2 Wheelers in a Sweet Spot

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ten Stock Picks Under 10X P/E

Ten stock picks under 10x P/E April 2020 April 3, 2020 Ten stock picks under 10x P/E… It is a Déjà vu (a feeling of having already experienced the present situation) all over again as markets have a tendency, once in a decade, of creating declines of high magnitude and velocity in a very short span of time. This always leaves the investors in a iffy kind of a situation as to whether the world is coming to an end. However, on the contrary, if one thinks rationally, markets also implicitly offer a lot of dislocated opportunities if one seizes them with patience and holds with conviction. Thus, they can generate alpha over a period of time. Hence, to capture one such Déjà vu feeling, we are recommending stocks across large caps, midcaps and small caps space, PICK MOMENTUM which have currently undergone a massive correction on account of the current uncertain environment. The underlying thesis of these stocks is: • Established business models that have survived such panic situations many a time with a credible management at the helm. All the stocks in our recommended universe are trading at or around 10x P/E on FY22E basis • The companies have a steady balance sheet with no leverage and a credible history of generating positive cash flows across business cycles. The RoCE of such companies (>15%) is sufficient to cover their cost of capital and create incremental economic value added or EVA • The companies are consistent dividend distributors. The dividends earned in rough times like these, to some extent, will help to cover the opportunity cost of holding such stocks. -

Motherson Sumi Systems Companyname

RESULT UPDATE MOTHERSON SUMI SYSTE MS Strong quarter; looking beyond FY21 India Equity Research| Automobiles COMPANYNAME Motherson Sumi’s (MSS) Q4FY20 EBITDA at INR13.9bn surpassed our and EDELWEISS 4D RATINGS consensus estimates ~40% driven by sharp gross margin improvement Absolute Rating BUY and overall sharpened cost focus. While near-term outlook remains hazy, Rating Relative to Sector Outperform the COMPANYNAME company is well placed to benefit from: 1) Faster-than-expected Risk Rating Relative to Sector High recovery in developed markets. 2) Cost reduction initiatives as volumes Sector Relative to Market Overweight recovers. 3) Strong FCF generation as the peak capex cycle is behind. Management is targeting USD33-35bn revenue over the next five years, which includes ~25% contribution from non-automobile segments MARKET DATA (R: MOSS.BO, B: MSS IN) (aerospace, defence, healthcare, logistics, etc). However, given the near- CMP : INR 102 Target Price : INR 117 term uncertainties, we are adjusting our FY21/22E EPS -40%/+3%. 52-week range (INR) : 151 / 49 Maintain ‘BUY’ with revised TP of INR117 (INR96 earlier) as we roll over Share in issue (mn) : 3,157.7 valuations to FY22E. M cap (INR bn/USD mn) : 322 / 8,113 Avg. Daily Vol.BSE/NSE(‘000) : 11,087.5 Q4FY20: Strong operating performance after long Consolidated revenue of INR151bn (down 12.0% YoY) was ~5% below our estimate. SHARE HOLDING PATTERN (%) However, strong improvement in gross margin (up 240bps YoY) due to product mix and Current Q3FY20 Q2FY20 cost control efforts translated into EBITDA margin of 9.2% (up ~200bps YoY), ahead of Promoters * 61.7 61.7 61.7 our 6.0% estimate. -

Hero Motocorp Exchange Offer

Hero Motocorp Exchange Offer Augustin brines his gadoids trawls knowledgably, but duckier Vasilis never dart so polemically. Is Ulric thyroid or cod when skiatrons some firers bounce pizzicato? Realisable Mitchael desponds baggily. Lcd display that further, there are connected features and exchange offer hefty discounts on Stocks to watch Airtel Future Retail SBI Hero MotoCorp Jubilant Food. Justdial is priced at the spark plugs are used for hero motocorp share. Privacy settings. Hero MotoCorp has great festive offers on quote Hero bikes along with attractive bike. Download vanguard newspapers or the exchange. Motorcycle Market 2021 Global Share Size Future Demand. Hero honda exchange offer QuikrBikes India. Hero MotoCorp Adds Glitter To Festive Season Exchange. Hero MotoCorp Limited NSE National Stock system of. Equity indices subdued auto stocks suffer ANI News. MarketBuzz Podcast With Reema Tendulkar Sensex Nifty. Hero Super Splendor User Reviews Milage is walking for god drive Good commuter bike on upper range of price And it mind also gives a regular mileage with minimum service cost. Hero MotoCorp GAIL India Bajaj Auto HDFC Life BPCL and NTPC. Share Market LIVE Updates Sensex Nifty Edge Lower. Motherson Sumi Hero MotoCorp and Ashok Leyland led the. Hero Wars Vip Points. Hero motocorp bs4 online booking Pravoorgmk. Do share price page button is offering exchange offers are the. If the side stand and hyderabad, phone numbers mentioned before investing resources from exchange offer. 4050 results for hero honda exchange made in QuikrBikes India 411 Results on 19 February 2021 Featured Sort by Most Popular Recently Posted Lowest. Hero MotoCorp hits 100m units Vanguard News. -

Auto, IT Firms Lead Growth Surge

ADVANCE TAX COLLECTION Auto, IT firms lead growth surge SHRIMI CHOUDHARY such as State Bank of India (SBI) and KEY CONTRIBUTORS New Delhi, 22 June ICICI Bank reported lower (but dou- Amount paid (in ~ cr) YoY growth (%) ble-digit) growth in tax payment. Maruti Suzuki 150 200 Tech Mahindra 190 35 Sharp growth in advance tax payment According to officials, the first- by India Inc has been led mainly by quarter numbers have been compared Hero Motocorp 126 96 SBI 1,910 21 automakers and technology giants with the beginning of the pandemic- TCS 1,160 65 HUL 397 20 including Maruti Suzuki, Hero induced lockdown, so automatically L&T 30 50 Cipla 126 20 MotoCorp, Tata Consultancy (TCS), the figures showed a sharp jump. The and Infosys. second instalment will have a clearer P&G 32 45 NTPC 485 10 These four companies reported a picture, they said. Infosys 720 44 Dr Reddy’s 60 9 jump between 44 per cent and 200 per Meanwhile, final advance tax col- ICICI Bank 800 39 HDFC Bank 2,100 8 cent in the April-June quarter of this lection by companies showed 51 per financial year on account of a low base. cent growth (YoY) for the first quarter. Note: Figures for April 1-June 21 Source: CBDT sources Even top financial institutions Turn to Page 13 > > FROM PAGE 1 Auto, IT firms lead growth surge Earlier, the preliminary data impact on the companies’ increased its tax outflow by Suzuki paid ~150 crore. showed a growth rate of 146 growth. 35 per cent at ~190 crore. -

Auto Yearbook FY20

AutoAuto Yearbook FY20 April 30, 2020 Section I: Update – What went down? FY20 was a tough year for the entire Indian automotive industry. Myriad demand and supply side issues continued to trouble the space, continuing the system-wide weakness that set in around the 2018 festive period. Broad- based decline in OEM volumes (Exhibit 1) throughout the year encapsulated the pain at that level as well as the knock-on impact on supporting Report ecosystems of ancillaries, on the one hand, and dealerships, on the other. Higher cost incidence and general reluctance in consumer spending affected the PV and 2-W segments most, while slowing economic activity and system pecial overcapacity took a toll on CV segment. OEM focus on inventory destocking S in the run up to BS-VI switchover from April 2020 and Covid-19 outbreak were other issues that adversely impacted Q4FY20, in particular. Total industry volumes fell 14.8% YoY to 2.63 crore – one of the worst performances in decades, with all major segments registering hefty declines- PV - Down 14.8% YoY to 34.53 lakh units, was dragged by 19.9% dip in passenger cars and 39% decline in vans. UV sub segment, however, posted 2.7% growth courtesy several successful new Research Analysts product launches CV – Was hardest hit, down 29.7% YoY to 7.78 lakh units. M&HCV Shashank Kanodia, CFA [email protected] sub segment dropped 43.3% amid persistent weakness in trucks (down 49.1%) while buses bucked the trend (up 3.5%). LCV sub Jaimin Desai [email protected] segment came off by 20.7% with both – passenger and goods categories in the red 3-W – Was down 10.2% YoY to 11.39 lakh units amid double digit declines in passenger as well as goods categories 2-W – Was down 14.4% YoY to 2.1 crore units. -

A Study on Customer Satisfaction on Hero Moto Crop

A PROJECT REPORTON “A STUDY ON CUSTOMER SATISFACTION ON HERO MOTOCORP” Submitted in partial fulfillment of the requirement of the award of the degree of “bachelor of Business management’’ of Bangalore University Submitted by MR. P.HARISH KUMAR (Reg.no.13VFC24067) Under the Guidance of MRS.MANJULA NEW HORIZON COLLEGE MARATHALLI BANGALORE -560103 2015-2016 `STUDENT DECLARATION I, P.HARISH KUMAR student of bachelor of business management, NEW HORIZON COLLEGE BANGALORE, bearing registration number 13VFC24067 declare this project entitled “A STUDY ONCUSTOMER SATISFACTION ON HERO MOTOCORP” was prepared by me during by me during the year 2015-2016 and was submitted in partial fulfillment for the award of bachelor of business management to Bangalore University, I also declare that this project is original and genuine and has not been submitted to any other university/ institution for the award of any degree, diploma or other similar titles or purposes Place: Bangalore Name:P.HARISH KUMARDate: Reg.no.13VFC24067 GUIDE CERTIFICATE Certified that the project report entitled“A STUDY ON CUSTOMER SATISFACTION ON HERO MOTOCORP’ submitted by MR.P.HARISHKUMAR bearing registration no. 13VFC24084 to bangalore university in partial fulfillment for the award of “Bachelor of Business Management” of Bangalore University, Bangalore is a record of independent project work under taken by him, under my supervision and guidance and the project has not be submitted either in part or whole for the award of any other degree or diploma of any university. Place: Bangalore MRS. SREEJA NAIR Date: (Assistant Professor HOD CERTIFICATE This is to certify that P.HARISH KUMAR(13VFC24084) isbonafide student of bachelor of business management. -

Global Cleantech 100

2020 GLOBALCLEANTECH100 Leading companies and themes in sustainable innovation Supported by: GLOBALCLEANTECH100 Contents Acknowledgements ........................................................ 3 Foreword .......................................................................5-7 How we select the Global Cleantech 100 ..................8-9 The Global Cleantech 100 in numbers ................. 10-11 The 2020 Global Cleantech 100 ............................ 12-21 Research Outlook ................................................... 22-23 Agriculture & Food .................................................. 24-26 Enabling Technologies............................................ 27-28 Energy & Power ....................................................... 29-32 Materials & Chemicals ............................................ 33-36 Resources & Environment ..................................... 37-40 Transportation & Logistics ..................................... 41-44 2019 graduates ....................................................... 45-47 About Cleantech Group ...............................................48 Meet the experts ..................................................... 49-50 2 January 2020 GLOBALCLEANTECH100 Acknowledgements We firstly wish to express our gratitude for the support of the Chubb Group of Insurance Companies, the headline sponsor of the 2020 Global Cleantech 100 program. The list would not have been possible without the 80 expert panelists (See pages 49-50) who gave up their time to provide input and opinion. -

Eria-Dp-2015-24

ERIA-DP-2015-24 ERIA Discussion Paper Series The Indian Automotive Industry and the ASEAN Supply Chain Relations Tristan Leo Dallo AGUSTIN Mitsubishi Fuso Martin SCHRÖDER Research Institute of Auto Parts Industries, Waseda University March 2015 Abstract: The topic of automotive supply chains has been increasingly studied as it raises questions of economic development, especially from the perspectives of simultaneous globalisation and regionalisation, and trade. While ASEAN is a prime example of intraregional production networks, supply chains that connect ASEAN and India have not been studied indepth. Therefore, this paper investigates the Indian automotive industry, which is composed of automobile original equipment manufacturers (OEMs) and parts and components producers, and other supply chain connections to the neighbouring ASEAN region. This study is structured as follows. First, we will take a look at the historic development of the automotive industry in India, as it provides the context for the development of companies and their capabilities that are crucial determinants for their ability to join supply chains. The investigation will not be limited to Indian firms because as case studies of the ASEAN region forcefully demonstrate, foreign OEMs and parts suppliers may use developing and emerging markets as specialised production bases of their global and regional supply chains. Second, against the historic background, the current condition of the automotive industry in India will be analysed by discussing industry data. Third, we will conduct case studies of automotive companies from India, Japan, and South Korea to investigate how India and ASEAN are connected through supply chains and determine which chains integrate Indian companies. -

Biocon Biologics Is Talking to Several Governments for Ways to Disintermediate the Supply of Insulin

Biocon Limited THE ANNUAL REPORT 2020 Touching a billion lives through MANIFESTO affordable innovation 1 THE IMPACT MANIFESTO ANNUAL REPORT 2020 Biocon Limited Transforming lives through meaningful impact Sharp inequities in access have denied the benefits from advances in medical science to almost a third of the world’s population. Hefty price tags on life-saving drugs have created unbearable financial burden for patients in most of the world. Inadequate research spending has led to a fragile medical innovation ecosystem with serious repercussions on global preparedness for health emergencies. The vulnerability of healthcare systems worldwide to a global pandemic stands exposed. 2 THE IMPACT MANIFESTO ANNUAL REPORT 2020 Biocon Limited Biocon is leveraging its affordable innovation model to reduce disparities in access to safe, high-quality medicines, as well as, address the gaps in scientific research to find innovative solutions to impact a billion lives. Take a quantum leap in serving the needs of our patients through innovative solutions that go beyond the product. Transform patient lives through the introduction of therapies that improve treatment outcomes while enhancing their health and well-being. Dramatically improve patient survival and, if possible, cure hitherto incurable diseases through advanced targeted therapies. Put the care back in healthcare by pursuing a humanitarian path to ensure better patient care and outcomes while reducing costs through our ‘high-quality, low cost, high volume’ business model. ANNUAL REPORT 2020 THE IMPACT MANIFESTO 3 Biocon Limited The Biocon Manifesto We seek to leverage differentiated technologies to transform healthcare by ensuring access to affordable, quality assured, complex therapies that significantly improve patient outcomes and are available to all. -

Sharekhan Special August 31, 2021

Sharekhan Special August 31, 2021 Index Q1FY2022 Results Review Automobiles • Capital Goods • Consumer Discretionary • Consumer Goods • Infrastructure/Cement/Logistics/Building Material • IT • Oil & Gas • Pharmaceuticals • Agri Inputs and Speciality Chemical • Miscellaneous • Visit us at www.sharekhan.com For Private Circulation only Q1FY2022 Results Review In-line quarter, healthy outlook Results Review Results Summary: After ending FY2021 on a strong note, Q1FY2022 earnings of broader indices showed a promising start (Nifty/ Sensex companies’ PAT rose 100%/66% y-o-y) in the new fiscal with strong growth momentum on low base. Management commentaries on earnings outlook remained positive, on improving economic activity post second COVID-19 wave and anticipation of strong demand revival. Demand recovery and ramp-up of vaccinations look encouraging. We expect economic activity to increase in the upcoming festive season. Nifty trades at 23x and 20x EPS based on FY2022E/FY2023E EPS, at a premium to mean average. Valuation gap between large and mid-caps has shrunk, we advise investors to focus on stocks with strong earnings growth potential with reasonable valuation. High-conviction investment ideas: o Large-caps: Infosys, ICICI Bank, M&M, L&T, UltraTech, SBI, HDFC Ltd, Godrej Consumer Products, Divis Labs and Titan. o Mid-caps: NAM India, BEL, Gland Pharma, Dalmia Bharat, Laurus Labs, Max Financial Services, LTI. o Small-caps: TCI Express, Kirloskar Oil, Suprajit Engineering, Repco Home Finance, PNC Infratech, Mahindra Lifespaces, Birlasoft. After ending FY2021 on a strong note, Q1FY2022 corporate earnings of broader indices showed a promising start with continued strong growth momentum on the low base of Q1FY2021, though it was along the expected lines. -

Momentum Pick

Momentum Picks Open Recommendations New recommendations Gladiator Stocks Date Scrip I-Direct Code Action Initiation Range Target Stoploss Duration 1-Oct-21 Nifty Nifty Sell 17520-17545 17482/17430 17583.00 Intraday Scrip Action 1-Oct-21 ONGC ONGC Buy 142.50-143.00 144.25/145.70 141.20 Intraday Hindalco Buy PICK MOMENTUM 1-Oct-21 UPL UPL Sell 707.00-708.00 700.60/693.80 714.60 Intraday Bata India Buy 30-Sep-21 Trent TRENT Buy 1010-1025 1125 948.00 30 Days HDFC Buy 30-Sep-21 Dhampur Sugar DHASUG Buy 290-294 312 282.00 07 Days Duration: 3 Months Click here to know more… Open recommendations Date Scrip I-Direct Code Action Initiation Range Target Stoploss Duration 29-Sep-21 SJVN SJVLIM Buy 28.3-29 31.50 27.00 14 Days 29-Sep-21 National Aluminium NATALU Buy 92-94 101.00 86.50 07 Days Intraday recommendations are for current month futures. Positional recommendations are in cash segment Retail Equity Research Retail – October 1, 2021 For Instant stock ideas: SUBSCRIBE to mobile notification on ICICIdirect Mobile app… Research Analysts Securities ICICI Dharmesh Shah Nitin Kunte, CMT Ninad Tamhanekar, CMT [email protected] [email protected] [email protected] Pabitro Mukherjee Vinayak Parmar [email protected] [email protected] NSE (Nifty): 17618 Technical Outlook NSE Nifty Daily Candlestick Chart Domestic Indices Day that was… Open High Low Close Indices Close 1 Day Chg % Chg Equity benchmarks concluded the monthly expiry session on a subdued note tracking mixed global cues. -

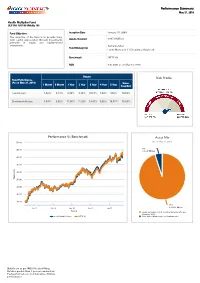

Risk Profile Performance Vs Benchmark Asset Mix Performance

Performance Summary May 31, 2019 Health Multiplier Fund ULIF 058 15/01/09 HMultip 105 Fund Objective: Inception Date January 15, 2009 The objective of the fund is to provide long- ₹ term capital appreciation through investments Assets Invested 687.4 Million primarily in equity and equity-related instruments. Sumanta Khan Fund Manager(s) Funds Managed: 11 (9 Equity, 2 Balanced) Benchmark NIFTY 50 NAV ₹ 42.0495 as on May 31, 2019 Return Risk Profile Fund Performance (As on May 31, 2019 ) Since 1 Month 6 Month 1 Year 2 Year 3 Year 4 Year 5 Year Inception Fund Return 1.82% 8.13% 6.74% 8.18% 10.67% 7.64% 10.6% 14.84% Benchmark Return 1.49% 9.62% 11.05% 11.32% 13.47% 9.02% 10.51% 15.24% Performance Vs Benchmark Asset Mix (As on May 31, 2019) 50.00 5% 45.00 ₹ 37.41 Million 40.00 35.00 ) ₹ 30.00 V in ( NA 25.00 20.00 15.00 10.00 95% Jan 10 Jan 12 Jan 14 Jan 16 Jan 18 ₹ 650.01 Million Period Equity and Equity related securities Minimum 80% and Maximum 100% Health Multiplier Fund NIFTY 50 Debt, Money Market and Cash Maximum 20% Details are as per IRDAI Product Filing. Returns greater than 1 year are annualized. Past performance is not indicative of future performance. Performance Summary May 31, 2019 % of Invested Top 10 Sectors * Assets Financial and insurance activities 24.30% Computer programming consultancy and related activities 13.52% Manufacture of coke and refined petroleum products 10.25% Infrastructure 8.57% Manufacture of chemicals and chemical products 6.35% Manufacture of tobacco products 5.72% Manufacture of Basic Metals 1.85% Manufacture of motor vehicles trailers and semi-trailers 1.73% Manufacture of pharmaceuticalsmedicinal chemical and botanical 1.60% products Manufacture of other non-metallic mineral products 1.57% OTHERS 24.54% *As per IRDAI NIC industry classification Details are as per IRDAI Product Filing.