Labor, Lower Manhattan has reached its highest level of private-sector employment since before September 11th. Strong leasing across industry sectors and in a diverse set of buildings helped push private-sector employment to 251,334, a figure not seen since the third quarter of 2001. Relocations, particularly from Midtown South, continue to drive leasing in Lower Manhattan. Two million square feet of deals helped Lower Manhattan outperform Manhattan’s other submarkets during one of the busiest quarters in seven years. The district’s retail and hospitality markets continued to thrive with new restaurants and hotels opening. Vigorous First Quarter Leasing Activity Two million square feet of new deals were inked in the first quarter. Leasing represented the second highest quarterly total in more than seven years and was 52% above the five-year quarterly average. The strong leasing trend continues the momentum from the end of 2018 when 2.1 million square feet were leased. Lower Manhattan was the only submarket in New York City to register an increase in leasing activity above the five-year quarterly average. -

AGENCY LEASE and AGREEMENT Dated As of June 30, 2016 by And

AGENCY LEASE AND AGREEMENT Dated as of June 30, 2016 by and between NEW YORK CITY INDUSTRIAL DEVELOPMENT AGENCY and LIC SITE B-1 OWNER, L.L.C., a limited liability company organized and existing under the laws of the State of Delaware, having an office at c/o Tishman Speyer, 45 Rockefeller Plaza, 9th Floor, New York, New York 10111, as Lessee New York City Industrial Development Agency 2016 LIC Site B-1 Owner, L.L.C. Project Affecting the Land generally known by the street address 28-10 Queens Plaza South, Queens, New York 11101 Block 420 and Lot 1, in the County of Queens, City and State of New York as more particularly described in Exhibit A to this Agency Lease Agreement on the Official Tax Map of Queens County Record and Return to: Hawkins Delafield & Wood LLP 28 Liberty Street New York, New York 10005 Attention: Arthur M. Cohen, Esq. 2628631.12 040613 AGMT TABLE OF CONTENTS Page ARTICLE I DEFINITIONS AND CONSTRUCTION Section 1.1. Definitions ........................................................................................................... 3 Section 1.2. Construction....................................................................................................... 24 ARTICLE II REPRESENTATIONS AND WARRANTIES Section 2.1. Representations and Warranties by Agency ........................................................ 26 Section 2.2. Representations and Warranties by the Lessee .................................................... 26 ARTICLE III LEASEHOLD INTEREST CONVEYED TO THE AGENCY; THE PROJECT; MAINTENANCE; REMOVAL