Comprehensive Annual Financial Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cape May County Voter Registration

Cape May County A Profile of Cape May County New Jersey Avalon ● Cape May ● Cape May Court House ● Cape May Point ● Dennis Township ● Lower Township ● Middle Township ● North Wildwood ● Ocean City ● Sea Isle City ● Stone Harbor ● Upper Township ● West Cape May ● West Wildwood ● Wildwood ● Wildwood Crest ● Woodbine Table of Contents Overview and Geographical Background ..................................................................................................... 3 Housing Density........................................................................................................................................ 4 Transportation ........................................................................................................................................... 5 Public Transportation ............................................................................................................................ 5 County Road Mileage ........................................................................................................................... 6 Commute: Travel Time to Work ........................................................................................................... 7 Demographics ............................................................................................................................................... 8 Population (2010) ..................................................................................................................................... 8 Race (2010) .............................................................................................................................................. -

ESSER II LEA Allocations (March 2021)

New Jersey Department of Education Elementary and Secondary School Emergency Relief (ESSER) Fund Local Education Agency (LEA) Allocations as of March 12, 2021 ESSER I Title I Allocation County County District Status (includes funds for Name Code Code Name (Y or N) nonpublic schools) Atlantic 01 0010 Absecon Public Schools District Y $ 232,945 Atlantic 01 0110 Atlantic City School District Y $ 3,977,177 Atlantic 01 0125 Atlantic County Special Services School District N $ 15,000 Atlantic 01 0120 Atlantic County Vocational School District Y $ 468,868 Atlantic 01 0570 Brigantine Public School District Y $ 210,406 Atlantic 01 0590 Buena Regional School District Y $ 766,392 Atlantic 01 1300 Egg Harbor City School District Y $ 243,850 Atlantic 01 1310 Egg Harbor Township School District Y $ 1,154,885 Atlantic 01 1410 Estell Manor School District Y $ 34,931 Atlantic 01 1540 Folsom Borough School District Y $ 60,490 Atlantic 01 1690 Galloway Township Public Schools Y $ 657,068 Atlantic 01 1790 Greater Egg Harbor Regional High School District Y $ 575,150 Atlantic 01 1940 Hamilton Township School District Y $ 548,921 Atlantic 01 1960 Hammonton School District Y $ 710,222 Atlantic 01 2680 Linwood City School District Y $ 54,356 Atlantic 01 2910 Mainland Regional High School Y $ 147,940 Atlantic 01 3020 Margate City School District Y $ 48,451 Atlantic 01 3480 Mullica Township School District Y $ 159,718 Atlantic 01 3720 Northfield City School District Y $ 222,573 Atlantic 01 4180 Pleasantville Public School District Y $ 1,267,320 Atlantic 01 4240 -

New Jersey Student Climate Challenge Eligible Schools

NEW JERSEY STUDENT CLIMATE CHALLENGE ELIGIBLE SCHOOLS Important Note: Schools in the districts listed below serving six grade students and K‐6 districts in Atlantic City Electric's service territory that are not listed are also eligible to participate. Please email [email protected] if you have any questions regarding your school's elibility. COUNTY DISTRICT SCHOOL Atlantic Absecon Public Schools District Emma C Attales Atlantic Atlantic City School District Atlantic City High School Atlantic Atlantic City School District Chelsea Heights School Atlantic Atlantic City School District Dr Martin Luther King Jr School Complex Atlantic Atlantic City School District New York Avenue School Atlantic Atlantic City School District Pennsylvania Ave School Atlantic Atlantic City School District Richmond Avenue School Atlantic Atlantic City School District Sovereign Avenue School Atlantic Atlantic City School District Texas Avenue School Atlantic Atlantic City School District Uptown School Complex Atlantic Atlantic County Special Services School District Atlantic County High School Atlantic Atlantic County Vocational School District Atlantic County Alternative High School Atlantic Atlantic County Vocational School District Atlantic County Institute Of Technology Atlantic Brigantine Public School District Brigantine Community School Atlantic Buena Regional School District Buena Regional School District Atlantic Buena Regional School District Buena Regional School District Atlantic Chartertech High School For The Performing -

ESSER I Allocation Atlantic 01 0010 Absecon Public Schools Di

New Jersey Department of Education Elementary and Secondary School Emergency Relief (ESSER) Fund Local Education Agency (LEA) Allocations as of March 29, 2021 ESSER I Title I Allocation County County District Status (includes funds for Name Code Code Name (Y or N) nonpublic schools) Atlantic 01 0010 Absecon Public Schools District Y $ 232,945 Atlantic 01 0110 Atlantic City School District Y $ 3,977,177 Atlantic 01 0125 Atlantic County Special Services School District N $ 15,000 Atlantic 01 0120 Atlantic County Vocational School District Y $ 468,868 Atlantic 01 0570 Brigantine Public School District Y $ 210,406 Atlantic 01 0590 Buena Regional School District Y $ 766,392 Atlantic 01 1300 Egg Harbor City School District Y $ 243,850 Atlantic 01 1310 Egg Harbor Township School District Y $ 1,154,885 Atlantic 01 1410 Estell Manor School District Y $ 34,931 Atlantic 01 1540 Folsom Borough School District Y $ 60,490 Atlantic 01 1690 Galloway Township Public Schools Y $ 657,068 Atlantic 01 1790 Greater Egg Harbor Regional High School District Y $ 575,150 Atlantic 01 1940 Hamilton Township School District Y $ 548,921 Atlantic 01 1960 Hammonton School District Y $ 710,222 Atlantic 01 2680 Linwood City School District Y $ 54,356 Atlantic 01 2910 Mainland Regional High School Y $ 147,940 Atlantic 01 3020 Margate City School District Y $ 48,451 Atlantic 01 3480 Mullica Township School District Y $ 159,718 Atlantic 01 3720 Northfield City School District Y $ 222,573 Atlantic 01 4180 Pleasantville Public School District Y $ 1,267,320 Atlantic 01 4240 -

Houston, Texas 77092 (713) 744-6835 NOTICE

7145 West Tidwell Road ~ Houston, Texas 77092 (713) 744-6835 www.esc4.net Publication Date: August 28, 2014 NOTICE TO OFFEROR SUBMITTAL DEADLINE: Wednesday, October 8, 2014 @ 2:00 PM CDT Questions regarding this solicitation must be submitted in writing to Robert Zingelmann at [email protected] or (713) 744-6835 no later than October 1, 2014 . All questions and answers will be posted to both www.esc4.net and www.tcpn.org under Solicitations . Offerors are responsible for viewing either website to review all questions and answers prior to submitting proposals . Please note that oral communications concerning this RFP shall not be binding and shall in no way excuse the responsive Offeror of the obligations set forth in this proposal. Request for Proposal (RFP) by Region 4 Education Service Center (“ESC”) for School Supplies On behalf of itself, other government agencies and non-profits, made available through The Cooperative Purchasing Network “TCPN.” Solicitation Number 14-16 Note: Envelopes must be sealed, prominently marked with the RFP solicitation number, RFP title, RFP opening time/date and name of vendor. Electronic submissions of the RFP will not be accepted. Submissions must be received by the Region 4 ESC office at: 7145 West Tidwell Road, Houston, TX 77092 no later than 2:00 pm CDT, at which time the bid opening process shall commence. Proposals will be collected in a conference room to be determined by Region 4 ESC and opened and recorded publicly. Page 1 of 158 ATTENTION OFFERORS : Submission of a proposal confers NO RIGHT on an Offeror to an award or to a subsequent contract. -

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27

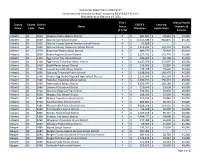

ABCDEFGH 1 TEACHER AND PRINCIPAL EVALUATIONS 2014-15 2 Chart shows the number of teachers who were rated in each category 3 If there were fewer than 10 in any category is is marked with an * 4 5 COUNTY_NAMDISTRICT CATEGORY INEFFECTIVEPARTIALLY_EEFFECTIVE HIGHLY_EFFECTIVETOTAL 6 ATLANTIC Absecon Public Schools TEACHERS * * 36 36 72 7 ATLANTIC Absecon Public Schools PRIN/AP/VP * * * * 2 8 ATLANTIC Atlantic City Public Schools TEACHERS * * 555 84 655 9 ATLANTIC Atlantic City Public Schools PRIN/AP/VP * * * 20 22 10 ATLANTIC Atlantic County Vocational School District TEACHERS * * 95 21 116 11 ATLANTIC Atlantic County Vocational School District PRIN/AP/VP * * * * 3 12 ATLANTIC Atlantic County Special Services School District TEACHERS * * 55 10 66 13 ATLANTIC Atlantic County Special Services School District PRIN/AP/VP * * * * 4 14 ATLANTIC Brigantine Public Schools TEACHERS * * * 65 69 15 ATLANTIC Brigantine Public Schools PRIN/AP/VP * * * * 2 16 ATLANTIC BUENA REGIONAL SCHOOL DISTRICT TEACHERS * * 140 17 159 17 ATLANTIC EGG HARBOR CITY SCHOOL DISTRICT TEACHERS * 25 17 * 44 18 ATLANTIC EGG HARBOR TOWNSHIP SCHOOL DISTRICT TEACHERS * * 336 236 573 19 ATLANTIC EGG HARBOR TOWNSHIP SCHOOL DISTRICT PRIN/AP/VP * * 10 * 19 20 ATLANTIC ESTELL MANOR CITY SCHOOL DISTRICT TEACHERS * * * * 15 21 ATLANTIC Folsom Borough School District TEACHERS * * 11 27 38 22 ATLANTIC GALLOWAY TOWNSHIP PUBLIC SCHOOLS TEACHERS * * 251 34 285 23 ATLANTIC GALLOWAY TOWNSHIP PUBLIC SCHOOLS PRIN/AP/VP * * * * 11 24 ATLANTIC Greater Egg Harbor Regional High School DistrictTEACHERS -

(ESSER II) Fund Allocations As of February 19, 2021

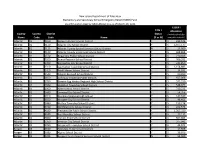

New Jersey Department of Education Elementary and Secondary School Emergency Relief (ESSER II) Fund Allocations as of February 19, 2021 Title I Mental Health County County District ESSER II Learning Name Status Supports & Name Code Code Allocation Acceleration (Y or N) Services Atlantic 01 0010 Absecon Public Schools District Y $ 684,684 $ 43,940 $ 45,000 Atlantic 01 0110 Atlantic City School District Y $ 15,315,588 $ 982,876 $ 45,000 Atlantic 01 0125 Atlantic County Special Services School District N $ 91,828 $ - $ - Atlantic 01 0120 Atlantic County Vocational School District Y $ 1,816,193 $ 116,554 $ 45,000 Atlantic 01 0570 Brigantine Public School District Y $ 886,773 $ 56,909 $ 45,000 Atlantic 01 0590 Buena Regional School District Y $ 2,224,702 $ 142,770 $ 45,000 Atlantic 01 1300 Egg Harbor City School District Y $ 946,922 $ 60,768 $ 45,000 Atlantic 01 1310 Egg Harbor Township School District Y $ 4,247,076 $ 272,555 $ 45,000 Atlantic 01 1410 Estell Manor School District Y $ 135,503 $ 25,000 $ 45,000 Atlantic 01 1540 Folsom Borough School District Y $ 235,208 $ 25,000 $ 45,000 Atlantic 01 1690 Galloway Township Public Schools Y $ 2,188,936 $ 140,475 $ 45,000 Atlantic 01 1790 Greater Egg Harbor Regional High School District Y $ 2,231,309 $ 143,194 $ 45,000 Atlantic 01 1940 Hamilton Township School District Y $ 2,030,751 $ 130,323 $ 45,000 Atlantic 01 1960 Hammonton School District Y $ 2,620,797 $ 168,189 $ 45,000 Atlantic 01 2680 Linwood City School District Y $ 210,699 $ 25,000 $ 45,000 Atlantic 01 2910 Mainland Regional High School -

Schools and Libraries 2Q2014 Funding Year 2012 Authorizations - 4Q2013 Page 1 of 242

Universal Service Administrative Company Appendix SL36 Schools and Libraries 2Q2014 Funding Year 2012 Authorizations - 4Q2013 Page 1 of 242 Applicant Name City State Primary Authorized 100 ACADEMY OF EXCELLENCE NORTH LAS VEGAS NV 2,226.64 A B C UNIFIED SCHOOL DISTRICT CERRITOS CA 185,395.78 A W BEATTIE AVTS DISTRICT ALLISON PARK PA 40.02 A-C COMM UNIT SCHOOL DIST 262 ASHLAND IL 24,190.44 A.W. BROWN FELLOWSHIP CHARTER SCHOOL DALLAS TX 48,883.09 AAA ACADEMY POSEN IL 6,767.38 AB GRAHAM ACADEMY ST PARIS OH 2,720.16 ABBE REGIONAL LIBRARY AIKEN SC 14,462.00 ABBEVILLE SENIOR HIGH SCHOOL ABBEVILLE LA 3,428.26 ABERDEEN PUBLIC LIBRARY ABERDEEN ID 1,476.19 ABERDEEN SCHOOL DISTRICT ABERDEEN MS 210,537.19 ABERDEEN SCHOOL DISTRICT 5 ABERDEEN WA 34.06 ABERDEEN SCHOOL DISTRICT 58 ABERDEEN ID 657.79 ABILENE FREE PUBLIC LIBRARY ABILENE KS 126.00 ABILENE UNIF SCH DISTRICT 435 ABILENE KS 466.67 ABINGDON COMM SCHOOL DIST 217 ABINGDON IL 10,841.01 ABINGTON SCHOOL DISTRICT ABINGTON MA 263.69 ABINGTON SCHOOL DISTRICT ABINGTON PA 387.78 ABRAHAM JOSHUA HESCHEL SCHOOLS NEW YORK NY 53,061.25 ABSAROKEE SCHOOL DIST 52-52 C ABSAROKEE MT 1,346.85 ABSECON PUBLIC SCHOOL DISTRICT ABSECON NJ 5,279.68 ABYSSINIAN DEVELOPMENT CORPORATION NEW YORK NY 1,374.89 ACADEMIA ADVENTISTA DEL OESTE SECUNDARIA MAYAGUEZ PR 1,910.16 Academia Bautista Sotera Sanchez Canovanas PR 1,255.72 ACADEMIA BAUTISTE DE YAUCO YAUCO PR 2,595.60 ACADEMIA CESAR CHAVEZ SAINT PAUL MN 3,691.46 Academia del Sagrado Corazon Santurce PR 4,165.78 ACADEMIA DISCIPULOS DE CRISTO EN VEGA ALTA VEGA ALTA PR 3,198.60 Academia Disipulos de Cristo (7-12) Bayamon PR 9,338.76 ACADEMIA ELOHIM CAGUAS PR 17,568.90 ACADEMIA JULIO TORRES RODRIGUEZ, INC. -

Cape May County, New Jersey PSAP Consolidation Dispatch Study

Cape May County, New Jersey PSAP Consolidation Dispatch Study FINAL REPORT Prepared by: INTERTECH ASSOCIATES 77-55 Schanck Road, Suite A-14, Freehold, NJ 07728 732.431.4236 www.intertechassociates.com January 20, 2014 Cape May County, New Jersey PSAP Consolidation Dispatch Study Table of Contents Volume I: Executive Summary ................................................. 1 1.0 Overview: Executive Summary .................................................................. 2 1.1 Background and Demographics................................................................. 2 1.2 Findings .................................................................................................... 3 1.3 Regionalization Models .............................................................................. 5 1.4 Operational Findings ................................................................................. 6 1.5 Financial Findings .................................................................................... 7 1.6 Recommendation: Barrier Island/Mid-County Communications Center ..... 8 1.7 Conclusion .............................................................................................. 11 Tables: Table 1.1 Cape May County PSAPs .................................................................. 4 Volume II: Existing Conditions ............................................... 12 2.0 Overview: Executive Summary ................................................................ 13 2.1 Findings Summary ................................................................................. -

News Di Gests

Herald Prayers Answered; Assumption Remains Open NEWS By LAUREN SUIT merge with St. Ann Church in Wildwood and last April, Galante has been met with protests would remain open only part of the year, under at his public appearances. DI GESTS WILDWOOD CREST — The Church of the the diocese’s original restructuring plan. On June 11, Assumption parishioners fi lled Assumption won’t have to close its doors in this A parish merger was one fate that some the sanctuary pews in an effort to show Galante borough at the end of the season. churches in this diocese face during a process that their parish is fi ghting to keep their spiri- On Guard Bishop of Camden Joseph A. Galante an- called “gathering God’s gifts.” The restructur- tual identity as many churches in the Diocese CREST HAVEN — County Health De- nounced Aug. 26 that Assumption would be ing is a response by the Catholic Church that of Camden are looking toward restructuring. partment tests of 69 ocean and bay recre- allowed to hold services through the whole has more parishes than there are worshipers, Outside, hundreds of parishioners walked ational sites Aug. 22 found 10 locations that year. priests, or money to sustain them. past members of other churches in the diocese exceeded the state-set limit for enterococcus The Church of the Assumption was slated to Since the restructuring plan was announced (Page A4 Please) bacteria of 104 per 100-milliter sample. Those readings dropped to acceptable levels since that date. For updated reports, call the hotline: 465-2422. -

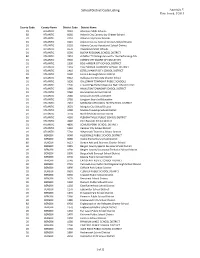

Appendix V Date Issued: 5/2015

School District Code Listing Appendix V Date Issued: 5/2015 County Code County Name District Code District Name 01 ATLANTIC 0010 Absecon Public Schools 80 ATLANTIC 6060 Atlantic City Community Charter School 01 ATLANTIC 0110 Atlantic City Public Schools 01 ATLANTIC 0125 Atlantic County Special Services School District 01 ATLANTIC 0120 Atlantic County Vocational School District 01 ATLANTIC 0570 Brigantine Public Schools 01 ATLANTIC 0590 BUENA REGIONAL SCHOOL DISTRICT 80 ATLANTIC 7410 chARTer~TECH High School for the Performing Arts 01 ATLANTIC 0960 CORBIN CITY BOARD OF EDUCATION 01 ATLANTIC 1300 EGG HARBOR CITY SCHOOL DISTRICT 01 ATLANTIC 1310 EGG HARBOR TOWNSHIP SCHOOL DISTRICT 01 ATLANTIC 1410 ESTELL MANOR CITY SCHOOL DISTRICT 01 ATLANTIC 1540 Folsom Borough School District 80 ATLANTIC 6612 Galloway Community Charter School 01 ATLANTIC 1690 GALLOWAY TOWNSHIP PUBLIC SCHOOLS 01 ATLANTIC 1790 Greater Egg Harbor Regional High School District 01 ATLANTIC 1940 HAMILTON TOWNSHIP SCHOOL DISTRICT 01 ATLANTIC 1960 Hammonton School District 01 ATLANTIC 2680 Linwood City School District 01 ATLANTIC 2780 Longport Board of Education 01 ATLANTIC 2910 MAINLAND REGIONAL HIGH SCHOOL DISTRICT 01 ATLANTIC 3020 Margate City School District 01 ATLANTIC 3480 Mullica Township School District 01 ATLANTIC 3720 Northfield City School District 01 ATLANTIC 4180 PLEASANTVILLE PUBLIC SCHOOL DISTRICT 01 ATLANTIC 4240 Port Republic School District 01 ATLANTIC 4800 SOMERS POINT SCHOOL DISTRICT 01 ATLANTIC 5350 Ventnor City School District 01 ATLANTIC 5760 Weymouth Township -

Carahsoft Technology Corp

CARAHSOFT’S RESPONSE TO THE The Cooperative Purchasing Network REQUEST FOR PROPOSAL Software and Related Products and Services SOLICITATION NO. 15-04 Tuesday March 3, 2015 CARAHSOFT TECHNOLOGY CORP. 12369 SUNRISE VALLEY DRIVE RESTON, VA 20191 888.66.CARAH | WWW.CARAHSOFT.COM carahsoft March 3, 2015 TCPN Region 4 ESC Office 7145 West Tidwell Road Houston, TX 77092 Re: Carahsoft’s Response to The Cooperative Purchasing Network’s Request for Proposal for Software and Related Products and Services, Solicitation # 15-04 Dear Mr. Zingelmann, Carahsoft Technology Corporation appreciates the opportunity to respond to The Cooperative Purchasing Network (TCPN)’s Request for Proposal for Software and Related Products and Services. Carahsoft is proposing its entire product line, which fully meets TCPN’s requirements for Software and Related Products and Services. Our team has considered TCPN’s requirements outlined in the Request for Proposal, and has carefully put together a solution that will best meet your needs. Carahsoft is submitting as a current TCPN contract holder (#R5011) and top rated IT reseller and distributor. Carahsoft has utilized the TCPN contract to sell over $3,000,000 in IT products and services to various agencies. Carahsoft has delivered best value solutions to our government and education clients for over ten years, including Region IV and TCPN’s member agencies. In fact, Carahsoft has delivered almost $100,000,000 in sales to Education agencies in 2014, and has completed $15,000,000 of those sales in the State of Texas. Please feel free to contact me directly at 703.230.7545/[email protected] or Robert Moore at 703.871.8504/[email protected] with any questions or communications that will assist TCPN in the evaluation of our response.