DNB Bank ASA (Incorporated with Limited Liability in Norway) U.S.$10,000,000,000 Medium-Term Note Program

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Resolution Plan 2018 Public Section

RESOLUTION PLAN 2018 PUBLIC SECTION TABLE OF CONTENTS Page INTRODUCTION ......................................................................................................................... 1 1. Names of Material Entities .................................................................................... 3 2. Description of Core Business Lines ....................................................................... 3 3. Summary Financial Information Regarding Assets, Liabilities, Capital, and Major Funding Sources. .................................................................................. 4 4. Description of Derivatives and Hedging Activities ............................................... 7 5. Memberships in Material Payment, Clearing, and Settlement Systems ................ 7 6. Description of Foreign Operations......................................................................... 8 7. Identities of Material Supervisory Authorities ...................................................... 8 8. Identities of Principal Officers ............................................................................... 9 9. Corporate Governance Structure and Processes Related to Resolution Planning ............................................................................................................... 10 10. Material Management Information Systems ........................................................ 11 11. High Level Description of Resolution Strategy ................................................... 12 -i- INTRODUCTION Section -

Wells Fargo International Equity Fund

QUARTERLY MUTUAL FUND COMMENTARY Q4 2020 | All information is as of 12/31/2020 unless otherwise indicated. Wells Fargo International Equity Fund Quarterly review GENERAL FUND INFORMATION ● The International Equity Fund underperformed the MSCI ACWI ex USA Index (Net) Ticker: WFENX and the MSCI ACWI ex USA Value Index (Net) for the quarter that ended December 31, 2020. Portfolio managers: Dale A. Winner, ● Performance was driven largely by stock selection, with positive contributions coming CFA®; and Venk Lal from investments in the industrials and materials sectors as well as in China/Hong Subadvisor: Wells Capital Kong and Canada. Management Inc. ● Positions in information technology (IT) and health care as well as in France and Japan Category: Foreign large value detracted from performance. Market review FUND STRATEGY ● Maintains a core equity style that International equity markets initially declined in October before advancing 19.6% in the emphasizes bottom-up stock final two months of the year as multiple COVID-19 vaccines reached 90%+ efficacy and selection based on rigorous, uncertainty surrounding the U.S. presidential election receded, resulting in a 17.0% in-depth, fundamental company return for the MSCI All Country World ex USA Index (Net) in the fourth quarter, the research highest quarterly return since the third quarter of 2009. In this environment, the Global ● Uses a bottom-up research process Purchasing Managers’ Index (PMI) reached 53.3 in October, the highest level since that targets companies with August 2018, but fell back to 52.7 in December, still in expansionary territory. Emerging underestimated earnings growth markets outperformed developed markets and sovereign yields saw mixed fluctuations potential or those trading at during the period, including the U.S. -

How Selection Mechanisms in Financial Institutions Contribute to Regional Path Development

How selection mechanisms in financial institutions contribute to regional path development Martin Gjelsvik Research Manager/Professor II IRIS/University of Stavanger, Norway E-mail: [email protected] Abstract This paper addresses an issue absent in most studies on regional economic development, the role of financial institutions. The study concentrates on how the financial institutions select which firms and projects to fund, and how the selection mechanisms enable or constrain development trajectories in their respective regions. The study is guided by an evolutionary perspective on regional economic development, invoking the concept of path dependency. In that context, financial institutions may contribute to path extension, path renewal, path transplantation or path creation. The paper is based on a study of financial institutions in four Norwegian regions, and offers micro-level insights on what is selected to form the four respective path developments. We find that banks primarily support path extensions and to some degree path renewal. Venture capital has turned into private equity funds and has become more risk averse. They contribute primarily to restructuring of existing industries. Seed capital to fund start-ups is scarce, and has become even scarcer after the financial crisis. 1 Introduction Financial institutions are obviously a vital element in the regional innovation ecology. However, they are mostly absent in accounts of regional innovation systems. When financial institutions are dealt with in this context, the focus is generally confined to the role of venture capital. Surprisingly, the role of banks in regional development are left out. This paper addresses this gap by discussing the role of a differentiated set of financial institutions, including banks, venture capital, seed capital and wealthy individuals. -

Country Profile, Norway

Update April 2009 COUNTRY PROFILE, NORWAY Introduction and Country Background 2 Banking Environment 4 Financial Authorities 6 Legal & Regulatory Issues 8 Market Dominant Banks 11 Clearing Systems 14 Payments & Collections Methods & Instruments 16 Electronic Banking 19 Cash Pooling Solutions 21 Tax Issues 23 Source and Contacts 28 Page 1 of 28 Country profile, Norway Introduction and Country Background Norway’s rugged Key Facts coastline facing the North Atlantic sea Capital - Major Cities Oslo – Bergen, Trondheim, Stavanger stretches over 2,500 Area 324,220 km2 km Population 4.799 million (01-2009 estimate) Languages Norwegian Currency NOK (Norwegian Kroner) Telephone Code +47 National/ Bank 2009 — 1 Jan; 9-10, 13 Apr; 1, 17, 21 May; 1 Jun; 25- Holidays 26 Dec Bank Hours Generally from 8:15–15:30 Mon-Fri* Business Hours 10.00–17.00 Mon–Fri, to 19.00 Thu, 9:00–14.00 Sat Stock Exchange Oslo Børs (Oslo Stock Exchange) Leading Share Index OSEBX Overall Share Index OSEAX There is usually a designated day during the week when business hours are ex- tended. However, this day varies from bank to bank. Measured by per cap- Economic Performance ita GDP, Norway is among the wealthiest 2005 2006 2007 2008 countries in the Exchange Rate – NOK/EUR1 8.00 8.05 8.0153 8.2194 world, supported in Exchange Rate – NOK/USD1 6.4450 6.4180 5.8600 5.6361 large part by its ex- Money Market Rate (%)1 2.15 3.02 4.79 6.01 ploitation of oil and Consumer Inflation (%)2 1.6 2.3 0.8 3.2 gas reserves Unemployment Rate (%)3 4.6 3.4 2.5 2.5 GDP (NOK billions)4 1,946 1,995 -

2626667.Pdf (1.837Mb)

BI Norwegian Business School - campus Oslo GRA 19703 Master Thesis Thesis Master of Science Evaluating the Predictive Power of Leading Indicators Used by Analysts to Predict the Stock Return for Norwegian Listed Companies Navn: Amanda Marit Ackerman Myhre Hadi Khaddaj Start: 15.01.2020 09.00 Finish: 01.09.2020 12.00 GRA 19703 0981324 0983760 Evaluating the Predictive Power of Leading Indicators Used by Analysts to Predict the Stock Return for Norwegian Listed Companies Supervisor: Ignacio Garcia de Olalla Lopez Programme: Master of Science in Business with Major in Accounting and Business Control Abstract This paper studies the predictive power of leading indicators used by interviewed analysts to predict the monthly excess stock returns for some of the most influential Norwegian companies listed on the Oslo Stock Exchange. The thesis primarily seeks to evaluate whether a multiple factor forecast model or a forecast combination model incorporating additional explanatory variables have the ability to outperform a five common factor (FCF) benchmark forecast model containing common factors for the Norwegian stock market. The in-sample and out-of- sample forecasting results indicate that a multiple factor forecast model fails to outperform the FCF benchmark model. Interestingly, a forecast combination model with additional explanatory variables for the Norwegian market is expected to outperform the FCF benchmark forecast model. GRA 19703 0981324 0983760 Acknowledgements This thesis was written as the final piece of assessment after five years at BI Norwegian Business School and marks the completion of the Master of Science in Business program. We would like to thank our supervisor Ignacio Garcia de Olalla Lopez for his help and guidance through this process. -

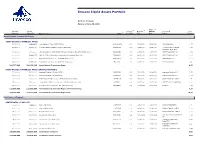

Invesco Liquid Assets Portfolio

Invesco Liquid Assets Portfolio Portfolio Holdings Data as of June 30, 2021 4 2 3 Final Principal Market 1 Coupon/ Maturity Maturity Associated % of Amount Value ($) Name of Issue CUSIP Yield (%) Date Date Issuer Portfolio Asset Backed Commercial Paper ASSET-BACKED COMMERCIAL PAPER 25,000,000 24,998,958 Ionic Capital III Trust (CEP-UBS AG) 46220WUG9 0.13 07/16/2021 07/16/2021 UBS GROUP AG 1.27 37,777,000 37,774,140 Lexington Parker Capital Company (Multi-CEP) 52953AUV5 0.15 07/29/2021 07/29/2021 Lexington Parker Capital 1.93 Company (Multi-CEP) 10,500,000 10,500,000 LMA Americas LLC (CEP-Credit Agricole Corporate & Investment Bank S.A.) 53944QXR6 0.05 10/25/2021 10/25/2021 CREDIT AGRICOLE SA 0.54 40,000,000 39,992,272 LMA SA (CEP-Credit Agricole Corporate & Investment Bank S.A.) 53944QW30 0.24 09/03/2021 09/03/2021 CREDIT AGRICOLE SA 2.04 20,000,000 20,000,000 Ridgefield Funding Co. LLC (CEP-BNP Paribas S.A.) 76582JW26 0.14 09/02/2021 09/02/2021 BNP PARIBAS SA 1.02 55,000,000 54,964,250 Ridgefield Funding Co. LLC (CEP-BNP Paribas S.A.) 76582JY81 0.14 11/08/2021 11/08/2021 BNP PARIBAS SA 2.80 188,277,000 188,229,620 Asset-Backed Commercial Paper 9.60 ASSET-BACKED COMMERCIAL PAPER (INTEREST BEARING) 50,000,000 50,000,000 Anglesea Funding LLC (Multi-CEP) 0347M5VG1 0.17 07/01/2021 08/04/2021 Anglesea Funding LLC 2.55 25,000,000 25,000,000 Anglesea Funding LLC (Multi-CEP) 0347M5VL0 0.17 07/01/2021 08/04/2021 Anglesea Funding LLC 1.27 10,000,000 10,000,000 Bedford Row Funding Corp. -

The Evolution of the Financial Services Industry and Its Impact on U.S

THOUGHT LEADERSHIP SERIES THE EVOLUTION OF THE FINANCIAL SERVICES INDUSTRY AND ITS IMPACT ON U.S. OFFICE SPACE June 2017 TABLE OF CONTENTS OVERVIEW OF U.S. FINANCIAL SERVICES INDUSTRY I PAGE: 4 OVERVIEW OF OFFICE MARKET CONDITIONS IN 11 MAJOR FINANCIAL CENTERS PAGE: 8 A. ATLANTA, GA PAGE: 8 B. BOSTON, MA PAGE: 10 C. CHARLOTTE, NC PAGE: 12 D. CHICAGO, IL PAGE: 14 E. DALLAS-FORT WORTH, TX II PAGE: 16 F. DENVER, CO PAGE: 18 G. MANHATTAN, NY PAGE: 20 H. ORANGE COUNTY, CA PAGE: 22 I. SAN FRANCISCO, CA PAGE: 24 J. WASHINGTON, DC PAGE: 26 K. WILMINGTON, DE PAGE: 28 MARKET SUMMARY AND ACTION STEPS III PAGE: 30 KEY FINDINGS The financial services sector has adapted its office-space usage in ways that are consistent with many office-using industries. However, its relationship to real estate has changed as a result of its role within the broader economy. In particular, four major causes have spurred a reduction in gross leasing activity by financial services firms: increased government regulation following the Great Recession of 2007-2009, cost reduction, efficient space utilization, and the emergence of the financial technology (fintech) sector. While demand for office space among financial services tenants has edged down recently overall, industry demand is inconsistent among major metros. For example, leasing increased for financial services tenants in San Francisco from 10% of all leasing activity in 2015 to 20% in 2016, while leasing among tenants in New York City declined from 32% to 20% over the same time period. Leasing trends within the financial services industry correlate with: the types of institutions involved, environments with policies and incentives that are conducive to doing business, the scale of operations and access to a highly-skilled talent pool, a shift from some urban to suburban locations, and a desire for new construction. -

Annual Report 2005 Dnb NOR Groupdnb NOR 2005

Annual report 2005 DnB NOR Group 2005 NORDnB Group www.dnbnor.com • Frits Thaulow, A Winterday, 1890 • The works of art featured in the annual report are The annual report has been produced by DnB NOR Shareholders registered as owners in DnB NOR ASA part of DnB NOR’s collection. This is one of Norway’s Corporate Communications, Group Financal Report- with the Norwegian Central Securities Depository largest private art collections, consisting of over ing and DnB NOR Graphic Centre. (VPS) can now receive annual reports electronically 10 000 works of art dating back from the end of the Design: Marit Høyland, Graphic Centre instead of by regular mail. For more information, 1800s to the present day. The works of art are on Photos: Stig B. Fiksdal and Anne-Line Bakken please contact your VPS registrar or go directly to display in DnB NOR’s offices in Norway and abroad, Print: Grafix AS www.vps.no/erapport.html. where they can be enjoyed by employees, customers and other visitors. 2005 in brief 4 Key fi gures and fi nancial calendar 5 From the desk of the CEO 6 What DnB NOR aspires to be 8 Directors’ report 10 Corporate governance 28 Risk and capital management 32 Stakeholders • Shareholders Contents • Customers 50 • Employees 52 • Society and the environment 5 Business areas 58 Staff and support units 76 Annual accounts 79 Auditor’s and Control Committee’s reports 158 Special articles • Pension reform 160 • Stability in the Norwegian economy 162 Contact information 164 Governing bodies 166 The Group’s annual report has been approved by the Board of Directors in the original Norwegian version. -

The Annual Report 2002 Documents Telenor's Strong Position in the Norwegian Market, an Enhanced Capacity to Deliver in The

The Annual Report 2002 documents Telenor’s strong position in the Norwegian market, an enhanced capacity to deliver in the Nordic market and a developed position as an international mobile communications company. With its modern communications solutions, Telenor simplifies daily life for more than 15 million customers. TELENOR Telenor – internationalisation and growth 2 Positioned for growth – Interview with CEO Jon Fredrik Baksaas 6 Telenor in 2002 8 FINANCIAL REVIEW THE ANNUAL REPORT Operating and financial review and prospects 50 Directors’ Report 2002 10 Telenor’s Corporate Governance 18 Financial Statements Telenor’s Board of Directors 20 Statement of profit and loss – Telenor Group 72 Telenor’s Group Management 22 Balance sheet – Telenor Group 73 Cash flow statement – Telenor Group 74 VISION 24 Equity – Telenor Group 75 Accounting principles – Telenor Group 76 OPERATIONS Notes to the financial statements – Telenor Group 80 Activities and value creation 34 Accounts – Telenor ASA 120 Telenor Mobile 38 Auditor’s report 13 1 Telenor Networks 42 Statement from the corporate assembly of Telenor 13 1 Telenor Plus 44 Telenor Business Solutions 46 SHAREHOLDER INFORMATION Other activities 48 Shareholder information 134 MARKET INFORMATION 2002 2001 2000 1999 1998 MOBILE COMMUNICATION Norway Mobile subscriptions (NMT + GSM) (000s) 2,382 2,307 2,199 1,950 1,552 GSM subscriptions (000s) 2,330 2,237 2,056 1,735 1,260 – of which prepaid (000s) 1,115 1,027 911 732 316 Revenue per GSM subscription per month (ARPU)1) 346 340 338 341 366 Traffic minutes -

The Norwegian Banks in the Nordic Consortia: a Case of International Strategic Alliances in Banking 1

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Research Papers in Economics Financial The Norwegian Banks in the Nordic Institutions Consortia: A Case of International Center Strategic Alliances in Banking by Siv Fagerland Jacobsen Adrian E. Tschoegl 97-39 THE WHARTON FINANCIAL INSTITUTIONS CENTER The Wharton Financial Institutions Center provides a multi-disciplinary research approach to the problems and opportunities facing the financial services industry in its search for competitive excellence. The Center's research focuses on the issues related to managing risk at the firm level as well as ways to improve productivity and performance. The Center fosters the development of a community of faculty, visiting scholars and Ph.D. candidates whose research interests complement and support the mission of the Center. The Center works closely with industry executives and practitioners to ensure that its research is informed by the operating realities and competitive demands facing industry participants as they pursue competitive excellence. Copies of the working papers summarized here are available from the Center. If you would like to learn more about the Center or become a member of our research community, please let us know of your interest. Anthony M. Santomero Director The Working Paper Series is made possible by a generous grant from the Alfred P. Sloan Foundation The Norwegian Banks in the Nordic Consortia: A Case of International Strategic Alliances in Banking 1 August 1997 Release 1.05 (Not released yet) Comments are welcome. Abstract: Despite the scholarly interest in joint ventures and strategic alliances, the consortium bank movement represents an under-researched phase in post-war banking history. -

Sparebankstiftelsen DNB NOR Årsrapport

Sparebankstiftelsen DNB NOR Årsrapport Forside: Nær 70 fjellrockentusiaster brukte en langhelg i sommerferien til å arbeide dugnad for Vinjerock på Eidsbugarden i Jotunheimen i 2011. Arrangementet som gikk under navnet Krafsefestivalen, samlet frivillige fra hele landet. Vinjerock har fått bidrag til utbedring av festivalområdet av Sparebankstiftelsen DNB NOR. Januar 2011 Juni 2011 • Representanter for kulturlivet og frivil- • Telemark Museum får en samling av lighets-Norge inviteres til idémyldring porselen laget på Porsgrunn Porselens- for det som skal bli Oslos nye kulturhus i fabrikk på 1800-tallet i gave. Øvre Slottsgate 3. • Den nye utescenen på Akershus festning, • Raftostiftelsen, som hvert år deler ut som stiftelsen har bidratt til, blir Raftoprisen til menneskerettighets- høytidelig åpnet av daværende forsvars- forkjempere, åpner sitt nye undervisn- minister Grete Faremo og Oslos ingstilbud, Rettighetstanken. Sparebank- ordfører Fabian Stang. stiftelsen DNB NOR har bidratt med 1,4 millioner kroner. Juli 2011 • Festivalen Valdres Sommersymfoni Februar 2011 arrangeres, denne gang med nytt • Det kommer inn 1.690 gavesøknader konsertflygel. innen fristen 15. februar. Prioriterte • Nær 70 fjellrockentusiaster bruker en områder for 2011 er: Kulturminner og langhelg i sommerferien til å arbeide Ut i naturen. dugnad for Vinjerock i Jotunheimen. Med midler fra stiftelsen utbedres festivalområdet. Mars 2011 • Henie Onstad Kunstsenter får 4,5 mil- August 2011 lioner kroner over en treårs periode i gave til kjøp av ung eksperimentell samtids- • Kull 2 starter på Dannelsesprogrammet; kunst, og formidling av denne. ledelsesprogrammet som gis som inspi- rasjon til unge folk engasjert i frivillige organisasjoner. April 2011 • For første gang vises Svelviks historie i • Norsk Fjellmuseum i Lom får 2,469.000 et eget spill som engasjerer hele lokal- kroner til å tilgjengeliggjøre Klimapark miljøet. -

Det Viktigste Er Ikke Å Kunne Fly, Men Å Lage Fine Spor.”

Årsrapport 2004 ”Det viktigste er ikke å kunne fly, men å lage fine spor.” Innhold Vital – Norges største liv- og pensjonsselskap, side 1 Tre ting på en gang – administrerende direktør, side 3 2004 i korte trekk, side 4 Hovedtall/nøkkeltall (proforma), side 5 Lovendring for fremtiden, side 7 Kapitalforvaltning – lave renter og gode aksjemarkeder, side 8 Bedriftsmarked – sterk fl yttebalanse, side 9 Personmarked – sterk økning i salget, side 10 Offentlig marked – størst blant private selskaper, side 11 Vitals ledelse, side 12 Organisasjon, side 15 Vitals styrende organer, side 16 Årsberetning og regnskap, side 19 (Se egen innholdsfortegnelse) Beretninger – revisor, aktuar og kontrollkomité, side 50 Embedded Value per 31. desember 2004, side 53 Fra liv til pensjon Forsikringstekniske forhold, side 54 Defi nisjoner, side 56 Årene som kommer vet vi ikke så mye om, Vitals kontorer, side 58 men når det gjelder året som gikk har vi mye å fortelle. Bildene i denne årsrapporten er hentet fra årets Vital-kalender. I tillegg til at den viser kalenderåret 2005 fra januar til desember , presenterer den en visuell reise gjennom alle livets faser. Fra de første skrittene vi tar til den siste perioden vi lever her på kloden. Fra første tegn til liv og frem til pensjonsalderen. Vital – Norges største liv- og pensjonsselskap Vital Forsikring ASA er det største selskapet innen livsforsikring og pensjonssparing i Norge og Vital Link AS er det klart ledende selskapet innen unit linked-forsikring her i landet. Vital Forsikring, med datterselskapene Vital Eiendom og Vital Visjon: Vital gjør fremtiden enklere. Pekon, og søsterselskapet Vital Link, utgjør forretningsområdet Liv- og pensjon i DnB NOR-konsernet.