MSCI EAFE Index (USD) (NET)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Does International Diversification Pay?

Does International Diversification Pay? Vivek Bhargava1, Daniel K. Konku2, and D. K. Malhotra3 Advances in computer and telecommunications technology have contributed to the emergence of more integrated global financial markets, allowing for the dissemination of information and the execution of transactions on a real-time basis around the clock and around the globe. To determine if an investor can gain additional diversification benefits by investing in today’s increasingly integrated global financial markets, returns on four different indexes—Standard & Poor’s Composite 500 (S&P 500); Morgan Stanley Capital International (MSCI) World Index; Europe, Australia, and Far East (EAFE) Index; and the MSCI Europe Index—are analyzed for a 22-year period, from 1978 to 2000. Although the benefits from international diversification are decreasing, an investor is better off investing a portion of his or her portfolio in international markets, especially the European markets. Keywords: Diversification, Mutual fund selection, Risk reduction Introduction The objective of this paper is to determine whether an Globalization of financial markets is one of the most investor today can still gain diversification benefits significant economic developments over the last by investing in international markets. The monthly decade. Advances in computer and returns of four different indexes--Standard & Poor’s telecommunications technology contributed to the 500 (S&P 500); Morgan Stanley Capital International emergence of global financial markets, permitting the (MSCI) World Index; the Europe, Australia and Far dissemination of information and execution of East (EAFE) Index; and the MSCI Europe Index— transactions on a real-time basis around the clock and are analyzed over a 22-year period, from 1978 to around the globe. -

MSCI EAFE All Cap Index (USD)

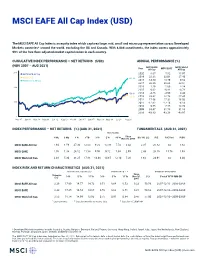

MSCI EAFE All Cap Index (USD) The MSCI EAFE All Cap Index is an equity index which captures large, mid, small and micro cap representation across Developed Markets countries* around the world, excluding the US and Canada. With 8,088 constituents, the index covers approximately 99% of the free float-adjusted market capitalization in each country. CUMULATIVE INDEX PERFORMANCE — NET RETURNS (USD) ANNUAL PERFORMANCE (%) (NOV 2007 – AUG 2021) MSCI EAFE MSCI World Year All Cap MSCI EAFE All Cap 300 MSCI EAFE All Cap 2020 8.67 7.82 15.97 2019 22.38 22.01 27.40 MSCI EAFE 262.28 MSCI World All Cap 2018 -14.50 -13.79 -9.52 2017 26.35 25.03 22.51 200 2016 1.29 1.00 8.24 2015 0.62 -0.81 -0.78 158.80 2014 -4.86 -4.90 4.44 149.91 2013 23.62 22.78 27.45 2012 17.56 17.32 16.03 100 2011 -12.62 -12.14 -6.13 2010 9.55 7.75 13.74 2009 33.47 31.78 31.83 2008 -43.83 -43.38 -40.97 0 Nov 07 Jan 09 Mar 10 May 11 Jun 12 Aug 13 Oct 14 Dec 15 Jan 17 Mar 18 May 19 Jul 20 Aug 21 INDEX PERFORMANCE — NET RETURNS (%) (AUG 31, 2021) FUNDAMENTALS (AUG 31, 2021) ANNUALIZED Since 1 Mo 3 Mo 1 Yr YTD 3 Yr 5 Yr 10 Yr Nov 30, 2007 Div Yld (%) P/E P/E Fwd P/BV MSCI EAFE All Cap 1.94 1.59 27.30 12.03 9.20 10.09 7.74 3.42 2.35 20.82 na 1.82 MSCI EAFE 1.76 1.38 26.12 11.58 9.00 9.72 7.34 2.99 2.43 20.10 15.76 1.93 MSCI World All Cap 2.48 5.30 31.25 17.81 14.48 14.65 12.10 7.26 1.64 24.91 na 3.04 INDEX RISK AND RETURN CHARACTERISTICS (AUG 31, 2021) ANNUALIZED STD DEV (%) 2 SHARPE RATIO 2 , 3 MAXIMUM DRAWDOWN Turnover Since 1 3 Yr 5 Yr 10 Yr 3 Yr 5 Yr 10 Yr Nov 30, (%) Period YYYY-MM-DD -

Client Demand for Sustainable Investing Is Growing

Client demand for sustainable investing is growing Assets in US sustainable funds reached $231 billion by the end of 2020, up from $139 billion at the end of 2019 — a roughly 66% increase.1 In fact, 85% of all individual investors, including 95% of millennials, have expressed an interest in sustainable investing.2 When your clients and prospects ask you about sustainable investing, will you be prepared to have the conversation? INVESTING IN A MORE SUSTAINABLE ECONOMY We believe that capital markets will be shaped We seek to invest in companies that are profoundly by global sustainability challenges well-positioned to benefit from this transition including climate change, environmental to a more sustainable global economy, which pollution, natural resource constraints and is why we integrate environmental, social human capital issues such as diversity, inclusion ESG and governance (ESG) factors across all and gender equity. We expect these trends will drive growth our strategies. In-depth ESG analysis helps for well-positioned companies and create risks for those unable us understand a company’s quality and character, which we or unwilling to adapt. believe enhances our investment decisions. INTEGRATING ESG CRITERIA INTO FINANCIAL ANALYSIS CAN HELP ENHANCE RETURNS US INTERNATIONAL DEVELOPED EMERGING MARKETS 15.00 8.00 12.00 7.02 7.00 9.52 6.29 10.00 12.00 11.37 10.85 6.00 8.00 7.07 9.00 5.00 4.00 6.00 6.00 3.00 4.00 2.00 Annualized Return (%) Return Annualized 3.00 (%) Return Annualized (%) Return Annualized 2.00 1.00 0.00 0.00 0.00 (Annualized return: 5/1/90 to 6/30/21) (Annualized return: 10/1/07 to 6/30/21) (Annualized return: 6/6/13 to 6/30/21) MSCI KLD 400 Social Index MSCI EAFE ESG Leaders Index MSCI Emerging Markets ESG Leaders Index S&P 500 Index MSCI EAFE Index MSCI Emerging Markets Index Data as of 6/30/2021 Investing involves risk, including the loss of principal. -

Quarterly Market Review

Quarterly Market Review [Third Quarter 2018] www.rathbonewarwick.com Quarterly Market Review [Third Quarter 2018] This report features world capital market performance Overview: and a timeline of events for the past quarter. It begins with a global overview, then features the returns of stock and Market Summary bond asset classes in the US and international markets. World Stock Market Performance The report also illustrates the impact of globally diversified portfolios and features a quarterly topic. World Asset Classes US Stocks International Developed Stocks Emerging Markets Stocks Select Country Performance Select Currency Performance vs. US Dollar Real Estate Investment Trusts (REITs) Commodities Fixed Income Impact of Diversification Rathbone Warwick Investment Management (“RWIM”) is a Registered Investment Adviser. This document is solely for informational purposes. Advisory services are only offered to clients or prospective clients where RWIM and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by RWIM unless a client service agreement is in place. www.rathbonewarwick.com Market Summary [Index Returns] Global International Emerging Global Bond US Stock Developed Markets Real US Bond Market Market Stocks Stocks Estate Market ex US Q3 2018 STOCKS BONDS 7.12% 1.31% -1.09% -0.03% 0.02% -0.17% Since Jan. 2001 Avg. Quarterly Return 2.0% 1.5% 2.9% 2.6% 1.1% 1.1% Best 16.8% 25.9% 34.7% 32.3% 4.6% 4.6% Quarter 2009 Q2 2009 Q2 2009 Q2 2009 Q3 2001 Q3 2008 Q4 Worst -22.8% -21.2% -27.6% -36.1% -3.0% -2.7% Quarter 2008 Q4 2008 Q4 2008 Q4 2008 Q4 2016 Q4 2015 Q2 Past performance is not a guarantee of future results. -

The Case for a Global Perspective

Schwab Center for Financial Research The case for a global perspective Jeffrey Kleintop, CFA Chief Global Investment Strategist What the Masters can teach us about investing Global stocks have tended to provide returns similar to those of U.S. stocks over long-term periods in the Markets have become more globally diversified of late, forcing investors to adopt a past. Valuations point to similar 5—10% annualized broader, worldwide perspective. This is a theme relevant even in championship golf, total returns across the world’s major regions in the where the national diversity of players in the 2015 Masters tournament bears an uncanny future (page 10). resemblance to stocks in the MSCI All Country World Index. Just as top players can be found on the world’s golf courses, savvy investors can be found on the world’s stock exchanges. But the lessons don’t stop there. 5–10% Geographic distribution of players at the Masters Annualized and stocks in the MSCI All Country World Index total returns Masters players MSCI AC World Index 50% U.S. 51% 16% Europe* 16% Avoiding the traps During the worst 10-year period for 13% Emerging Markets 14% stocks over the past 45 years, U.S. stocks fell an annualized 4.2%, 1.0% 12% U.K. 7% while global stocks lost 2.5% and International international stocks measured by 7% Asia Pacific 9% the MSCI EAFE Index lost only 2.5% 1.0% (page 6). Global 2% Canada 3% 4.2% * Excluding the U.K. Source: Charles Schwab, MSCI data as of April 10, 2015. -

The New Neutral: the Long-Term Case for Currency Hedging

Robert Bush Thought Leadership Xpert Insights 12/17 The New Neutral—The long-term case for currency hedging It’s fair to say that currency-hedged approaches to The Long Term Case for Currency Hedging) and international investing have really come to the fore consider the more strategic reasons for hedging, and, over the last few years, with $14.8 billion of AUM in in particular, the potential risk reduction it offers. hedged ETFs at the beginning of 2014, compared with “$41bn of AUM as of the end of November Take a look at Figure 1, which reflects the difference 2017” (Source: Morningstar). Without asking every in volatility for the MSCI EAFE, a key benchmark single investor’s motivation, it’s impossible to say for international developed equity markets, on a exactly what the driving force behind this interest hedged (without currency) and an un-hedged (with has been, but we suspect the strong performance currency) basis. A positive number represents more of the dollar, particularly against the euro and the risk in the basket that includes currency. What was yen, where quantitative easing has weakened those surprising, to us at least, was that over this time currencies, has really shone a spotlight on the role period leaving currency in resulted in volatility on currencies can play in an international investment. average 2.7 percentage points higher 90% of the time. It really begs the question—why? What is it Instead of focusing on the tactical, return-oriented about currency—and, by the way, it’s not, in our aspects of the hedging decision, let’s focus on some view, additional return—that meant investors lost key findings from research we’ve recently undertaken out by retaining their exposure? (see our latest White Paper The New Neutral: Figure 1: The difference in volatility between MSCI EAFE hedged and un-hedged (2/1978–2/2017) 8.00 6.00 4.00 2.00 0.00 –2.00 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2017 Source: Morningstar Direct, 3/31/1973–11/30/17. -

Notice of Filing of Proposed Rule Change to List and Trade Options on the MSCI EAFE Index and on the MSCI Emerging Markets Index

SECURITIES AND EXCHANGE COMMISSION (Release No. 34-74430; File No. SR-CBOE-2015-023) March 4, 2015 Self-Regulatory Organizations; Chicago Board Options Exchange, Incorporated; Notice of Filing of Proposed Rule Change to List and Trade Options on the MSCI EAFE Index and on the MSCI Emerging Markets Index Pursuant to Section 19(b)(1) of the Securities Exchange Act of 1934 (the “Act” or “Exchange Act”),1 and Rule 19b-4 thereunder,2 notice is hereby given that on February 26, 2015, the Chicago Board Options Exchange, Incorporated (the “Exchange” or “CBOE”) filed with the Securities and Exchange Commission (the “Commission”) the proposed rule change as described in Items I, II, and III below, which Items have been prepared by the Exchange. The Commission is publishing this notice to solicit comments on the proposed rule change from interested persons. I. Self-Regulatory Organization’s Statement of the Terms of Substance of the Proposed Rule Change CBOE proposes to list and trade options that overlie the MSCI EAFE Index and the MSCI Emerging Markets Index (“EAFE options” and “EM options”). EAFE and EM options would be P.M., cash-settled contracts with European-style exercise. The text of the proposed rule change is available on the Exchange’s Web site (http://www.cboe.com/AboutCBOE/CBOELegal RegulatoryHome.aspx), at the Exchange’s Office of the Secretary, and at the Commission. II. Self-Regulatory Organization’s Statement of the Purpose of, and Statutory Basis for, the Proposed Rule Change In its filing with the Commission, the self-regulatory organization included statements concerning the purpose of and basis for the proposed rule change and discussed any comments it 1 15 U.S.C. -

MSCI ACWI Ex Ireland Index (USD)

MSCI ACWI ex Ireland Index (USD) The MSCI ACWI ex Ireland Index captures large and mid cap representation across 22 of 23 Developed Markets (DM) countries (excluding Ireland) and 27 Emerging Markets (EM) countries*. With 2,959 constituents, the index covers approximately 85% of the global equity opportunity set outside Ireland. CUMULATIVE INDEX PERFORMANCE — GROSS RETURNS (USD) ANNUAL PERFORMANCE (%) (AUG 2006 – AUG 2021) MSCI ACWI Year ex Ireland MSCI World MSCI ACWI MSCI ACWI ex Ireland 2020 16.83 16.50 16.82 MSCI World 338.06 2019 27.28 28.40 27.30 MSCI ACWI 325.46 2018 -8.90 -8.20 -8.93 300 324.55 2017 24.63 23.07 24.62 2016 8.51 8.15 8.48 2015 -1.86 -0.32 -1.84 2014 4.71 5.50 4.71 200 2013 23.42 27.37 23.44 2012 16.81 16.54 16.80 2011 -6.88 -5.02 -6.86 2010 13.25 12.34 13.21 100 2009 35.44 30.79 35.41 2008 -41.76 -40.33 -41.85 50 2007 12.31 9.57 12.18 Aug 06 Nov 07 Feb 09 May 10 Aug 11 Nov 12 Feb 14 May 15 Aug 16 Nov 17 Feb 19 May 20 Aug 21 INDEX PERFORMANCE — GROSS RETURNS (%) (AUG 31, 2021) FUNDAMENTALS (AUG 31, 2021) ANNUALIZED Since 1 Mo 3 Mo 1 Yr YTD 3 Yr 5 Yr 10 Yr Dec 31, 1998 Div Yld (%) P/E P/E Fwd P/BV MSCI ACWI ex Ireland 2.53 4.66 29.18 16.24 14.91 14.88 11.86 6.98 1.71 22.52 18.45 3.07 MSCI World 2.52 5.97 30.33 18.29 15.56 15.44 12.76 6.98 1.66 23.87 19.54 3.31 MSCI ACWI 2.53 4.67 29.18 16.24 14.91 14.88 11.86 6.97 1.71 22.54 18.46 3.07 INDEX RISK AND RETURN CHARACTERISTICS (AUG 31, 2021) ANNUALIZED STD DEV (%) 2 SHARPE RATIO 2 , 3 MAXIMUM DRAWDOWN Turnover Since 1 3 Yr 5 Yr 10 Yr 3 Yr 5 Yr 10 Yr Dec 31, (%) Period YYYY-MM-DD -

Product Commentary CLEARBRIDGE INTERNATIONAL GROWTH FUND

2Q 2021 Product Commentary CLEARBRIDGE INTERNATIONAL GROWTH FUND Elisa Mazen, Michael Testorf, CFA, Pawel Wroblewski, CFA and Thor Olsson Portfolio Managers Average annual total returns and fund expenses (%) Key takeaways as of June 30, 2021 • Recent Fund outperformance has been broad- based, led by more defensive, secular growth Since Incept. Expenses companies, with structural and emerging growth Class A 3-mo 1-yr 5-yr 10-yr (02/03/09) Gross Net holdings also contributing. Excluding sales 6.77 29.06 16.17 11.55 14.43 1.10 1.06 charges • Banks and energy are two areas we have mostly Including effects avoided, but our valuation approach to growth of maximum 0.62 21.64 14.80 10.89 13.88 1.10 1.06 helped identify two European banks and a global sales charges oil services provider in the quarter whose MSCI EAFE (Net) 5.17 32.35 10.28 5.89 N/A - - risk/reward were too attractive to overlook. (USD) Performance shown represents past performance and is no guarantee of future • International equity markets have seen rotating results. Current performance may be higher or lower than the performance shown. leadership due to various factors, such as the Investment return and principal value will fluctuate so shares, when redeemed, may be likelihood of interest rate increases and differing worth more or less than the original cost. Class A shares have a maximum front-end sales charge of 5.75%. Total returns assume the reinvestment of all distributions at net asset monetary policies, moves creating short-term value and the deduction of all Fund expenses. -

MSCI EAFE ESG Screened Index (USD)

MSCI EAFE ESG Screened Index (USD) The MSCI EAFE ESG Screened Index is based on the MSCI EAFE Index, its parent index, and includes large and mid-cap securities across 21 Developed Markets (DM)* countries excluding the U.S and Canada. The index excludes companies from the parent index that are associated with controversial, civilian and nuclear weapons and tobacco, that derive revenues from thermal coal and oil sands extraction and that are not compliant with the United Nations Global Compact principles. CUMULATIVE INDEX PERFORMANCE — NET RETURNS (USD) ANNUAL PERFORMANCE (%) (MAY 2012 – AUG 2021) MSCI EAFE Year ESG Screened MSCI EAFE MSCI EAFE ESG Screened 2020 9.27 7.82 MSCI EAFE 2019 22.43 22.01 231.82 2018 -14.27 -13.79 225.67 2017 25.13 25.03 200 2016 0.09 1.00 2015 -0.04 -0.81 2014 -4.61 -4.90 2013 23.88 22.78 100 50 May 12 Mar 13 Dec 13 Sep 14 Jun 15 Apr 16 Jan 17 Oct 17 Jul 18 May 19 Feb 20 Nov 20 Aug 21 INDEX PERFORMANCE — NET RETURNS (%) (AUG 31, 2021) FUNDAMENTALS (AUG 31, 2021) ANNUALIZED Since 1 Mo 3 Mo 1 Yr YTD 3 Yr 5 Yr 10 Yr May 31, 2012 Div Yld (%) P/E P/E Fwd P/BV MSCI EAFE ESG Screened 2.06 1.57 25.94 11.49 9.44 9.86 na 9.51 2.30 20.23 16.30 1.95 MSCI EAFE 1.76 1.38 26.12 11.58 9.00 9.72 na 9.19 2.43 20.10 15.76 1.93 INDEX RISK AND RETURN CHARACTERISTICS (MAY 31, 2012 – AUG 31, 2021) ANNUALIZED STD DEV (%) 2 SHARPE RATIO 2 , 3 MAXIMUM DRAWDOWN TrackingTurnover Since Beta 1 3 Yr 5 Yr 10 Yr 3 Yr 5 Yr 10 Yr May 31, (%) Period YYYY-MM-DD Error (%) (%) 2012 MSCI EAFE ESG Screened 0.99 0.66 4.50 17.51 14.42 na 0.53 0.64 na 0.68 33.72 2018-01-25—2020-03-23 MSCI EAFE 1.00 0.00 2.32 17.65 14.54 na 0.50 0.62 na 0.66 34.12 2018-01-25—2020-03-23 1 Last 12 months 2 Based on monthly net returns data 3 Based on ICE LIBOR 1M *DM countries include: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the UK. -

MSCI EAFE Index.Indd

���������������� The MSCI EAFE Index® is recognized as the pre-eminent benchmark in the United States to measure international equity performance. It comprises 21 MSCI country indices, representing the devel- oped markes outside of North America: Europe, Australasia and the Far East. Since inception in, the MSCI EAFE Index has had an average gross annual return of 11.2%. MSCI aims to include in its international indices 85% of the free fl oat-adjusted market capitaliza- tion in each industry group, within each country. As of Dec 30, 2005 the MSCI EAFE Index contained 1,137 securities with a total market capitalization of over USD 10.2 trillion. The MSCI EAFE Index is published daily by MSCI and through multiple vendors and in real time every 60 seconds through Reuters and Bloomberg. ����������������������������������������� COUNTRY NO OF SECURITIES WEIGHT COUNTRY NO OF SECURITIES WEIGHT Japan 369 25.6% Finland 21 1.4% United Kingdom 155 24.0% Belgium 20 1.1% France 62 9.3% Singapore 41 0.8% Switzerland 38 6.9% Denmark 19 0.8% Germany 50 6.8% Ireland 17 0.8% Australia 83 5.2% Norway 18 0.7% Italy 39 3.8% Greece 21 0.6% Spain 33 3.7% Austria 13 0.4% Netherlands 26 3.4% Portugal 11 0.3% Sweden 47 2.4% New Zealand 13 0.2% Hong Kong 41 1.6% EAFE Total 1137 100.0% ��������������� ������������������������������������������������������������������� ������ ����� ��� ��������������������������� �� ����� ����� ����� ����� ����� ����� ����� ����� ����� ����� ����� ����� ����� ����� ����� ����� ����� ����� ����� Gross Index Level CONTACT US Amsterdam + 31.20.462.1382 Atlanta + 1.404.949.4529 ���������������������������������������� ������������������������������������������ Boston + 1.617.856.8716 SECTOR NO OF SECURITIES WEIGHT INDEX CAPITALIZATION AND CONCENTRATION 226 Cape Town Financials 28.5% Total Market Capitalization (USD, MM) 10,218,281 + 27.21.683.3245 209 Consumer Discretionary 12.3% Number of Securities 1,137 China Netcom 233 Industrials 10.7% Dollar Wt. -

Foreign Equityequity

ForeignForeign EquityEquity • All ETFs providers are placed in alphabetical order. • Click logo to buy ETF through EasyEquities website. • Risk profile included. • Research from Intellidex is included for most ETFs available on the EasyEquities site. • Provider logos click through to ETFs information on provider’s home page. • Providers Fact sheets are included. • The Total Expense Ratios (TERs) for each ETF is shown (as at March 2018). - Total Expense Ratios (TERs) Measure the costs of operating the ETF portfolios, including the management fees and costs of the issuing company. The TER is included in price of the ETF product and is not paid directly by the investor. The Ashburton Global 1200 ETF provides investors with efficient exposure RISK to the global equity market by tracking the S&P Global 1200. Ashburton Global 1200 ETF houses various global indices under one fund. Ashburton ETF Global 1200 ETF combines seven indices: the S&P 500 (US); S&P Europe Aggressive Global 1200 350; S&P TOPIX 150 (Japan); S&P/TSX 60 (Canada); S&P/ASX All Australian 50; S&P Asia 50; and S&P Latin America 40 FACT SHEET TER: 0,45% The Cloud Atlas Big50 ex-SA ETF is an investment product that invests in RISK the 50 most representative companies across the African continent. The 50 companies in this ETF track the Cloud Atlas AMI Big50 ex-SA index (beta+), which is an enhanced index designed to maximize sector and Moderate ETF country exposure Big 50 FACT SHEET TER: 0,75% The CoreShares S&P 500 ETF tracks the S&P 500® Index.