Volatility Asymmetry of Scale Indexes - Taking China As an Example

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

指数单张 Factsheet Returns and Volatility Annual Performances Free

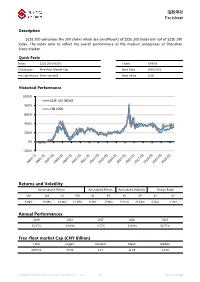

指数单张 Factsheet ————————————————————————————————————————————————————————— Description SZSE 200 comprises the 200 stocks which are constituents of SZSE 300 Index but not of SZSE 100 Index. The index aims to reflect the overall performance of the medium enterprises of Shenzhen Stock Market. Quick Facts Index SZSE 200 INDEX Ticker 399006 Calculation Free-float Market Cap Base Date 2010/5/31 Periodic Review Semi-annually Base Value 1000 Historical Performance 1000% SZSE 200 INDEX 800% CNI 1000 600% 400% 200% 0% -200% Returns and Volatility Accumulative Return Annualized Return Annualized Volatility Sharpe Ratio 1M 3M 1Y YTD 3Y 5Y 3Y 5Y 3Y 5Y 9.96% 18.99% 28.86% 15.39% 0.20% -7.98% 24.44% 28.63% 0.56% -1.20% Annual Performances 2019 2018 2017 2016 2015 33.57% -33.69% -3.57% -23.09% 50.77% SZSE 200 Index Free-float market Cap (CNY Billion) Total Largest Smallest Mean Median 2476.51 37.96 1.17 12.38 11.30 Copyright©2020 Shenzhen Securities Information Co., Ltd. 1/2 As of June 2020 指数单张 Factsheet ————————————————————————————————————————————————————————— Sector Breakdown Market Breakdown Sector No. of Constituents Weight Market No. of Constituents Weight Information Technology 44 30.19% SZSE Main Borad 65 23.95% Materials 36 14.90% SME Borad 85 45.98% Health Care 23 13.90% ChiNext Borad 50 30.07% Industrials 26 12.05% SSE Main Board 0 0.00% Consumer Discretionary 19 8.20% Financials 17 6.32% Fundamentals Consumer Staples 10 4.63% PE 27.19 Real Estate 11 3.99% PB 2.42 Telecommunication Services 7 3.75% ROE 7.79% Energy 4 1.31% Utilities 3 0.76% -

Ground Rules for the Szse 100 Index Szse 300 Index Szse

GROUND RULES FOR THE SZSE 100 INDEX SZSE 300 INDEX SZSE 200 INDEX SZSE 700 INDEX SZSE 1000 INDEX Shenzhen Securities Information Co., Ltd. June, 2015 TABLE OF CONTENTS 1.0 INTRODUCTION .............................................................................................. 3 2.0 INDEX MANAGEMENT .................................................................................... 6 3.0 INDEX CONSTRUCTION ................................................................................... 8 4.0 PERIODIC REVIEW OF CONSTITUENTS ............................................................ 10 5.0 CHANGES TO CONSTITUENT COMPANIES....................................................... 12 6.0 INDEX ALGORITHM AND CALCULATION METHOD .......................................... 15 A. INDEX OPENING AND CLOSING HOURS .......................................................... 17 B. FURTHER INFORMATION ............................................................................... 18 SECTION 1 1.0 INTRODUCTION 1.1 This paper sets out the Ground Rules for the management of the SZSE Scale Indices. The SZSE Scale Indices are developed by Shenzhen Securities Information Co., Ltd (‘SSI’). Copies of the Ground Rules are available from SSI on the website of CNINDEX (www.cnindex.com.cn/en/). 1.2 Index Family SZSE Scale Indices are designed to reflect the Shenzhen equity market. SZSE 1000 Index SZSE300 Index SZSE 700 Index SZSE100 Index SZSE200 Index The SZSE 100 Index focuses on the large-cap sector of the market and consists of the top 100 A-share listed -

1/1(W) W 2011/9/6

w 页码,1/1(W) SZSE 1000 Index and Other Indices issued and SZSE Scale Index System Established 2011-9-1 Shenzhen Stock Exchange and Shenzhen Securities Information Co., Ltd. declared recently to issue SZSE 200 index, SZSE 700 index, SZSE 1000 index, SZSE 700 style index and SZSE 1000 style index on September 1. The SZSE 200 index, SZSE 700 index and SZSE 1000 index, jointly with the SZSE 100 index and the SZSE 300 index, constitute the SZSE scale index system; and the SZSE 700 style index and SZSE 1000 style index, together with the SZSE 300 style index, constitute the SZSE style index system. According to the compilation scheme, the SZSE 100 is specified as large-cap index, SZSE 200 as mid-cap index, SZSE 700 as small-cap index, SZSE 300 as large- and mid-cap index, and SZSE 1000 as large-, mid- and small-cap index. The constituent selection method of the SZSE 1000 index is as follows: the float market capitalization and the turnover are weighted by 2:1 and ranked in descending order, and the top 1000 Shenzhen A-share stocks are selected as the constituents. Excluding the SZSE 300 sample stocks, the remaining 700 stocks in the SZSE 1000 sample stocks are selected to constitute the SZSE 700 index. Excluding the SZSE 100 sample stocks, the 200 stocks in the SZSE 300 sample stocks are selected as the constituents of SZSE 200 index. As the latest data indicates, the float market capitalization coverage rate of the SZSE 100 index, the SZSE 200 index and the SZSE 700 index on the A-share stock market is 45.5%, 22.5% and 28.4% respectively, reflecting that the market capitalization of Shenzhen market is in low and unchanged trend, with the majority stocks being the mid- and small-cap stocks. -

World Equity Indices

World Equity Indices Period: Thu Jun 30 2016 - Thu Jul 21 2016 Base Currency: EUR Last Trade Information Historical Return Index Value Net Chg % Chg Time Local Curr Adj North/Latin America DOW JONES INDUS. AVG 18517.23 -77.80 -.42 7/21 +3.28 +4.02 S&P 500 INDEX 2165.17 -7.85 -.36 7/21 +3.16 +3.91 NASDAQ COMPOSITE INDEX 5073.90 -16.03 -.31 7/21 +4.77 +5.54 S&P/TSX COMPOSITE INDEX 14565.83 +32.26 +.22 7/21 +3.56 +3.01 MEXICO IPC INDEX 47364.81 -140.44 -.30 7/21 +3.04 +2.13 BRAZIL IBOVESPA INDEX 56641.49 +63.44 +.11 7/21 +9.93 +8.73 Europe/Africa/Middle East Euro Stoxx 50 Pr 2976.36 +7.87 +.27 13:42 +3.62 +3.62 FTSE 100 INDEX 6726.95 +27.06 +.40 13:42 +3.01 +3.15 CAC 40 INDEX 4386.59 +10.34 +.24 13:42 +3.27 +3.27 DAX INDEX 10165.12 +8.91 +.09 13:42 +4.92 +4.92 IBEX 35 INDEX 8599.90 +16.30 +.19 13:42 +5.15 +5.15 FTSE MIB INDEX 16847.90 +42.50 +.25 13:42 +3.75 +3.75 AEX-Index 452.81 +.84 +.19 13:42 +3.69 +3.69 OMX STOCKHOLM 30 INDEX 1377.98 -3.72 -.27 13:57 +4.39 +3.50 SWISS MARKET INDEX 8196.28 +13.83 +.17 13:42 +2.02 +1.75 Asia/Pacific NIKKEI 225 16627.25 -182.97 -1.09 08:15 +7.92 +6.02 HANG SENG INDEX 21964.27 -36.22 -.16 10:01 +5.80 +6.61 S&P/ASX 200 INDEX 5498.19 -14.21 -.26 09:15 +5.33 +6.72 United States DOW JONES INDUS. -

How Does Foreign Sentiment Affect the Chinese Stock Markets? ‒ Some Empirical Evidence *

1 Volume 20, Number 3 – September 2018 China Accounting and Finance Review 中国会计与财务研究 2018 年 9 月 第 20 卷 第 3 期 How Does Foreign Sentiment Affect the Chinese * Stock Markets? ‒ Some Empirical Evidence Xiao Li, Dehua Shen, and Wei Zhang 1 Received 8th of January 2018 Accepted 13th of April 2018 © The Author(s) 2018. This article is published with open access by The Hong Kong Polytechnic University. Abstract In this paper, making use of a uniquely mismatched sample of investor sentiment extracted from Twitter and the Chinese stock markets (Twitter is not available in mainland China), we show that foreign sentiment has a material impact on the Chinese stock markets at both the market and industry levels. In particular, we find that (1) for the contemporaneous relationship, foreign sentiment can only influence returns on market and industry indexes when investors are in their extreme states of mind, and (2) significant sentiment contagion exists during the tranquil period, while no sentiment contagion exists during the turbulent period. Using the unique Shanghai-Hong Kong Stock Connect programme, we further prove that market purchase can propagate foreign sentiment contagion in the Chinese stock market. The results of this paper have practical implications for investors who are interested in investing in Chinese stock markets. Keywords: Sentiment Contagion, Twitter Happiness Sentiment, Social Media, Shanghai-Hong Kong Stock Connect, Market Purchase * This work is supported by the National Natural Science Foundation of China (71701150 and 71790594), the Young Elite Scientists Sponsorship Program of Tianjin (TJSQNTJ-2017-09) and Fundamental Research Funds for the Central Universities (63182064). -

Traders' Guide 2016

Traders’ Guide 2016 Kepler Cheuvreux is the leading independent European financial services company specialising in advisory services and intermediation for the investment management industry. We have four business lines: Equities, Debt & Credit, Investment Solutions, and Corporate Finance. Headquartered in Paris, the company employees over 550 professionals and has offices in Amsterdam, Boston, Frankfurt, Geneva, London, Madrid, Milan, New York, San Francisco, Stockholm, Vienna, and Zurich. We are a unique multi-local European broker. Kepler Cheuvreux has the most extensive research coverage in Europe and the largest distribution platform with a team of over 100 involved in sales, trading and execution. In terms of market share, we are a Top 10 broker in European equities, combined with global execution capability. Our main purpose is to provide our clients with “unconflicted” execution. As an agency broker, we offer execution in Equities, Equity/debt Derivatives, ETFs and Fixed Income. We cover the US, European and Asian markets. Our client base is made up of asset managers, hedge funds, investment banks, insurance companies, family offices, sovereign wealth funds, retail clients, ECM partners and corporates. It is important to note that the foundation of the business is our Research Products, leveraged across all four business lines. We cover 650 stocks in Europe, and this breadth is complimented by our Asian research distribution, agreement with CIMB, which covers 750 Asian stocks. Our sector and country traders are in constant contact with our analysts to ensure all breaking and corporate news as well as rating changes are taken into account. Our firm has one of the highest cash block crossing rates in the industry: 13% in Large Caps, 22% in Mid Caps and 27% in Small Caps year-to-July 2017. -

Statistics Definitions and Examples

Statistics definitions and examples Last update: September 2013 The Federation’s member exchanges have reached a general agreement on the following statistical notions, and they strictly comply with the definitions below. These definitions and examples are intended to help readers to understand the statistics and how they are compiled. Note on exchange groupings: BME (Spanish Exchanges) is the holding company of Barcelona, Bilbao, Madrid and Valencia exchanges. Statistics of NASDAQ are presented in two different groups: NASDAQ US operating in the USA NASDAQ OMX Nordic Exchange which includes Copenhagen, Helsinki, Iceland, Stockholm, Tallinn, Riga and Vilnius stock exchanges. Statistics of Intercontinental Exchange are presented in four different groups: NYSE and NYSE Derivatives ICE Futures US ICE Futures Canada ICE Futures Europe Statistics of Euronext include Amsterdam, Brussels, Lisbon and Paris Statistics of BATS Global Markets are presented in two different groups: BATS (US) BATS Chi-X 1. EQUITY All data contained in the following equity market tables include the Main/Official market and the Alternative /SMEs markets supervised and regulated by the Exchange. Equity 1.1 - Domestic market capitalization Definition The domestic market capitalization of a stock exchange is the total number of issued shares of domestic companies (as defined in the number of listed companies definition), including their several classes, multiplied by their respective prices at a given time. This figure reflects the comprehensive value of the market