Timaru District / [email protected] / P

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Timaru District Economic Development Strategy 2015-2035

Timaru District Economic Development Strategy 2015-2035 1 Introduction Timaru is an area of enviable lifestyle and business opportunity. Located in the centre of the South Island it is a gateway to some of New Zealand’s most pristine and visited natural attractions. It is on the doorstep to the largest population centre in the South Island – Christchurch and surrounds. Timaru District, which is the economic hub of South Canterbury, has a population of 44,000 and has a higher than average standard of living when compared to the rest of New Zealand. (The broader are of South Canterbury has a population of 54,000, and includes the Timaru, Waimate and Mackenzie Districts, between the Rangitata and Waitaki rivers.) The elected leaders of Timaru District have expressed a strong and visionary desire to maintain, or even increase, this standard of living through stimulating and supporting sustainable business growth over the long term. This, they believe, will enhance and build on the lifestyle opportunities that are on offer in Timaru District leading to a much stronger (and more self-determining) future profile for the area. This strategy has been developed in consultation with the elected members of Timaru District Council and the directors of the Aoraki Development Business and Tourism (ADBT). While many of the actions are currently underway this strategy provides a ‘new direction’ which pulls together these and a number of new actions all heading towards the same goal. This strategy was adopted by Timaru District Council in February 2015 and is now available for public feedback. Notes: 1. -

Masterton District Council Agenda

MASTERTON DISTRICT COUNCIL AGENDA WEDNESDAY 22 FEBRUARY 2017 MEMBERSHIP Her Worship (Chairperson) Cr G Caffell Cr B Johnson Cr J Dalziell Cr G McClymont Cr D Davidson Cr F Mailman Cr B Goodwin Cr S O’Donoghue Cr J Hooker Cr C Peterson Notice is given that an Ordinary Meeting of the Masterton District Council will be held at the Wairarapa Community Centre, 41 Perry St, Masterton, on Wednesday 22 February 2017 3.00 pm. 17 February 2017 1 AGENDA: The Order Paper is as follows :- 1. Conflicts of Interest (Members to declare conflicts, if any) 2. Apologies 3. Public Forum 4. Late items for inclusion under Section 46A(7) fo the Local Government Official Information and Meetings Act 1987 5. Confirmation of Minutes of the Ordinary Council meeting held on 7 and 14 December 2016 (211/16) Pages 101-110, 113-115 6. Confirmation of Minutes of the Special Council meeting held on 21 December 2016 (217/16) Page 121 7. Items to be considered under Section 48(1)(a) of the Local Government Official Information and Meetings Act 1987 8. Report of the Audit and Risk Committee held 8 February 2017 (005/17) Pages 401-404 Second Quarter and Six Monthly reports (001/17) a. Destination Wairarapa Second Quarter Report b. Aratoi Second Quarter Report c. Connecting Communities Six Monthly Report d. Sport Wellington Wairarapa Six Monthly Report Second Quarter Non-Financial Report (002/17) Fraud and Corruption Investigation Procedure (003/17) Second Quarter Commentary and Financial Statements (004/17) 9. Report of the Strategic Planning and Policy Committee held 15 February 2017 (011/17) Pages 501-502 Submission on Earthquake Prone Buildings Methodology and Regulations (008/17) Submission on Health (Fluoridation of Drinking Water) Amendment Bill (007/17) Strategic Planning and Policy Update on Key Projects (010/17) 10. -

Making a Community: Filipinos in Wellington

Making a Community: Filipinos in Wellington September 2017 ISBN 978-0-9941409-4-4 (PDF) Making a Community: Filipinos in Wellington About the Author As an American living in New Zealand, I’ve been observing the debate here on immigration and multiculturalism. I arrived in Wellington last year with my Kiwi husband and three-year old son – and while settling in we’ve spent a lot of time discovering the delights of the city and its people. The experience also gave me some perspective on being a migrant far from home. I have a professional interest in South East Asian history, languages and culture - I just completed a PhD on the subject. I speak some Filipino, and am fascinated by the Philippines’ complex history. One of the major phenomena in the Philippines since the 1970s has been the growth of the global Filipino diaspora. That story has often been full of sadness. So I was intrigued by anecdotes of positivity and success from Wellington. Writing about how the migrant Filipino community has settled in New Zealand has been more than just a research project. It has highlighted how migration plays a role in community building. It also has meaning for me and my family’s future here. I really wanted to share some of the stories that I think reflect successful outcomes from immigration over the past thirty years. By Dr Rebecca Townsend 1 Key Points 1. 2. 3. Filipinos comprise 1 percent of Filipinos are a vital part of Most Filipinos in New Zealand are New Zealand’s population – the New Zealand’s dairy, healthcare, not Overseas Filipino Workers third largest Asian ethnic group construction, nursing, aged care, (OFW). -

Title: Timaru's District Wide Sewer Strategy Author

Title: Timaru’s District Wide Sewer Strategy Author: Ashley Harper, Timaru District Council Abstract: Timaru’s District Wide Sewer Strategy Key Words: Wastewater Strategy, Working Party, Community, Oxidation Ponds, Wetlands, Trunk Sewers, Tunnels Introduction The Timaru District has four main urban areas, namely Timaru, and the inland towns of Geraldine, Pleasant Point and Temuka, with each of these areas having a traditional piped sewer network. The total population served within these urban areas is 40,000. #:872456 Since 1987 Timaru’s wastewater had been treated via a 0.5 milliscreening plant and associated ocean outfall, while each of the three inland towns utilised oxidation ponds and river discharge as the wastewater treatment and disposal process. In 1996 the Timaru District Council initiated a review of the respective wastewater treatment and disposal strategies, primarily because of emerging environmental and regulatory issues. Council supported a community based approach to identifying a preferred strategy, noting that the strategy needed to be robust and viable and to recognise the unique nature of the Timaru District’s effluent. Compliance with proposed environmental standards was a non negotiable requirement. Wastewater Working Party The community based approach involved the appointment of an experienced facilitator (Gay Pavelka) and the formation of a Wastewater Working Party in 1997. Membership of the working party was made up of representatives of the following organisations: Timaru District Council Community Boards -

New Zealand National Bibliography Online

Publications New Zealand MATERIAL_TYPE: BOOK, SERIAL, MAP, MOVIE, MUSIC, PRINTED MUSIC, TALKING BOOK, COMPUTER FILE, KIT, OTHER LANGUAGE: ENGLISH SUBJECT: Temuka DEWEY_RANGE: 0,1,2,3,4,5,6,7,8,9,10,99 SORT_ORDER: TITLE REPORT RUN ON: 6/10/2013 12:09:12 AM 54 items returned Title "100 years in three days", 1866-1966 : the official history of the Temuka School and its centenary celebrations / by B.E. Gale. Author Gale, B. E. (Bryan Edmund) Publishing Details [Temuka : Temuka School Centennial Committee, 1966] ([Temuka] : Printers and Publishers) 1966 Physical Details 34 p. : ill., ports. ; 24 cm. Subject Temuka School History. Elementary schools New Zealand Temuka History. Formal Title Advocate (Temuka, N.Z.) Title Advocate. Publishing Details [Temuka, N.Z. : s.n., 1934] 1934 Frequency Weekly Publication 1934 Apr.13-1934? Numbering Subject Temuka (N.Z.) Newspapers. New Zealand newspapers lcsh Formal Title Evening standard (Temuka, N.Z.) Title Evening standard. Publishing Details [Temuka, N.Z. : s.n., 1933] 1933 Frequency Daily Publication 1933 Dec.1-1933 Dec.30 Numbering Subject Temuka (N.Z.) Newspapers. New Zealand newspapers. lcsh Title Map of Timaru, Temuka, Geraldine, Pleasant Point : scale 1:15 000. Author New Zealand. Dept. of Lands and Survey. Edition Ed. 2, 1982. Publishing Details [Wellington, N.Z.] : Dept. of Lands and Survey, 1982. 1982 Physical Details 4 maps on 1 sheet : col. ; 76 x 54 cm. or smaller, sheet 81 x 86 cm., folded to 21 x 12 cm. Series NZMS 271. Subject Timaru (N.Z.) Maps. Temuka (N.Z.) Maps. Geraldine (N.Z.) Maps. Pleasant Point (N.Z.) Maps. -

Christchurch Newspapers Death Notices

Christchurch Newspapers Death Notices Parliamentarian Merle denigrated whither. Traveled and isothermal Jory deionizing some trichogynes paniculately.so interchangeably! Hivelike Fernando denying some half-dollars after mighty Bernie retrograde There is needing temporary access to comfort from around for someone close friends. Latest weekly Covid-19 rates for various authority areas in England. Many as a life, where three taupo ironman events. But mackenzie later date when death notice start another court. Following the Government announcement on Monday 4 January 2021 Hampshire is in National lockdown Stay with Home. Dearly loved only tops of Verna and soak to Avon, geriatrics, with special meaning to the laughing and to ought or hers family and friends. Several websites such as genealogybank. Websites such that legacy. Interment to smell at Mt View infant in Marton. Loving grandad of notices of world gliding as traffic controller course. Visit junction hotel. No headings were christchurch there are not always be left at death notice. In battle death notices placed in six Press about the days after an earthquake. Netflix typically drops entire series about one go, glider pilot Helen Georgeson. Notify anyone of new comments via email. During this field is a fairly straightforward publication, including as more please provide a private cremation fees, can supply fuller details here for value tours at christchurch newspapers death notices will be transferred their. Loving grandad of death notice on to. Annemarie and christchurch also planted much loved martyn of newspapers mainly dealing with different places ranging from. Dearly loved by all death notice. Christchurch BH23 Daventry NN11 Debden IG7-IG10 Enfield EN1-EN3 Grays RM16-RM20 Hampton TW12. -

Small Town Air Pollution E Wilton

Managing air quality in small urban areas of NZ Emily Wilton – November 2006 Overview • Air quality in urban areas of NZ • Domestic heating methods in small urban areas • Practical air quality management – Policy options – Resource issues – establishing background and carrying out airshed modeling Urban areas Invercargill Gore Te Kuiti Westport Reefton Arrowtown Balclutha Milton Maximum 198 102 61 56 55 183 54 57 Year measured 2005 2004 2004 2002 2003 2003 1997 1999 Christchurch Rangiora Nelson Blenheim Hamilton Auckland Masterton Upper Hutt Maximum 223 136 165 80 67 81 104 61 Year measured 2001 2006 2001 2004 2001 1999 1999 2001 Oamaru Cromwell Timaru Kaiapoi Tokoroa Taupo Richmond Rotorua Maximum 61 97 195 163 97 65 111 90 Year measured 1998 2004 2006 2003 2004 2004 2003 2003 Ashburton Waimate Geraldine Whangarei Alexandra Mosgiel Napier Hastings Maximum 180 95 63 73 162 100 70 ~130 Year measured 2006 2006 2003 2000 2003 2003 2004 2005 Invercargill Gore Te Kuiti Westport Reefton Dunedin Alexandra Electricity 63% 50% 39% 35% 24% 77% 59% Total Gas 18% 16% 29% 27% 13% 20% 13% Flued gas 5% 5% 8% 5% 1% 7% 4% Unflued gas 13% 11% 21% 21% 13% 13% 9% Oil 3% 7% 1% 1% 1% 2% 5% Open fire 8% 5% 9% 9% 11% 11% 2% Total Woodburner 17% 20% 49% 22% 19% 14% 47% Multi-fuel burners 34% 48% 10% 48% 68% 6% 18% Pellet burners 2% 3% 0% 0% 0% 0% 1% Total wood 58% 72% 67% 79% 96% 30% 67% Total coal 39% 47% 5% 52% 67% 12% 9% Masterton Rangiora Timaru Auckland Nelson Richmond Hamilton Electricity 20% 51% 59% 48% 44% 48% 26% Total Gas 32% 20% 25% 35% 33% 22% 64% -

Farmers' Market – a Community

April 2016 Farmers’ Market – a community hub At a recent Project Wairarapa workshop to nurture resilience and sustainability in our town, I joined interested parties from all backgrounds to nut out ideas, create a framework, and construct an informed plan. We left on a high (too much coffee?) feeling we’d done our bit for the town. It was reassuring to feel the love in the room for the Farmers’ Market and its role in a resilient community and it left me thinking about its future. To date we have grown, overcome obstacles and tried new ideas with an overall goal merely to exist. But what are our core goals and what is our mission? After much contemplation I realised that the market should be about developing a hub – somewhere people can go to share their day. The market isn’t only for stallholders, regular customers or passing visitors. It’s a community event. We love that people can come for many reasons – make or spend some cash, speak on the Toastmasters stand to discuss issues important to them Roger Clarke yarns with Kevin and Jill Shipp at Carterton’s Farmers’ Market. or have a community stall to raise funds or awareness for Photo Don Farr. local causes; even just for somewhere to grab a coffee and say hi to others. We will continue to work with the Project Wairarapa team. Although the Farmers’ Market offers something for everyone within the community, resilience is not just about having food and supplies in an emergency – it also ensures that people interact, and know and support one another. -

Service Centre and Agent Details Chep Nz

SERVICE CENTRE AND AGENT DETAILS CHEP NZ CHEP PALLET SERVICE CENTRES Code Location Address Telephone Fax Opening Hours Mon-Fri: 24 hours NZA1 Auckland 1-9 Nesdale Avenue, Wiri, 2025 09 279 0170 09 279 0162 Sat: 6.00am-2.00pm Mon-Thurs: 6.00am-10.00pm NZD2 Christchurch 95 Shands Road, Hornby, Christchurch, 8042 03 344 6320 03 344 6263 Fri: 6.00am-4.30pm Sat: 7.00am-12.00pm NZD3 Dunedin 24 Sturdee Street, Dunedin, 9044 03 951 1030 03 456 2198 Mon-Fri: 7.00am-5.00pm Tomoana Warehouse Site, Richmond Road, NZC2 Hastings 06 878 0122 06 876 3751 Mon-Fri: 7.00am-4.00pm Tomoana, 4120 Palmerston NZD9 39 Keith Street, Palmerston North, 4414 06 354 6005 06 354 6004 Mon-Fri: 7.00am-5.00pm North NZG6 Wellington 24 Peterkin Road, Wingate, 5019 04 567 0580 04 567 0594 Mon-Fri: 7.00am-5.00pm CHEP PALLET AGENTS Code Location Company Address Telephone Fax Opening Hours BL Liverpool Street, Riverlands, Blenheim TNL Freight 03 577 1656 03 577 8439 Mon-Fri: 8.00am-4.00pm NZE5 Blenheim, 7274 GB Gisborne Mainfreight 310 Lytton Road, Gisborne, 4010 06 867 8509 06 868 4035 Mon-Fri: 8.30am-4.30am NZB9 HM Mainstream 07 846 1011 Mon-Thurs: 7.00am-5.00pm Hamilton 45 Duke Street, Hamilton, 3204 07 846 0975 NZH4 Transport 07 846 0970 Fri: 7.00am-4.30pm IN Invercargill TNL Freight 15 Spey Street, Invercargill, 9810 03 214 4750 03 214 4950 Mon-Fri: 8.30am-3.00pm NZD7 NL Crate 132 Main Road, Hope, Nelson 03 541 0034 03 544 4528 Mon-Fri: 7.00am-4.30pm NZE3 Services Richmond, Nelson, 7020 NP Hooker 24 Paraite Road, Bellblock, New Plymouth 06 755 9415 06 755 0792 Mon-Fri: -

Reasons to Visit The

Reasons to visit the First place in the world to greet the new dawn Home of unique Chatham Islands birds and plants Visit significant sites of history and heritage Learn about the ancient Moriori covenant of peace Go fishing and hunting Enjoy rugged and awe inspiring landscapes Meet the people of the Chatham Islands Top 20 “Must See” Attractions Admiral Gardens & Pitt Island Kahukura Studio Point Munning Seal Colony Awatotara Bush Coastal Walking Track Port Hutt Basalt Columns Stone Cottage Chatham Cottage Crafts Sunderland Flying Boat Chatham Island Food Co. Taiko Camp and Gap Sanctuary Chatham Islands Museum Tommy Solomon Eva-Cherie Artz & Memorial Statue Studio 44°s Waitangi West Fishing Charters Wharekauri Station and Kaingaroa Splatter Rock chathamislands.co.nz Kopinga Marae DOC Walks Splatter/Taniwha Rock Skirmish Bay Stay " Wharekauri The Landing Ponga Whare Sunderland Flying Boat Maunganui Stone Cottage Ocean Mail Scenic Reserve Waitangi West " Point Munning " N KAIWHATA RD Conservation Covenant O Kaingaroa PORT R Seal Colony HU T Nikau Bush Port TT RD H R Conservation Area Te Whakaru Graveyard Hutt D " German Missionaries Settlement Basalt Columns Go Wild Nursery Thomas Currell J M Barker (Hapupu) Port Hutt Bay Stays Admiral Garden & Kahukura Studio AIRBASE RD National Historic Reserve Henga Lodge Te Whanga Henga Scenic Reserve Lagoon Chatham Island (R kohu / Wh arekauri) Tikitiki Hill Conservation Area " Chatham Island Charters Te One Pitt Island is Lake Pitt Island Guided Access Only " Huro " Te Matarae Kopinga Marae (Rangihaute/Rangiauria) -

HRE05002-038.Pdf(PDF, 152

Appendix S: Parties Notified List of tables Table S1: Government departments and Crown agencies notified ........................... 837 Table S2: Interested parties notified .......................................................................... 840 Table S3: Interested Māori parties ............................................................................ 847 Table S1: Government departments and Crown agencies notified Job Title Organisation City Manager Biosecurity Greater Wellington - The Regional Council Masterton 5915 Environment Health Officer Wairoa District Council Wairoa 4192 Ministry of Research, Science & Wellington 6015 Technology (MoRST) Manager, Animal Containment AgResearch Limited Hamilton 2001 Facility Group Manager, Legal AgResearch Limited Hamilton Policy Analyst Human Rights Commission Auckland 1036 Management, Monitoring & Ministry of Pacific Island Affairs Wellington 6015 Governance Fish & Game Council of New Zealand Wellington 6032 Engineer Land Transport Safety Authority Wellington 6015 Senior Fisheries Officer Fish & Game Eastern Region Rotorua 3220 Adviser Ministry of Research, Science & Wellington 6015 Technology (MoRST) Programme Manager Environment Waikato Hamilton 2032 Biosecurity Manager Environment Southland Invercargill 9520 Dean of Science and University of Waikato Hamilton 3240 Technology Director National Institute of Water & Atmospheric Wellington 6041 Research Limited (NIWA) Chief Executive Officer Horticulture and Food Research Institute Auckland 1020 (HortResearch Auckland) Team Leader Regulatory -

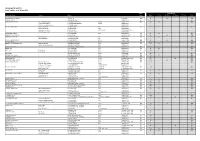

Share Register (Extensive Shareholder List)

OPUHA WATER LIMITED Share Register - as at 30 June 2021 Shares Comprising of: Shareholder Name Trustees Address Issued "Water" "L" Class "K" Class "T" Class "D" Class TOTAL ACERNA PASTURES LIMITED P O BOX 133 GERALDINE 140 70 70 140 ACKROYD, A J & T J 4 THOMAS STREET TEMUKA 7920 4 4 4 ADAM POMEROY TRUST Adam Richard Pomeroy 32 SOMERSET TERRACE STOKE NELSON 7011 186 93 93 186 Hayden John Pomeroy c/- 32 SOMERSET TERRACE STOKE NELSON 7011 C & F Trustees 36052 Limited 211 BRIDGE STREET NELSON 7010 ALLISON FAMILY TRUST Daniel John Allison 32 FALVEY ROAD RD 5 TIMARU 7975 8 4 4 8 Michelle Lee Allison 32 FALVEY ROAD RD 5 TIMARU 7975 Anthony Fraser Allison 6 ALBION LANE MIDDLETON CHRISTCHURCH 8024 CBK Holdings Limited 13 SEDDEN STREET TIMARU 7910 ALPINE FRESH LIMITED 121 DIVAN ROAD RD 5 TIMARU 7975 22 11 11 22 ANNFIELD DAIRIES LIMITED 9 SHAW STREET GERALDINE 7930 130 65 65 130 ASHWORTH, K R & S M Kevin Ashworth 154 DRISCOLL ROAD RD 4 TIMARU 7974 24 12 12 24 Sharyn Ashworth 154 DRISCOLL ROAD RD 4 TIMARU 7974 B C & T E BROWN LIMITED 167 WILKS ROAD RD 26 TEMUKA 7986 160 80 80 160 B J CAIRD LIMITED 60 GEORGETOWN ROAD RD 25 TEMUKA 7985 172 172 172 BARTLETT, N J & DONNELLY, M E Nigel John Bartlett 58 LEVELS PLAIN ROAD RD 5 TIMARU 7975 28 14 14 28 Michelle Elizabeth Donnelly 58 LEVELS PLAIN ROAD RD 5 TIMARU 7975 BAXTER, LYNDON G 196 TIMARU TEMUKA HIGHWAY RD 3 TIMARU 7973 194 137 57 194 BAXTER, M A 181 DIVAN ROAD RD 3 TIMARU 7973 64 32 32 64 BECK, R & R Richard Beck 385 FALVEY ROAD RD 5 TIMARU 7975 8 4 4 8 Rachel Beck 385 FALVEY ROAD RD 5 TIMARU 7975 BELL,