0 Swire Pacific Annual Report 2009 Quality in Every Detail Swire Properties Believes That the Quality of Its Planning and Design Creates Long-Term Value

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Swire Properties Delivers Solid Results in First Half of 2021

For Immediate Release Swire Properties Delivers Solid Results in First Half of 2021 Strong fundamentals, combined with a balanced portfolio and strategic capital management fuelling Company’s future growth Summary of 2021 Interim Results • Increase in attributable underlying profit to HK$4,513 million, driven by the sale of car parking spaces at Taikoo Shing in Hong Kong. • Strong fundamentals delivering sustainable dividend growth of 3% year-on-year. • Resilient Hong Kong office portfolio with high occupancies and stable rents. • Robust Chinese Mainland retail portfolio with 38% year-on-year increase in attributable gross rental income. • Gradual recovery in Hong Kong retail portfolio with high occupancy and an increase in retail sales. • Strong balance sheet to scale up our investments in Hong Kong and the Chinese Mainland. Six months ended 30th June 2021 2020 Note HK$M HK$M Change Results Revenue 9,068 6,551 +38% Profit attributable to the Company's shareholders Underlying (a), (b) 4,513 3,753 +20% Recurring underlying (b) 3,716 3,702 0% Reported 1,984 1,029 +93% HK$ HK$ Earnings per share Underlying (c), (d) 0.77 0.64 +20% Recurring underlying (c), (d) 0.64 0.63 0% Reported (c), (d) 0.34 0.18 +93% Dividend per share First interim 0.31 0.30 +3% 30th June 31st December 2021 2020 HK$ HK$ Change Financial Position Equity attributable to the Company’s shareholders per share (a) 49.21 49.36 0% Gearing ratio (a) 3.1% 2.3% +0.8%pt. Notes: (a) Refer to the glossary on page 66 of the announcement of 2021 Interim Results of Swire Properties Limited (the “Results Announcement”), dated 12 August 2021, for definition. -

David Zhao Joins Burson-Marsteller As Executive Vice President

Contact: Brad Burgess +86-10-5816-2566 [email protected] NEWS RELEASE Swire Properties Taps Burson-Marsteller For Brand Building In China Beijing, August 21, 2012 – Burson-Marsteller, a leading public relations and communications consulting company, was awarded a one-year corporate retainer to elevate the reputation of Swire Properties in Mainland China and to increase awareness of its brand among potential partners and customers. A Guangzhou-led team of property branding professionals at Burson-Marsteller China will develop corporate communications and media strategies for Swire Properties’ corporate brand and its innovative mixed-use developments, positioning them as unique places to live, work and play. “Swire Properties is strongly positioned in Hong Kong as a leading developer and owner of large-scale mixed-use properties,” said Chris Deri, Burson-Marsteller China’s CEO. “This year marks Swire Properties’ listing on the Main Board of the Hong Kong Stock Exchange and its 40th anniversary. We are proud and excited to be its communications partner in Mainland China at this significant moment and are eager to support its branding campaigns within China.” Swire Properties has significant investments on the mainland, including Sanlitun Village and INDIGO in Beijing, TaiKoo Hui in Guangzhou, Daci Temple project in Chengdu and Dazhongli project in Shanghai. The company also has representative offices in Beijing, Shanghai, Guangzhou and Chengdu to explore new business opportunities. “Swire Properties has spent the past 40 years developing transformational projects which create lasting value for our stakeholders and the community at large,” said Vivian Lo, Swire Properties’ Assistant Director of Public Affairs, Mainland China. -

Fast Facts 2021

BEVERAGES & MARINE SHIPPING LINES FOOD CHAIN SERVICES THE CHINA NAVIGATION BEVERAGES COMPANY (CNCo) OFFSHORE SUPPORT SERVICES SWIRE COCA-COLA Swire Shipping, CNCo’s liner shipping division, offers multipurpose liner services for transporting containerised, A strategic partner of The Coca-Cola Company breakbulk and project cargoes, connecting North America since the 1960s. to the Pacific Islands and Oceania. Through Swire Projects, CNCo offers project parcelling and transport engineering Holds the franchise to manufacture, market and services to the energy, resource and infrastructure sectors. distribute products of The Coca-Cola Company in an extensive area of the western USA, the Hong Kong SAR, Taiwan region, and 11 provinces and the Shanghai Municipality in the Chinese Mainland. SWIRE BULK In business since 1978, Swire Coca-Cola, USA is one of the largest independent Coca-Cola bottlers in the United States, operating in 13 states. SWIRE ENERGY SERVICES (SES) UNITED STATES Operates across strategic locations in North America, including Mexico and the Caribbean. Offers offshore Leading vessel owner and operator specialising in container solutions, equipment rentals and sales, transporting cargoes in the dry bulk segment. Has Franchise population Sales volume integrity services, aviation services and chemical presence in the Atlantic and opens its Atlantic Americas plants 6 million handling services. desk in Miami. in 13 states 30.3 million 317 unit cases* * A unit case comprises 24 8-ounce servings. @2021 The Coca-Cola Company FAST FACTS -

FAST FACTS 2021 Swire Is a Highly Diversified Global Business Group, Which Has Been in Turnover US$23,830M Operation for Over 200 Years

GF210715e FAST FACTS 2021 FACTS FAST Swire is a highly diversified global business group, which has been in Turnover US$23,830M operation for over 200 years. Within Asia, Swire’s activities principally come Turnover | 2016-2020 Turnover by Region | 2020 Turnover by Division | 2020 US$M US$M US$M under the group’s publicly quoted arm, Swire Pacific Ltd. Elsewhere in the 35,000 Hong Kong SAR Property 30,000 Chinese Mainland Aviation world, businesses are held by parent company, John Swire & Sons Ltd. 25,000 Other Asia Beverages & 20,000 SW Pacific Food Chain Marine Services 15,000 Americas Trading & Industrial 10,000 Europe Head Office Africa & Middle East 5,000 Marine Global# 0 16 17 18 19 20 Capital Employed US$75,803M Capital Employed | 2016-2020 Capital Employed by Region | 2020 Capital Employed by Division | 2020 US$M US$M US$M 80,000 Hong Kong SAR Property 70,000 Chinese Mainland Aviation 60,000 Other Asia Beverages & 50,000 SW Pacific Food Chain 40,000 Marine Services Americas 30,000 Trading & Industrial ABOUT JOHN SWIRE & SONS LTD Europe 20,000 Head Office & Africa & Middle East 10,000 Swire Investments Marine Global# 0 • Established in 1816 and headquartered in London. 16 17 18 19 20 • Responsible for formulating and directing overall group strategy. Provides a range of services within the group, including recruitment, employment and training of staff. Employees 121,211 Employees | 2016-2020 Employees by Region | 2020 Employees by Division | 2020 • Holds a 58% shareholding in Swire Pacific in the Hong Kong Special Administrative Region (“Hong Kong SAR”). -

HKRI Taikoo Hui Shanghai

FACT SHEET HKRI Taikoo Hui Shanghai Located in the heart of West Nanjing Road CBD, Jing’an District, Shanghai, HKRI Taikoo Hui is a 50:50 joint venture between two Hong Kong listed companies, HKR International and Swire Properties. The development comprises a lifestyle shopping mall, two premium Grade A office towers, two boutique hotels and one serviced residence, an underground shopping corridor, providing a mixed-use space for working, shopping, dining, leisure and living enjoyment. Location :West Nanjing Road CBD,Shanghai Opening year :Opened in phases from the second half of 2016 Developer :HKR International Limited (50%) Swire Properties Limited (50%) Architect :Wong & Ouyang (HK) Limited – Architect Architect MAKE AECOM Environmental Planning and Design (Shanghai) Co.,td. –Structural engineer Parsons Brinckerhoff (Asia) Ltd. –Building services engineer Total site area :Approx. 63,000 sqm / approx. 676,000 sq ft Gross floor area :Total GFA approx. 322,000 sqm / over 3.46 million sq ft A lifestyle shopping mall – HKRI Taikoo Hui (Approx. 100,000 sqm / approx. 1.078 million sq ft) Two office towers – HKRI Centre one and HKRI Centre two (over 170,000 sqm/ approx. 1,85 million sq ft) Two boutique hotels and one serviced apartments – The Sukhothai Shanghai – The Middle House and The Middle House Residences (over 50,000 sqm/ approx. 538,195 sq ft, with more than 400 rooms in total) One commercial metro space – MetroLink (over 3,000 sqm/ approx. 3,600 sq ft) Parking space :Approx. 1,200 Accessibility :The Complex has a direct access to Metro Line 13, with Line 2 and Line 12 at West Nanjing Road station only waking distance away. -

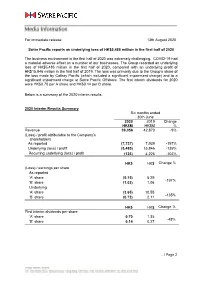

For Immediate Release 13Th August 2020 Swire Pacific Reports an Underlying Loss of HK$5,485 Million in the First Half of 2020 Th

For immediate release 13th August 2020 Swire Pacific reports an underlying loss of HK$5,485 million in the first half of 2020 The business environment in the first half of 2020 was extremely challenging. COVID-19 had a material adverse effect on a number of our businesses. The Group recorded an underlying loss of HK$5,485 million in the first half of 2020, compared with an underlying profit of HK$15,846 million in the first half of 2019. The loss was primarily due to the Group’s share of the loss made by Cathay Pacific (which included a significant impairment charge) and to a significant impairment charge at Swire Pacific Offshore. The first interim dividends for 2020 were HK$0.70 per A share and HK$0.14 per B share. Below is a summary of the 2020 interim results: 2020 Interim Results Summary Six months ended 30th June 2020 2019 Change HK$M HK$M % Revenue 39,056 42,870 -9% (Loss) / profit attributable to the Company’s shareholders As reported (7,737) 7,939 -197% Underlying (loss) / profit (5,485) 15,846 -135% Recurring underlying (loss) / profit (123) 4,226 -103% HK$ HK$ Change % (Loss) / earnings per share As reported ‘A’ share (5.15) 5.29 -197% ‘B’ share (1.03) 1.06 Underlying ‘A’ share (3.65) 10.55 -135% ‘B’ share (0.73) 2.11 HK$ HK$ Change % First interim dividends per share ‘A’ share 0.70 1.35 -48% ‘B’ share 0.14 0.27 … / Page 2 / …2 Divisional Highlights: Property Division • The recurring underlying profit in the first half of 2020 (which excludes gains from the sales of interests in investment properties of HK$42 million, compared with HK$11,937 million in the first half of 2019) was HK$3,067 million, compared with HK$3,319 million in the first half of 2019. -

Sino-Ocean Taikoo Li Chengdu the Story of an Original Development Sino-Ocean Taikoo Li Chengdu the Story of an Original Development Sino-Ocean Li Chengdu Taikoo

Sino-Ocean Taikoo Li Chengdu The story of an original development Sino-Ocean Taikoo Li Chengdu The story of an original development Sino-Ocean Li Chengdu Taikoo 1 10 Preface 23 Introduction: Setting the scene 29 History: Brick, dragons and burning words 38 Architecture: Good ordinary buildings 45 Place: An original city centre Sino-Ocean Li Chengdu Taikoo 50 Sino-Ocean Li Chengdu Taikoo Public Space: Intimacy, human scale and enjoyment 55 Movement: Fast and slow 60 Art: Personal and public expression 67 Hospitality: The Temple House 2 3 Sino-Ocean Taikoo Li Chengdu A new heart of Chengdu 2011 2015 Sino-Ocean Li Chengdu Taikoo Sino-Ocean Li Chengdu Taikoo 4 5 Throughout our 40-year history Swire Properties has initiated projects that add value to both a place and its people. Nowhere is that more evident than in our newly opened retail-led, mixed-use Daci Temple development in the heart of Chengdu. The Jinjiang district authorities in Chengdu wanted to continue the energetic development of the city while at the same time respect the heritage of a historically important site, with the 1,400-year-old Daci Temple as its centre point. We shared their vision and very much appreciated the confidence they showed in our commitment to create an original, premium commercial complex that preserved the singular nature of the location and enhanced the fabric of the neighbourhood in a positive manner. Swire have been trading in China for 150 years and Sino-Ocean Taikoo Li Chengdu is one of five completed or nearly completed developments in Swire Properties’ own Sino-Ocean Li Chengdu Taikoo Sino-Ocean Li Chengdu Taikoo expanding portfolio in the country. -

FAST FACTS 2019 Swire Is a Highly Diversified Global Business Group, Which Has Been in Turnover US$32,517M Operation for Over 200 Years

FAST FACTS 2019 Swire is a highly diversified global business group, which has been in Turnover US$32,517M operation for over 200 years. Within Asia, Swire’s activities principally come Turnover | 2014-2018 Turnover by Region | 2018 Turnover by Division | 2018 US$M US$M US$M under the group’s publicly quoted arm, Swire Pacific Ltd. Elsewhere in the 35,000 Hong Kong Property 30,000 Mainland China Aviation world, businesses are held by parent company, John Swire & Sons Ltd. 25,000 Other Asia Beverages & 20,000 SW Pacific Food Chain Marine Services 15,000 Americas Trading & Industrial 10,000 Europe Head Office Africa & Middle East 5,000 Marine Global# 0 14 15 16 17 18 Capital Employed US$71,006M Capital Employed | 2014-2018 Capital Employed by Region | 2018 Capital Employed by Division | 2018 US$M US$M US$M 80,000 Hong Kong Property 70,000 Mainland China Aviation 60,000 Other Asia Beverages & 50,000 Food Chain SW Pacific 40,000 Marine Services Americas 30,000 Trading & Industrial Europe ABOUT JOHN SWIRE & SONS LTD 20,000 Head Office Africa & Middle East 10,000 Marine Global# 0 • Established in 1816 and headquartered in London. 14 15 16 17 18 • Responsible for formulating and directing overall group strategy. Provides a range of services within the group, Employees 133,624 including recruitment, employment and training of staff. Employees | 2014-2018 Employees by Region | 2018 Employees by Division | 2018 • Holds a 55% shareholding in Swire Pacific in Hong Kong. Hong Kong Property 140,000 Mainland China Aviation • Holds controlling stakes in a range of businesses trading 120,000 Other Asia Beverages & in the UK, North America, Australia, Papua New Guinea, 100,000 By SW Pacific Food Chain East and West Africa, and across Southeast Asia. -

Factsheets of Sino-Ocean Taikoo Li Chengdu Factsheets

Sino-Ocean Taikoo Li Chengdu Located in the city centre of Chengdu, Sino-Ocean Taikoo Li Chengdu is jointly developed by Swire Properties and Sino-Ocean Group, comprises an open-plan, low-rise and lane-driven shopping mall, The Temple House, a boutique hotel with 100 rooms and 42 serviced apartments managed by Swire Hotels, as well as the 47- storey Grade A office tower Pinnacle One. Location : Close to the Chunxi Road retail district, the Complex is located in the Daci Temple area, south of Dacisi Road, east of Shamao Street in Jinjiang District, Chengdu Opening year : Grand opened in April 2015 Developer : Swire Properties Limited (50%) Sino-Ocean Group Holding Limited (50%) Architect : The Oval Partnership (HK) – Master Planner and Master Architect MAKE Architects (UK) – Hotel and Office Spawton Architecture Ltd & Elena Galli Giallini Ltd – For the Interior Design of the Basement Shopping Mall Total site area : Approx. 74,000 sqm / approx. 795,000 sq ft Gross floor area : Total GFA approx. 266,000 sqm / over 2.86 million sq ft Street-style retail – Sino-Ocean Taikoo Li Chengdu (Approx. 114,000 sqm / approx. 1.23 million sq ft) Intriguing urban hotel – The Temple House (100 guests rooms, over 21,000 sqm / over 227,000 sq ft) Residence (42 units, over 10,000 sqm / over 108,000 sq ft) Office tower – Pinnacle One (for trading purpose) (Approx. 121,000 sqm / approx. 1.3 million sq ft) Updated: Oct 2017 Car parking space : Approx. 1,000 (Shopping mall) Approx. 610 (Pinnacle One) Accessibility : The Complex has a direct connection to the interchange metro station of Line 2 and Line 3 Features : The architectural design of Sino-Ocean Taikoo Li Chengdu pays homage to traditional Sichuan architecture with an innovative, modern approach. -

Swire Pacific Limited Announces 2020 Annual Results

For immediate release 11th March 2021 Swire Pacific reports an underlying loss of HK$3,969 million in 2020 The progress of many of the Group’s businesses was arrested in 2020 by COVID-19. Cathay Pacific was particularly hard hit. The Group recorded an underlying loss of HK$3,969 million in 2020, compared with an underlying profit of HK$17,797 million in 2019. The deterioration in the results was primarily due to a significant reduction in profits on the sale of investment properties and to losses (including impairment charges and restructuring costs) at Cathay Pacific. Disregarding significant non-recurring items in both years, the 2020 recurring underlying loss was HK$609 million, compared with a profit of HK$7,221 million in 2019. Dividends for the full year are HK$1.70 per A share and HK$0.34 per B share. Below is a summary of the 2020 annual results: 2020 Annual Results Summary 2020 2019 HK$M HK$M Change % Revenue 80,032 85,652 -7% (Loss) / profit attributable to the Company’s shareholders As reported (10,999) 9,007 N/A Underlying (loss) / profit (3,969) 17,797 N/A Recurring underlying (loss) / profit (609) 7,221 N/A HK$ HK$ Change % (Loss) / earnings per share As reported ‘A’ share (7.32) 6.00 N/A ‘B’ share (1.46) 1.20 Underlying ‘A’ share (2.64) 11.85 N/A ‘B’ share (0.53) 2.37 HK$ HK$ Change % Full year dividends per share ‘A’ share 1.70 3.00 -43% ‘B’ share 0.34 0.60 … / Page 2 / …2 Divisional Highlights: Property Division • The recurring underlying profit from the Property Division in 2020 (which excludes gains from the sale of interests in investment properties aggregating HK$4,584 million, compared with HK$13,528 million in 2019) was HK$5,834 million, compared with HK$6,269 million in 2019. -

FAST FACTS 2021 CHINESE MAINLAND Cf210715e 2020 KEY FINANCIALS – CHINESE MAINLAND

FAST FACTS 2021 CHINESE MAINLAND CF210715e 2020 KEY FINANCIALS – CHINESE MAINLAND The Swire group’s principal areas of operation are Turnover US$6,302M in the Asia Pacific region, centred on Greater China, 太古 US$M US$M where the name or Taikoo, meaning “Great and 9,000 Ancient”, is a household name. Swire’s businesses 8,000 are grouped into five categories: Property, Aviation, 7,000 Beverages & Food Chain, Marine Services and Trading 6,000 By 5,000 & Industrial. These activities come under Hong Kong- Division 4,000 based, publicly quoted Swire Pacific Limited, or are 3,000 held by parent company, John Swire & Sons Limited. 2,000 1,000 Swire first opened an office in Shanghai in 1866 to 0 16 17 18 19 20 trade in tea and textiles. Today, the group’s interests in the Chinese Mainland range from properties and aircraft engineering to retailing. Swire subsidiaries are partners to some of the Chinese Mainland’s most successful companies, including Sino-Ocean Group Capital Employed US$17,015M Holding, Air China and COFCO. International partners on the Chinese Mainland include The Coca-Cola US$M US$M Company and The Boeing Company. 18,000 15,000 12,000 By Division^ 9,000 6,000 3,000 0 16 17 18 19 20 ^ A division may have negative capital employed. These figures have been excluded from the divisional breakdown. Employees 38,007 40,000 35,000 30,000 By 25,000 Division 20,000 15,000 10,000 5,000 0 16 17 18 19 20 Property Trading & Industrial Aviation Head Office Beverages & Food Chain Information within this document is prepared on a 100% basis for subsidiaries of the Swire group, direct joint ventures of the Swire group and associated companies (which have services agreements in place with the Swire group). -

Swire Properties Sustainable Development

SUSTAINABLE DEVELOPMENT REPORT 2017 TABLE OF CONTENTS 03 05 06 08 Chief Executive’s About Profile of SD 2030 Message this Report Swire Properties Limited Strategy 15 17 24 SD Materiality SUSTAINABLE Governance DEVELOPMENT IN ACTION: TaiKoo Hui 33 48 68 81 109 PLACES PEOPLE PARTNERS PERFORMANCE PERFORMANCE (ENVIRONMENT) (ECONOMIC) 121 124 126 GRI and HKEX ESG Reporting External Charters and Awards and Memberships Certifications 132 140 142 Performance Data Summary Assurance Report Global Reporting Initiative Content Index We welcome your feedback on our sustainable development 150 performance and reporting. You can contact us by email at HKEX ESG Reporting [email protected] or fill in the Guide Index PLACES PEOPLE PARTNERS PERFORMANCE PERFORMANCE MENU (ENVIRONMENT) (ECONOMIC) CHIEF EXECUTIVE’S MESSAGE 2017 was the first full calendar year of implementing our Sustainable Development (“SD”) strategy – what we call our SD 2030 Strategy – and the focus has been on ‘getting things done’. This strategy is aimed at ensuring that SD is integrated into every facet of our business, so it is vital that everyone at Swire Properties not only understands what our strategy is about, but also feels empowered to contribute to what we are trying to achieve. Our employees are critical to the implementation of the strategy and it has been heartening to see them getting involved at every level. I am particularly proud of the progress we are making to integrate SD throughout our business by breaking down geographic and functional silos. We have incorporated SD focus areas directly into our annual budget-planning processes and, most importantly, we are putting SD key performance indicators into action.