Safeguarding Markets from Pernicious Pay to Play: a Model Explaining Why the SEC Regulates Money in Politics

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

B4 the MESSENGER, Friday, March 9, 2012 6:30 7:30 8:30 9:30

B4 B4 THE MESSENGER, Friday, March 9, 2012 03/9 6AM 6:30 7AM 7:30 8AM 8:30 9AM 9:30 10AM 10:30 11AM 11:30 WBKO ^ 5:30 AM Kentucky (N) Good Morning America Andrew Garfield; Richard Blais. (N) Å Live! With Kelly (N) Å The View (N) Å WBKO at Midday (N) % Today Kathy Bates; Elizabeth Olsen. (N) Å The 700 Club (N) Å WHAG News at 12:00PM (N) _ _ Paid Program Storm Stories Å Eyewitness News Daybreak (N) Local 7 News Lifestyles Family Feud Å Family Feud Å Animal Adv Å Swift Justice Å Judge Mathis Å 3 ( 5:00 The Daily Buzz Å Better (N) Å Cash Cab Å Cash Cab Å The Cosby Show Å The Cosby Show Å Law & Order: Criminal Intent Å C ) 5:00 QVC This Morning Perricone MD Cosmeceuticals Kitchen Innovations LizClaiborne New York Fashion. Q Check Style Edition . * 14 News Sunrise (N) Å Today Kathy Bates; Elizabeth Olsen. (N) Å Today (N) Å Today (N) Å :15 Midday With Mike (N) Å 9 + 5:00 Eyewitness News Daybreak (N) Å Good Morning America Andrew Garfield; Richard Blais. (N) Å Live! With Kelly (N) Å The View (N) Å FreeCruise Paid Program ) , Arthur (EI) Å Martha Speaks Å Curious George Å Cat in the Hat Å Super Why! Å Dinosaur Train Å Sesame Street (EI) Å Sid the Science Å WordWorld (EI) Å Super Why! Å Barney & Friends Å L ` Morning News Å Morning News Å CBS This Morning Ewan McGregor; Grant Hill. (N) Å The Doctors (N) Å The Price Is Right (N) Å The Young and the Restless (N) Å & 2 BBC World News Å Kentucky Health Å Body Electric Å TV 411 Å GED Connection Å GED Connection Å Paint This-Jerry Å Quilt in a Day Å Knitting Daily Å Beads, Baubles Å Charlie Rose Å WGN / Paid Program Paid Program Bewitched Å Dream of Jeannie Å Matlock “The Ghost” Å Matlock “The Class” Å In the Heat of the Night “Discovery” Å In the Heat of the Night Å INSP 1 Int’nl Fellowship Life Today Å Creflo Dollar Å Feed the Children Victory Today Life Today Å Joseph Prince Å Joyce Meyer Å Humanitarian Int’nl Fellowship The Waltons “The Idol” TBN 5 Spring Praise-A-Thon Spring Praise-A-Thon HGTV 7 Destination De Marriage/Const. -

New Hampshire Road Trip!

JANUARY 2012 Remembering Longtime IOP Advisor Milt Gwirtzman New JFK Jr. Forum Microsite Alumni Q & A with Peter Buttigieg ’04 2012 Polling and Research Careers and Internships New Mayors Conference NEW HAMPSHIRE ROAD TRIP! With the 2012 Republican presidential primary race in high gear this fall, students packed buses to nearby New Hampshire to meet presidential candidates as the IOP conducted timely younger voter public opinion research in Iowa and the Granite State. Welcome to the Institute of Politics at Harvard University Trey Grayson, Director The 2012 election cycle is in high gear, and the past six months have been fast- paced at the Institute. As you will note in this newsletter, the IOP has been at the forefront of election and campaign-related programming, with events, conferences and younger voter research unavailable anywhere else. One of my biggest goals since beginning service as the Institute’s Director has been to improve how the IOP utilizes technology – in an effort to maximize efficiency internally and best distribute and share our content externally to audiences inter- ested in politics and public service. Toward this end, we are very pleased this month to unveil the new online home for John F. Kennedy Jr. Forum programming at www.jfkjrforum.org (see feature on next page). The new microsite not only has a state-of-the art design but also can broadcast Forum programming in a format allowing Forum events to be streamed live or viewed later on any computer or device, including iPads and iPhones. We are also hard at work building a new IOP-wide website – scheduled to be completed next fall – which improves our current website layout and better integrates key online content from Institute students and student publications like the Harvard Political Review. -

Notable Alumni in Journalism, Publishing and Print Media

Notable Alumni in Journalism, Publishing and Print Media UNION IN THE WORLD Paul Andrews ’71, technology Kenneth Gilpin ’72, economics writer (U.S. News & World Report, reporter, The New York Times The New York Times) Richard Roth ’70, award-winning Andrea Barrett ’74, writer; National television journalist, CBS News; won Book Award winner (Ship Fever and the RTNDA Edward R. Murrow Award Other Stories, 1996); Pulitzer Prize for and two Emmy Awards Fiction finalist (Servants of the Map, 2003); recipient, MacArthur Fellowship Howard Simons ’51, managing ‘Genius Grant’ (2001) director of the Washington Post during Watergate coverage Nicole Beland ’96, executive editor of Cosmopolitan magazine; Scott Stedman ’99, founder, columnist for Men’s Health The L Magazine magazine; freelance writer Kate White ’72, editor-in-chief, Phil Beuth ’54, former president of Cosmopolitan magazine; author; morning and late night programming Hearst Corp. executive on ABC; one of the creators of the Capital Cities broadcast empire, which John Howard Payne 1806–1808, poet, acquired ABC in the mid-1980s playwright, actor and creator of the popular song “Home! Sweet Home!” John Bigelow 1835, managing editor and co-owner of the New York Evening Dylan Ratigan ’94, host of MSNBC’s The Post with poet William Cullen Bryant; Dylan Ratigan Show and former global anti-slavery activist; consul-general managing editor for corporate finance and minister to France under President at Bloomberg News. Developed more Lincoln. Noted author and co-founder than half a dozen broadcast and new of the New York Public Library media properties, including CNBC’s Fast Money. Richard Ferguson ’67, vice president and co-chief operating officer, Cox Radio, Inc.; former president and co-owner, NewCity Communications Union College 807 Union Street, Schenectady, NY 12308 518.388.6180 WWW.UNION.EDU Last updated: 7/2012. -

Efficacy of the Obama Policies to Combat Al-Qa'eda, the Taliban, And

Digital Commons at St. Mary's University Faculty Articles School of Law Faculty Scholarship 2010 Efficacy of the Obamaolicies P to Combat Al-Qa’eda, the Taliban, and Associated Forces—The First Year Jeffrey F. Addicott St. Mary's University School of Law, [email protected] Follow this and additional works at: https://commons.stmarytx.edu/facarticles Part of the Law Commons Recommended Citation Jeffrey F. Addicott, Efficacy of the Obama Policies to Combat Al-Qa’eda, the Taliban, and Associated Forces—The First Year , 30 Pace L. Rev. 340 (2010). This Article is brought to you for free and open access by the School of Law Faculty Scholarship at Digital Commons at St. Mary's University. It has been accepted for inclusion in Faculty Articles by an authorized administrator of Digital Commons at St. Mary's University. For more information, please contact [email protected]. Efficacy of the Obama Policies to Combat Al-Qa’eda, the Taliban, and Associated Forces—The First Year Jeffrey F. Addicott “The views of men can only be known, or guessed at, by their words or actions.”1 George Washington, 1799 When Senator Barack Obama ran for President of the United States in the 2008 election against Senator John McCain,2 his major campaign slogans were based on a cry for “change.”3 Of course, even the novice student of political science knows that the promise of change crops up during practically every presidential campaign in American history Distinguished Professor of Law and Director, Center for Terrorism Law, St. Mary‟s University School of Law. -

Occupy Wall Street's Challenge to an American Public Transcript

City University of New York (CUNY) CUNY Academic Works All Dissertations, Theses, and Capstone Projects Dissertations, Theses, and Capstone Projects 10-2014 Occupy Wall Street's Challenge to an American Public Transcript Christopher Neville Leary Graduate Center, City University of New York How does access to this work benefit ou?y Let us know! More information about this work at: https://academicworks.cuny.edu/gc_etds/324 Discover additional works at: https://academicworks.cuny.edu This work is made publicly available by the City University of New York (CUNY). Contact: [email protected] OCCUPY WALL STREET’S CHALLENGE TO AN AMERICAN PUBLIC TRANSCRIPT by Christopher Leary A dissertation submitted to the Graduate Faculty in English in partial fulfillment of the requirements for the degree of Doctor of Philosophy, The City University of New York 2014 This manuscript has been read and accepted for the Graduate Faculty in English in satisfaction of the dissertation requirement for the degree of Doctor of Philosophy. Dr. Ira Shor ________ _ 5/21/2014 __________________ ______ Date Chair of Examining Committee __Dr. Mario DiGangi ______________ _________________________ Date Executive Officer Dr. Jessica Yood Dr. Ashley Dawson Supervisory Committee THE CITY UNIVERSITY OF NEW YORK ii Abstract OCCUPY WALL STREET’S CHALLENGE TO AN AMERICAN PUBLIC TRANSCRIPT by Christopher Leary Adviser: Dr. Ira Shor This dissertation examines the rhetoric and discourses of the anti-corporate movement Occupy Wall Street, using frameworks from political ethnography and critical discourse analysis to offer a thick, triangulated description of a single event, Occupy Wall Street’s occupation of Zuccotti Park. The study shows how Occupy achieved a disturbing positionality relative to the forces which routinely dominate public discourse and proposes that Occupy’s encampment was politically intolerable to the status quo because the movement held the potential to consolidate critical thought and action. -

Super PAC Me: the Effects of Unlimited Secret Money in the 2012 Elections and Renewed Need for Campaign Finance Reform" (2013)

Seton Hall University eRepository @ Seton Hall Law School Student Scholarship Seton Hall Law 5-1-2013 Super PAC Me: The ffecE ts of Unlimited Secret Money in the 2012 Elections and Renewed Need for Campaign Finance Reform Jason Daniel Angelo Follow this and additional works at: https://scholarship.shu.edu/student_scholarship Recommended Citation Angelo, Jason Daniel, "Super PAC Me: The Effects of Unlimited Secret Money in the 2012 Elections and Renewed Need for Campaign Finance Reform" (2013). Law School Student Scholarship. 178. https://scholarship.shu.edu/student_scholarship/178 SUPER PAC ME: THE EFFECTS OF UNLIMITED SECRET MONEY IN THE 2012 E LECTIONS AND THE RENEWED NEED FOR CAMPAIGN FINANCE REFORM By Jason D. Angelo* "Thank you, God bless you all, and God Bless Citizens United!" 1 The irony in Stephen Colbert's voice was apparent, but his point was not lost amongst the satire: following the Supreme Court's green-light in the controversial case Citizens United v. FEC, the unprecedented amount of money being expended in anticipation ofthe 2012 federal elections is cause for concern, and nothing less than the integrity of American democracy itself is at stake. Colbert's late-night demonstration of the ease with which candidates can create and subsequently 'distance' themselves from so-called super 'PACs' - political action committees that exist solely for promoting a specific candidate3 - made a mockery of a system built to safeguard the electoral process but now being manipulated by those who can ' pay to play' at the expense of those who cannot afford to have their voices heard. 4 Why should the amount of money in politics matter to the average American? There are billions ofreasons.5 ' Big money' dominates the American political landscape and continually chips away at the integrity of our representative democracy; "wealthy contributors .. -

No SB Caucus Needed As Only Emma & Noah Now Running Primary Now

Vol. 37, No. 5 www.arlingtondemocrats.org May 2012 Congrats! One election is canceled . Emma No SB caucus needed as only Violand- Sanchez Emma & Noah now running The School Board Caucus scheduled for May able to eliminate two—the School Board caucus and 9 and 12 has now been canceled as only two candi- the caucus to elect delegates to the state and 8th Dis- dates remain seeking the Democratic endorsement trict conventions. Since in both cases, the number for the two School Board seats on the ballot this of candidates does not exceed the number of seats, November. no caucus is required. Larry Fishtahler pulled out of the race in Fishtahler issued a statement explaining his April leaving just Noah Simon, president of the PTA withdrawal. “From the time I began, I knew that to at the Science Focus School, and Emma Violand- be successful, a number of conditions should be met Sanchez, an incumbent, in the running for the en- by the end of March. Over the spring break, I de- Noah dorsement for the two seats. termined that a necessary condition had not been The May 2 monthly ACDC meeting will be achieved,” he said, without detailing what that con- Simon asked to give the formal Democratic endorsement dition was. to Simon and Violand-Sanchez. Fishtahler was the Democratic endorsee for the Where ACDC was adding more and more elec- School Board race in 2003, but lost to Dave Foster, for School Board tions at the beginning of the year, it has now been the incumbent and Republican-endorsed candidate. -

I Can Be Amazed

PAGE 10B PRESS & DAKOTAN ■ FRIDAY, MARCH 2, 2012 FRIDAY PRIMETIME/LATE NIGHT MARCH 9, 2012 Conservative 3:00 3:30 4:00 4:30 5:00 5:30 6:00 6:30 7:00 7:30 8:00 8:30 9:00 9:30 10:00 10:30 11:00 11:30 12:00 12:30 1:00 1:30 BROADCAST STATIONS Girls High School Basketball SDHSAA Class Fetch! Nightly PBS NewsHour (N) (In Girls High School Basketball SDHSAA Class Girls High School Basketball SDHSAA Class Don McLean: American Trou- America’s POV Singer Patti PBS B Tournament, Consolation Game: Teams TBA. With Ruff Business Stereo) Å B Tournament, First Semifinal: Teams TBA. (N) B Tournament, Second Semifinal: Teams TBA. badour Singer-songwriter Don Heartland Smith’s career. (In Publisher KUSD ^ 8 ^ (N) (Live) Ruffman Report (Live) (N) (Live) McLean’s career. Å Stereo) Å KTIV $ 4 $ Extra (N) Cash Ellen DeGeneres News 4 News News 4 Ent Who Do You Grimm (N) Å Dateline NBC (N) News 4 Jay Leno Late Night Carson News 4 Extra The Doctors “What the Judge Judge KDLT NBC KDLT The Big Who Do You Think You Grimm Investigating an Dateline NBC (N) (In KDLT The Tonight Show Late Night With Jimmy Last Call According Paid Pro- NBC Heck Does That Do?” Judy Å Judy Å News Nightly News Bang Are? “Jerome Bettis” arson-related homicide. Stereo) Å News With Jay Leno (In Fallon (In Stereo) Å With Car- to Jim Å gram Breitbart KDLT % 5 % (N) Å (N) Å News (N) (N) Å Theory (N) Å (N) Å (N) Å Stereo) Å son Daly KCAU ) 6 ) Dr. -

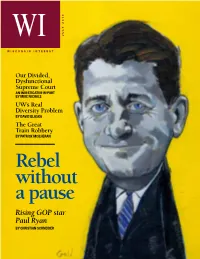

Rebel Without a Pause Rising GOP Star Paul Ryan by Christian Schneider Editor > Charles J

WI 2010 JULY WISCONSIN INTEREST Our Divided, Dysfunctional Supreme Court AN INVESTIGATIVE REPORT BY MIKE NICHOLS UW’s Real Diversity Problem BY DAVID BLASKA The Great Train Robbery BY PATRICK MCILHERAN Rebel without a pause Rising GOP star Paul Ryan BY CHRISTIAN SCHNEIDER Editor > CHARLES J. SYKES Hard choices WI WISCONSIN INTEREST For a rising political star, Paul Ryan remains a nation’s foremost celebrity wonk, asking: remarkably lonely political figure. For years, “What’s so damn special about Paul Ryan?” under both Democrats and Republicans, he More than his matinee-idol looks. has warned about the need to avert a fiscal “Ryan is a throwback,” writes Schneider, Publisher: meltdown, but even though his detailed “he could easily have been a conservative Wisconsin Policy Research Institute, Inc. “Roadmap” for restraining government politician in the era before cable news. He spending was widely praised, it was embraced has risen to national stardom by taking the Editor: Charles J. Sykes by very few. path least traveled by modern politicians: He Despite lip-service praise from President knows a lot of stuff.” Managing Editor: Marc Eisen Obama, Democrats have launched serial Also in this issue, Mike Nichols examines Art Direction: attacks against the plan, while GOP leaders Wisconsin’s dysfunctional, divided Supreme Stephan & Brady, Inc. have made themselves scarce, avoiding being Court and the implications for law in the state. Contributors: yoked to the specificity of Ryan’s hard choices. Patrick McIlheran deconstructs the state’s David Blaska But Ryan’s warnings have taken on new signature boondoggle, the billion-dollar not- Richard Esenberg urgency as Europe’s debt crisis unfolds, and so-fast train from Milwaukee to somewhere Patrick McIlheran the U.S. -

Corruption Perceptions Index 2019

CORRUPTION PERCEPTIONS INDEX 2019 Transparency International is a global movement with one vision: a world in which government, business, civil society and the daily lives of people are free of corruption. With more than 100 chapters worldwide and an international secretariat in Berlin, we are leading the fight against corruption to turn this vision into reality. #cpi2019 www.transparency.org/cpi Every effort has been made to verify the accuracy of the information contained in this report. All information was believed to be correct as of January 2020. Nevertheless, Transparency International cannot accept responsibility for the consequences of its use for other purposes or in other contexts. ISBN: 978-3-96076-134-1 2020 Transparency International. Except where otherwise noted, this work is licensed under CC BY-ND 4.0 DE. Quotation permitted. Please contact Transparency International – [email protected] – regarding derivatives requests. CORRUPTION PERCEPTIONS INDEX 2019 2-3 14-15 22-23 Map and results Asia Pacific Western Europe & Indonesia European Union 4-5 Papua New Guinea Malta Executive summary Estonia Recommendations 16-17 Eastern Europe & 24-25 Central Asia Trouble at the top 6-8 Armenia Global highlights TABLE OF CONTENTS TABLE Kosovo 26 Methodology 9-11 18-19 Political integrity Middle East & North 27-29 Transparency in Africa Endnotes campaign finance Tunisia Political decision-making Saudi Arabia 12-13 20-21 Americas Sub-Saharan Africa United States Angola Brazil Ghana TRANSPARENCY INTERNATIONAL 180 COUNTRIES. 180 SCORES. -

Sue Ansel President & Chief Executive Officer Gables Residential

Sue Ansel President & Chief Executive Officer Gables Residential Sue Ansel is President and Chief Executive Officer. In her 25 plus years with Gables, she has held positions in acquisitions, development, and operations and has led important company initiatives including the advancement of real estate technology efforts and third-party client services. Sue serves on several boards and committee’s including serving as an officer and on the Executive Committee of the National Multi-Housing Council, The Real Estate Council Foundation Board of Directors, the Legislative Affairs Committee of the Apartment Association of Greater Dallas, The Dallas Summer Musical Board of Directors and the Board of Visitors of DePauw University where she serves as Chairman. Sue is also a member of the Urban Land Institute and a graduate of DePauw University. Daniel Barile Director & Senior Investment Analyst SkyBridge Capital Daniel Barile is a Director and Senior Investment Analyst at SkyBridge Capital. He is responsible for hedge fund manager sourcing, research and due diligence, primarily for event driven and macro strategies. Prior to joining SkyBridge, Mr. Barile covered traditional and alternative asset managers from a variety of perspectives at Citi Alternative Investments, Fitch Ratings and Merrill Lynch Investment Managers (now BlackRock). Mr. Barile received a B.S. in Management with a concentration in Finance from Binghamton University and holds the Chartered Financial Analyst (CFA) and Chartered Alternative Investment Analyst (CAIA) designations. David R. Barker Partner, Barker Apartments Adjunct Professor, Department of Finance, University of Iowa David R. Barker is an American author, academic and businessman. A former economist for the Federal Reserve, Barker is the author of Welcome to Free America, a book set in the year 2057 as a guide to immigrants coming to the former United States after the collapse of government. -

CPB Station Activity Survey for 2017 1. Describe Your Overall

Section 6: Local Content & Services Report– CPB Station Activity Survey for 2017 1. Describe your overall goals and approach to address identified community issues, needs, and interests through your station’s vital local services, such as multiplatform long and short-form content, digital and in-person engagement, education services, community information, partnership support, and other activities, and audiences you reached or new audiences you engaged. New York Public Radio (NYPR) is an independent nonprofit news and cultural organization that owns and operates a portfolio of radio stations, digital properties, and a performance space in Manhattan. NYPR’s commitment to the community and to public service is central to its mission. NYPR produces groundbreaking news and cultural programming that invite ongoing civic dialogue. We continuously explore ways to be an essential resource for New York City’s diverse communities, promoting inclusion, awareness and intercultural engagement. NYPR is dedicated to developing meaningful partnerships, promotions and special events to extend our mission. By immersing ourselves in the community, NYPR addresses issues that reflect the issues and interests of our time and help tell the stories that matter. We constantly work to increase our relevance as a public radio station and ensure that our programming reflects the voices of the New York metropolitan area. Through content across the station’s distribution channels and platforms on-air, online and on the ground, NYPR strengthens community connections throughout the city. We are committed to reflecting the values, concerns and goals of our multi-cultural and multi-ethnic listeners. NYPR provides responsive services and tools that enable our audience to access our content anywhere any time.