Southwark Employment Land Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

KINGSTON Upon THAMES - LOCAL SERVICES April 2014 KINGSTON Upon THAMES

KINGSTON upon THAMES - LOCAL SERVICES April 2014 KINGSTON upon THAMES 1. SPEECH AND LANGUAGE THERAPY SERVICE(s) Your Health Care www.yourhealthcare.org/Services/speech-and-language-therapy.htm Various clinics & locations Pre-school children: Carmel Brady 020 8274 7814 online email form School age children: Linda Talbot 020 8547 6670 SLT at Services for Disabled Children, The Moor Lane Centre 020 8547 6527 www.kingston.gov.uk/info/200247/supporting_disabled_children_and_their_families/510/services_for_disabled_children/7 2. Royal Borough of KINGSTON upon THAMES 020 8547 5000 www.kingston.gov.uk Guildhall, High Street, Kingston upon Thames KT1 1EU [email protected] • SPECIAL EDUCATIONAL NEEDS Special Educational Needs 020 8547 5004 www.kingston.gov.uk/info/200230/special_education_needs_sen Children, Schools and Families, [email protected] Guildhall 2, High Street, Kingston upon Thames KT1 1EU • EDUCATIONAL PSYCHOLOGY Educational Psychology Team The Moor Lane Centre, Moor Lane, Chessington, Surrey KT9 2AA (referral through schools only) 3. SCHOOLS with specialist Speech and Language provision The following school has specialist provision for Speech & Language difficulties: Castle Hill Primary School 020 8397 2006 www.castlehill.kingston.sch.uk Buckland Road, Chessington, Surrey KT9 1JE [email protected] 4. PARENT PARTNERSHIP EnhanceAble Anna Fayda: PPS officer 020 8547 6200 www.enhanceable.org/parentpartnership.htm EnhanceAble Children's Services, The Moor Lane Centre, [email protected] Moor Lane, Chessington, Surrey KT9 2AA 5. PARENT and CARER FORUM Kingston Parents Forum 020 8546 3258 http://e-voice.org.uk/parentsforum/ KINGSTON upon THAMES - LOCAL SERVICES April 2014 53-55 Canbury Park Road, Kingston upon Thames, Surrey KT2 6LQ [email protected] 6. -

The Growth of London Through Transport Map of London’S Boroughs

Kingston The growth of London through transport Map of London’s boroughs 10 The map shows the current boundaries of London’s Key boroughs. The content of 2 1 Barking 17 Hillingdon this album relates to the & Dagenham 15 31 18 Hounslow area highlighted on the map. 14 26 2 Barnet 16 19 Islington This album is one of a 3 Bexley 20 Kensington series looking at London 17 4 6 12 19 4 Brent & Chelsea boroughs and their transport 1 25 stories from 1800 to the 5 Bromley 21 Kingston 9 30 present day. 33 7 6 Camden 22 Lambeth 23 Lewisham 7 City of London 13 20 28 8 Croydon 24 Merton 18 11 3 9 Ealing 25 Newham 22 32 23 26 Redbridge 27 10 Enfield 11 Greenwich 27 Richmond 28 Southwark 24 12 Hackney 29 Sutton Kingston 13 Hammersmith 21 5 & Fulham 30 Tower Hamlets 29 8 14 Haringey 31 Waltham Forest 15 Harrow 32 Wandsworth 16 Havering 33 Westminster A3 RICHMOND RIVER A307 THAMES ROAD KINGSTON A308 UPON Kingston Hill THAMES * * Kings Road Kingston A238 Turks Pier Norbiton * * Bentalls A3 * Market Place NEW * Cambridge* A2043 Road MALDEN Estates New Malden A307 Kingston Bridge Berrylands KINGSTON SURBITON RIVER THAMES UPON KINGSTON BY PASS THAMES Surbiton A240 A3 Malden Beresford Avenue* Manor Worcester Park A243 A309 A240 A3 Tolworth Haycroft* Estate HOOK A3 0 miles ½ 1 Manseld* Chessington Road North 0 kilometres 1 Chessington South A243 A3 A243 * RBK. marked are at theLocalHistoryRoom page. Thoseinthecollection atthebottomofeach are fortheimages References the book. can befoundatthebackof contributing tothisalbum Details ofthepartner theseries. -

Local Support Services Guide

LOCAL SUPPORT SERVICES GUIDE Kingston Race and Equalities Council Neville House 55 Eden Street Kingston upon Thames Surrey KT1 1BW Phone: 0208 547 2332 Fax: 0208 547 1510 Website: www.kingstonrec.org Asylum and Immigration Tribunal (A.I.T.) 17 Ewell Road Sessions House Surbiton Surrey, KT6 6AQ Tel: 0845 6000 877 Website: www.ait.gov.uk Refugee Action Kingston Kathryn Betham Siddeley House, 50 Canbury Park Road, Kingston Upon Thames, Surrey KT26LX Tel:020 8547 0115 Fax: 020 8547 1114 Website: www.refugeeactionkingston.org.uk Kingston Racial Equality Council. John Azah, DirectorWelcare House53-55 Canbury Park RoadKingston upon Thames Surrey KT26LQ Tel: 020 8547 2332 Website: www.kingstonrec.org Kingston Interpreting Service Barbara Morton: Guildhall 1 Kingston upon Thames KT11EU Tel: 020 8547 5822 Kingston Churches Action for Homeless People 36a Fife Rd, Kingston upon Thames, Surrey KT1 1SU Telephone: 020 8255 7400 Website: www.kcah.org.uk Gypsy & Traveller Education Service Co-ordinator (Royal Borough of Kingston Traveller Education Service) Tel: 07826 955 967 Website: www.kingston.gov.uk/gypsyandtravellersupportservice.htm Domestic Violence - Domestic Violence Helpline: 0808 2000 247 this is a free 24 hour helpline run by women’s aid and refuge Website: www.kingston.gov.uk/domestic_violence - Kingston Domestic Violence One Stop Shop is a service providing information and confidential support to people who have experienced domestic violence. It is held every Monday 9.30am to 12.30pm In the Baptist Church Union Street Kingston KT1 1RP - -

19+Neville+Avenue.Pdf

Amberwood 19 Neville Avenue, New Malden, Surrey, KT3 4SN GUIDE PRICE £4,250,000 WWW.COOMBERESIDENTIAL.COM LOCATION Neville Avenue is one of the premiere roads within the exclusive Coombe House Private estate which is approached from top off Traps Lane or from Warren Rise off Coombe Lane West. This wonderfully friendly estate is equidistant between Kingston and Wimbledon town centres. Both have excellent shopping facilities, from department stores housing concessions found in famous West End streets and specialised boutiques to a wide range of restaurants meeting the palates from across the world. The A3 trunk road offers fast access to central London and both Gatwick and Heathrow airports via the M25 motorway network. The nearest train station at New Malden is within walking distance and the 57 bus route runs along nearby Coombe Lane West to Wimbledon from where there are frequent services to Waterloo with its underground links to points throughout the city. The immediate area offers a wide range of recreational facilities including five golf courses, tennis and squash clubs and many leisure centres. The 2,360 acres of Richmond Park, an area of outstanding beauty easily accessed from Kingston Gate and Ladderstile Gate, provide a picturesque setting in which to picnic, go horse riding, jogging or just take a leisurely walk. Theatres at Wimbledon and Richmond are also popular alternatives to the West End. There are numerous excellent local schools for all ages, private, state and a variety of international educational establishments, many within walking distance. The Coombe House private estate is extremely well run and managed by the residents. -

PORTSMOUTH ROAD the Thames Landscape Strategy Review 1 9 7

REACH 03 PORTSMOUTH ROAD The Thames Landscape Strategy Review 1 9 7 Landscape Character Reach No 3 PORTSMOUTH ROAD 4.03.1 Overview 1994-2012 • Construction of new cycle/footpath along Barge Walk and the opening of views across the river • Habitat enhancement in the Home Park including restoration of acid grassland • Long-running planning process for the Seething Wells fi lter beds • TLS initiative to restore the historic Home Park water meadows. • RBKuT Kingston Town Centre Area Action Plan K+20 • RBK and TLS Integrated Moorings Business Plan • Management of riverside vegetation along the Barge Walk • Restoration of the Long Water Avenue in 2006 LANDSCAPE CHARACTER 4.03.2 The Portsmouth Road Reach runs north from Seething Wells up to Kingston. The reach has a character of wide open grassland, interrupted only by trees, park and water-works walls and the Portsmouth Road blocks of fl ats. Hampton Court Park extends over the entire Middlesex side right up to Hampton Wick, while the Surrey bank divides between the former Water Works and the Queen’s Promenade. The Portsmouth Road follows the river the length of the reach on the Surrey side. This is one of the only sections of the upstream London Thames where a road has been built alongside the river. The busy road and associated linear developments make a harsh contrast with the rhythm of parkland and historic town waterfronts which characterise the rest of the river. Portsmouth Road 4.03.3 Hampton Court Park is held in the circling sweep of the Thames, as its fl ow curves from south to north. -

Mobile-Friendly Guide

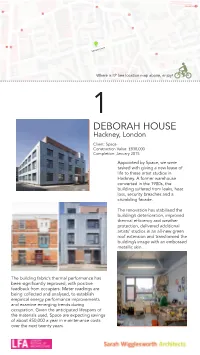

Retreat place Where is it? See location map above, enjoy! 1 DEBORAH HOUSE Hackney, London Client: Space Construction Value: £838,000 Completion: January 2015 Appointed by Space, we were tasked with giving a new lease of life to these artist studios in Hackney. A former warehouse converted in the 1980s, the building suffered from leaks, heat loss, security breaches and a crumbling facade. The renovation has stabilised the building’s deterioration, improved thermal efficiency and weather protection, delivered additional artists’ studios in an all-new green roof extension and transformed the building’s image with an embossed metallic skin. The building fabric’s thermal performance has been significantly improved, with positive feedback from occupiers. Meter readings are being collected and analysed, to establish empirical energy performance improvements and examine emerging trends during occupation. Given the anticipated lifespans of the materials used, Space are expecting savings of about £50,000 a year in maintenance costs over the next twenty years. Tower Bridge Rd Where is it? See location map above, enjoy! 2 BERMONDSEY BICYCLE STORE Bermondsey, London Client: Igloo Regeneration Construction Value: £120,000 Completion: 2008 Bermondsey Bicycle Store forms a striking entrance to Bermondsey Square – a lively public space at the heart of an ambitious regeneration project in south-east London. Embedding green transport values within the local community, the store accommodates 76 bikes belonging to the square’s workers and residents. Using ordinary materials in an original and exciting manner, the intervention adds sparkle to Igloo’s vision for inner city living. Drawing on the narrative of silver trinkets and treasures past, the landscaping is conceived as a textured carpet adorned with jewel-like street objects. -

404 Ewell Road TOLWORTH Surrey KT6 7HG New Lease Or

020 7493 9911 15 Bolton Street, Mayfair, London, W1J 8BG w: www.ianscott.com 402 – 404 Ewell Road TOLWORTH Surrey KT6 7HG New Lease or Freehold ( with VP ) Available Location: Tolworth is a popular London suburb some 3 miles south of Kingston Upon Thames whilst close to Surbiton, New Malden and Wimbledon with excellent road communications to the A3, and therefore easy access to both Central London and M25 motorway. The famous 22 storey Tolworth Tower nearby has recently received planning consent for conversion of the offices into over 100 new homes as well as 68 serviced apartments. The property is prominently situated just off the Broadway in a parade of other shops with on street parking available at the front. Nearby occupiers include B & M, Sainsbury Local, Iceland, Tesco Express / Esso Garage and M & S Simply Food. Accommodation: The property comprises the following approximate dimensions and floor areas - Net Frontage - 41' ( 12.49 m ) Internal Width - 40' 7'' (12.36 m ) Shop Depth - 40' 4'' ( 12.29 m ) Built Depth - 73' 4'' ( 22.35 m ) Ground Floor retail - 1890 sq ft ( 175.5 sq m ) Ground Floor - Rear External Self contained storeroom - 656 sq ft ( 61 sq m ) First Floor Offices / ancillary / WC's - 1508 sq ft ( 140 sq m ) Tenure: The property is available (subject to agreeing vacant possession ) on a new lease for a term to be agreed seeking rental offers of £50,000 pax. Freehold: Our client may also consider a FH sale (with full vacant possession) seeking offers in excess of £675,000 excl. Vat . -

Where to Stayin Kingston

Where to Stay in Kingston Kingston and the surrounding area offers a range of accommodation to suit all tastes, including 4 star and budget hotels, family run guesthouses and bed and breakfasts. Hotels Antoinette Hotel Beaufort Road, Kingston upon Thames, Surrey KT1 2TQ 020 8546 1044 www.antoinettehotel.com Distance from Kingston: 0.9 miles Brook Kingston Lodge Hotel 94 Kingston Hill, Kingston Upon Thames, Surrey KT2 7NP 020 8541 4481 www.brook-hotels.co.uk Distance from Kingston: 1.8 miles The Bull and Bush Hotel Washington Road, Kingston upon Thames, Surrey KT1 3JB 020 8549 4488 www.thebullandbush.net Distance from Kingston: 0.8 miles Chase Lodge Hotel 10 Park Road, Kingston upon Thames, Surrey KT1 4AS 020 8943 1862 www.chaselodgehotel.com Distance from Kingston: 0.5 miles Ditton Lodge Hotel 47 Lovelace Road, Surbiton, Surrey KT6 6NZ 020 8399 7482 www.dittonlodge.co.uk Distance from Kingston: 2.3miles Hermes Hotel 1 Portsmouth Road, Kingston upon Thames, Surrey KT1 2LU 020 8546 5322 www.hermes-hotel.co.uk Distance from Kingston: 0.7 miles Holiday Inn London – Kingston South Portsmouth Road, London, Surrey KT6 5QQ 020 8786 6505 www.hikingston.co.uk Distance from Kingston: 1.8 miles Holiday Inn Hotel London-Chessington Leatherhead Road, Chessington KT9 2NE 0870 890 0567 www.holidayinn.com Distance from Kingston: 4.8 miles Hotel Bosco 9 Saint Mark's Hill, Surbiton, Surrey KT6 4LQ 020 8339 5720 www.hotelbosco.co.uk Distance from Kingston: 1.5 miles The Lensbury Broom Road, Teddington, Middlesex TW11 9NU 020 8614 6400 www.lensbury.com -

The Collaborative City

the londoncollaborative The Collaborative City Working together to shape London’s future March 2008 THE PROJECT The London Collaborative aims to increase the capacity of London’s public sector to respond to the key strategic challenges facing the capital. These include meeting the needs of a growing, increasingly diverse and transient population; extending prosperity while safe- guarding cohesion and wellbeing, and preparing for change driven by carbon reduction. For more information visit young- foundation.org/london Abbey Wood Abchurch Lane Abchurch Yard Acton Acton Green Adams Court Addington Addiscombe Addle Hill Addle Street Adelphi Wharf Albion Place Aldborough Hatch Alder- manbury Aldermanbury Square Alderman’s Walk Alders- brook Aldersgate Street Aldersgate Street Aldgate Aldgate Aldgate High Street Alexandra Palace Alexandra Park Allhal- lows and Stairs Allhallows Lane Alperton Amen Corner Amen CornerThe Amen Collaborative Court America Square City Amerley Anchor Wharf Angel Working Angel Court together Angel to Court shape Angel London’s Passage future Angel Street Arkley Arthur Street Artillery Ground Artillery Lane Artillery AperfieldLane Artillery Apothecary Passage Street Arundel Appold Stairs StreetArundel Ardleigh Street Ashen Green- tree CourtFORE WAustinORD Friars Austin Friars Passage4 Austin Friars Square 1 AveINTRO MariaDUctio LaneN Avery Hill Axe Inn Back6 Alley Back of Golden2 Square OVerVie WBalham Ball Court Bandonhill 10 Bank Bankend Wharf Bankside3 LONDON to BarbicanDAY Barking Barkingside12 Barley Mow Passage4 -

The Royal Borough of Kingston Upon Thames

The Royal Borough of Kingston upon Thames Health and Care Plan 2019-2021 Kingston’s Health and Care Plan 2019-2021 – an introduction from Cllr Liz Green, Chair of the Health and Wellbeing Board Local people have been involved in the development of this two year Health and Care Plan for Kingston which brings together our commitment to deliver on the health and care priorities important to them. This plan focuses on the actions which no single organisation could achieve alone. In addition to all the other work we do, this plan is about our local NHS, the Council, voluntary and community services working better as a whole system to improve health and care together. Across all of our organisations, there are significant financial challenges ahead and this plan is, therefore, incredibly important for prioritising our resources where they are needed most. These priorities and actions identified for children to start well, for adults to live well, for people to age well, for carers to be supported and for prevention to be championed across all ages, have been endorsed by local people, the voluntary and community sector and professionals across the health and care system. Cllr Liz Green Chair of the Health and Wellbeing Board August 2019 The Royal Borough of Kingston upon Thames Health and Care Plan 2 2019-2021 Contents Our health and care partnership and joint vision 4 The Kingston story 8 The challenges we face in health and care in the borough of Kingston Start well 11 Live well 14 Age well 17 The wider determinants of health in the borough -

Richmond Upon Thames Est Un Quartier De Londres Richmond Upon Thames È Una Cittadina Di Londra De Todos Los Municipios Londinenses, Richmond Unique

www.visitrichmond.co.uk 2011 - 04 historic gems 2011 - 06 riverside retreat RICHMOND - 2011 08 open spaces 2011 - 10 museums and galleries UPON 2011 - 12 eating out 2011 - 14 shopping 2011 - 16 ghosts and hauntings THAMES 2011 - 18 attractions 2011 - 26 map VisitRichmond Guide 2011 2011 - 28 richmond hill 2011 - 30 restaurants and bars 2011 - 36 accommodation 2011 - 45 events 2011 - 50 travel information French Italian Spanish Richmond upon Thames est un quartier de Londres Richmond upon Thames è una cittadina di Londra De todos los municipios londinenses, Richmond unique. Traversé par la Tamise sur 33 kilomètres unica. Attraversata dal Tamigi che scorre lungo upon Thames es único. Por su centro pasa el río de campagne bordée de maisons élégantes et de 33km di campagna passando di fronte a case Támesis, que fl uye a lo largo de 33 kilómetros beaux jardins. La rivière relie le palais de Hampton eleganti e bellissimi giardini, il fi ume collega il de paisaje, pasando ante viviendas elegantes Court et les jardins botaniques royaux de Kew aux Palazzo di Hampton Court e I Giardini Botanici Reali y hermosos jardines. El río enlaza el palacio de villes de Richmond et de Twickenham. En explorant di KEW alle cittadine di Richmond e Twickenham. Hampton Court y el Real Jardín Botánico de ce lieu de résidence favorite de la royauté, des Esplorando questa località già dimora favorita Kew con las villas de Richmond y Twickenham. grands peintres et des hommes d’Etat, on découvre dalla famiglia reale, da grandi artisti ed uomini Lugar predilecto de la realeza, de hombres de des parcs magnifi ques, des styles d’architecture di stato, potrete scoprire I magnifi ci parchi, gli estado y grandes artistas, cuenta con parques originaux et toute une variété de restaurants et de originali stili architettorici oltre ad un’ ampia varietà magnífi cos y estilos inspirados de arquitectura pubs. -

CBRE Hot 100 the Winners of London’S Residential Market Contents

CBRE Hot 100 The winners of London’s residential market Contents Boroughs to buy in 03 Tallest completed towers in London 07 Tallest future towers in London 08 Niche developments 09 Riverside schemes 11 First-time buyer locations 13 Most expensive commuter towns 17 Most affordable commuter towns 17 Addresses 19 Crossrail winners 21 3 | 4 Top 10 1. Camden 2. Merton 3. Richmond upon Thames 4. Southwark Boroughs to buy in AVeraGE house price: AVeraGE rent (pcm): AVeraGE house price: AVeraGE rent (pcm): AVeraGE house price: AVeraGE rent (pcm): AVeraGE house price: AVeraGE rent (pcm): £3,844 £1,804 £2,215 £1,840 AVeraGE Yield: AVeraGE Yield: AVeraGE Yield: AVeraGE Yield: We have considered a number of economic and housing 4.5% 5.3% 4.9% 5.5% market metrics to identify the London Boroughs 2013 price Growth: 2013 price Growth: 2013 price Growth: 2013 price Growth: with the most potential for capital growth over the 11% 9.4% 8.6% 9.8% next few years. The metrics include demographic £687,539 £380,656 £514,439 £428,742 trends, forthcoming regeneration and infrastructure As a borough, Camden boasts an array of Despite being relatively close to Central Richmond is also popular because of its The north of the borough is now one of the improvements, the rental market, house price trends desirable areas; from the bustling market London with good transport links in and village-like appeal, aided by its expansive most popular spots in London, following and the socio-economic backdrop. and lively music scene that is Camden out, Merton is one of London’s quieter park and enviable riverside location.