Chairman's Statement

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

0 Swire Pacific Annual Report 2009 Quality in Every Detail Swire Properties Believes That the Quality of Its Planning and Design Creates Long-Term Value

0 Swire Pacific Annual Report 009 Quality in Every Detail Swire Properties believes that the quality of its planning and design creates long-term value. Swire Pacific Annual Report 009 Review of Operations Property Division Swire Properties’ property investment portfolio in Hong Kong comprises office and retail premises in prime locations, as well as hotel interests, serviced apartments and other luxury residential accommodation. The completed portfolio in Hong Kong totals 4.9 million square feet of gross floor area. In Mainland China, Swire Properties has interests in major commercial mixed-use developments in Beijing, Shanghai and Guangzhou, which will total 8.0 million square feet on completion, of which .6 million square feet has already been completed. In the United States, Swire Properties owns a 75% interest in the Mandarin Oriental Hotel in Miami, Florida. In the United Kingdom, Swire Properties owns four small hotels. Swire Properties’ trading portfolio comprises land and residential apartments under development in Hong Kong and Florida, as well as the remaining units for sale at the Island Lodge and Asia residential developments in Hong Kong and Miami respectively. Particulars of the Group’s key properties are set out on pages 79 to 89. 2009 008 HK$M HK$M Turnover Gross rental income derived from Offices 4,115 3,63 Retail 3,060 ,90 Residential 268 9 Other revenue * 83 74 Property investment 7,526 6,907 Property trading 643 889 Hotels 172 56 Total turnover 8,341 7,95 Operating profit derived from Property investment 5,607 5,012 Valuation gains on investment properties 14,383 84 Property trading 70 98 Hotels (474) (86) Total operating profit 19,586 5,308 Share of post-tax profits from jointly controlled and associated companies 163 83 Attributable profit 15,390 4,93 * Other revenue is mainly estate management fees. -

FAST FACTS 2021 Swire Is a Highly Diversified Global Business Group, Which Has Been in Turnover US$23,830M Operation for Over 200 Years

GF210715e FAST FACTS 2021 FACTS FAST Swire is a highly diversified global business group, which has been in Turnover US$23,830M operation for over 200 years. Within Asia, Swire’s activities principally come Turnover | 2016-2020 Turnover by Region | 2020 Turnover by Division | 2020 US$M US$M US$M under the group’s publicly quoted arm, Swire Pacific Ltd. Elsewhere in the 35,000 Hong Kong SAR Property 30,000 Chinese Mainland Aviation world, businesses are held by parent company, John Swire & Sons Ltd. 25,000 Other Asia Beverages & 20,000 SW Pacific Food Chain Marine Services 15,000 Americas Trading & Industrial 10,000 Europe Head Office Africa & Middle East 5,000 Marine Global# 0 16 17 18 19 20 Capital Employed US$75,803M Capital Employed | 2016-2020 Capital Employed by Region | 2020 Capital Employed by Division | 2020 US$M US$M US$M 80,000 Hong Kong SAR Property 70,000 Chinese Mainland Aviation 60,000 Other Asia Beverages & 50,000 SW Pacific Food Chain 40,000 Marine Services Americas 30,000 Trading & Industrial ABOUT JOHN SWIRE & SONS LTD Europe 20,000 Head Office & Africa & Middle East 10,000 Swire Investments Marine Global# 0 • Established in 1816 and headquartered in London. 16 17 18 19 20 • Responsible for formulating and directing overall group strategy. Provides a range of services within the group, including recruitment, employment and training of staff. Employees 121,211 Employees | 2016-2020 Employees by Region | 2020 Employees by Division | 2020 • Holds a 58% shareholding in Swire Pacific in the Hong Kong Special Administrative Region (“Hong Kong SAR”). -

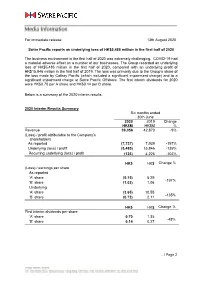

For Immediate Release 13Th August 2020 Swire Pacific Reports an Underlying Loss of HK$5,485 Million in the First Half of 2020 Th

For immediate release 13th August 2020 Swire Pacific reports an underlying loss of HK$5,485 million in the first half of 2020 The business environment in the first half of 2020 was extremely challenging. COVID-19 had a material adverse effect on a number of our businesses. The Group recorded an underlying loss of HK$5,485 million in the first half of 2020, compared with an underlying profit of HK$15,846 million in the first half of 2019. The loss was primarily due to the Group’s share of the loss made by Cathay Pacific (which included a significant impairment charge) and to a significant impairment charge at Swire Pacific Offshore. The first interim dividends for 2020 were HK$0.70 per A share and HK$0.14 per B share. Below is a summary of the 2020 interim results: 2020 Interim Results Summary Six months ended 30th June 2020 2019 Change HK$M HK$M % Revenue 39,056 42,870 -9% (Loss) / profit attributable to the Company’s shareholders As reported (7,737) 7,939 -197% Underlying (loss) / profit (5,485) 15,846 -135% Recurring underlying (loss) / profit (123) 4,226 -103% HK$ HK$ Change % (Loss) / earnings per share As reported ‘A’ share (5.15) 5.29 -197% ‘B’ share (1.03) 1.06 Underlying ‘A’ share (3.65) 10.55 -135% ‘B’ share (0.73) 2.11 HK$ HK$ Change % First interim dividends per share ‘A’ share 0.70 1.35 -48% ‘B’ share 0.14 0.27 … / Page 2 / …2 Divisional Highlights: Property Division • The recurring underlying profit in the first half of 2020 (which excludes gains from the sales of interests in investment properties of HK$42 million, compared with HK$11,937 million in the first half of 2019) was HK$3,067 million, compared with HK$3,319 million in the first half of 2019. -

FAST FACTS 2019 Swire Is a Highly Diversified Global Business Group, Which Has Been in Turnover US$32,517M Operation for Over 200 Years

FAST FACTS 2019 Swire is a highly diversified global business group, which has been in Turnover US$32,517M operation for over 200 years. Within Asia, Swire’s activities principally come Turnover | 2014-2018 Turnover by Region | 2018 Turnover by Division | 2018 US$M US$M US$M under the group’s publicly quoted arm, Swire Pacific Ltd. Elsewhere in the 35,000 Hong Kong Property 30,000 Mainland China Aviation world, businesses are held by parent company, John Swire & Sons Ltd. 25,000 Other Asia Beverages & 20,000 SW Pacific Food Chain Marine Services 15,000 Americas Trading & Industrial 10,000 Europe Head Office Africa & Middle East 5,000 Marine Global# 0 14 15 16 17 18 Capital Employed US$71,006M Capital Employed | 2014-2018 Capital Employed by Region | 2018 Capital Employed by Division | 2018 US$M US$M US$M 80,000 Hong Kong Property 70,000 Mainland China Aviation 60,000 Other Asia Beverages & 50,000 Food Chain SW Pacific 40,000 Marine Services Americas 30,000 Trading & Industrial Europe ABOUT JOHN SWIRE & SONS LTD 20,000 Head Office Africa & Middle East 10,000 Marine Global# 0 • Established in 1816 and headquartered in London. 14 15 16 17 18 • Responsible for formulating and directing overall group strategy. Provides a range of services within the group, Employees 133,624 including recruitment, employment and training of staff. Employees | 2014-2018 Employees by Region | 2018 Employees by Division | 2018 • Holds a 55% shareholding in Swire Pacific in Hong Kong. Hong Kong Property 140,000 Mainland China Aviation • Holds controlling stakes in a range of businesses trading 120,000 Other Asia Beverages & in the UK, North America, Australia, Papua New Guinea, 100,000 By SW Pacific Food Chain East and West Africa, and across Southeast Asia. -

FAST FACTS 2021 CHINESE MAINLAND Cf210715e 2020 KEY FINANCIALS – CHINESE MAINLAND

FAST FACTS 2021 CHINESE MAINLAND CF210715e 2020 KEY FINANCIALS – CHINESE MAINLAND The Swire group’s principal areas of operation are Turnover US$6,302M in the Asia Pacific region, centred on Greater China, 太古 US$M US$M where the name or Taikoo, meaning “Great and 9,000 Ancient”, is a household name. Swire’s businesses 8,000 are grouped into five categories: Property, Aviation, 7,000 Beverages & Food Chain, Marine Services and Trading 6,000 By 5,000 & Industrial. These activities come under Hong Kong- Division 4,000 based, publicly quoted Swire Pacific Limited, or are 3,000 held by parent company, John Swire & Sons Limited. 2,000 1,000 Swire first opened an office in Shanghai in 1866 to 0 16 17 18 19 20 trade in tea and textiles. Today, the group’s interests in the Chinese Mainland range from properties and aircraft engineering to retailing. Swire subsidiaries are partners to some of the Chinese Mainland’s most successful companies, including Sino-Ocean Group Capital Employed US$17,015M Holding, Air China and COFCO. International partners on the Chinese Mainland include The Coca-Cola US$M US$M Company and The Boeing Company. 18,000 15,000 12,000 By Division^ 9,000 6,000 3,000 0 16 17 18 19 20 ^ A division may have negative capital employed. These figures have been excluded from the divisional breakdown. Employees 38,007 40,000 35,000 30,000 By 25,000 Division 20,000 15,000 10,000 5,000 0 16 17 18 19 20 Property Trading & Industrial Aviation Head Office Beverages & Food Chain Information within this document is prepared on a 100% basis for subsidiaries of the Swire group, direct joint ventures of the Swire group and associated companies (which have services agreements in place with the Swire group). -

2Nd ISSUE 2014 SWIRENEWS 30 2Nd ISSUE 2014

2nd ISSUE 2014 SWIRENEWS 30 2nd ISSUE 2014 Contents Newswire 1 Out & About 26 Features Archives A word from the Precious cargo 28 new man at the top 14 The gift of education The Swire group is a multi-national, multi-disciplined 20 commercial group, with its principal areas of operations in the Asia Pacific region, and centred on the Greater China area. Hong Kong is home to publicly quoted Swire Pacific, whose core businesses are grouped under five operating divisions: property, aviation, beverages, marine services, and trading & industrial. John Swire & Sons Limited, headquartered in the UK, is the parent company of the group. In addition to its controlling shareholding in Swire Pacific, John Swire & Sons Limited operates a range of wholly-owned businesses, including deep-sea shipping, cold storage, off-shore and road transport logistics services and agricultural activities with main areas of operation in Australia, Papua New Guinea, East Africa, Sri Lanka, the USA and the UK. Please send material to the Editor, GPO Box 1, Hong Kong, or email us at [email protected]. For pictures, we welcome prints, colour slides or computer graphics in JPG format (500dpi and 20cm Swire Properties played x 16cm), and digital photos taken by cameras with 8 host to the world’s largest Megapixels or above. elephant art exhibition which showcased more Swire News is published in Hong Kong, by the Group than 100 individually- Public Affairs Department. painted, life-size baby elephant statues, each Copyright©2014 with its own unique design. Story on page 3. Cindy Cheung Editor Charlotte Bleasdale Deputy Editor Barry Chu Manager Design/Production NEWSWIRE 1 Newswire CORPORATE John Swire & Sons John Swire & Sons since 1st Kong, Japan and Papua New and of Swire Oilfield Limited announces January 2005. -

Swire Pacific Annual Report 2020 1

SW_2020_Cover.ai size: 210mm(W) x 285mm(H) spine: 16mm Annual Report 2020 Annual Report 2020 Stock Codes: ‘A’ Shares 00019 ‘B’ Shares 00087 www.swirepacific.com C M Y K Hot Stamping Silver CONTENTS 1 Corporate Statement FINANCIAL STATEMENTS 3 2020 Performance Highlights 121 Independent Auditor’s Report 4 Chairman’s Statement 131 Consolidated Statement of Profit or Loss 7 Finance Director’s Statement 132 Consolidated Statement of Other Comprehensive Income MANAGEMENT DISCUSSION 133 Consolidated Statement of Financial Position AND ANALYSIS 134 Consolidated Statement of Cash Flows 12 2020 Performance Review and Outlook 135 Consolidated Statement of Changes in Equity 12 Property Division 136 Notes to the Financial Statements 30 Aviation Division 204 Principal Accounting Policies 44 Beverages Division 207 Principal Subsidiary, Joint Venture and Associated Companies 56 Marine Services Division 218 Cathay Pacific Airways Limited – Abridged 66 Trading & Industrial Division Financial Statements 72 Financial Review 81 Financing SUPPLEMENTARY INFORMATION CORPORATE GOVERNANCE & 220 Summary of Past Performance SUSTAINABILITY 222 Schedule of Principal Group Properties 232 Group Structure Chart 89 Corporate Governance Report 234 Glossary 101 Risk Management 236 Financial Calendar and Information for Investors 106 Directors and Officers 236 Disclaimer 107 Directors’ Report 113 Sustainable Development Review Note: Definitions of the terms and ratios used in this report can be found in the Glossary. SWIRE PACIFIC ANNUAL REPORT 2020 1 CORPORATE STATEMENT SUSTAINABLE GROWTH Swire Pacific is a Hong Kong based international conglomerate with a diversified portfolio of market leading businesses. The Company has a long history in Greater China, where the name Swire or 太古 has been established for over 150 years. -

Annual Report 2018

paper: Savile Row Tweed Extra White 300gsm SW_2018_Cover.ai size: 210mm(W) x 285mm(H) spine: 16mm Cover ANNUAL REPORT ANNUAL ANNUAL REPORT 2018 2018 www.swirepacific.com Stock Codes: ‘A’ Shares 00019 ‘B’ Shares 00087 C M Y K PMS 7562U CONTENTS 1 Corporate Statement FINANCIAL STATEMENTS 3 2018 Performance Highlights 117 Independent Auditor’s Report 4 Chairman’s Statement 124 Consolidated Statement of Profit or Loss 6 Finance Director’s Statement 125 Consolidated Statement of Other Comprehensive Income MANAGEMENT DISCUSSION 126 Consolidated Statement of Financial Position AND ANALYSIS 127 Consolidated Statement of Cash Flows 10 2018 Performance Review and 128 Consolidated Statement of Changes in Equity Outlook 129 Notes to the Financial Statements 10 Property Division 203 Principal Accounting Policies 26 Aviation Division 206 Principal Subsidiary, Joint Venture and 42 Beverages Division Associated Companies and Investments 52 Marine Services Division 218 Cathay Pacific Airways Limited – Abridged Financial Statements 62 Trading & Industrial Division 70 Financial Review SUPPLEMENTARY INFORMATION 79 Financing 220 Summary of Past Performance CORPORATE GOVERNANCE & 222 Schedule of Principal Group Properties SUSTAINABILITY 232 Group Structure Chart 234 Glossary 86 Corporate Governance Report 236 Financial Calendar and Information 98 Risk Management for Investors 101 Directors and Officers 236 Disclaimer 102 Directors’ Report 109 Sustainable Development Review Note: Definitions of the terms and ratios used in this report can be found in the Glossary. SWIRE PACIFIC 2018 ANNUAL REPORT 1 CORPORATE STATEMENT SUSTAINABLE GROWTH Swire Pacific is a Hong Kong based international conglomerate with a diversified portfolio of market leading businesses. The Company has a long history in Greater China, where the name Swire or 太古 has been established for over 150 years. -

2019 Annual Report

paper: 300gsm [Acumen - Salona Offset] - FSC SW_2020_Cover.ai size: 210mm(W) x 285mm(H) spine: 16mm ANNUAL REPORT 2019 www.swirepacific.com Stock Codes: ‘A’ Shares 00019 ‘B’ Shares 00087 ANNUAL REPORT 2019 C M Y K CONTENTS 1 Corporate Statement FINANCIAL STATEMENTS 3 2019 Performance Highlights 121 Independent Auditor’s Report 4 Chairman’s Statement 128 Consolidated Statement of Profit or Loss 6 Finance Director’s Statement 129 Consolidated Statement of Other Comprehensive Income MANAGEMENT DISCUSSION 130 Consolidated Statement of Financial Position AND ANALYSIS 131 Consolidated Statement of Cash Flows 10 2019 Performance Review and Outlook 132 Consolidated Statement of Changes in Equity 10 Property Division 133 Notes to the Financial Statements 28 Aviation Division 204 Principal Accounting Policies 44 Beverages Division 207 Principal Subsidiary, Joint Venture and Associated Companies and Investments 56 Marine Services Division 218 Cathay Pacific Airways Limited – Abridged 66 Trading & Industrial Division Financial Statements 72 Financial Review 81 Financing SUPPLEMENTARY INFORMATION CORPORATE GOVERNANCE & 220 Summary of Past Performance SUSTAINABILITY 222 Schedule of Principal Group Properties 232 Group Structure Chart 89 Corporate Governance Report 234 Glossary 101 Risk Management 236 Financial Calendar and Information for Investors 106 Directors and Officers 236 Disclaimer 107 Directors’ Report 113 Sustainable Development Review Note: Definitions of the terms and ratios used in this report can be found in the Glossary. SWIRE PACIFIC ANNUAL REPORT 2019 1 CORPORATE STATEMENT SUSTAINABLE GROWTH Swire Pacific is a Hong Kong based international conglomerate with a diversified portfolio of market leading businesses. The Company has a long history in Greater China, where the name Swire or 太古 has been established for over 150 years. -

Swire Properties Announces 2020 Annual Results

For Immediate Release Swire Properties Announces 2020 Final Results Strong fundamentals to drive future growth despite challenging conditions Summary of 2020 Annual Results • Strong fundamentals delivering dividend growth of 3% year-on-year despite a decrease in underlying profit. • Resilient office performance in Hong Kong underpinned by Taikoo Place with positive rental reversions. • High Hong Kong retail occupancy rate throughout difficult times reflecting the Company’s strong relationships with tenants. • Strong rebound of Chinese mainland portfolio with retail sales up 29% year-on-year in second half of 2020. • Robust capital management to pursue further projects and continue scaling up the Company’s investment in the region. 2020 2019 Note HK$M HK$M Change Results For the year Revenue 13,308 14,222 -6% Profit attributable to the Company's shareholders Underlying (a),(b) 12,679 24,130 -47% Recurring underlying (b) 7,089 7,633 -7% HK$ HK$ Earnings per share Underlying (c) 2.17 4.12 -47% Recurring underlying (c) 1.21 1.30 -7% Dividend per share First interim 0.30 0.29 +3% Second interim 0.61 0.59 +3% HK$ HK$ Financial Position At 31st December Equity attributable to the Company’s shareholders per share (a) 49.36 49.05 +1% Gearing ratio (a) 2.3% 5.3% -3.0%pt. Notes: (a) Refer to the glossary on page 57 of the announcement of 2020 Final Results of Swire Properties Limited (the “Results Announcement”), dated 11 March 2021, for definition. (b) A reconciliation between reported profit and underlying profit attributable to the Company’s shareholders is provided on page 7 of the Results Announcement. -

Interim Report 2019

Interim Report 2019 Stock Code: 1972 Contents 1 Financial Highlights 2 Chairman’s Statement 5 Review of Operations 23 Financing 29 Report on Review of Condensed Interim Financial Statements 30 Condensed Interim Financial Statements 35 Notes to the Condensed Interim Financial Statements 53 Supplementary Information 55 Glossary 56 Financial Calendar and Information for Investors Financial Highlights Six months ended 30th June 2019 2018 Note HK$M HK$M Change Results Revenue 7,510 7,309 +3% Profit attributable to the Company's shareholders Underlying (a), (b) 18,606 6,219 +199% Recurring underlying (b) 4,049 3,732 +8% Reported 8,973 21,205 -58% Cash generated from operations 2,158 5,308 -59% Net cash inflow before financing 15,104 7,628 +98% HK$ HK$ Earnings per share Underlying (c) 3.18 1.06 +199% Recurring underlying (c) 0.69 0.64 +8% Reported (c) 1.53 3.62 -58% Dividends per share First interim 0.29 0.27 +7% 30th June 31st December 2019 2018 HK$M HK$M Change Financial Position Total equity (including non-controlling interests) 286,714 281,291 +2% Net debt 15,670 29,905 -48% Gearing ratio (a) 5.5% 10.6% -5.1%pt. HK$ HK$ Equity attributable to the Company’s shareholders per share (a) 48.66 47.74 +2% Notes: (a) Refer to glossary on page 55 for definition. (b) A reconciliation between reported profit and underlying profit attributable to the Company’s shareholders is provided on page 6. (c) Refer to note 11 in the financial statements for the weighted average number of shares. -

Annual Report 2019 CONTENTS

Stock Code: 1972 Annual Report 2019 CONTENTS 4 2019 Highlights 8 Company Profile 9 Financial Highlights 10 Ten-Year Financial Summary 13 Chairman’s Statement 16 Key Business Strategies MANAGEMENT DISCUSSION & ANALYSIS 20 Review of Operations 54 Financial Review 61 Financing CORPORATE GOVERNANCE & SUSTAINABILITY 72 Corporate Governance 84 Risk Management 88 Directors and Officers 90 Directors’ Report 97 Sustainable Development AUDITOR’S REPORT AND ACCOUNTS 106 Independent Auditor’s Report 110 Consolidated Statement of Profit or Loss 111 Consolidated Statement of Other Comprehensive Income 112 Consolidated Statement of Financial Position 113 Consolidated Statement of Cash Flows 114 Consolidated Statement of Changes in Equity 115 Notes to the Financial Statements 178 Principal Accounting Policies 181 Principal Subsidiary, Joint Venture and Associated Companies SUPPLEMENTARY INFORMATION 184 Schedule of Principal Group Properties 195 Glossary 196 Financial Calendar and Information for Investors Creative Transformation Captures what we do and how we do it. It underlines the creative mindset and long-term approach that enables us to seek out new perspectives, and original thinking that goes beyond the conventional. It also encapsulates our ability to unlock the potential of places and create vibrant destinations that can engender further growth and create sustainable value for our stakeholders. Swire Properties Annual Report 2019 2019 Highlights 1 Completed the sale of 100% 1 interest in a subsidiary which owned two office buildings at 14 Taikoo