Wm. Wrigley Jr. Company Investor Presentation First Quarter 2005

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Product List - - 1800 854 234

Product List - www.TheProfessors.com.au - 1800 854 234 Allens Marella Jubes (1.3kg bag) Red Vines - Original Red Twists (1 tray x 141g) Bubblicious Fruit Twist Gum (18 packs x 5 gum pieces) Allens Marella Jubes Saver Pack (4 x 190g Bags) Red Vines - Original Red Twists (12 trays x 141g) Bubblicious Watermelon Gum (18 packs x 5 gum pieces) Hershey's Kisses (12 x 150g bags) Allens Milk Bottles (1.3kg bag) Red Vines - Original Red Twists (6 trays x 141g) Cadbury Boost Stix Twin Bar (55g x 30) Sixlets - Black- ( Bulk 4.5kg box) Allens Milko Chews (3kg bag) Red Vines 4lbs tub (240pc - unwrapped red vines in a display tub) Cadbury Buzz (42 x 20g bars in a Display Unit) Sixlets - Gold- ( Bulk 4.5kg box) Allens Milkos (150 Stick Display Unit) Cadbury Caramello Block (10 x 110g blocks) Sixlets - Lime Green- ( Bulk 4.5kg box) Allens Minties (1 kg Bag) Cadbury Caramello Koala (72 x 20gm in a Display Unit) Sweetworld Jelly Pencils (12 x400g hang sell bags) Arnotts Allens Party Mix (1.3 kg Bag) Arnotts Tim Tam Fingers (28 x 40g packs) Cadbury Caramello Rolls (36 x 55g Rolls) AB Food and Beverages Allens Pineapples (1.3kg bag) Arnotts Wagon Wheels (16 x 48g biscuits) Cadbury Cherry Ripe (48 x 52g bars in a display unit) Allens Racing Cars (1.3kg bag) Cadbury Chocolate Fish (42 x 20g in a Display Unit) Ovalteenies (24 bags in a Display Unit) Allens Retro Party Mix (1kg bag) Bassett Cadbury Chomp Caramel Bars (50 bars in Display Unit) AIT Confectionery Allens Ripe Raspberries (1.3kg Bag) Bassetts Pear Drops (12 x 200g bags) Cadbury Crunchie (42 x 50g -

Mars, Incorporated Donates Nearly Half a Million Dollars to Recovery

Mars, Incorporated Donates Nearly Half a Million Dollars to Recovery Efforts Following Severe Winter Storms Cash and in-kind donations will support people and pets in affected Mars communities McLEAN, Va. (February 26, 2021) — In response to the devasting winter storms across many communities in the U.S., Mars, Incorporated announced a donation of nearly $500,000 in cash and in-kind donations, inclusive of a $100,000 donation to American Red Cross Disaster Relief. Grant F. Reid, CEO of Mars said: “We’re grateful that our Mars Associates are safe following the recent destructive and dangerous storms. But, many of them, their families and friends have been impacted along with millions of others We’re thankful for partner organizations like the American Red Cross that are bringing additional resources and relief to communities, people and pets, and we’re proud to play a part in supporting that work.” Mars has more than 60,000 Associates in the U.S. and presence in 49 states. In addition to the $100,000 American Red Cross donation, Mars Wrigley, Mars Food, Mars Petcare and Royal Canin will make in-kind product donations to help people and pets. As an extension of Mars Petcare, the Pedigree Foundation is supporting impacted pets and animal welfare organizations with $25,000 in disaster relief grants. Mars Veterinary Health practices including Banfield Pet Hospital, BluePearl and VCA Animal Hospitals are providing a range of support in local communities across Texas. In addition, the Banfield Foundation and VCA Charities are donating medical supplies, funding veterinary relief teams and the transport of impacted pets. -

NEW PLANT SELECTIONS for 2021 ANNUALS Year of the Sunflower the Sunflower Is One of the Most Popular Genera of Flowers to Grow in Your Garden

NEW PLANT SELECTIONS FOR 2021 ANNUALS Year of the Sunflower The Sunflower is one of the most popular genera of flowers to grow in your garden. First-time to experienced gardeners gravitate to these bold, easy to grow flowers. Sunflowers originated in the Americas and domestic seeds dating back to 2100 BC have been found in Mexico. Native Americans grew sunflowers as a crop, and explorers eventually brought the flowers to Europe in the 1500s. Over the next few centuries, sunflowers became increasingly popular on the European and Asian continent, with Russian farmers growing over 2 million acres in the early 19th century (most of which was used to manufacture sunflower oil). How to Grow and Care for Sunflowers: Sunflower seeds can be direct sown after the risk of frost has passed or started indoors. Seeds should be sown ¼” to ½” deep and kept moist. Taller, larger sunflower varieties have a large taproot to keep them rooted and do not do well when they are transplanted so direct sowing of those varieties is recommended. Choose a site, or a container, in full sun, with average fertility and good drainage. https://ngb.org/year-of-the-sunflower/ Proven Winners 2021 Annual of the Year – Supertunia Mini Vista® Pink Star Meet the newest star in our annual lineup! Take a closer look at Supertunia Mini Vista® Pink Star petunia to find ideas for incorporating it into your garden and learn what it needs to thrive. There’s no denying the popularity of Supertunia Vista® Bubblegum® petunia, and we know you are going to love her “little sister” – Supertunia Mini Vista® Pink Star. -

Retail Gourmet Chocolate

BBuullkk WWrraappppeedd Rock Candy Rock Candy Swizzle Root Beer Barrels Saltwater Taffy nndd Demitasse White Sticks Asst 6.5” 503780, 31lb bulk 577670, 15lb bulk CCaa yy 586670, 100ct 586860, 120ct (approx. 50pcs/lb) (approx. 40pcs/lb) Dryden & Palmer Dryden & Palmer Sunrise Sesame Honey Smarties Starlight, Asst Fruit Starlight Mints Starlight Spearmints Treats 504510, 40lb bulk 503770, 31lb bulk 503760, 31lb 503750, 31lb 586940, 20lb bulk (approx. 64pcs/lb) (approx. 86pcs/lb) (approx. 86pcs/lb) (approx. 80pcs/lb) (approx. 84pcs/lb) 15 tablets per roll Sunrise Sunrise Starburst Fruit Bon Bons, Strawberry Superbubble Gum Tootsie Pops, Assorted Tootsie Roll Midgee, Chews Original 503820, 31lb bulk 584010, 4lb or 530750, 39lb bulk Assorted 534672, 6/41oz (approx. 68pcs/lb) Case-8 (approx. 30pcs/lb) 530710, 30lb bulk bags (approx. 85pcs/lb) Tootsie (approx. 70pcs/lb) Tootsie Tootsie Roll Midgee Thank You Mint, Thank You Mint, Breathsavers 530700, 30lb bulk Chocolate Buttermint MM Wintergreen (approx. 70pcs/lb) 504595, 10lb bulk 504594, 10lb bulk ttss 505310, 24ct (approx. 65pcs/lb) (approx. 100pcs/lb) iinn Breathsavers Breathsavers Mentos, Mixed Fruit Altoids Smalls Altoids Smalls Peppermint Spearmint 505261, 15/1.32oz rolls Peppermint, Cinnamon, 505300, 24ct 505320, 24ct Sugar Free Sugar Free 597531, 9/.37oz 597533, 9/.37oz MM ss Altoids Altoids Altoids Altoids Smalls iinntt Wintergreen Peppermint Cinnamon Wintergreen, 597441, 12/1.76oz 597451, 12/1.75oz 597401, 12/1.76oz Sugar Free tins tins tins 597532, 9/.37oz GGuumm Stride Gum Stride -

Student Hospitalized with Meningitis More Than 80 People Seek Treatment at Student Health Services After Possible Exposure to Virus Saturday

Itt Section 2 In Sports An Associated Collegiate Press Five-Star All-American Newspaper Delaware 26 and a National Pacemaker Geared up for a Del. state 7 primus album This ain't football page 81 FREE FRIDAY Student hospitalized with meningitis More than 80 people seek treatment at Student Health Services after possible exposure to virus Saturday By Stacey Bernstein Wilmington Hospital and was throat discharges of an infected Delucia is Delaware's ninth quarters during the incubation Assistant Fratu~ Editor declared to be in intensive care as person during its incubation case of meningitis since the period. After complaining of chills, a of Wednesday night. Siebold said. period from one to 10 days, most beginning of 1993, as compared In addition, parties and other fever, a headache and a rash, a However, he said, Delucia is commonly being less than four, to two cases in 1992, Siebold social gatherings involved in university student was transferred continuing to improve each day. Siebold said. said. These cases are not related, close personal contact like sharing to Wilmington Hospital and Approximately 80 students, People who should be he said. of beverage glasses may also diagnosed with meningitis who were either at the 271 Towne concerned are those who have However, he said, it is spread the disease. Monday night, officials said. Court party or were in direct come in direct contact with the impossible to know exactly how Siebold said It is hard, Kevin Deluci'a (BE JR), who contact with Delucia, have infected individual, Siebold said. -

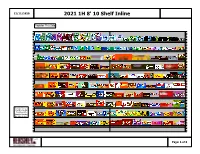

2021 1H 4' 10 Shelf Inline

12/11/2020 2021 1H 8' 10 Shelf Inline Register This Side Replace Reese's Crunchy Cookie Cup King with Reese's Crunchy Bar King in April Page: 1 of 6 12/11/2020 2021 1H 8' 10 Shelf Inline Register This Side 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 Shelf: 10 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 Shelf: 9 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 Shelf: 8 1 2 3 4 5 6 7 8 9 10 11 12 13 14 Shelf: 7 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 Shelf: 6 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Shelf: 5 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Shelf: 4 Replace Reese's 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Crunchy Cookie Shelf: 3 Cup King with Reese's Crunchy Bar King in April 1 2 3 4 5 6 7 8 9 10 11 12 13 14 Shelf: 2 1 2 3 4 5 6 7 8 9 10 11 12 13 14 Shelf: 1 Page: 2 of 6 12/11/2020 2021 1H 8' 10 Shelf Inline Segment-Packtype Mints Bottle & Mega Gum Nonchocolate King and Standard Chocolate King Singles Gum Chocolate Standard Register This Side EXTRA EXTRA EXTRA ICE ICE ICE ICE ICE ICE ICE TRIDENT TRIDENT REFRESHE REFRESHE REFRESHE BREAKERS BREAKERS BREAKERS BREAKERS BREAKERS BREAKERS BREAKERS VIBES S/F MENTOS MENTOS MENTOS VIBES R RS RS S/F CUBE S/F CUBE S/F CUBE S/F CUBE S/F CUBE S/F CUBE S/F CUBE SPEARMINT PURE FRESH PURE FRESH PURE WHITE EXTRA EXTRA 5 COBALT S/F POLAR BERRY 5 RAIN PEPPERMI SPEARMIN WNTRGRN ARCTIC RASPBRY CINN BLK CHR S/F GUM - FRESH GUM - S/F GM SWT SPEARMINT 5 SPRMNT ICE MIX TRIDENT POLAR 35PC 5 RAIN 5 5 DENTYNE TROP BT SPEARMINT MNT 35PC NT T GRAPE SORBT MINT 50PC GUM SGR ICE 35PC 35PC -

Effort to Reduce Carbon Footprint | Press Releases

PRESS RELEASE Wm. Wrigley Jr. Company Launches Effort to Reduce Carbon Footprint Enabled by Infosys Technologies World’s Largest Manufacturer of Chewing Gum Seeks to Transform Logistics Operations in Western Europe London, UK - November 20, 2008: In a move to extend its social responsibility leadership, the world’s leading manufacturer of chewing gum Wm. Wrigley Jr. Company is reducing the carbon footprint it creates in its logistics operations, Infosys Technologies announced today. Infosys is enabling Wrigley to transform its logistics operations by providing solutions and services in a pilot to determine how much carbon emissions are produced and subsequently may be reduced across the company’s truck-based shipping operations in Western Europe. “Managing our impact on the environment is an integral part of Wrigley corporate philosophy,” said Ian Robertson, head of supply chain sustainability at Wm. Wrigley Jr. Company. “We’re committed to making improvements across all operations but need an integrated enterprise system to measure progress. Infosys provided that solution and services to empower that process.” Early in the pilot, Infosys identified logistics operations in which Wrigley may reduce its carbon footprint by as much as 20 percent, and provided process consulting around operational adoption. The analysis will continue to evaluate Wrigley’s complex distribution network across six countries in Western Europe – spanning more than 44 million kilometers a year in shipments between suppliers, the company and its own customers and includes its distribution centers – for CO2 emissions emitted according to the UK’s Defra (Department for Environment, Food and Rural Affairs) standards. Infosys is using its patent-pending Logistics Optimization solution and carbon management tools to deliver the carbon footprint analysis to Wrigley as a managed information service. -

Market Achievements History Product

Wrigley ENG 15.03.2007 12:56 Page 170 Market a confectionery product.These products deliver a Since its founding in 1891,Wrigley has established range of benefits including dental protection itself as a leader in the confectionery industry. It is (Orbit), fresh breath (Winterfresh), enhancing best known for chewing gum and is the world’s memory and improving concentration (Airwaves), largest manufacturer of these products, some of relief of stress, helping in smoking cessation and which are among the best known and loved brands snack avoidance. in the world.Today,Wrigley's brands are woven into Wrigley is one of the pioneers in developing the fabric of everyday life around the world and are the dental benefits of chewing sugarfree gum - sold in over 150 countries.The original brands chewing a sugar-free gum like Orbit reduces the Wrigley’s Spearmint, Doublemint and Juicy Fruit incidence of tooth decay by 40%. Its work and have been joined by the hugely successful brands support in the area of oral healthcare has resulted Orbit,Winterfresh, Airwaves and Hubba Bubba. in dental professionals recommending sugarfree gum Chewing gum consumption in Croatia exceeds to their patients. the amount of 34 million USD and holds 34.8% of the total confectionery market (Nielsen, MAT chewing AM06). In comparison with the past year, the gum companies in the market has witnessed a 3.2% growth, and today, United States, but the industry Wrigley's Orbit is in Croatia a synonym for top was relatively undeveloped. Mr.Wrigley decided that quality chewing gum, holding the leading brand chewing gum was the product with the potential he position in the confectionery category (chocolates had been looking for, so he began marketing it excluded).This product holds 57.4% of the total under his own name. -

February 2014

february 2014 San Diego’s Garden Resource San Diego’s Independent Nursery Since 1928 TM In This Issue The Plants Of Love The Plants Of Love 1 BY MELANIE POTTER Red Roses 2014 Plant Trends 1 The “Plants Of The Year” Are... 1 The nursery used to sell a book entitled, Order early from a florist to avoid being left Words From Walter: Orchids 3 ‘Plants of Love’ by Christian Ratsch which empty handed, or buy your beloved a rose You Can Grow Blueberries 3 detailed the history of aphrodisiacs from A bush. Look for these red roses: Always and Old Ben: Bird Feeding Month 4 to Z, actually Achillea millefolium (Yarrow) Forever, American Dream, Chrysler Imperial, Home Vineyards 5 to Zingiber officinale (Ginger) with garlic, Darcy Bussell, Drop Dead Red, Firefighter, opium, and wheat in between. However, try In the Mood, Ingrid Bergman, Legends, Mr. Tool Shed: Product Highlights 6 passing any of those off as a valentine on Feb. Lincoln, Oh My, Oklahoma, O.L. Weeks, Specials, Coupons & Classes 7 14, and you are guaranteed to spend this day Olympiad, Papa Meilland, Trumpeter, and of love, sleeping solo on the sofa. Veteran’s Honor. Any of these planted now will deliver a bouquet this Discover Us! March or April! www.walterandersen.com Orchids facebook.com/walterandersens I asked our orchid buyer, Emily twitter.com/walterandersens Drury, which orchids would impress her as a gift on February Our Online Store 14, and her suggestions were: Watch Videos Cymbidiums, with their very showy, tall flower spikes that can be grown outside here and The “Plants Of The bloom again next year. -

Kosher Nosh Guide Summer 2020

k Kosher Nosh Guide Summer 2020 For the latest information check www.isitkosher.uk CONTENTS 5 USING THE PRODUCT LISTINGS 5 EXPLANATION OF KASHRUT SYMBOLS 5 PROBLEMATIC E NUMBERS 6 BISCUITS 6 BREAD 7 CHOCOLATE & SWEET SPREADS 7 CONFECTIONERY 18 CRACKERS, RICE & CORN CAKES 18 CRISPS & SNACKS 20 DESSERTS 21 ENERGY & PROTEIN SNACKS 22 ENERGY DRINKS 23 FRUIT SNACKS 24 HOT CHOCOLATE & MALTED DRINKS 24 ICE CREAM CONES & WAFERS 25 ICE CREAMS, LOLLIES & SORBET 29 MILK SHAKES & MIXES 30 NUTS & SEEDS 31 PEANUT BUTTER & MARMITE 31 POPCORN 31 SNACK BARS 34 SOFT DRINKS 42 SUGAR FREE CONFECTIONERY 43 SYRUPS & TOPPINGS 43 YOGHURT DRINKS 44 YOGHURTS & DAIRY DESSERTS The information in this guide is only applicable to products made for the UK market. All details are correct at the time of going to press but are subject to change. For the latest information check www.isitkosher.uk. Sign up for email alerts and updates on www.kosher.org.uk or join Facebook KLBD Kosher Direct. No assumptions should be made about the kosher status of products not listed, even if others in the range are approved or certified. It is preferable, whenever possible, to buy products made under Rabbinical supervision. WARNING: The designation ‘Parev’ does not guarantee that a product is suitable for those with dairy or lactose intolerance. WARNING: The ‘Nut Free’ symbol is displayed next to a product based on information from manufacturers. The KLBD takes no responsibility for this designation. You are advised to check the allergen information on each product. k GUESS WHAT'S IN YOUR FOOD k USING THE PRODUCT LISTINGS Hi Noshers! PRODUCTS WHICH ARE KLBD CERTIFIED Even in these difficult times, and perhaps now more than ever, Like many kashrut authorities around the world, the KLBD uses the American we need our Nosh! kosher logo system. -

Members' Magazine

MEMBERS’ MAGAZINE SEPTEMBER-OCTOBER 2018 Supporting the Human-Animal Bond Alberta Helping Animals Society 2018 VETERINARY PRESENTED BY FORENSICS WORKSHOP From routine investigations to cases that end up in court, veterinary forensics is an emerging area of study in the veterinary profession. Put your skills to the test at this two day workshop featuring: • Veterinary Forensics 101: Investigations, • Panel presentation with ABVMA, Animal Evidence Collection, Forensic Reports, Care and Control (ACC) Edmonton, Alberta Toxicology, Pathology Agriculture and Forestry, (AAF) Calgary Dr. Margaret Doyle, Riverbend Veterinary Humane Society (CHS), Alberta SPCA (ABSPCA) Clinic, and Mr. Brad Nichols, Calgary Dr. Phil Buote - (ABVMA), Mr. Keith Scott Humane Society (ACC), Dr. Hussein Keshwani (AAF), Mr. Brad • Issues with Recongition and Reporting: Nichols (CHS), Mr. Ken Dean (ABSPCA) Six Stages of Veterinary Response to • Solve the Case, dinner and networking event - Animal Cruelty, Abuse and Neglect submit your case slides for an open discussion Dr. Phil Arkow, The National Link Coalition of various forensics cases • The Animal Abuse/Family Violence Link and • Preparing for Court Its Implications for Veterinary Social Work Ms. Rose Greenwood, Crown Prosecutor, Dr. Phil Arkow, The National Link Coalition Justice and Solicitor General • Emotional Suffering of Animals or People in • Necropsy, handling the post-mortem Animal Abuse Cases Dr. Nick Nation, Animal Pathology Services Ltd. Dr. Rebecca Ledger, Animal Behaviour and • Compiling the Case for Trial Welfare Scientist, Langara College Crime Scene Photography • The Animal Protection Act in Alberta Constable Stuart Saunders, Edmonton - it’s impact on various organizations. Police Service Role of Vet and Tech Teams in the Field Mr. -

Wrigley Some Research Online to Help

The 7 Steps - April 1. CONTEXT Mindmap anything you know about the topic, including vocabulary. Do Wrigley some research online to help. Listening Questions 1 1. In what year was Wrigley founded? 2. QUESTIONS . 2. What was the first product William Wrigley Jr. sold? . Read the listening questions to 3. Why did he decide to focus on selling gum? check your . understanding. 4. When was the Doublemint flavor introduced? Look up any new vocabulary. 5. Who bought Wrigley in 2008? . 3. LISTEN Listening Questions 2 1. Which MLB team did the Wrigley family own and when did they sell it? Listen and answer . the questions 2. How old is Fenway Park? using full sentences. Circle . the number of times and % you 3. What does Koshien Stadium share in common with Wrigley Field? understood. 4. When was the first official night game played at Wrigley Field? . 5. How long did the Chicago Cubs go between World Series championships? Listening 1 1 2 3 4 5 . % % % % % Discussion Questions 1. What snacks did you eat when you were younger? Is gum a popular snack in Japan? Listening 2 1 2 3 4 5 2. How do you feel about huge companies investing in sporting teams? How does it benefit them? % % % % % 4. CHECK ANSWERS TRANSCRIPT 1 When it comes to chewing gum, the Wrigley name is one of the most famous. The Wm. Wrigley Read through the Jr. Company, or Wrigley for short, was founded by William Wrigley Jr. in 1891 and is transcript and headquartered in Chicago, Illinois. underline the When William Wrigley Jr.