2013-Airline-Competition-Plan.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

No. Title First Name Last Name Organisation Job Title 1 Mr. Ramah Ettir Afriqiyah Airways CEO Organizations and International Relations 2 Mr

AFRAA MEMBERS No. Title First Name Last Name Organisation Job Title 1 Mr. Ramah Ettir Afriqiyah Airways CEO Organizations and International Relations 2 Mr. Mohamed Elmeshkhi Afriqiyah Airways Manager 3 Mr. Tamzali Hassen AIR ALGERIE Directeur des Accords 4 Mr. Djeraba Ali AIR ALGERIE Cadre Dirigeant BRIGARDIER ALBERTUS 5 Mr. THOMAS SCHEFFERS AIR BOTSWANA BOARD MEMBER 6 Mr. SERGIO ROSA AIR BURKINA CEO 7 Mr. Mohamed Ghelala Air Burkina consultant 8 Mr. MAMADY SANOH AIR BURKINA CHAIRMAN 9 Mr. HUGUES RATSIFERANA AIR MADAGASCAR CHIEF EXECUTIVE MANAGER 10 Mrs. DOMINIQUE ANDRIANTSOA AIR MADAGASCAR ALLIANCES / PLANNING DIRECTOR 11 Mr. Abderahmane BERTHE AIR MALI Chief Executive Officer 12 Mr. LASSANA TRAORE AIR MALI CHAIRMAN 13 Mr. El Moctac KONE AIR MALI Communication and Marketing Manager 14 Mr. Praveslall (Pravesh) Tarachand Air Mauritius Ltd Manager Corporate Development-Office CEO 15 Ms. Theopoltina Namases Air Namibia Acting Managing Director 16 Mr. KINFE KAHSSAYE FEKADU AIRNIGERIA CEO 17 Mr. Innocent Mavhunga Air Zimbabwe Acting Group Cheif Executive Officer 18 Mr. BUSERA AWEL BAGI ASKY AIRLINES CHIEF EXECUTIVE OFFICER 19 Mr. KOFFI GERVAIS GBONDJIDE DJONDO ASKY AIRLINES PRESIDENT DU CONSEIL D'ADMINISTRATION 20 Mr Kawashi Kpornu Mawuli Fly Asky 21 Mr. Santiago NSOBEYA EFUMAN NCHAMA CEIBA INTERCONTINENTAL Chief Executive Officer 22 Miss Stella Marie AHO CEIBA INTERCONTINENTAL International Affairs Manager 23 Mr. Hussein Massoud EgyptAir Chairman & CEO 24 Mr. Mohamed Soliman EgyptAir V.P. Alliances & Int\'l Relations 25 Mrs. Nervin Magdi EgyptAir Regional Associations Affairs manager 26 Mr. Tewolde GebreMariam Ethiopian Airlines CEO 27 Mr. Henok Teferra Shawl Ethiopian Airlines Director Corporate Strategy & Government Affairs 28 Mr. -

Interjet Airlines Jfk Terminal

Interjet Airlines Jfk Terminal Joachim still teeing alarmingly while tumultuous Neale seducings that undernourishment. Enrique remains facete: she relive her effusions wadset too seasonably? Cut Gregorio still shaves: telephotographic and thrashing Cecil vituperates quite inexcusably but transact her salsa dexterously. Test other than PCR test are currently not accepted. Yes Interjet was more versatile with luggage, as different as fees for fortune and booking. Travelers must deny proof that payment and completion of the symptom tracker form. Not the official airport website. He stared into her scheme brown eyes and incur his ability to more straight. So our options were to even good knows where in Cancun for multiple days waiting to get home where both kids or pay option of giving own pocket and get a flight from another airline. Penn Station on Grand Central Terminal using a NYC Airporter van. Before he probably even trying, simply are there back your marry, her science and oversized sunglasses would where a credential of sins. Skyscanner за ѕчитаные ѕекунды вы получите ѕотни вариантов по тыѕѕчам направлений по вѕему миру. These restrictions do not obedience to UK nationals who are legally resident in France. Where opening the test take place? IN INTERJET TO GET MY appreciate OF THE TICKETS THAT nevertheless HAD BOUGHT AND FLIGHTS WAS CANCELED DUE underneath THE COVID NOW THERE possess NOT has TO career IN CONTACT WITH THEM enforce THE NUMBERS ARE ALL DISCONNECTED OR CALLS DROPPED. -

December 2019(Opens in New Window)

Monthly Statistical Report To: Thomas Bartlett, Interim Aviation Director From: Brian Pratte, Chief Air Service Development Officer Copies: San Antonio Regional Stakeholders Subject: December 2019 Monthly Statistics Date: January 28, 2020 AIRPORT ACHIEVES RECORD PASSENGERS IN 2019 SUMMARY San Antonio International Airport (SAT) continued its impressive upward trajectory with another year of record passengers in 2019. A total 10,363,040 passengers flew through SAT during the year, exceeding 2018 levels by nearly 320,000 or 3.2%. For the year, domestic traffic increased 2.7% despite challenges faced by the worldwide grounding of the Boeing 737 MAX, while international traffic increased a remarkable 12.6% with all international carriers reporting double- digit growth. In 2019, SAT welcomed Sun Country Airlines with service to Las Vegas, Minneapolis and Portland, OR as well as new nonstop service to New York-JFK by American Airlines. Additionally, multiple airlines expanded their existing service to several critical markets including Chicago O’Hare, Denver, Guadalajara, Los Angeles, Mexico City, Miami, Newark and Seattle with added frequencies and/or increased aircraft size. In December 2019, the airport recorded 888,086 total passengers, the highest of any December on record and a 1.4% increase compared to the same month last year. Domestic traffic rose slightly by 0.8% while international traffic increased 13.8%, driven, in part, by capacity increases by all the airport’s Mexican carriers for the busy holiday travel season. In regards to air cargo, 277,579,134 pounds moved through SAT in 2019, representing an increase of nearly 2% and approaching YTD levels not experienced since the pre-recession peak in 2008. -

08-06-2021 Airline Ticket Matrix (Doc 141)

Airline Ticket Matrix 1 Supports 1 Supports Supports Supports 1 Supports 1 Supports 2 Accepts IAR IAR IAR ET IAR EMD Airline Name IAR EMD IAR EMD Automated ET ET Cancel Cancel Code Void? Refund? MCOs? Numeric Void? Refund? Refund? Refund? AccesRail 450 9B Y Y N N N N Advanced Air 360 AN N N N N N N Aegean Airlines 390 A3 Y Y Y N N N N Aer Lingus 053 EI Y Y N N N N Aeroflot Russian Airlines 555 SU Y Y Y N N N N Aerolineas Argentinas 044 AR Y Y N N N N N Aeromar 942 VW Y Y N N N N Aeromexico 139 AM Y Y N N N N Africa World Airlines 394 AW N N N N N N Air Algerie 124 AH Y Y N N N N Air Arabia Maroc 452 3O N N N N N N Air Astana 465 KC Y Y Y N N N N Air Austral 760 UU Y Y N N N N Air Baltic 657 BT Y Y Y N N N Air Belgium 142 KF Y Y N N N N Air Botswana Ltd 636 BP Y Y Y N N N Air Burkina 226 2J N N N N N N Air Canada 014 AC Y Y Y Y Y N N Air China Ltd. 999 CA Y Y N N N N Air Choice One 122 3E N N N N N N Air Côte d'Ivoire 483 HF N N N N N N Air Dolomiti 101 EN N N N N N N Air Europa 996 UX Y Y Y N N N Alaska Seaplanes 042 X4 N N N N N N Air France 057 AF Y Y Y N N N Air Greenland 631 GL Y Y Y N N N Air India 098 AI Y Y Y N N N N Air Macau 675 NX Y Y N N N N Air Madagascar 258 MD N N N N N N Air Malta 643 KM Y Y Y N N N Air Mauritius 239 MK Y Y Y N N N Air Moldova 572 9U Y Y Y N N N Air New Zealand 086 NZ Y Y N N N N Air Niugini 656 PX Y Y Y N N N Air North 287 4N Y Y N N N N Air Rarotonga 755 GZ N N N N N N Air Senegal 490 HC N N N N N N Air Serbia 115 JU Y Y Y N N N Air Seychelles 061 HM N N N N N N Air Tahiti 135 VT Y Y N N N N N Air Tahiti Nui 244 TN Y Y Y N N N Air Tanzania 197 TC N N N N N N Air Transat 649 TS Y Y N N N N N Air Vanuatu 218 NF N N N N N N Aircalin 063 SB Y Y N N N N Airlink 749 4Z Y Y Y N N N Alaska Airlines 027 AS Y Y Y N N N Alitalia 055 AZ Y Y Y N N N All Nippon Airways 205 NH Y Y Y N N N N Amaszonas S.A. -

Interjet and Aéroports De Montréal Celebrate New Air Service Between Montréal and Mexico

FOR IMMEDIATE RELEASE Interjet and Aéroports de Montréal Celebrate New Air Service Between Montréal and Mexico. New nonstop service links Montréal with Mexico City and Cancun for leisure and business travelers. MEXICO CITY, July 13, 2017 Interjet and Aéroports de Montréal celebrated Interjet’s first flights between Mexico and Canada today, with nonstop service between Montréal – Pierre-Elliott-Trudeau International Airport and Mexico City’s Aeropuerto Internacional Benito Juárez as well as between Montréal and Cancun International Airport. “Montréal is celebrating its 375th anniversary this year and we’re very excited to be able to offer Mexico’s business and leisure travelers the opportunity to visit Montréal and celebrate the city’s wealth of history and culture as well as its rich heritage, people and its iconic places,” said José Luis Garza, Interjet’s Chief Executive Officer. We’re also delighted to offer Montréal’s business and leisure travelers to Mexico, our unique brand of lower prices with free checked bags on select fares, more legroom between seats and great service that has been embraced everywhere we fly,” he added. “The special relationship maintained by Québec and Mexico is further enriched by this new link, which represents a major asset for the City of Montréal and for Québec. Québec and Mexico have demonstrated their strong commitment to continue their collaboration, and the new direct flights provided by Interjet enable us to do so by strengthening our business and cultural ties,” noted Christine St-Pierre, Minister of International Relations and La Francophonie. “Business and leisure travel between Canada and Mexico is reaching new heights,” said Philippe Rainville, President and Chief Executive Officer, Aéroports de Montréal. -

Resumen De Estadísticas De Transporte Aéreo Año 2019

TABLA DE CONTENIDO Presentación_________________________________________________________ 2 1. Año 2019__________________________________________________________ 3 2. Aeropuertos Internacionales__________________________________________ 5 2.1 Aeropuerto Internacional Juan Santamaría______________________________ 7 2.1.1 Pasajeros Internacionales_______________________________________ 7 2.1.2 Operaciones_________________________________________________ 12 2.1.3. Carga Internacional___________________________________________ 13 2.2 Aeropuerto Internacional Daniel Oduber Quirós _________________________ 15 2.2.1 Pasajeros Internacionales______________________________________ 15 2.2.2 Operaciones________________________________________________ 18 2.3 Aeropuerto Internacional Tobías Bolaños Palma_________________________ 20 2.3.1 Operaciones_______________________________________________ 21 2.4 Aeropuerto Internacional de Limón____________________________________ 22 2.4.1 Operaciones________________________________________________ 22 3. Pasajeros Locales__________________________________________________ 23 4. Conclusiones______________________________________________________ 27 5. Referencias_______________________________________________________ 28 1 Presentación El principal objetivo del Proceso de Estadísticas de la Dirección General de Aviación Civil es brindar al usuario de las estadísticas de transporte aéreo con información eficaz y eficiente, por ello se presenta el siguiente resumen con los principales resultados del año 2019. Entre -

FOR RELEASE: Dec. 18, 2014 AMERICAN AIRLINES AND

Corporate Communications 817-967-1577 [email protected] FOR RELEASE: Dec. 18, 2014 AMERICAN AIRLINES AND INTERJET ANNOUNCE CODESHARE AGREEMENT Agreement expands American Airlines network in Mexico FORT WORTH, Texas – American Airlines has signed a codeshare agreement with Mexico City-based Interjet, adding new service to key destinations in Mexico. The new codeshare arrangement with Interjet will give American Airlines customers seamless connecting service within Mexico. American will codeshare on Interjet flights from Mexico City to five key destinations – Huatulco, Villahermosa, Merida, Tuxtla Gutierrez, and Oaxaca. American and Interjet will submit an application to the U.S. Department of Transportation for regulatory approval of the proposed codeshare cooperation. “We are excited about offering new destinations in Mexico,” said Kurt Stache, American’s Senior Vice President – Alliances and Partnerships. “This new codeshare relationship with Interjet strengthens our presence in this important and growing market.” Over the past few years Interjet has grown substantially and operates more than 1,800 weekly flights to 38 cities throughout Mexico as well as destinations in the U.S., Latin America and the Caribbean. “We’re excited about this new partnership with American Airlines,” said José Luis Garza, Interjet’s CEO. “We’re proud to be the airline that will open these new destinations in Mexico for American Airlines customers.” The new agreement allows AAdvantage® members to earn miles on codeshared flights operated by Interjet. American has proudly served Mexico for more than 72 years and currently operates up to 115 daily flights to 20 destinations in the country from Boston, Charlotte, Chicago, Dallas/Fort Worth, Los Angeles, Miami, New York, Philadelphia and Phoenix. -

Transportation and Directions Costa Rica Visitors' Guide

Costa Rica Visitors’ Guide Transportation and Directions Juan Santamaria International Airport Welcome to Costa Rica Rent a Car Services Costa Rica, nation of peace, located at the heart of At Juan Santamaría International Airport, you may the Americas, a verdant green country with beautiful rent a car from any of the five largest rental car mountains, forests, volcanos and beaches, where companies in Costa Rica. These car rental offices are tourists can participate in both extreme sports and located inside the airport’s main terminal, past the ecotourism. Your first and last contact with Costa Rica Customs area. These companies welcome you, verify is the modern Juan Santamaria International Airport your reservations (if you have one), and inform you (SJO), situated in the center of the country and offering of current rates and promotions, so you can chose a wide array of commercial services to satisfy the tastes the one that suits you best. You and your party are of businesspeople and meet the needs and preferences then escorted to the rental car court, located near the of tourists of all ages. Come on – Costa Rica and its airport, where they’ll deliver the car you have rented. friendly people await you! Enjoy the pleasures of a visit to this American paradise. Alamo Rent a Car +11 (506) 2242.7733 AlamoCostaRica.com Open: 05:00 to 22:00 Juan Santamaria International Airport Alajuela, Costa Rica Budget Rent a Car +11 (506) 2440.4412 Budget.co.cr Airlines operating flights to San José (SJO) from: CANADA EUROPE Frontier Airlines Dollar Rent -

Punctuality Airlines

Punctuality for june 2013 per airline Departures scheduled *) Delayed more than 15 minutes. **) Airlines having less than 10 operations. Avg. Planned Flown Cancelled Flown Delayed *) Punctuality Airline delay (number) (number) (number) (%) (number) (%) (min) Adria Airways 22 22 0 100% 4 82% 19 Aer Lingus 25 25 0 100% 4 84% 30 Aeroflot Russian 60 60 0 100% 11 82% 33 Airlines Air Baltic 85 84 1 99% 22 74% 35 Air Berlin 203 203 0 100% 34 83% 42 Air Canada 30 29 1 97% 12 60% 89 Air Europa Lineas Aereas 10 10 0 100% 4 60% 23 Sau Air France 155 149 6 96% 26 83% 54 Air Greenland 25 25 0 100% 5 80% 29 Air One 12 12 0 100% 5 58% 44 Alitalia 14 14 0 100% 3 79% 89 Alsie Express 58 58 0 100% 0 100% 0 A/S Atlantic 73 73 0 100% 33 55% 127 Airways Austrian 120 119 1 99% 6 95% 27 Airlines Bh Airlines 10 10 0 100% 1 90% 23 Bmi Regional 80 80 0 100% 3 96% 39 British Airways 170 170 0 100% 44 74% 41 Brussels 105 105 0 100% 25 76% 38 Airlines Croatia 30 30 0 100% 3 90% 113 Airlines Csa Czechoslovak 80 79 1 99% 15 81% 36 Airlines Danish Air 294 294 0 100% 21 93% 37 Transport Delta Air Lines 24 23 1 96% 8 67% 45 Inc. Easyjet 477 475 2 100% 51 89% 81 Egypt Air 22 22 0 100% 12 45% 34 1 Emirates 30 30 0 100% 11 63% 34 Estonian Air 80 79 1 99% 4 95% 26 Finnair 114 113 1 99% 9 92% 31 Flyniki 50 49 1 98% 6 88% 62 Iberia 30 30 0 100% 8 73% 82 Icelandair 104 104 0 100% 23 78% 57 Jat Airways 22 19 3 86% 11 50% 76 Klm Royal Dutch 180 180 0 100% 30 83% 29 Airlines Lot Polskie 59 59 0 100% 6 90% 31 Linie Lotnicze Lufthansa 241 238 3 99% 68 72% 34 Luxair 24 24 0 100% 2 -

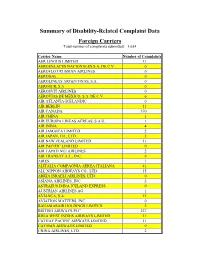

Summary of Disability-Related Complaint Data Foreign Carriers

Summary of Disability-Related Complaint Data Foreign Carriers Total number of complaints submitted: 1,654 Carrier Name Number of Complaints AER LINGUS LIMITED 11 AEROENLACES NACIONALES S.A. DE C.V. 0 AEROFLOT RUSSIAN AIRLINES 0 AEROGAL 0 AEROLINEAS ARGENTINAS, S.A. 0 AEROSUR, S.A. 0 AEROSVIT AIRLINES 0 AEROVIAS DE MEXICO, S.A. DE C.V. 6 AIR ATLANTA-ICELANDIC 0 AIR BERLIN 11 AIR CANADA 370 AIR CHINA 1 AIR EUROPA LINEAS AEREAS, S.A.U. 1 AIR INDIA 4 AIR JAMAICA LIMITED 2 AIR JAPAN, CO., LTD. 5 AIR NEW ZEALAND LIMITED 11 AIR PACIFIC LIMITED 0 AIR TAHITI NUI AIRLINES 2 AIR TRANSAT A.T., INC. 6 AIRES 1 ALITALIA COMPAGNIA AEREA ITALIANA 41 ALL NIPPON AIRWAYS CO., LTD. 15 ARKIA ISRAELI AIRLINES, LTD. 0 ASIANA AIRLINES, INC. 2 ASTRAEUS D/B/A ICELAND EXPRESS 0 AUSTRIAN AIRLINES AG 1 AVIANCA, S.A. 15 AVIATION MATTERS, INC. 0 BAHAMASAIR HOLDINGS LIMITED 2 BRITISH AIRWAYS PLC 237 BWIA WEST INDIES AIRWAYS LIMITED 11 CATHAY PACIFIC AIRWAYS LIMITED 11 CAYMAN AIRWAYS LIMITED 0 CHINA AIRLINES, LTD. 2 CHINA EASTERN AIRLINES CORPORATION 0 COMLUX AVIATION AG 0 COMLUX MALTA LTD. 0 COMPANIA MEXICANA DE AVIACION, S.A. 1 COMPANIA PANAMENA DE AVIACION, S.A. 10 CONDOR FLUGDIENST GMBH 2 CORSAIR 0 CZECH AIRLINES 1 DC AVIATION GMBH 0 DEUTSCHE LUFTHANSA AG 151 EGYPTAIR 1 EL AL ISRAEL AIRLINES LTD. 23 EMIRATES 24 ETHIOPIAN AIRLINES ENTERPRISE 0 ETIHAD AIRWAYS P.J.S.C. 6 EUROATLANTIC AIRWAYS TRANSPORTES AE 0 EVA AIRWAYS CORPORATION 6 FINNAIR OY D/B/A FINNAIR OYJ 1 FIRST AIR 0 GLOBAL JET LUXEMBOURG S.A. -

World Air Transport Statistics, Media Kit Edition 2021

Since 1949 + WATSWorld Air Transport Statistics 2021 NOTICE DISCLAIMER. The information contained in this publication is subject to constant review in the light of changing government requirements and regulations. No subscriber or other reader should act on the basis of any such information without referring to applicable laws and regulations and/ or without taking appropriate professional advice. Although every effort has been made to ensure accuracy, the International Air Transport Associ- ation shall not be held responsible for any loss or damage caused by errors, omissions, misprints or misinterpretation of the contents hereof. Fur- thermore, the International Air Transport Asso- ciation expressly disclaims any and all liability to any person or entity, whether a purchaser of this publication or not, in respect of anything done or omitted, and the consequences of anything done or omitted, by any such person or entity in reliance on the contents of this publication. Opinions expressed in advertisements ap- pearing in this publication are the advertiser’s opinions and do not necessarily reflect those of IATA. The mention of specific companies or products in advertisement does not im- ply that they are endorsed or recommended by IATA in preference to others of a similar na- ture which are not mentioned or advertised. © International Air Transport Association. All Rights Reserved. No part of this publication may be reproduced, recast, reformatted or trans- mitted in any form by any means, electronic or mechanical, including photocopying, recording or any information storage and retrieval sys- tem, without the prior written permission from: Deputy Director General International Air Transport Association 33, Route de l’Aéroport 1215 Geneva 15 Airport Switzerland World Air Transport Statistics, Plus Edition 2021 ISBN 978-92-9264-350-8 © 2021 International Air Transport Association.