Abe-San Goes, Suga-San Comes Reversal Winners

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Real Estate Sector 4 August 2015 Japan

Deutsche Bank Group Markets Research Industry Date Real estate sector 4 August 2015 Japan Real Estate Yoji Otani, CMA Akiko Komine, CMA Research Analyst Research Analyst (+81) 3 5156-6756 (+81) 3 5156-6765 [email protected] [email protected] F.I.T.T. for investors Last dance Bubbles always come in different forms With the big cliff of April 2017 in sight, enjoy the last party like a driver careening to the cliff's brink. Japan is now painted in a completely optimistic light, with the pessimism which permeated Japan after the Great East Japan Earthquake in 2011 forgotten and expectations for the 2020 Tokyo Olympics riding high. The bank lending balance to the real estate sector is at a record high, and we expect bubble-like conditions in the real estate market to heighten due to increased investment in real estate to save on inheritance taxes. History repeats itself, but always in a slightly different form. We have no choice but to dance while the dance music continues to play. ________________________________________________________________________________________________________________ Deutsche Securities Inc. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 124/04/2015. Deutsche Bank Group Markets Research Japan Industry Date 4 August 2015 Real Estate Real estate sector FITT Research Yoji Otani, CMA Akiko Komine, CMA Research Analyst Research Analyst Last dance (+81) 3 5156-6756 (+81) 3 5156-6765 [email protected] [email protected] Bubbles always come in different forms Top picks With the big cliff of April 2017 in sight, enjoy the last party like a driver Mitsui Fudosan (8801.T),¥3,464 Buy careening to the cliff's brink. -

NOTICE of the CONVOCATION of the 148Th ORDINARY GENERAL MEETING of SHAREHOLDERS

This document has partly been translated from the Japanese original for reference purposes only. In the event of any discrepancy between this translated document and the Japanese original, the original shall prevail. The Company assumes no responsibility for this translation or for direct, indirect or any other forms of damages arising from the translation. Securities Code: 4021 May 31, 2018 To Those Shareholders with Voting Rights Kojiro Kinoshita Representative Director, President & CEO Nissan Chemical Industries, Ltd. 7-1, Kanda Nishiki-cho 3-chome, Chiyoda-ku, Tokyo, JAPAN NOTICE OF THE CONVOCATION OF THE 148th ORDINARY GENERAL MEETING OF SHAREHOLDERS You are cordially invited to attend the 148th Ordinary General Meeting of Shareholders of Nissan Chemical Industries, Ltd. (the “Company”). The meeting will be held as described below. If you are unable to attend the meeting, you can exercise your voting rights by either of the following means. Please review the Reference Documents for the General Meeting of Shareholders, and exercise your voting rights. Exercise of Voting Rights in Writing Please indicate your votes for or against the proposals on the enclosed Voting Rights Exercise Form and return it to the Company, ensuring that the form reaches us by 5:40 p.m., Tuesday, June 26, 2018. Exercise of Voting Rights via the Internet, etc. Please access the website for exercising voting rights as indicated in the enclosed Voting Rights Exercise Form and exercise your voting rights by 5:40 p.m., Tuesday, June 26, 2018 (please refer to page 2 hereof). 1. Date and Time: Wednesday, June 27, 2018 at 10:00 a.m. -

Stoxx® Japan 600 Esg-X Index

STOXX® JAPAN 600 ESG-X INDEX Components1 Company Supersector Country Weight (%) Toyota Motor Corp. Automobiles & Parts Japan 3.87 Sony Corp. Consumer Products & Services Japan 2.55 Softbank Group Corp. Telecommunications Japan 2.44 Keyence Corp. Industrial Goods & Services Japan 1.77 RECRUIT HOLDINGS Industrial Goods & Services Japan 1.54 Mitsubishi UFJ Financial Group Banks Japan 1.48 Shin-Etsu Chemical Co. Ltd. Chemicals Japan 1.36 Nippon Telegraph & Telephone C Telecommunications Japan 1.36 Nintendo Co. Ltd. Consumer Products & Services Japan 1.30 Nidec Corp. Technology Japan 1.30 Fast Retailing Co. Ltd. Retail Japan 1.25 Daikin Industries Ltd. Construction & Materials Japan 1.19 Takeda Pharmaceutical Co. Ltd. Health Care Japan 1.18 Tokyo Electron Ltd. Technology Japan 1.16 Honda Motor Co. Ltd. Automobiles & Parts Japan 1.10 Daiichi Sankyo Co. Ltd. Health Care Japan 1.08 Sumitomo Mitsui Financial Grou Banks Japan 1.04 Murata Manufacturing Co. Ltd. Technology Japan 1.03 KDDI Corp. Telecommunications Japan 1.02 Hitachi Ltd. Industrial Goods & Services Japan 0.92 Itochu Corp. Industrial Goods & Services Japan 0.92 Fanuc Ltd. Industrial Goods & Services Japan 0.90 Hoya Corp. Health Care Japan 0.84 Mitsubishi Corp. Industrial Goods & Services Japan 0.83 Mizuho Financial Group Inc. Banks Japan 0.76 SOFTBANK Telecommunications Japan 0.75 Denso Corp. Automobiles & Parts Japan 0.72 Mitsui & Co. Ltd. Industrial Goods & Services Japan 0.71 Tokio Marine Holdings Inc. Insurance Japan 0.70 Oriental Land Co. Ltd. Travel & Leisure Japan 0.68 SMC Corp. Industrial Goods & Services Japan 0.68 Mitsubishi Electric Corp. Industrial Goods & Services Japan 0.67 Seven & I Holdings Co. -

Directors Auditors

Management Team (As of June 26, 2019) 5 Shinichi Hayashi 6 Motoya Aizawa Director and Managing Officer External Director In charge of Real Estate Solutions Department Apr. 1984 Joined Heiwa Real Estate Co., Ltd. (the Company) Apr. 1965 Joined Nippon Kangyo Securities Co., Ltd. (currently Mizuho Securities Co., Ltd.) Apr. 2007 Manager of Nagoya Branch of the Company Nov. 1973 Managing Director of Aizawa Securities Co., Ltd. Jun. 2010 General Manager, Group Leader of Building Sales Group, Leasing Headquarters of the Company Dec. 1979 President and CEO of Aizawa Securities Co., Ltd. 5 Jun. 2011 General Manager, Group Leader of Building Sales Group, Leasing Headquarters of the Company Jun. 1998 Chairman of Aizawa Securities Co., Ltd. Jun. 2012 Managing Officer (current position) in charge of the Redevelopment of the Nihonbashi Kabutocho Jun. 2008 Chairman and President of Aizawa Securities Co., Ltd. 4 3 2 District, and Group Leader of Building Sales Group, Leasing Headquarters of the Company Jun. 2010 External Director of Heiwa Real Estate Co., Ltd. (current position) 11 Jun. 2013 In charge of the Headquarters of Redevelopment of the Nihonbashi Kabutocho District Jun. 2011 President and CEO of Aizawa Securities Co., Ltd. May 2015 General Manager of Real Estate Marketing Department and in charge of Real Estate Jul. 2018 Chairman of Aizawa Securities Co., Ltd. 10 Marketing Department of the Company Oct. 2018 Chairman and CEO of Aizawa Securities Co., Ltd. Jun. 2015 In charge of Property Management Department of the Company Jun. 2019 Senior Advisor of Aizawa Securities Co., Ltd. (current position) Jul. 2016 Manager of Sapporo Branch of the Company 8 Jun. -

ACXW Avantis International Small Cap Value

American Century Investments® Quarterly Portfolio Holdings Avantis® International Small Cap Value ETF (AVDV) May 28, 2021 Avantis International Small Cap Value ETF - Schedule of Investments MAY 28, 2021 (UNAUDITED) Shares/ Principal Amount ($) Value ($) COMMON STOCKS — 99.4% Australia — 8.0% Adairs Ltd. 64,691 233,414 Adbri Ltd. 444,216 1,141,164 Aeris Resources Ltd.(1) 238,800 31,179 Alkane Resources Ltd.(1)(2) 152,741 103,278 Alliance Aviation Services Ltd.(1) 50,306 171,065 Asaleo Care Ltd. 212,115 229,790 Aurelia Metals Ltd. 716,008 245,064 Austal Ltd. 283,491 520,718 Australian Finance Group Ltd. 186,297 400,567 Australian Pharmaceutical Industries Ltd. 419,111 373,258 Bank of Queensland Ltd. 555,800 3,869,929 Beach Energy Ltd. 2,204,143 2,167,414 Bendigo & Adelaide Bank Ltd. 252,445 2,042,517 Boral Ltd.(1) 116,988 619,401 Calix Ltd.(1) 39,671 84,060 Cedar Woods Properties Ltd. 8,294 45,011 Champion Iron Ltd.(1) 492,380 2,502,893 Collins Foods Ltd. 16,697 160,894 Coronado Global Resources, Inc.(1) 453,537 242,887 CSR Ltd. 651,143 2,799,491 Dacian Gold Ltd.(1) 129,467 28,363 Deterra Royalties Ltd. 179,435 579,460 Eclipx Group Ltd.(1) 432,641 710,525 Emeco Holdings Ltd.(1) 476,645 332,757 EML Payments Ltd.(1) 327,130 862,970 Galaxy Resources Ltd.(1) 3,318 9,808 Genworth Mortgage Insurance Australia Ltd.(1) 442,504 945,096 Gold Road Resources Ltd. 660,222 763,347 GrainCorp Ltd., A Shares 347,275 1,343,019 Grange Resources Ltd. -

ACZH Avantis International Small Cap Value

American Century Investments® Quarterly Portfolio Holdings Avantis® International Small Cap Value Fund May 28, 2021 Avantis International Small Cap Value Fund - Schedule of Investments MAY 28, 2021 (UNAUDITED) Shares/ Principal Amount ($) Value ($) COMMON STOCKS — 98.5% Australia — 8.0% Adairs Ltd. 10,087 36,395 Adbri Ltd. 41,613 106,901 Aeris Resources Ltd.(1) 194,638 25,413 Alkane Resources Ltd.(1)(2) 23,444 15,852 Alliance Aviation Services Ltd.(1) 9,551 32,478 Asaleo Care Ltd. 55,544 60,172 Aurelia Metals Ltd. 117,534 40,228 Austal Ltd. 40,665 74,694 Australian Finance Group Ltd. 27,184 58,450 Australian Pharmaceutical Industries Ltd. 57,039 50,799 Bank of Queensland Ltd. 50,470 351,413 Beach Energy Ltd. 256,312 252,041 Bega Cheese Ltd. 10,686 47,626 Bendigo & Adelaide Bank Ltd. 28,090 227,274 Boral Ltd.(1) 23,590 124,899 Brickworks Ltd. 3,303 53,477 Byron Energy Ltd.(1) 7,834 635 Calix Ltd.(1) 13,271 28,120 Champion Iron Ltd.(1) 59,052 300,176 Class Ltd. 1,392 1,856 Coronado Global Resources, Inc.(1) 116,275 62,270 CSR Ltd. 61,819 265,781 Dacian Gold Ltd.(1) 57,096 12,508 Eclipx Group Ltd.(1) 40,478 66,477 Emeco Holdings Ltd.(1) 64,744 45,199 EML Payments Ltd.(1) 32,108 84,701 Fleetwood Ltd. 1,403 2,649 Galaxy Resources Ltd.(1) 50,126 148,165 Genworth Mortgage Insurance Australia Ltd.(1) 23,355 49,881 Gold Road Resources Ltd. 119,473 138,134 GrainCorp Ltd., A Shares 46,105 178,302 Grange Resources Ltd. -

VIRTUS ALLIANZGI INTERNATIONAL SMALL-CAP FUND SCHEDULE of INVESTMENTS (Unaudited) JUNE 30, 2021

VIRTUS ALLIANZGI INTERNATIONAL SMALL-CAP FUND SCHEDULE OF INVESTMENTS (Unaudited) JUNE 30, 2021 ($ reported in thousands) Shares Value Shares Value Shares Value PREFERRED STOCK—1.4% Germany—continued Netherlands—continued Jenoptik AG 36,671 $ 1,003 ASR Nederland NV 28,191 $ 1,090 Germany—1.4% Scout24 AG 12,804 1,080 Jungheinrich AG 24,964 $ 1,220 2,396 7,828 TOTAL PREFERRED STOCK New Zealand—0.4% (Identified Cost $558) 1,220 Hong Kong—4.0% Eroad Ltd.(1) 77,475 338 Hutchmed China Ltd. ADR(1) 32,400 1,272 Norway—3.2% COMMON STOCKS—96.6% (1) Melco International Elkem ASA 382,528 1,392 (1) Storebrand ASA 157,554 1,427 Australia—5.4% Development Ltd. 313,000 575 ALS Ltd. 110,041 1,076 Techtronic Industries Co., 2,819 Ansell Ltd. 8,707 284 Ltd. 36,000 629 Bapcor Ltd. 91,762 585 VTech Holdings Ltd. 92,600 975 South Korea—1.0% Nick Scali Ltd. 60,321 530 3,451 Koh Young Technology, Inc. 41,490 877 Northern Star Resources Sweden—2.9% Ltd. 32,100 235 Ireland—1.6% AAK AB 53,435 1,198 Openpay Group Ltd.(1) 87,481 94 Grafton Group plc 86,460 1,372 Elekta AB Class B 88,983 1,289 Paradigm Biopharmaceuticals Italy—2.7% 2,487 Ltd.(1) 182,378 287 Buzzi Unicem SpA 44,177 1,172 Pro Medicus Ltd. 21,200 934 ERG SpA 41,083 1,218 Switzerland—4.8% Starpharma Holdings Ltd.(1) 585,545 657 2,390 Georg Fischer AG 1,100 1,632 Interroll Holding AG 389 1,543 4,682 Japan—26.4% OC Oerlikon Corp. -

Printmgr File

November 30, 2020 Semi-Annual Report DBX ETF Trust Xtrackers Eurozone Equity ETF (EURZ) Xtrackers International Real Estate ETF (HAUZ) Xtrackers Japan JPX-Nikkei 400 Equity ETF (JPN) DBX ETF Trust Table of Contents Page Shareholder Letter ....................................................................... 1 Portfolio Summary Xtrackers Eurozone Equity ETF ......................................................... 3 Xtrackers International Real Estate ETF .................................................. 4 Xtrackers Japan JPX-Nikkei 400 Equity ETF .............................................. 5 Fees and Expenses ....................................................................... 6 Schedules of Investments Xtrackers Eurozone Equity ETF ......................................................... 7 Xtrackers International Real Estate ETF .................................................. 12 Xtrackers Japan JPX-Nikkei 400 Equity ETF .............................................. 21 Statements of Assets and Liabilities ........................................................ 26 Statements of Operations ................................................................. 27 Statements of Changes in Net Assets ....................................................... 28 Financial Highlights ...................................................................... 30 Notes to Financial Statements ............................................................. 32 Additional Information ................................................................... -

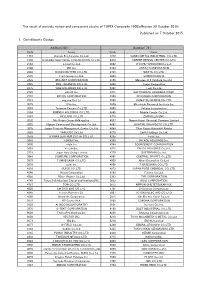

Published on 7 October 2015 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 30 October 2015) Published on 7 October 2015 1. Constituents Change Addition( 80 ) Deletion( 72 ) Code Issue Code Issue 1712 Daiseki Eco.Solution Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 1930 HOKURIKU ELECTRICAL CONSTRUCTION CO.,LTD. 2410 CAREER DESIGN CENTER CO.,LTD. 2183 Linical Co.,Ltd. 2692 ITOCHU-SHOKUHIN Co.,Ltd. 2198 IKK Inc. 2733 ARATA CORPORATION 2266 ROKKO BUTTER CO.,LTD. 2735 WATTS CO.,LTD. 2372 I'rom Group Co.,Ltd. 3004 SHINYEI KAISHA 2428 WELLNET CORPORATION 3159 Maruzen CHI Holdings Co.,Ltd. 2445 SRG TAKAMIYA CO.,LTD. 3204 Toabo Corporation 2475 WDB HOLDINGS CO.,LTD. 3361 Toell Co.,Ltd. 2729 JALUX Inc. 3371 SOFTCREATE HOLDINGS CORP. 2767 FIELDS CORPORATION 3396 FELISSIMO CORPORATION 2931 euglena Co.,Ltd. 3580 KOMATSU SEIREN CO.,LTD. 3079 DVx Inc. 3636 Mitsubishi Research Institute,Inc. 3093 Treasure Factory Co.,LTD. 3639 Voltage Incorporation 3194 KIRINDO HOLDINGS CO.,LTD. 3669 Mobile Create Co.,Ltd. 3197 SKYLARK CO.,LTD 3770 ZAPPALLAS,INC. 3232 Mie Kotsu Group Holdings,Inc. 4007 Nippon Kasei Chemical Company Limited 3252 Nippon Commercial Development Co.,Ltd. 4097 KOATSU GAS KOGYO CO.,LTD. 3276 Japan Property Management Center Co.,Ltd. 4098 Titan Kogyo Kabushiki Kaisha 3385 YAKUODO.Co.,Ltd. 4275 Carlit Holdings Co.,Ltd. 3553 KYOWA LEATHER CLOTH CO.,LTD. 4295 Faith, Inc. 3649 FINDEX Inc. 4326 INTAGE HOLDINGS Inc. 3660 istyle Inc. 4344 SOURCENEXT CORPORATION 3681 V-cube,Inc. 4671 FALCO HOLDINGS Co.,Ltd. 3751 Japan Asia Group Limited 4779 SOFTBRAIN Co.,Ltd. 3844 COMTURE CORPORATION 4801 CENTRAL SPORTS Co.,LTD. -

Ief-I Q3 2020

Units Cost Market Value INTERNATIONAL EQUITY FUND-I International Equities 96.98% International Common Stocks AUSTRALIA ABACUS PROPERTY GROUP 1,012 2,330 2,115 ACCENT GROUP LTD 3,078 2,769 3,636 ADBRI LTD 222,373 489,412 455,535 AFTERPAY LTD 18,738 959,482 1,095,892 AGL ENERGY LTD 3,706 49,589 36,243 ALTIUM LTD 8,294 143,981 216,118 ALUMINA LTD 4,292 6,887 4,283 AMP LTD 15,427 26,616 14,529 ANSELL LTD 484 8,876 12,950 APA GROUP 14,634 114,162 108,585 APPEN LTD 11,282 194,407 276,316 AUB GROUP LTD 224 2,028 2,677 AUSNET SERVICES 9,482 10,386 12,844 AUSTRALIA & NEW ZEALAND BANKIN 19,794 340,672 245,226 AUSTRALIAN PHARMACEUTICAL INDU 4,466 3,770 3,377 BANK OF QUEENSLAND LTD 1,943 13,268 8,008 BEACH ENERGY LTD 3,992 4,280 3,824 BEGA CHEESE LTD 740 2,588 2,684 BENDIGO & ADELAIDE BANK LTD 2,573 19,560 11,180 BHP GROUP LTD 16,897 429,820 435,111 BHP GROUP PLC 83,670 1,755,966 1,787,133 BLUESCOPE STEEL LTD 9,170 73,684 83,770 BORAL LTD 6,095 21,195 19,989 BRAMBLES LTD 135,706 987,557 1,022,317 BRICKWORKS LTD 256 2,997 3,571 BWP TRUST 2,510 6,241 7,282 CENTURIA INDUSTRIAL REIT 1,754 3,538 3,919 CENTURIA OFFICE REIT 154,762 199,550 226,593 CHALLENGER LTD 2,442 13,473 6,728 CHAMPION IRON LTD 1,118 2,075 2,350 CHARTER HALL LONG WALE REIT 2,392 8,444 8,621 CHARTER HALL RETAIL REIT 174,503 464,770 421,358 CHARTER HALL SOCIAL INFRASTRUC 1,209 2,007 2,458 CIMIC GROUP LTD 4,894 73,980 65,249 COCA-COLA AMATIL LTD 2,108 12,258 14,383 COCHLEAR LTD 1,177 155,370 167,412 COMMONWEALTH BANK OF AUSTRALIA 12,637 659,871 577,971 CORONADO GLOBAL RESOURCES INC 1,327 -

Integrated Report 2020 Contents

Staying Ahead of the Times to Provide New Value Integrated Report 2020 Contents P 2 Track Record of Mitsubishi Estate P 50 ESG Section and Its Business Expansion 52 Materiality 54 Environment (E) Mitsubishi Estate’s Strengths P 5 55 TCFD 6 Marunouchi Today 56 Human Resources and Diversity (S) “A Love for People 57 Resilience (S) Mitsubishi Estate’s Value Creation Model P 8 58 SASB 59 Corporate Governance (G) P 10 Message from the President A Love for the City ” 59 Message from the Chairman of the Board 60 Directors Overview of Long-Term Management Plan 2030 P 14 61 Corporate Executive Officers, Executive Officers, Forever Taking On New Challenges—The Mitsubishi Estate Group 16 The Group’s Strengths and Growth Strategies and Group Executive Officers 18 Road Map for 2030 62 Characteristics of Corporate Governance System 64 Evaluation of the Effectiveness of the Board of 20 SPECIAL FEATURE 1 Domestic Asset Business Directors / Remuneration CO • MO • RE YOTSUYA The Spirit of Mitsubishi: Three Principles 65 Shares Held for Strategic Purposes 22 SPECIAL FEATURE International Asset Business 2 66 Message from an Outside Director “Shoki Hoko” “Shoji Komei” “Ritsugyo Boeki” Condominium Business in Bangkok, Thailand 68 Risk Management 24 SPECIAL FEATURE 3 Non-Asset Business Corporate Responsibility to Society Integrity and Fairness Global Understanding through Business Participation in the Elevator Media Business Strive to enrich society, both materially Maintain principles of transparency Expand business, P 71 Financial Section and spiritually, while contributing and openness, based on an all-encompassing 26 Message from the Corporate Officer in Charge of toward the preservation of conducting business with global perspective. -

American Century Investments® Quarterly Portfolio Holdings Avantis

American Century Investments® Quarterly Portfolio Holdings Avantis® International Equity ETF (AVDE) November 30, 2020 Avantis International Equity ETF - Schedule of Investments NOVEMBER 30, 2020 (UNAUDITED) Shares/ Principal Amount ($) Value ($) COMMON STOCKS — 99.7% Australia — 6.5% Accent Group Ltd. 14,526 23,059 Adairs Ltd. 9,223 21,547 Adbri Ltd. 12,481 28,274 Afterpay Ltd.(1) 48 3,354 AGL Energy Ltd. 8,984 89,075 Alkane Resources Ltd.(1)(2) 41,938 31,367 Alliance Aviation Services Ltd.(1) 5,187 13,148 ALS Ltd. 2,039 14,302 Altium Ltd. 1,563 40,787 Alumina Ltd. 16,346 20,996 AMA Group Ltd.(1) 16,885 9,258 AMP Ltd. 223,348 280,458 Ampol Ltd. 2,595 58,421 Ansell Ltd. 1,333 36,644 APA Group 16,232 123,383 Appen Ltd. 1,821 42,222 ARB Corp. Ltd. 3,172 64,616 Ardent Leisure Group Ltd.(1) 22,550 13,624 Aristocrat Leisure Ltd. 12,775 300,907 ASX Ltd. 1,422 80,525 Atlas Arteria Ltd. 5,725 27,252 Atlassian Corp. plc, Class A(1) 2,086 469,454 Aurelia Metals Ltd. 60,190 18,351 Aurizon Holdings Ltd. 113,756 355,100 AusNet Services 71,401 97,009 Austal Ltd. 23,896 51,252 Australia & New Zealand Banking Group Ltd. 67,427 1,121,525 Australian Agricultural Co. Ltd.(1) 32,331 25,519 Australian Ethical Investment Ltd. 3,654 13,530 Australian Finance Group Ltd. 21,308 37,254 Australian Pharmaceutical Industries Ltd. 29,606 26,147 Bank of Queensland Ltd.