South Africa

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

BUILDING from SCRATCH: New Cities, Privatized Urbanism and the Spatial Restructuring of Johannesburg After Apartheid

INTERNATIONAL JOURNAL OF URBAN AND REGIONAL RESEARCH 471 DOI:10.1111/1468-2427.12180 — BUILDING FROM SCRATCH: New Cities, Privatized Urbanism and the Spatial Restructuring of Johannesburg after Apartheid claire w. herbert and martin j. murray Abstract By the start of the twenty-first century, the once dominant historical downtown core of Johannesburg had lost its privileged status as the center of business and commercial activities, the metropolitan landscape having been restructured into an assemblage of sprawling, rival edge cities. Real estate developers have recently unveiled ambitious plans to build two completely new cities from scratch: Waterfall City and Lanseria Airport City ( formerly called Cradle City) are master-planned, holistically designed ‘satellite cities’ built on vacant land. While incorporating features found in earlier city-building efforts, these two new self-contained, privately-managed cities operate outside the administrative reach of public authority and thus exemplify the global trend toward privatized urbanism. Waterfall City, located on land that has been owned by the same extended family for nearly 100 years, is spearheaded by a single corporate entity. Lanseria Airport City/Cradle City is a planned ‘aerotropolis’ surrounding the existing Lanseria airport at the northwest corner of the Johannesburg metropole. These two new private cities differ from earlier large-scale urban projects because everything from basic infrastructure (including utilities, sewerage, and the installation and maintenance of roadways), -

MWS Confirmation Package Distribution

20 OCTOBER - 26 OCTOBER 2013 TOURNAMENT CONFIRMATION PACKAGE www.worldindoorcricketfederation.com 01 Dear World Indoor Cricket Federation participants I would like to extend a warm South African welcome to all players, managers and officials taking part in the Indoor Cricket Masters World Series 2013. The tournament will take place in the Gauteng province which can be considered as the sporting hub of the African continent. South Africa has played host to a few major sporting world cups in the past, the largest three being the Soccer, Cricket and Rugby world cups, so we have developed a reputation for hosting fantastic international Indoor Cricket events. Gauteng Province is situated a stone throw away from some of the most spectacular tourist destinations we have, so visiting some of these before or after the tournament would be an experience not to be missed. There are a host of game reserves within a 3 hour drive where you could get a true experience of the famous African Bushveld. There you would be able to see the “big 5” which are the Lion, Elephant, Rhino, Leopard and Buffalo, in their natural environment. We will also be situated two hours away from Sun City, South Africa’s version of Las Vegas. Sun City is best known for playing host to the $2 mill golf tournament, five star hotels and casino’s all nestled into the Pilandsberg game reserve where you will also find the “Big 5”. Indoor Cricket or “Action Cricket” as it is better known in South Africa is one of the fastest growing sports in this sport mad country. -

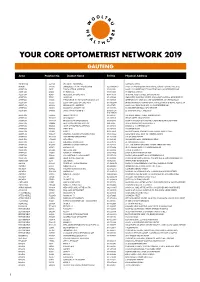

Your Core Optometrist Network 2019 Gauteng

YOUR CORE OPTOMETRIST NETWORK 2019 GAUTENG Area Practice No. Doctor Name Tel No. Physical Address ACTONVILLE 456640 JHETAM N - ACTONVILLE 1539 MAYET DRIVE AKASIA 478490 ENGELBRECHT A J A - WONDERPARK 012 5490086/7 SHOP 404 WONDERPARK SHOPPING C, CNR OF HEINRICH AVE & OL ALBERTON 58017 TORGA OPTICAL ALBERTON 011 8691918 SHOP U 142, ALBERTON CITY SHOPPING MALL, VOORTREKKER ROAD ALBERTON 141453 DU PLESSIS L C 011 8692488 99 MICHELLE AVENUE ALBERTON 145831 MEYERSDAL OPTOMETRISTS 011 8676158 10 HENNIE ALBERTS STREET, BRACKENHURST ALBERTON 177962 JANSEN N 011 9074385 LEMON TREE SHOPPING CENTRE, CNR SWART KOPPIES & HEIDELBERG RD ALBERTON 192406 THEOLOGO R, DU TOIT M & PRINSLOO C M J 011 9076515 ALBERTON CITY, SHOP S03, CNR VOORTREKKER & DU PLESSIS ROAD ALBERTON 195502 ZELDA VAN COLLER OPTOMETRISTS 011 9002044 BRACKEN GARDEN SHOPPING CNTR, CNR DELPHINIUM & HENNIE ALBERTS STR ALBERTON 266639 SIKOSANA J T - ALBERTON 011 9071870 SHOP 23-24 VILLAGE SQUARE, 46 VOORTREKKER ROAD ALBERTON 280828 RAMOVHA & DOWLEY INC 011 9070956 53 VOORTREKKER ROAD, NEW REDRUTH ALBERTON 348066 JANSE VAN RENSBURG C Y 011 8690754/ 25 PADSTOW STREET, RACEVIEW 072 7986170 ALBERTON 650366 MR IZAT SCHOLTZ 011 9001791 172 HENNIE ALBERTS STREET, BRACKENHURST ALBERTON 7008384 GLUCKMAN P 011 9078745 1E FORE STREET, NEW REDRUTH ALBERTON 7009259 BRACKEN CITY OPTOMETRISTS 011 8673920 SHOP 26 BRACKEN CITY, HENNIE ALBERTS ROAD, BRACKENHURST ALBERTON 7010834 NEW VISION OPTOMETRISTS CC 090 79235 19 NEW QUAY ROAD, NEW REDRUTH ALBERTON 7010893 I CARE OPTOMETRISTS ALBERTON 011 9071046 SHOPS -

Mont D'or Bohemian House

FACT SHEET – MONT D’OR BOHEMIAN HOUSE ROOM TYPE King size beds Queen size beds ROOM TOTALS 2 8 • Check in 14:00 – 16:00 PM, Check out 10:00 AM • We accept all major credit cards, except Diners • GPS co-ordinates: -25.7887 Latitude & 28.2502 Longitude • Average temperatures in Pretoria: MONTH JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC Min (°C) 17 17 16 12 8 5 4 7 12 14 15 17 Max (°C) 29 29 27 25 23 20 20 23 27 28 28 29 IN-ROOM FACILITIES: • Housekeeping once daily • Bathrobes • Air-conditioning • Complimentary essential • Tea & Coffee making facilities toiletries/amenities • Mini fridge • Electronic safe • Hairdryer • All Rooms have an en-suite • Television bathroom BOUTIQUE HOTEL FACILITIES: • Dining room or veranda • 24-hour security • Free Wi-Fi • Day Spa • Swimming Pool with minibar • Walking distance from Waterkloof • Scan & Fax Facilities Heights (Restaurants) • Secure Parking THINGS TO DO IN PRETORIA: • The Rovos Rail (9km) • Sun Arena Times Square (2km) • Menlyn Park (4km) • The Blue Train (7km) CONFERENCE STYLES: (Inclusive of a white board and a TV screen with an HDMI Cable) • Intimate conference room – between 8 and 12 delegates www.montdorpta.co.za 389 Eridanus Street, Waterkloof Ridge Pretoria, South Africa, 0181 Tel: +27 72 654 4122 TRANSPORT: Nearest Airport: OR Tambo International Airport (38km) - Airport transfers are available on arrangement. Closest Gautrain Station: Pretoria/Hatfield DIRECTIONS TO MONT D’OR BOHEMIAN HOUSE • 18 minutes from The Blue Train | 34 minutes from OR Tambo Airport | 39 minutes from Rovos Rail • TRAVEL BY AIR The closest airport to Bohemian House is Lanseria International Airport, which is 52,4 km away or OR Tambo Airport which is 46,7 km away. -

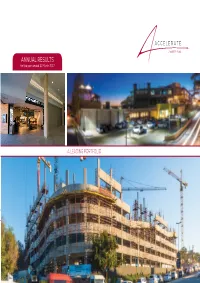

Accelerate Results Book 1106

ANNUAL RESULTS for the year ended 31 March 2017 A LEADING PORTFOLIO CONTENTS Accelerate since listing 1 Highlights for the period under review 4 Accelerate at a glance 6 Financial results 8 Like-for-like net property income and key indicators 12 Capital structure 17 Our strategic nodes 19 Looking forward 40 Annexure 1: Property portfolio summary 43 Annexure 2: Drive for quality since listing 47 Annexure 3: Accelerate’s positioning on the JSE 50 ACCELERATE SINCE LISTING 1 ACCELERATE SINCE LISTING Total return since listing Asset growth (Rands per share) (Rbn) R11,6bn 69 properties Total return since listing (75%) 3.68 R8,4bn 31 March 2017 distribution 0.58 61 properties R6,7bn R6,1bn 52 properties 31 March 2016 distribution 0.54 R5,5bn 52 properties 51 properties 31 March 2015 distribution 0.49 31 March 2014 distribution (110 days) 0.14 Capital growth 1.93 0 1 2 3 4 At listing Mar 14 Mar 15 Mar 16 Mar 17 RSA properties APF Europe Acquisition of Acquisition of Acquisition of KPMG portfolio Portside Eden Meander shopping centre 800 for R850m for R755m in George for R365m 700 APF lists at R4,88 600 Cents 500 Equalisation option (8%) on Acquisition of Fourways Super Regional agreed property portfolio in CEE (Austria and Slovakia) for €82,1m 400 Dec 13 Mar 14 Jun 14 Sep 14 Dec 14 Mar 15 Jun 15 Sep 15 Dec 15 Mar 16 Jun 16 Sep 16 Dec 16 Mar 17 2 STRATEGY, FOCUS AND OUTCOMES Strategy Retail focus Nodal strategy Drive for quality Geographic diversification Active asset Quality enhancing Establishing future growth Key operational focus Reduce vacancies -

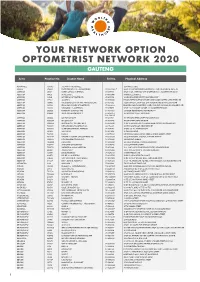

Your Network Option Optometrist Network 2020 Gauteng

YOUR NETWORK OPTION OPTOMETRIST NETWORK 2020 GAUTENG Area Practice No. Doctor Name Tel No. Physical Address ACTONVILLE 456640 JHETAM N - ACTONVILLE 1539 MAYET DRIVE AKASIA 478490 ENGELBRECHT A J A - WONDERPARK 012 5490086/7 SHOP 404 WONDERPARK SHOPPING C, CNR OF HEINRICH AVE & OL ALBERTON 58017 TORGA OPTICAL ALBERTON 011 8691918 SHOP U 142, ALBERTON CITY SHOPPING MALL, VOORTREKKER ROAD ALBERTON 141453 DU PLESSIS L C 011 8692488 99 MICHELLE AVENUE ALBERTON 145831 MEYERSDAL OPTOMETRISTS 011 8676158 10 HENNIE ALBERTS STREET, BRACKENHURST ALBERTON 177962 JANSEN N 011 9074385 LEMON TREE SHOPPING CENTRE, CNR SWART KOPPIES & HEIDELBERG RD ALBERTON 192406 THEOLOGO R, DU TOIT M & PRINSLOO C M J 011 9076515 ALBERTON CITY, SHOP S03, CNR VOORTREKKER & DU PLESSIS ROAD ALBERTON 195502 ZELDA VAN COLLER OPTOMETRISTS 011 9002044 BRACKEN GARDEN SHOPPING CNTR, CNR DELPHINIUM & HENNIE ALBERTS STR ALBERTON 266639 SIKOSANA J T - ALBERTON 011 9071870 SHOP 23-24 VILLAGE SQUARE, 46 VOORTREKKER ROAD ALBERTON 280828 RAMOVHA & DOWLEY INC 011 9070956 53 VOORTREKKER ROAD, NEW REDRUTH ALBERTON 348066 JANSE VAN RENSBURG C Y 011 8690754/ 25 PADSTOW STREET, RACEVIEW 072 7986170 ALBERTON 650366 MR IZAT SCHOLTZ 011 9001791 172 HENNIE ALBERTS STREET, BRACKENHURST ALBERTON 7008384 GLUCKMAN P 011 9078745 1E FORE STREET, NEW REDRUTH ALBERTON 7009259 BRACKEN CITY OPTOMETRISTS 011 8673920 SHOP 26 BRACKEN CITY, HENNIE ALBERTS ROAD, BRACKENHURST ALBERTON 7010834 NEW VISION OPTOMETRISTS CC 090 79235 19 NEW QUAY ROAD, NEW REDRUTH ALBERTON 7010893 I CARE OPTOMETRISTS ALBERTON 011 -

See the Sights, Hear the Sounds TSHWANE EXPERIENCE BUCKET LIST the CAPITAL EXPERIENCES DISCOVER THINGS to ESSENTIAL ADVENTURE TRAVEL INFO ACTIVITIES SEE & DO

A VISITORS’ GUIDE See the sights, hear the sounds TSHWANE EXPERIENCE BUCKET LIST THE CAPITAL EXPERIENCES DISCOVER THINGS TO ESSENTIAL ADVENTURE TRAVEL INFO ACTIVITIES SEE & DO discovertshwane.com @DISCOVERTSHWANE www.DiscoverTshwane.com - 4 - CONTENTS Experience Discover Jacaranda the Capital 6 our Gems16 City 20 Adventure Things To Bucketlist Activities18 See and Do30 Experiences38 -8- -9- -10- -12- -22- About City of Map of Essential Discover Tshwane Wonders Tshwane Travel Info Mamelodi -27- -46- -48- -52- -54- Tshwane Tshwane Taste of Travelling 10 Reasons Neighbourhoods on a Budget Tshwane in Tshwane to invest in Tshwane DISCOVER TSHWANE - 5 - FOREWORD GREETINGS FROM THE CAPITAL CITY! Welcome to our very first issue Immerse yourself in Tshwane’s of the Discover Tshwane visitors’ diverse tourism experiences and guide, the go-to magazine that then begin planning your next trip provides visitors with information on to our warm, vibrant and welcoming the City of Tshwane and its tourism city. offering. For more comprehensive Many people always ask what information about our destination, makes our city & region different, please access our website on: the answer to that question lies discovertshwane.com or get in touch in-between the covers of this with us through #discovertshwane magazine. on Facebook, Instagram or Twitter. It is full of great tips and ideas Enjoy your time in the City of that will help you maximize your Tshwane! experience of Tshwane when you get to visit. Through it, you will fall in love with our rich natural, cultural Immerse yourself and heritage resources, a number of in Tshwane’s beautiful buildings and attractions - “ from Church Square to the Palace of diverse tourism Justice, The Voortrekker Monument, experiences. -

Preferred Provider Pharmacies

PREFERRED PROVIDER PHARMACIES Practice no Practice name Address Town Province 6005411 Algoa Park Pharmacy Algoa Park Shopping Centre St Leonards Road Algoapark Eastern Cape 6076920 Dorans Pharmacy 48 Somerset Street Aliwal North Eastern Cape 346292 Medi-Rite Pharmacy - Amalinda Amalinda Shopping Centre Main Road Amalinda Eastern Cape Shop 1 Major Square Shopping 6003680 Beaconhurst Pharmacy Cnr Avalon & Major Square Road Beacon Bay Eastern Cape Complex 213462 Clicks Pharmacy - Beacon Bay Shop 26 Beacon Bay Retail Park Bonza Bay Road Beacon Bay Eastern Cape 192546 Clicks Pharmacy - Cleary Park Shop 4 Cleary Park Centre Standford Road Bethelsdorp Eastern Cape Cnr Stanford & Norman Middleton 245445 Medi-Rite Pharmacy - Bethelsdorp Cleary Park Shopping Centre Bethelsdorp Eastern Cape Road 95567 Klinicare Bluewater Bay Pharmacy Shop 6-7 N2 City Shopping Centre Hillcrest Drive Bluewater Bay Eastern Cape 6067379 Cambridge Pharmacy 18 Garcia Street Cambridge Eastern Cape 6082084 Klinicare Oval Pharmacy 17 Westbourne Road Central Eastern Cape 6078451 Marriott and Powell Pharmacy Prudential Building 40 Govan Mbeki Avenue Central Eastern Cape 379344 Provincial Westbourne Pharmacy 84C Westbourne Road Central Eastern Cape 6005977 Rink Street Pharmacy 4 Rink Street Central Eastern Cape 6005802 The Medicine Chest 77 Govan Mbeki Avenue Central Eastern Cape 376841 Klinicare Belmore Pharmacy 433 Cape Road Cotswold Eastern Cape 244732 P Ochse Pharmacy 17 Adderley Street Cradock Eastern Cape 6003567 Watersons Pharmacy Shop 4 Spar Complex Ja Calata Street -

Dis-Chem Clinics Offering Imupro, Ige and Lipidpro Sample Collections

Dis-Chem Clinics Offering ImuPro, IgE and LipidPro Sample Collections Please call ahead and ask to speak to the clinic sister to make a booking for your sample to be taken. Cape Town Shop E2 -E3 Bayside Mall, Cnr Blaauwberg Road & West Coast, Table View Cape Town Bayside Mall Western Cape South Africa 7441 021 522 6140 Shop F206 Blue Route Mall, 16 Tokai Road, Tokai Cape Town Blue Route Western Cape South Africa 7945 021 710 1230 Shop G41 Canal Walk Shopping Centre, Century Pl Boulevard Cape Town Canal Walk Western Cape South Africa 7441 021 551 5551 Shop G1 Standard Bank Galleria, 178-182 Main Road, Claremont Cape Town Claremont/Cavendish Western Cape South Africa 7700 021 673 1480 Shop 15 Sunvalley, Cnr Ou Kaapse Weg and Noordhoek Main Road Cape Town Noordhoek Western Cape South Africa 7975 021 784 4400 Paarl Mall Shop 95 Paarl Mall, Cnr Cecilla & New Vlei Road Paarl Western Cape South Africa 7620 021 863 5060 Shop 310 Somerset Mall, Cnr R44 & N2, Somerset West Cape Town Somerset Mall Western Cape South Africa 7130 021 850 5940 Shop 6 The Point Mall, 76 Regent Road, Sea Point The Point Cape Town Centre/Seapoint Western Cape South Africa 8005 021 430 2100 Pretoria Shop 206 Centurion Lake Mall, Heuwel Road Centurion Centurion Gauteng South Africa 0083 012 663-9363 Shop 35 Hillcrest Boulevard, Cnr Lynwood & Duxbury Road, Hatfield Pretoria Lynwood Gauteng South Africa 0083 012 362 3633 Shop U79 Kolonnade Shopping Centre, Cnr Dr van der Merwe & Sefako Makgatho Drive, Montana Montana Pretoria Gauteng South Africa 0182 012 523 9120 Shop 267 Woodlands Boulevard, Cnr Garsfontein Road & De Villabois Maruil Drive, Pretorius Park Ext. -

Store Code City Street Address Line 1 Street Address Line 2 Street

Store Postal Code City Street Address Line 1 Street Address Line 2 Street Address Line 3 Code WATT STREET BETWEEN 2ND 6353 ALEXANDRA SHOP NO G26 PAN AFRICA SHOPPING CENTRE AND 3RD 2090 6496 BAPONG SHOP 24 KEYA RONA SHOPPING CNTR R556 BAPONG 269 CNR. TOM JONES & NEWLANDS 8743 BENONI SHOP NO. L69-L72;L58A & B LAKESIDE MALL ST 1501 6234 BOTSWANA SHOP NO 14 NZANO CENTRE BLUE JACKET ST FRANCISTOWN CNR DE BRON & OKOVANGO 6136 BRACKENFELL SHOP L24 CAPE GATE CENTRE DRIVE 7560 8279 BRITS ERF 2709 SHOP NO 1 DE WITTS AVENUE 250 8326 BURGERSFORT TWIN CITY SHOP CENTRE 1150 8106 BUTHA BUTHE SHOP 7 104 CAPE TOWN BLANCKENBERGSTRAAT 51 7530 CNR JAN VAN RIEBEECK & 6294 CAPE TOWN SHOP NO 122 ZEVENWACHT VILLAGE CENTRE POLKADRAAI RD 7580 8069 CAPE TOWN SHOP NO 38 & 39 BELLVILLE MIDDESTAD MALL 16-24 CHARL MALAN ST 7530 CNR VOORTREKKER & DE LA RAY 8594 CAPE TOWN SHOP NO 9 PAROW CENTRE DRIVE 7500 8601 CAPE TOWN GOLDEN ACRE SHOPS ADDERLEYST 9 8001 CNR AZ BERMAN DRIVE & 8777 CAPE TOWN SHOP NO 5 PROMENADE MALL SHOPPING CENTRE MORGENSTER ROAD 7785 6569 CENTURION SHOP NO 69 FOREST HILL CITY MALL MAIN STREET 157 8063 DAVEYTON SHOP 5 DAVEYTON MALL HLAKWANA STREET 1507 6323 DURBAN SHOP NO 11-12 QUALBERT CENTRE VICTORIA & ALBERT ST 4000 6507 DURBAN SHOP NO 201B KARA CENTRE DR YUSUF DADOO STREET 4000 GREENSTONE SHOPPING CENTRECNR & VAN RIEBEECK GREENSTONE 6241 EDENVALE SHOP NO U122&U126 MODDERFONTEIN HILL 1609 6629 ESTCOURT SHOP B2A ITHALA CENTRE HARDING STREET ESTCOURT 3310 551 FRANCISTOWN H/V HASKINS & FRANCISLAAN 8227 FRANCISTOWN SHOP NO 17 NSWAZI MALL BLUE JACKET STR -

Store Locator

VISIT YOUR NEAREST EDGARS STORE TODAY! A CCOUNT Gauteng EDGARS BENONI LAKESIDE EDGARS WOODLANDS BLVD LAKESIDE MALL BENONI WOODLANDS BOULEVARD PRETORIUS PARK EDGARS BLACKHEATH CRESTA MAC MALL OF AFRICA CRESTA SHOPPING CENTRE CRESTA MALL OF AFRICA WATERFALL CITY EDGARS BROOKLYN EDGARS ALBERTON CITY BROOKLYN MALL AND DESIGN SQUARE NIEUW MUCKLENEUK ALBERTON CITY SHOPPING CENTRE ALBERTON EDGARS MALL AT CARNIVAL EDGARS SPRING MALL MALL AT CARNIVAL BRAKPAN SPRINGS MALL1 SPRINGS EDGARS CHRIS HANI CROSSING EDGARS CENTURION CENTRE CHRIS HANI CROSSING VOSLOORUS CENTURION MALL AND CENTURION BOULEVARD CENTURION EDGARS CLEARWATER MALL EDGARS CRADLE STONE MALL CLEARWATER MALL ROODEPOORT CRADLESTONE MALL KRUGERSDORP EDGARS EAST RAND EDGARS GREENSTONE MALL EAST RAND MALL BOKSBURG GREENSTONE SHOPPING CENTRE MODDERFONTEIN EDGARS EASTGATE EDGARS HEIDELBERG MALL EASTGATE SHOPPING CENTRE BEDFORDVIEW HEIDELBERG MALL HEIDELBERG EDGARS FESTIVAL MALL EDGARS JABULANI MALL FESTIVAL MALL KEMPTON PARK JABULANI MALL JABULANI EDGARS FOURWAYS EDGARS JUBILEE MALL FOURWAYS MALL FOURWAYS JUBILEE MALL HAMMANSKRAAL EDGARS KEYWEST EDGARS MALL OF AFRICA KEY WEST KRUGERSDORP MALL OF AFRICA WATERFALL EDGARS KOLONNADE EDGARS MALL OF THE SOUTH SHOP G 034 MALL OF THE SOUTH BRACKENHURST KOLONNADE SHOPPING CENTRE MONTANA PARK EDGARS MAMELODI CROSSING EDGARS MALL REDS MAMS MALL MAMELODI THE MALL AT REDS ROOIHUISKRAAL EXT 15 EDGARS RED SQUARE DAINFERN EDGARS MAPONYA DAINFERN SQUARE DAINFERN MAPONYA MALL KLIPSPRUIT EDGARS SOUTHGATE EDGARS MENLYN SOUTHGATE MALL SOUTHGATE MENLYN PARK SHOPPING -

Attacq: Fabulous at Best Life at Never Waste Mall of Africa Waterfall! a Crisis

ISSUE 2 2021 WATERFALL RETAINS WORLD’S BEST TITLE NEW STORES, NEW LIVE YOUR ATTACQ: FABULOUS AT BEST LIFE AT NEVER WASTE MALL OF AFRICA WATERFALL! A CRISIS The Sheds @ Waterfall CONTENTS The Sheds @ Waterfall ESTATE NEWS HOME FRONT TODAY’S CHILD Welcome Message from WATERFALL 4 W ATERFALL HOME SERVICE ProVIDERS C urro WATERFALL: AND Classifieds 39 LESSONS FROM 2020 34 WATERFALL retains WORLD’S BEST title 6 KYALAMI SCHOOLS: EXPERIENCE THE GAUTENG’S COOLEST MALL IS SPIRIT OF SUCCESS by RE-imagining NOW ALSO THE GREENEST 9 MOTORING education 36 LIVE YOUR BEST LIFE at WATERFALL 11 Mercedes-BENZ V300D 31 NEVER WASTE A crisis 16 TOYOTA Quantum VX Premium 32 LIFESTYLE New stores, New fabulous at MALL OF Africa 18 R ECIPE: CRUSTLESS SALMON AND Prawn Quiche 28 SHARES FOR THE future 22 DATING: 101 40 Netcare: TALKING SHOULDER arthritis 25 Click here for the 2021 WATERFALL CONTACTS 38 EDUCATION SUPPLEMENT Preparing your children for the future COVID-19 TEST Stations FIND YOUR COPY WITH THIS ISSUE! IN WATERFALL 38 Waterfall Magazine is published by Estates in Africa (Pty) Ltd, trading as EIA Publishing, on behalf of Waterfall and in association with the Waterfall Homeowners Association. The opinions expressed are not necessarily those of the Waterfall Homeowners Association, the Estate, the publisher, nor of the companies themselves. ESTATES IN AFRICA (PTY) LTD HEAD OFFICE: 32 Fricker Road, Illovo, Johannesburg. www.eiapublishing.co.za Publisher: Nico Maritz [email protected] Editor: Bev Hermanson 071 205 9502 [email protected] Marketing Manager: Martin Fourie 072 835 8405 [email protected] ()Pty Ltd Assistant Editor: Nicole Hermanson [email protected] Production Co-ordination: Chris Grant [email protected] Design: Diane van Noort [email protected] Cover Photo: Franz Rabe from Natural Photography [email protected] Waterfall Issue 2 2021 3 Waterfall News A message from WATERFALL e are proud trading.