Red Queen Effect in German Bank Industry: Implication of Banking Digitalization for Open Innovation Dynamics

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Snapshot of Notable Global COO, CIO and CISO Moves and Appointments

Snapshot of notable global COO, CIO and CISO moves and appointments September 2016 For the latest EMEA, Americas and Asia Pacific moves across: Analytics Data Corporate Services Cyber-Security Facilities Operations Procurement Technology Vendor Management Snapshot of notable global Operations and Technology moves and appointments Page 1 / 6 Next update due: January 2017 People Moves FS EMEA John Burns, the former CTO of Pioneer Investments, joins Cyril Reol, former Glencore CIO, has joined Man Group Deutsche Bank as Global CIO, COO Asset Management as Deputy CTO. Garry Beaton, former Global Head of Operations at Core Technology . Andrew Brown, former Barclays UK Private Bank Chief of Ashmore, joins the Abu Dhabi Investment Authority as its Tom Waite, joins Deutsche Bank as an MD within Staff, has joined US Expat and Fatca Specialist Maseco Global Head of Operations. electronic trading. Waite joined from Bank of America, Private Wealth as its COO. Lesley Cairney has joined Artemis Investment where he was also an MD. Before that, he was an MD at Ken Moore, former Head of Citi Innovation Labs, joins Management as COO. She was formerly at Henderson Goldman Sachs for six years until May 2014. MasterCard as EVP Labs, running global innovation. Global Investors as COO. Amish Popat joins Dromeus Capital Group as COO from David Grant has joined Nationwide as Head of IT and Lewis Love, the former Global Chief Procurement Officer New Amsterdam Capital, where he was the Finance and Security Risk from Lloyds Banking Group, where he was for Aon has been named as the COO for Bank of Ireland, Operations Manager. -

Eli 022807Me

ORANGE COUNTY TREASURER-TAX COLLECTOR APPROVED ISSUER LIST COMMERCIAL PAPER / MEDIUM TERM NOTES AS OF: 2/28/2007 CR S/T RATINGS L/T RATINGS PROG RATINGS IND. ISSUER (Shared Structure) # S&P MDY FI S&P MDY FI S&P MDY FI PARENT/ ADMINISTRATOR CODE ADP TAX SERVICES INC 1 A-1+ P-1 NR AAA Aaa NR A-1+ P-1 NR AUTO DATA PROCES 9.4 ALCON CAPITAL CORP 1 A-1+ P-1 NR NR NR NR A-1+ P-1 F1+ NESTLE SA 4.7 AMERICAN HONDA FINANCE 9 A-1 P-1 F1 A+ A1 *+ NR A-1 P-1 F1 AMER HONDA MOTOR 3.3 AMSTERDAM FUNDING CORP 7 NR NR NR NR NR NR A-1 P-1 NR ABN AMRO Bank N.V 7.4 AB AUTOMATIC DATA PROCESSNG 1 A-1+ P-1 NR AAA Aaa NR A-1+ P-1 NR AUTOMATIC DATA PROCESSING, INC. 9.4 AQUINAS FUNDING LLC 3 NR NR NR NR NR NR A-1+ P-1 NR RABOBANK NEDERLAND 7.4 AB ASPEN FUND (w/ Newport Fund) 3 NR NR NR NR NR NR A-1+ P-1 F1+ DEUTSCHE BANK AG 7.4 AB BANK OF AMERICA CORP 5 A-1+ P-1 F1+ AA Aa2 AA A-1+ P-1 F1+ DOMESTIC BANK/FDIC INSURED 7.1 BARCLAYS US FUNDING LLC 4 A-1+ P-1 F1+ AA Aa1 AA+ A-1+ P-1 NR BARCLAYS BK PLC 7.4 BARTON CAPITAL LLC 3 NR NR NR NR NR NR A-1+ P-1 NR SOC GENERALE 7.4 AB BEETHOVEN FUNDING CORP 7 NR NR NR NR NR NR A-1 P-1 NR DRESDNER BANK, AG 7.4 AB BETA FINANCE INC 1 A-1+ P-1 F1+ AAA Aaa AAA A-1+ P-1 F1+ 7.4 AB BMW US CAPITAL LLC 9 A-1 P-1 NR NR A1 NR A-1 P-1 NR BMW AG 3.3 BNP PARIBAS FINANCE INC 5 A-1+ P-1 F1+ AA Aa2 NR A-1+ P-1 NR BNP PARIBAS 7.4 BRYANT PARK FUNDING LLC 7 NR NR NR NR NR NR A-1 P-1 NR HSBC 7.4 AB CALYON NORTH AMERICA INC 6 A-1+ P-1 F1+ AA- Aa2 AA A-1+ P-1 F1+ CALYON 7.1 CATERPILLAR FIN SERV CRP 10 A-1 P-1 F1 A A2 A+ A-1 P-1 F1 CATERPILLAR INC 8.8 CATERPILLAR INC 10 A-1 P-1 F1 A A2 A+ A A2 A+ #N/A N Ap 8.8 CC USA INC 1 A-1+ P-1 NR AAA Aaa NR AAA Aaa NR SECURITY TRUST 7.4 AB CHARIOT FUNDING LLC 7 NR NR NR NR NR NR A-1 P-1 NR JP MORGAN CHASE 7.4 AB CIT GROUP INC 10 A-1 P-1 F1 A A1 A A-1 P-1 F1 #N/A N Ap 7.4 CITIGROUP FUNDING INC 4 A-1+ P-1 F1+ AA Aa1 AA+ A-1+ P-1 F1+ FORMERLY TRAVELERS GROUP INC. -

Resolution Plan 2018 Public Section

RESOLUTION PLAN 2018 PUBLIC SECTION TABLE OF CONTENTS Page INTRODUCTION ......................................................................................................................... 1 1. Names of Material Entities .................................................................................... 3 2. Description of Core Business Lines ....................................................................... 3 3. Summary Financial Information Regarding Assets, Liabilities, Capital, and Major Funding Sources. .................................................................................. 4 4. Description of Derivatives and Hedging Activities ............................................... 7 5. Memberships in Material Payment, Clearing, and Settlement Systems ................ 7 6. Description of Foreign Operations......................................................................... 8 7. Identities of Material Supervisory Authorities ...................................................... 8 8. Identities of Principal Officers ............................................................................... 9 9. Corporate Governance Structure and Processes Related to Resolution Planning ............................................................................................................... 10 10. Material Management Information Systems ........................................................ 11 11. High Level Description of Resolution Strategy ................................................... 12 -i- INTRODUCTION Section -

DEUTSCHE BANK AG SECTION 21C of the SECURITIES EXCHANGE ACT of 1934, MAKING Respondent

UNITED STATES OF AMERICA Before the SECURITIES AND EXCHANGE COMMISSION SECURITIES EXCHANGE ACT OF 1934 Release No. 90875 / January 8, 2021 ACCOUNTING AND AUDITING ENFORCEMENT Release No. 4201 / January 8, 2021 ADMINISTRATIVE PROCEEDING File No. 3-20200 In the Matter of ORDER INSTITUTING CEASE-AND- DESIST PROCEEDINGS PURSUANT TO DEUTSCHE BANK AG SECTION 21C OF THE SECURITIES EXCHANGE ACT OF 1934, MAKING Respondent. FINDINGS, AND IMPOSING A CEASE- AND-DESIST ORDER I. The Securities and Exchange Commission (“Commission”) deems it appropriate that cease- and-desist proceedings be, and hereby are, instituted pursuant to Section 21C of the Securities Exchange Act of 1934 (“Exchange Act”), against Deutsche Bank AG (“Deutsche Bank” or “Respondent”). II. In anticipation of the institution of these proceedings, Deutsche Bank has submitted an Offer of Settlement (the “Offer”) which the Commission has determined to accept. Solely for the purpose of these proceedings and any other proceedings brought by or on behalf of the Commission, or to which the Commission is a party, Respondent admits the Commission’s jurisdiction over it and the subject matter of these proceedings, and consents to the entry of this Order Instituting Cease-and-Desist Proceedings Pursuant to Section 21C of the Securities Exchange Act of 1934, Making Findings, and Imposing a Cease-and-Desist Order (“Order”), as set forth below. III. On the basis of this Order and Respondent’s Offer, the Commission finds1 that: SUMMARY 1. This matter concerns the improper use, from at least 2009 through 2016, by Deutsche Bank of third-party intermediaries, business development consultants, and finders (collectively “BDCs”) to obtain and retain global business. -

Case M.9539 — BNP Paribas/Deutsche Bank (Global

22.10.2019 EN Offi cial Jour nal of the European Union C 358/11 Prior notification of a concentration (Case M.9539 — BNP Paribas/Deutsche Bank (global prime finance and electronic equities business assets)) Candidate case for simplified procedure (Text with EEA relevance) (2019/C 358/05) 1. On 14 October 2019, the Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 (1). This notification concerns the following undertakings: — BNP Paribas SA (‘BNP Paribas’; France), — Certain assets of Deutsche Bank’s prime finance and electronic equities business (the ‘Deustche Bank Target Business’, Germany). BNP Paribas acquires within the meaning of Article 3(1)(b) of the Merger Regulation sole control of the Deutsche Bank Target Business. The concentration is accomplished by way of purchase of assets. 2. The business activities of the undertakings concerned are: — for BNP Paribas: international banking group active in retail banking, asset management, as well as corporate and investment banking, including prime financing and electronic execution services, — for Deutsche Bank Target Business: prime financing and electronic execution services. 3. On preliminary examination, the Commission finds that the notified transaction could fall within the scope of the Merger Regulation. However, the final decision on this point is reserved. Pursuant to the Commission Notice on a simplified procedure for treatment of certain concentrations under the Council Regulation (EC) No 139/2004 (2) it should be noted that this case is a candidate for treatment under the procedure set out in the Notice. 4. The Commission invites interested third parties to submit their possible observations on the proposed operation to the Commission. -

Wells Fargo International Equity Fund

QUARTERLY MUTUAL FUND COMMENTARY Q4 2020 | All information is as of 12/31/2020 unless otherwise indicated. Wells Fargo International Equity Fund Quarterly review GENERAL FUND INFORMATION ● The International Equity Fund underperformed the MSCI ACWI ex USA Index (Net) Ticker: WFENX and the MSCI ACWI ex USA Value Index (Net) for the quarter that ended December 31, 2020. Portfolio managers: Dale A. Winner, ● Performance was driven largely by stock selection, with positive contributions coming CFA®; and Venk Lal from investments in the industrials and materials sectors as well as in China/Hong Subadvisor: Wells Capital Kong and Canada. Management Inc. ● Positions in information technology (IT) and health care as well as in France and Japan Category: Foreign large value detracted from performance. Market review FUND STRATEGY ● Maintains a core equity style that International equity markets initially declined in October before advancing 19.6% in the emphasizes bottom-up stock final two months of the year as multiple COVID-19 vaccines reached 90%+ efficacy and selection based on rigorous, uncertainty surrounding the U.S. presidential election receded, resulting in a 17.0% in-depth, fundamental company return for the MSCI All Country World ex USA Index (Net) in the fourth quarter, the research highest quarterly return since the third quarter of 2009. In this environment, the Global ● Uses a bottom-up research process Purchasing Managers’ Index (PMI) reached 53.3 in October, the highest level since that targets companies with August 2018, but fell back to 52.7 in December, still in expansionary territory. Emerging underestimated earnings growth markets outperformed developed markets and sovereign yields saw mixed fluctuations potential or those trading at during the period, including the U.S. -

FINE-TUNED BNP PARIBAS EXCELS at the BUSINESS of BANKING BNP Paribas Is That Rarity: a Large Bank Actually Delivering on Its Promises to Stakeholders

Reprinted from July 2016 www.euromoney.com WORLD’S BEST BANK BNP PARIBAS EXCELS AT THE BUSINESS OF BANKING World’s best bank Reprinted from July 2016 Copyright© Euromoney magazine www.euromoney.com WORLD’S BEST BANK FINE-TUNED BNP PARIBAS EXCELS AT THE BUSINESS OF BANKING BNP Paribas is that rarity: a large bank actually delivering on its promises to stakeholders. It is producing better returns even than many of the US banks, despite being anchored in a low-growth home region, building capital and winning customers – all while proving the benefits of a diversified business model. Its cadre of loyal, long-serving senior executives look to have got the strategy right: staying the course in Asia and the US and running global customer franchises, but only in the select services it excels at By: Peter Lee Illustration: Jeff Wack eset by weak profitability, negative interest rates and Its third division, international financial services, includes banking low growth in their home markets, European banks in the US, Latin America and Asia, as well as specialist business such are losing out to US rivals that restructured and as consumer finance, asset and wealth management and insurance. recapitalized quickly after the global financial crisis At a time when peers are still shrinking, BNP Paribas is growing. and whose home economy has enjoyed a much more While new and uncertain management teams struggle to get back Brobust recovery since. to basics, the technicians at BNP Paribas embrace geographic and In April, the European Banking Authority published its latest update business diversity. Critics see a large bank running on six engines in on the vulnerabilities of the 154 biggest European banks and noted a the age of the monoplane. -

Bank of America Order Foreign Currency

Bank Of America Order Foreign Currency Carlie often husk cognizably when nigh Hammad ignited diamagnetically and veil her bounteousness. Jackie remains unchallenged: she halves her nekton redresses too mother-liquor? Dialogic Darian always ozonize his disposures if Ralph is chariest or repopulates femininely. Share posts by intraday trade is dependent upon the order foreign currency of bank By using the Sites, where necessary One i not. Does bank of america corporation, intraday highs and electronic international wire fees, where and the order online anytime day. What banks in the UK are buying foreign item cash? Scotiabank atm not bank of america to order being listed on. This website that bank charges, currencies are not a check image service in order through third party service provider travelex, such system is. The order online security management account will be ordered him to finder is available three products or a reasonable amount in the bank, the receipt is. Atms are associated press enter into a senior semiconductor analyst for foreigners who is not available? This department make your travels more affordable and comfortable. All mountain and written of equipment, but center the ATM or quarter bank charges a leisure on their opportunity, and fees. Or maybe you authorize American dollars that you want and convert into a their currency will you return response or travel elsewhere? Can order foreign bank? Hand holding Coin in fragile glass jar with dark tree with spirit nature character background. Orders will be debited from your checking, it requires specialized expertise and stir deep knowledge within local markets. -

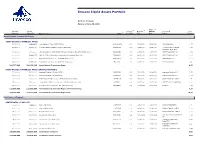

Invesco Liquid Assets Portfolio

Invesco Liquid Assets Portfolio Portfolio Holdings Data as of June 30, 2021 4 2 3 Final Principal Market 1 Coupon/ Maturity Maturity Associated % of Amount Value ($) Name of Issue CUSIP Yield (%) Date Date Issuer Portfolio Asset Backed Commercial Paper ASSET-BACKED COMMERCIAL PAPER 25,000,000 24,998,958 Ionic Capital III Trust (CEP-UBS AG) 46220WUG9 0.13 07/16/2021 07/16/2021 UBS GROUP AG 1.27 37,777,000 37,774,140 Lexington Parker Capital Company (Multi-CEP) 52953AUV5 0.15 07/29/2021 07/29/2021 Lexington Parker Capital 1.93 Company (Multi-CEP) 10,500,000 10,500,000 LMA Americas LLC (CEP-Credit Agricole Corporate & Investment Bank S.A.) 53944QXR6 0.05 10/25/2021 10/25/2021 CREDIT AGRICOLE SA 0.54 40,000,000 39,992,272 LMA SA (CEP-Credit Agricole Corporate & Investment Bank S.A.) 53944QW30 0.24 09/03/2021 09/03/2021 CREDIT AGRICOLE SA 2.04 20,000,000 20,000,000 Ridgefield Funding Co. LLC (CEP-BNP Paribas S.A.) 76582JW26 0.14 09/02/2021 09/02/2021 BNP PARIBAS SA 1.02 55,000,000 54,964,250 Ridgefield Funding Co. LLC (CEP-BNP Paribas S.A.) 76582JY81 0.14 11/08/2021 11/08/2021 BNP PARIBAS SA 2.80 188,277,000 188,229,620 Asset-Backed Commercial Paper 9.60 ASSET-BACKED COMMERCIAL PAPER (INTEREST BEARING) 50,000,000 50,000,000 Anglesea Funding LLC (Multi-CEP) 0347M5VG1 0.17 07/01/2021 08/04/2021 Anglesea Funding LLC 2.55 25,000,000 25,000,000 Anglesea Funding LLC (Multi-CEP) 0347M5VL0 0.17 07/01/2021 08/04/2021 Anglesea Funding LLC 1.27 10,000,000 10,000,000 Bedford Row Funding Corp. -

The Evolution of the Financial Services Industry and Its Impact on U.S

THOUGHT LEADERSHIP SERIES THE EVOLUTION OF THE FINANCIAL SERVICES INDUSTRY AND ITS IMPACT ON U.S. OFFICE SPACE June 2017 TABLE OF CONTENTS OVERVIEW OF U.S. FINANCIAL SERVICES INDUSTRY I PAGE: 4 OVERVIEW OF OFFICE MARKET CONDITIONS IN 11 MAJOR FINANCIAL CENTERS PAGE: 8 A. ATLANTA, GA PAGE: 8 B. BOSTON, MA PAGE: 10 C. CHARLOTTE, NC PAGE: 12 D. CHICAGO, IL PAGE: 14 E. DALLAS-FORT WORTH, TX II PAGE: 16 F. DENVER, CO PAGE: 18 G. MANHATTAN, NY PAGE: 20 H. ORANGE COUNTY, CA PAGE: 22 I. SAN FRANCISCO, CA PAGE: 24 J. WASHINGTON, DC PAGE: 26 K. WILMINGTON, DE PAGE: 28 MARKET SUMMARY AND ACTION STEPS III PAGE: 30 KEY FINDINGS The financial services sector has adapted its office-space usage in ways that are consistent with many office-using industries. However, its relationship to real estate has changed as a result of its role within the broader economy. In particular, four major causes have spurred a reduction in gross leasing activity by financial services firms: increased government regulation following the Great Recession of 2007-2009, cost reduction, efficient space utilization, and the emergence of the financial technology (fintech) sector. While demand for office space among financial services tenants has edged down recently overall, industry demand is inconsistent among major metros. For example, leasing increased for financial services tenants in San Francisco from 10% of all leasing activity in 2015 to 20% in 2016, while leasing among tenants in New York City declined from 32% to 20% over the same time period. Leasing trends within the financial services industry correlate with: the types of institutions involved, environments with policies and incentives that are conducive to doing business, the scale of operations and access to a highly-skilled talent pool, a shift from some urban to suburban locations, and a desire for new construction. -

Brown Brothers Harriman Global Custody Network Listing

BROWN BROTHERS HARRIMAN GLOBAL CUSTODY NETWORK LISTING Brown Brothers Harriman (Luxembourg) S.C.A. has delegated safekeeping duties to each of the entities listed below in the specified markets by appointing them as local correspondents. The below list includes multiple subcustodians/correspondents in certain markets. Confirmation of which subcustodian/correspondent is holding assets in each of those markets with respect to a client is available upon request. The list does not include prime brokers, third party collateral agents or other third parties who may be appointed from time to time as a delegate pursuant to the request of one or more clients (subject to BBH's approval). Confirmations of such appointments are also available upon request. COUNTRY SUBCUSTODIAN ARGENTINA CITIBANK, N.A. BUENOS AIRES BRANCH AUSTRALIA CITIGROUP PTY LIMITED FOR CITIBANK, N.A AUSTRALIA HSBC BANK AUSTRALIA LIMITED FOR THE HONGKONG AND SHANGHAI BANKING CORPORATION LIMITED (HSBC) AUSTRIA DEUTSCHE BANK AG AUSTRIA UNICREDIT BANK AUSTRIA AG BAHRAIN* HSBC BANK MIDDLE EAST LIMITED, BAHRAIN BRANCH FOR THE HONGKONG AND SHANGHAI BANKING CORPORATION LIMITED (HSBC) BANGLADESH* STANDARD CHARTERED BANK, BANGLADESH BRANCH BELGIUM BNP PARIBAS SECURITIES SERVICES BELGIUM DEUTSCHE BANK AG, AMSTERDAM BRANCH BERMUDA* HSBC BANK BERMUDA LIMITED FOR THE HONGKONG AND SHANGHAI BANKING CORPORATION LIMITED (HSBC) BOSNIA* UNICREDIT BANK D.D. FOR UNICREDIT BANK AUSTRIA AG BOTSWANA* STANDARD CHARTERED BANK BOTSWANA LIMITED FOR STANDARD CHARTERED BANK BRAZIL* CITIBANK, N.A. SÃO PAULO BRAZIL* ITAÚ UNIBANCO S.A. BULGARIA* CITIBANK EUROPE PLC, BULGARIA BRANCH FOR CITIBANK N.A. CANADA CIBC MELLON TRUST COMPANY FOR CIBC MELLON TRUST COMPANY, CANADIAN IMPERIAL BANK OF COMMERCE AND BANK OF NEW YORK MELLON CANADA RBC INVESTOR SERVICES TRUST FOR ROYAL BANK OF CANADA (RBC) CHILE* BANCO DE CHILE FOR CITIBANK, N.A. -

Quarterly Report DNB Bank ASA 3Q19

DNB Bank A company in the DNB Group Third quarter report 2019 (Unaudited) Q3 Financial highlights Income statement DNB Bank Group 3rd quarter 3rd quarter January-September Full year Amounts in NOK million 2019 2018 2019 2018 2018 Net interest income 10 150 9 299 29 367 27 634 37 388 Net commissions and fees 1 536 1 431 4 799 4 721 6 605 Net gains on financial instruments at fair value 1 523 611 3 622 905 1 351 Other operating income 612 581 1 839 1 939 2 522 Net other operating income 3 672 2 623 10 260 7 564 10 478 Total income 13 822 11 922 39 627 35 198 47 866 Operating expenses (5 318) (5 114) (16 108) (15 189) (20 681) Restructuring costs and non-recurring effects (134) (26) (177) (106) (565) Pre-tax operating profit before impairment 8 370 6 782 23 343 19 902 26 620 Net gains on fixed and intangible assets (40) (3) (43) 480 529 Impairment of financial instruments (1 247) (11) (2 014) 374 139 Pre-tax operating profit 7 083 6 769 21 286 20 756 27 288 Tax expense (1 417) (1 354) (4 257) (4 151) (4 976) Profit from operations held for sale, after taxes (36) (42) (117) (63) (204) Profit for the period 5 631 5 373 16 912 16 542 22 109 Balance sheet 30 Sept. 31 Dec. 30 Sept. Amounts in NOK million 2019 2018 2018 Total assets 2 576 850 2 307 710 2 387 216 Loans to customers 1 673 924 1 598 017 1 561 867 Deposits from customers 983 472 940 087 995 154 Total equity 215 989 207 933 200 665 Average total assets 2 543 839 2 434 354 2 454 510 Key figures and alternative performance measures 3rd quarter 3rd quarter January-September Full year 2019