(P&C UK) Limited of Merchant Retail Group

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Developing Employees As Organisational Assets

Developing Employees as Organisational Assets INTRODUCTION The Kingfisher Recruitment • The Person Specification How KMDS is evolving commercial and afterwards in key functions The Group requires from prospec- Kingfisher plc is one of Europe’s leading retailers based Management Development Scheme Investing in a trainee over ten years tive KMDS trainees: The KMDS was launched in 1995 and • a post-graduate certificate in man- around three main sectors - DIY, electrical and general involves significant cost as well as today has 172 individuals on the scheme agement studies from Templeton • excellent interpersonal skills merchandise. The company employs over 130,000 people in invest- risk. The risk includes choosing the working across the Group. All individu- College, Oxford The KMDS represents a key • enthusiasm and drive to become ment by the organisation in its human wrong type of person and equally als following the KMDS route joined in • a ‘skills tool-box’ consisting of 2,900 stores across 15 countries and has some of the best senior managers within 7-10 years assets. The scheme takes high-poten- importantly losing the person to anoth- their early 20s. Recently Kingfisher has day-release training to develop per- known retail brands in Europe, including B&Q, Castorama, • innovative approach to challenges tial graduates who want to make a er organisation during the training recognised that there are benefits in sonal skills Comet, Darty, BUT, Woolworths and Superdrug among opening up the process to existing high- career in retail, and provides them with process. For this reason, Kingfisher • the ability to analyse and make • a ‘buddy’ who is already on the others. -

Case No COMP/M.2951 - A.S

EN Case No COMP/M.2951 - A.S. WATSON / KRUIDVAT Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 27/09/2002 Also available in the CELEX database Document No 302M2951 Office for Official Publications of the European Communities L-2985 Luxembourg COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 27.09.2002 SG (2002) D/231850 In the published version of this decision, some PUBLIC VERSION information has been omitted pursuant to Article 17(2) of Council Regulation (EEC) No 4064/89 concerning non-disclosure of business secrets and other confidential information. The omissions are MERGER PROCEDURE shown thus […]. Where possible the information ARTICLE 6(1)(b) DECISION omitted has been replaced by ranges of figures or a general description. To the notifying party Dear Sir/Madam, Subject: Case No COMP/M.2951 - A.S. Watson/Kruidvat Notification of 29.08.2002 pursuant to Article 4 of Council Regulation No 4064/891 1. On 29 August 2002, the Commission received a notification of a proposed concentration whereby A.S. Watson & Co., Limited (“A.S. Watson”), which belongs to the Hong Kong based group Hutchison Whampoa Limited (“Hutchison”), intends to acquire within the meaning of Article 3(1)(b) of the Council Regulation (EEC) No 4064/89 (“the Merger Regulation”) control over Dutch companies Kruidvat Holding B.V., and Kruidvat Superdrug B.V. (hereinafter ”Kruidvat”). The companies are presently controlled by Kruidvat Beheer B.V. (”Kruidvat Beheer”). 2. After examination of the notification, the Commission has concluded that the notified operation falls within the scope of the Merger Regulation and does not raise serious doubts as to its compatibility with the common market and the functioning of the EEA Agreement. -

2015 Annual Report

Ports and Related Services Retail Infrastructure Energy Telecommunications 2015 Annual Report 22nd Floor, Hutchison House, 10 Harcourt Hutchison House, Hong Kong Road, 22nd Floor, Telephone: +852 2128 1188 Facsimile: www.ckh.com.hk +852 2128 1705 Corporate Information CK Hutchison Holdings Limited Board of dIreCtors eXeCUtIVe dIreCtors NoN-eXeCUtIVe dIreCtors Chairman CHOW Kun Chee, Roland, LLM LI Ka-shing, GBM, KBE, LLD (Hon), DSSc (Hon) LEE Yeh Kwong, Charles, GBM, GBS, OBE, JP Commandeur de la Légion d’Honneur Grand Officer of the Order Vasco Nunez de Balboa LEUNG Siu Hon, BA (Law) (Hons), Hon LL.D. Commandeur de l’Ordre de Léopold George Colin MAGNUS, OBE, BBS, MA Group Co-Managing director and INdepeNdeNt NoN-eXeCUtIVe dIreCtors Deputy Chairman KWOK Tun-li, Stanley, BSc (Arch), AA Dipl, LLD (Hon), ARIBA, MRAIC LI Tzar Kuoi, Victor, BSc, MSc, LLD (Hon) CHENG Hoi Chuen, Vincent, GBS, OBE, JP Group Co-Managing director The Hon Sir Michael David KADOORIE, GBS, LLD (Hon), DSc (Hon) FOK Kin Ning, Canning, BA, DFM, FCA (ANZ) Commandeur de la Légion d’Honneur Commandeur de l’Ordre des Arts et des Lettres Commandeur de l’Ordre de la Couronne CHOW WOO Mo Fong, Susan, BSc Commandeur de l’Ordre de Leopold II Group Deputy Managing Director LEE Wai Mun, Rose, JP, BBA Frank John SIXT, MA, LLL Group Finance Director and Deputy Managing Director William Elkin MOCATTA, FCA Alternate to Michael David Kadoorie IP Tak Chuen, Edmond, BA, MSc Deputy Managing Director William SHURNIAK, SOM, LLD (Hon) KAM Hing Lam, BSc, MBA WONG Chung Hin, CBE, JP Deputy -

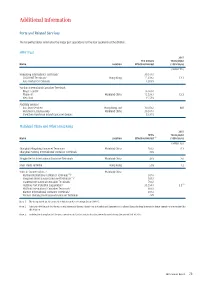

Additional Information

additional Information ports and related services The following tables summarise the major port operations for the four segments of the division. HpH trust 2015 The Group’s Throughput Name Location Effective Interest (100% basis) (million TEU) Hongkong International Terminals/ 30.07% / COSCO-HIT Terminals/ Hong Kong 15.03% / 12.1 Asia Container Terminals 12.03% Yantian International Container Terminals - Phase I and II/ 16.96% / Phase III/ Mainland China 15.53% / 12.2 West Port 15.53% Ancillary Services - Asia Port Services/ Hong Kong and 30.07% / N/A Hutchison Logistics (HK)/ Mainland China 30.07% / Shenzhen Hutchison Inland Container Depots 23.35% Mainland China and other Hong Kong 2015 HPH’s Throughput Name Location Effective Interest (1) (100% basis) (million TEU) Shanghai Mingdong Container Terminals/ Mainland China 50% / 8.3 Shanghai Pudong International Container Terminals 30% Ningbo Beilun International Container Terminals Mainland China 49% 2.0 River Trade Terminal Hong Kong 50% 1.2 Ports in Southern China - Mainland China (2) Nanhai International Container Terminals / 50% / (2) Jiangmen International Container Terminals / 50% / Shantou International Container Terminals/ 70% / (3) Huizhou Port Industrial Corporation/ 33.59% / 2.5 Huizhou International Container Terminals/ 80% / Xiamen International Container Terminals/ 49% / Xiamen Haicang International Container Terminals 49% Note 1: The Group holds an 80% interest in Hutchison Ports Holdings Group (“HPH”). Note 2: Although HPH Trust holds the economic interest in the two River Ports in Nanhai and Jiangmen in Southern China, the legal interests in these operations are retained by this division. Note 3: Includes the throughput of the port operations in Gaolan and Jiuzhou that were disposed during the second half of 2015. -

73 Watson Cover

Quarter 3 & 4 • 2007 A.S. Watson quarterly73 family magazine Superdurg thinks pink Fresh look • innovative concept On tour with Marionnaud PARKnSHOP shares Olympic spirit Watsons invests in people Wats Our Aroundthe world Focusstory Home Ourcommunity Hutchstory tents With a history dating back to 1828, the A.S. Watson Group (ASW) has evolved into an international retail and manufacturing businessn with operations in 36 th Co Fresh look innovative Superdrug thinks pink ...... Reaching the 300 Small bears for big Li's donation a tribute to markets worldwide. Today, the Group owns more than 7,800 retail stores concept...... milestone...... benefits...... those who choose to running the gamut from health & beauty chains, luxury perfumeries & cosmetics serve...... to food, electronics, fine wine and airport retail arms. An established player 21 34 in the beverage industry, ASW provides a full range of beverages from bottled water, fruit juices, soft drinks and tea products to the world’s finest wine labels 27 38 via its international wine wholesaler and distributor. 05 ASW employs over 98,000 staff and is a member of the world renowned Hong Kong-based conglomerate Hutchison Whampoa Limited, which has five core businesses - ports and related services; property and hotels; retail; energy, About A.S. Watson Group About A.S. Watson infrastructure, investments and others; and telecommunications in 55 countries. Editorial committee Published by • Adviser : Dominic Lai • Members : A.S. Watson & Co., Limited Wats On is the quarterly family magazine of the A.S. Watson Group. • Editor : Malina Ngai Group Office – Anna Tam, Jenny Cabrol, Anthea Chau Watson House, 1-5 Wo Liu Hang Road, Fotan, Hong Kong Health & Beauty – Nuanphan Pat Jayanama, Rita Wong, Jessin Yeung Email: [email protected] Materials from this publication may only be reprinted with full © Copyright A.S. -

Has Today Made the Attached Presentation (The “Presentation”) to Investors of the Company

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. (incorporated in Hong Kong with limited liability) (Stock Code: 13) ANNOUNCEMENT Hutchison Whampoa Limited (the “Company”) has today made the attached presentation (the “Presentation”) to investors of the Company. Potential investors and shareholders of the Company (the “Potential Investors and Shareholders”) are reminded that the Presentation includes publicly available third party information as well as historical financial information of the Company, recent operational data and best estimates by management of current market performance. Much of the information in the Presentation by its nature is not normally subject to independent review or audit and accordingly has not been reviewed or audited by the Company’s auditors. Potential Investors and Shareholders should exercise caution when dealing in the shares of the Company. By Order of the Board Edith Shih Company Secretary Hong Kong, 6 October 2011 As at the date of this announcement, the directors of the Company are: Executive Directors: Independent Non-executive Directors: Mr LI Ka-shing (Chairman) The Hon Sir Michael David KADOORIE Mr LI Tzar Kuoi, Victor (Deputy Chairman) Mr Holger KLUGE Mr FOK Kin-ning, Canning Mrs -

Encouraging the Chasing Abottle Or of Filling the Perfume up Kettle with Water for Acup of Tea

• • Encouraging the Cover Story HWL’s diverse businesses in the UK have one thing in common – they place great emphasis on the human factor By Mark Redvers DURING THE COURSE OF A TYPICAL DAY, millions of many different sectors, from the nation’s biggest and most Britons buy a product, or use a service, that has some connec- active ports, its fastest-growing 3G network, to some of its best- tion with Hutchison Whampoa Limited (HWL), whether it is known drug and perfume stores and various infrastructure receiving a text via the 3 phone network, buying a fridge projects that include water, electricity and property. that has been imported by a container ship, pur- HWL sees vast opportunities in the country, despite its chasing a bottle of perfume or filling up the current recession-hit status, and has grand plans for continued kettle with water for a cup of tea. commitment to this nation of 62 million people. In fact its HWL investments in entire philosophy is geared towards the long haul, with the UK cover constant investment in training schemes that enhance the skills of the workforce. 12 Sphere Surprisingly, perhaps, HWL is not a name that is widely employers in their immediate areas, so HPH-initiated schemes known outside the UK business community, even though the there, together with a similar scheme at London Thamesport, company has something like GBP17 billion invested in the allow children to learn how docks work, and the role they play country in companies that include Superdrug, the Perfume in creating jobs and generating wealth. -

Hutchison Whampoa Limited Annual Report 2005 18 16 12 32 27 23 20 35 30 26 24 17 28 13 31 29 25 21 19 33 22 14 36 3 15 8 34 4 5 9 6 11 2 10 7

OPERATIONS REVIEW 32 Hutchison Whampoa Limited Annual Report 2005 18 16 12 32 27 23 20 35 30 26 24 17 28 13 31 29 25 21 19 33 22 14 36 3 15 8 34 4 5 9 6 11 2 10 7 1 1 Australia 7 Indonesia 13 Romania 19 Slovenia 25 Austria 31 France 2 The Philippines 8 Mainland China 14 Turkey 20 Lithuania 26 Germany 32 United Kingdom 3 South Korea 9 Thailand 15 Israel 21 Hungary 27 The Netherlands 33 Spain 4 Taiwan 10 Singapore 16 Latvia 22 Italy 28 Luxembourg 34 Morocco 5 Hong Kong 11 Malaysia 17 Slovakia 23 Poland 29 Switzerland 35 Republic of Ireland 6 Macau 12 Russia 18 Estonia 24 Czech Republic 30 Belgium 36 Portugal Retail The retail division consists of the A S Watson group of companies, one of the world’s largest and most diversified retailers currently operating 11 retail chains in Europe and four major retail chains in Asia, with more than 7,100 stores in 36 markets worldwide that provide high quality personal care, health and beauty products; luxury perfumery and cosmetic products; food, wine and general merchandise; and consumer electronic and electrical appliances. A S Watson also manufactures and distributes various water and other beverages in Hong Kong and the Mainland. Hutchison Whampoa Limited Annual Report 2005 33 OPERATIONS REVIEW Retail These businesses are managed under four principal operating divisions: Health and Beauty; Luxury Perfumeries and Cosmetics; Food, Electronics and General Merchandise (“FEGM”); and Manufacturing. Total revenue for the retail division totalled HK$88,780 million, an increase of 30% compared to last year, mainly due to contributions from Marionnaud Parfumeries (“Marionnaud”) and The Perfume Shop, which were acquired in April and August respectively; a full-year contribution from the Rossmann retail chain in Germany, in which a 40% interest was acquired in August 2004; and also continued sales growth in PARKnSHOP and Watsons in the Mainland, Watsons in Taiwan and the UK retail operations. -

Watsons Experience Launches in Russia Focus Story

103 Watsons Experience Launches in Russia Focus Story Watsons Experience Launches in Russia Watsons is delighted to have opened its first Russian store in St.Petersberg. The launch of Asia’s No.1 health and beauty brand will deliver an unprecedented range of world-class products to the increasingly sophisticated Russian market. This is a country where people take great care over their appearance, and by introducing the products and advanced skincare regimens of Asia, Watsons taps into what it sees as huge market potential. WatsON 103 • Quarter 2 • 2018 01 Focus Story Russia will be the 12th market to host Watsons stores. In every market where it operates, Watsons sets the highest global standards in the health, wellness and beauty market. Putting customers first is what Watsons is all about. It offers customers real value, good service and expert advice – and St.Petersberg this is what Watsons will present to Russian customers. The launch of the first store in Russia is a significant step in the expansion of the Watsons brand. Watsons “cares deeply about its customers around the globe, addressing their health and beauty needs both instore and online. We are dedicated to making our customers Look Good and Feel Great and putting a smile on their faces. Andrei Melnikov ” General Manager Watsons Russia WatsON 103 • Quarter 2 • 2018 02 Focus Story Emerging Market, Golden Opportunity Russian customers are seeking out both new experiences Beauty trends from Asia and especially from Korea and new products in health and beauty. Russian is a – hugely popular across Asia but underdeveloped in Russia magnet for sophisticated travellers from across Europe, Digital and eCommerce solutions, which are well and it has significant potential for future growth. -

Principal Subsidiary and Associated Companies and Joint Ventures at 31 December 2020

Principal Subsidiary and Associated Companies and Joint Ventures at 31 December 2020 Nominal value of Place of incorporation / issued ordinary Percentage of Subsidiary and associated companies and principal place of share capital **/ equity attributable joint ventures operations registered capital to the Group Principal activities Ports and related services Alexandria International Container Terminals Egypt USD 30,000,000 59 Container terminal operating Company S.A.E. Amsterdam Container Terminals B.V. Netherlands EUR 18,400 80 Container terminal operating Brisbane Container Terminals Pty Limited Australia AUD 34,100,000 80 Container terminal operating Buenos Aires Container Terminal Services S.A. Argentina ARS 648,385,014 80 Container terminal operating ECT Delta Terminal B.V. Netherlands EUR 18,000 71 Container terminal operating Ensenada Cruiseport Village, S.A. de C.V. Mexico MXP 145,695,000 80 Cruise terminal operating Ensenada International Terminal, S.A. de C.V. Mexico MXP 160,195,000 80 Container terminal operating Europe Container Terminals B.V. Netherlands EUR 45,000,000 75 Holding company Euromax Terminal Rotterdam B.V. Netherlands EUR 100,000 49 Container terminal operating Freeport Container Port Limited Bahamas BSD 2,000 41 Container terminal operating Gdynia Container Terminal S.A. Poland PLN 11,379,300 80 Container terminal operating and rental of port real estate Harwich International Port Limited United Kingdom GBP 16,812,002 80 Container terminal operating ✡ Hongkong United Dockyards Limited Hong Kong HKD 76,000,000 50 Ship repairing, general engineering and tug operations ✡ 惠州港業股份有限公司 China RMB 300,000,000 27 Container terminal operating ✡ Huizhou Quanwan Port Development Co., Ltd. -

Solid Foundation Fosters Long-Term Development

20 1 7 Annual Report Solid Foundation Fosters Long-term Development 22nd Floor, Hutchison House, 10 Harcourt Road, Hong Kong Telephone: +852 2128 1188 2017 Annual Report Facsimile: +852 2128 1705 www.ckh.com.hk WorldReginfo - 7a0610cc-4251-4d12-8195-61d40b71508e Corporate Information CK Hutchison Holdings Limited BOARD OF DIRECTORS EXECUTIVE DIRECTORS NON-EXECUTIVE DIRECTORS Chairman CHOW Kun Chee, Roland, LLM LI Ka-shing, GBM, KBE, LLD (Hon), DSSc (Hon) CHOW WOO Mo Fong, Susan, BSc Commandeur de la Légion d’Honneur Grand Officer of the Order Vasco Nunez de Balboa LEE Yeh Kwong, Charles, GBM, GBS, OBE, JP Commandeur de l’Ordre de Léopold LEUNG Siu Hon, BA (Law) (Hons), LL.D. (Hon) Group Co-Managing Director and George Colin MAGNUS, OBE, BBS, MA Deputy Chairman LI Tzar Kuoi, Victor, BSc, MSc, LLD (Hon) INDEPENDENT NON-EXECUTIVE DIRECTORS Group Co-Managing Director KWOK Tun-li, Stanley, BSc (Arch), AA Dipl, LLD (Hon), ARIBA, MRAIC FOK Kin Ning, Canning, BA, DFM, FCA (ANZ) CHENG Hoi Chuen, Vincent, GBS, OBE, JP Frank John SIXT, MA, LLL The Hon Sir Michael David KADOORIE, GBS, LLD (Hon), DSc (Hon) Group Finance Director and Deputy Managing Director Commandeur de la Légion d’Honneur Commandeur de l’Ordre des Arts et des Lettres IP Tak Chuen, Edmond, BA, MSc Commandeur de l’Ordre de la Couronne Deputy Managing Director Commandeur de l’Ordre de Leopold II (William Elkin MOCATTA, FCA as his alternate) KAM Hing Lam, BSc, MBA Deputy Managing Director LEE Wai Mun, Rose, JP, BBA LAI Kai Ming, Dominic, BSc, MBA William SHURNIAK, S.O.M., M.S.M., LLD -

Daohengsecurities Ltd

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should consult your stockbroker or other registered dealer in securities, bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in CK Life Sciences Int’l., (Holdings) Inc., you should at once hand this circular and the accompanying proxy form to the purchaser or the transferee or to the bank, stockbroker or other agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. The Stock Exchange of Hong Kong Limited takes no responsibility for the contents of this circular, makes no representation as to its accuracy or completeness and expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. (Incorporated in the Cayman Islands with limited liability) (Stock Code: 8222) PROPOSED ELECTION OF DIRECTORS AT THE ANNUAL GENERAL MEETING, PROPOSED GENERAL MANDATES TO ISSUE NEW SHARES AND REPURCHASE SHARES AND CONTINUING CONNECTED TRANSACTIONS – RENEWAL OF THE EXISTING CKH SUPPLY AGREEMENT AND THE EXISTING HIL SUPPLY AGREEMENT Independent financial adviser to the Independent Board Committee and the Independent Shareholders in relation to the Continuing Connected Transactions DaoHengSecurities Ltd. A proxy form for use at the Annual General Meeting of the Company to be held at the Ballroom, 1st Floor, Harbour Plaza Hong Kong, 20 Tak Fung Street, Hung Hom, Kowloon, Hong Kong on 12 May 2005 is enclosed with this circular.