Annual Report 2005 Dnb NOR Groupdnb NOR 2005

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Baudits Rob Maiu Street Credit Uuiou

20— MANCHESTER HERALD, Tuesday. Oct. 10, 1989 I HOMES I HOMES I CARS FOR SALE CONDOMINIUMS I APARTMENTS I MISCELLANEOUS FOR SALE FOR SALE FOR RENT FOR SALE FOR SALE Decision In Hunt I Nobel MANCHESTER - Now MANCHESTER - A .1 Sp«ciolisl| Timely Buy. $184,900. BEAUTIFUL Northfleld MANCHESTER - 2 bed CHEVROLET 1978 Z28 only 135,000 for these Green Condo - 4 room brand new, huge, excit Wonderful 4 bedroom, room townhouse with E N D R O L L S Camaro - $950, t-tops, I'/i bath Colonial situ R a n c h . 2 b e d ro o m s , fireplace. All applian 350, sagInaw, 4 speed, Multipurpose use ing, 7 room , 1,800 sq. ft. newly carpeted, cen 27’/4" width — 25<i: MHS boys’ soccer | Economic scholar beautiful contempor- ated on a lovely lot on a ces, heat, hot water, 10 bolt post, stock quiet street. This qual tral air, carport. Prin carpeting, air condi 13" width — 2 for 254i wheels, no clutch. a i y Townhouses. cipals only. Call after Newsprint end rolls can be OK’d for Loomis/3 Cathedral ceilings, An ity built home awaits tioning. Call 649-5240. Runs. 875-4499._________ still in contention/11 honored for work/6 6pm. 645-1965.__________ picked up at the Manchaatar dersen windows, full you, complete with 2 MANCHESTER - 2 bed Herald ONLY before 11 a.m. 1984 FORD Escort Wagon basements, 2x6 con car garage, attic ton, SOUTH Windsor - 3 bed room townhouse with Monday through Thursday. - Auto, air, am/tm, struction, fam ily room security system and room Townhouse. -

Møter Med Utvalgte Malerier Av Inger Sitter 1952

Møter med utvalgte malerier av Inger Sitter 1952 – 1967 Emnekode KVI-3900 Sissel Dybvik Mastergradsoppgave i kunstvitenskap Fakultet for humaniora, samfunnsvitenskap og lærerutdanning Universitetet i Tromsø Våren 2010 Forsidebilde: Inger Sitter med maleriet Bibbi, 10.09.08. 2 Takk - Først og fremst til min veileder Svein Aamold for en spesielt krevende og inspirerende veiledning. - Til Ola for gode samtaler og positiv mottakelse av mine uavklarte spørsmål. - Til Liv Ragna for god støtte hele veien. - Til Torgrim for glimrende datateknisk bistand. - Til fakultetet for økonomisk bistand til mine galleri- og museumsbesøk. - Til min arbeidsplass Stakkevollan bedriftshelsetjeneste som gjorde det mulig å tilrettelegge dagen slik at jeg kunne følge forelesningene ved UiT. 3 ”Jeg skulle ønske at bildene mine kunne bli like naturlige og selvsagte som vær og vind og blodets kretsløp – og at de kunne oppleves som et stykke natur i seg selv, et stykke levende liv. Jeg skulle ønske at tilskueren ga tid, kunne gå inn i bildet – og fremfor alt ga opp sin redsel for ikke å forstå”. Inger Sitter 1990 4 Innhold Kap. I Introduksjon 7 1.1 Innledning 7 1.2 Om kunstneren Inger Sitter 9 1.3 Forskningshistorikk/litteratur 11 Kap. II Møte med maleriene 14 2.1 En gryende forenkling - abstraksjon 14 2.1.1 Gjenspeiling av modernismen 17 2.1.2 Konstruktivisme 28 2.1.3 Abstrakt eller nonfigurativt? 36 2.2 Det nonfigurative maleriet 41 2.2.1 Farge blir til form 44 2.2.2 Lyrisk abstrakt 52 2.2.3 En ny spontanitet 60 2.2.4 Fra mørke til lys 67 Kap. -

13Th International Conference on Cyber Conflict: Going Viral 2021

2021 13th International Conference on Cyber Confict: Going Viral T. Jančárková, L. Lindström, G. Visky, P. Zotz (Eds.) 2021 13TH INTERNATIONAL CONFERENCE ON CYBER CONFLICT: GOING VIRAL Copyright © 2021 by NATO CCDCOE Publications. All rights reserved. IEEE Catalog Number: CFP2126N-PRT ISBN (print): 978-9916-9565-4-0 ISBN (pdf): 978-9916-9565-5-7 COPYRIGHT AND REPRINT PERMISSIONS No part of this publication may be reprinted, reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of the NATO Cooperative Cyber Defence Centre of Excellence ([email protected]). This restriction does not apply to making digital or hard copies of this publication for internal use within NATO, or for personal or educational use when for non-proft or non-commercial purposes, providing that copies bear this notice and a full citation on the frst page as follows: [Article author(s)], [full article title] 2021 13th International Conference on Cyber Confict: Going Viral T. Jančárková, L. Lindström, G. Visky, P. Zotz (Eds.) 2021 © NATO CCDCOE Publications NATO CCDCOE Publications LEGAL NOTICE: This publication contains the opinions of the respective authors only. They do not Filtri tee 12, 10132 Tallinn, Estonia necessarily refect the policy or the opinion of NATO Phone: +372 717 6800 CCDCOE, NATO, or any agency or any government. NATO CCDCOE may not be held responsible for Fax: +372 717 6308 any loss or harm arising from the use of information E-mail: [email protected] contained in this book and is not responsible for the Web: www.ccdcoe.org content of the external sources, including external websites referenced in this publication. -

How Selection Mechanisms in Financial Institutions Contribute to Regional Path Development

How selection mechanisms in financial institutions contribute to regional path development Martin Gjelsvik Research Manager/Professor II IRIS/University of Stavanger, Norway E-mail: [email protected] Abstract This paper addresses an issue absent in most studies on regional economic development, the role of financial institutions. The study concentrates on how the financial institutions select which firms and projects to fund, and how the selection mechanisms enable or constrain development trajectories in their respective regions. The study is guided by an evolutionary perspective on regional economic development, invoking the concept of path dependency. In that context, financial institutions may contribute to path extension, path renewal, path transplantation or path creation. The paper is based on a study of financial institutions in four Norwegian regions, and offers micro-level insights on what is selected to form the four respective path developments. We find that banks primarily support path extensions and to some degree path renewal. Venture capital has turned into private equity funds and has become more risk averse. They contribute primarily to restructuring of existing industries. Seed capital to fund start-ups is scarce, and has become even scarcer after the financial crisis. 1 Introduction Financial institutions are obviously a vital element in the regional innovation ecology. However, they are mostly absent in accounts of regional innovation systems. When financial institutions are dealt with in this context, the focus is generally confined to the role of venture capital. Surprisingly, the role of banks in regional development are left out. This paper addresses this gap by discussing the role of a differentiated set of financial institutions, including banks, venture capital, seed capital and wealthy individuals. -

Country Profile, Norway

Update April 2009 COUNTRY PROFILE, NORWAY Introduction and Country Background 2 Banking Environment 4 Financial Authorities 6 Legal & Regulatory Issues 8 Market Dominant Banks 11 Clearing Systems 14 Payments & Collections Methods & Instruments 16 Electronic Banking 19 Cash Pooling Solutions 21 Tax Issues 23 Source and Contacts 28 Page 1 of 28 Country profile, Norway Introduction and Country Background Norway’s rugged Key Facts coastline facing the North Atlantic sea Capital - Major Cities Oslo – Bergen, Trondheim, Stavanger stretches over 2,500 Area 324,220 km2 km Population 4.799 million (01-2009 estimate) Languages Norwegian Currency NOK (Norwegian Kroner) Telephone Code +47 National/ Bank 2009 — 1 Jan; 9-10, 13 Apr; 1, 17, 21 May; 1 Jun; 25- Holidays 26 Dec Bank Hours Generally from 8:15–15:30 Mon-Fri* Business Hours 10.00–17.00 Mon–Fri, to 19.00 Thu, 9:00–14.00 Sat Stock Exchange Oslo Børs (Oslo Stock Exchange) Leading Share Index OSEBX Overall Share Index OSEAX There is usually a designated day during the week when business hours are ex- tended. However, this day varies from bank to bank. Measured by per cap- Economic Performance ita GDP, Norway is among the wealthiest 2005 2006 2007 2008 countries in the Exchange Rate – NOK/EUR1 8.00 8.05 8.0153 8.2194 world, supported in Exchange Rate – NOK/USD1 6.4450 6.4180 5.8600 5.6361 large part by its ex- Money Market Rate (%)1 2.15 3.02 4.79 6.01 ploitation of oil and Consumer Inflation (%)2 1.6 2.3 0.8 3.2 gas reserves Unemployment Rate (%)3 4.6 3.4 2.5 2.5 GDP (NOK billions)4 1,946 1,995 -

Art of the North

THE PEOPLE, PLACES, EVENTS AND INSTITUTIONS THAT CONTRIBUTE TO NORWAY’S VIBRANT ARTS SCENE. BY BORDALO II / PHOTO BY IAN COX IAN BY PHOTO / II BORDALO BY DEER BY SPY / PHOTO BY BRIANTALLMAN, BY VHILS / PHOTO BY IAN COX, COX, IAN BY PHOTO VHILS/ BY BRIANTALLMAN, BY PHOTO / SPY BY ALIVE URBAN ART “The future of Norwegian street and urban art is bright,” says Reed, who founded the Nuart BY FINTAN MAGEE / PHOTO BY IAN COX, COX, IAN BY PHOTO / MAGEE FINTAN BY Festival in 2001 as a celebration of street art, OF THE NORTH including graffiti, muralism, comic culture and stencil art. Held the first week of September, the event encourages conversation about what art From historic and contemporary artists to inspiring cities is and can be, as well as give a platform to local artists by staging events abroad and placing artists’ work in international collections, such as and districts, art is an important part of Norway’s identity, Berlin, Germany’s newly launched Urban Nation MONUMENT TO A DISAPPEARING MONUMENT DISAPPEARING A TO MONUMENT Museum for Urban Contemporary Art. “We as evidenced by the museums, galleries, festivals and people have a huge network of artists, producers and cultural workers who have come through the Nuart family,” says Reed, who is in the process of who celebrate the country’s creativity. “I think this idea that creating a Contemporary Institute for Urban Art in Stavanger, as well as collaborating with Oslo art is for everyone, the social democratization of the arts and TALLMAN, BRIAN BY PHOTO / NIMIBERGEN BY City Council on various projects. -

Byvekstavtale Mellom Oslo Kommune, Viken Fylkeskommune, Bærum

Byvekstavtale mellom Oslo kommune, Viken fylkeskommune, Bærum kommune, Lillestrøm kommune, Nordre Follo kommune og Staten v/Samferdselsdepartementet og Kommunal- og moderniseringsdepartementet Bakgrunn og formål Det er framforhandlet en byvekstavtale mellom staten, Oslo kommune, daværende Akershus fylkeskommune og kommunene Bærum, daværende Skedsmo og daværende Oppegård, jf vedlegg datert 26.06.2019. Den framforhandlede byvekstavtalen legger til grunn et nullvekstmål om at veksten i persontransporten skal tas med kollektivtransport, sykkel og gange. Byvekstavtalen er et virkemiddel for å nå dette målet. Byvekstavtalen skal også bidra til mer effektiv arealbruk og mer attraktive by- og tettstedssentre. Staten v/Samferdselsdepartementet og Kommunal- og moderniseringsdepartementet, Oslo kommune, Viken fylkeskommune, Bærum kommune, Lillestrøm kommune og Nordre Follo kommune inngår med dette byvekstavtale for Osloområdet for perioden 2019-2029 i tråd med vedlagte dokument. Lokalpolitisk behandling Det ble gitt tilslutning til den framforhandlede byvekstavtalen ved vedtak i Oslo bystyre 13.11.2019, Viken fylkesting 13.12.2019, Bærum kommunestyre 27.11.2019, daværende Skedsmo kommunestyre (nåværende Lillestrøm kommune) 21.11.2019 og daværende Oppegård kommunestyre (nåværende Nordre Follo kommune) 23.09.2019. Samferdselsdepartementets og Kommunal- og moderniseringsdepartementets behandling Etter drøftinger i regjeringen slutter Samferdselsdepartementet og Kommunal- og moderniseringsdepartementet seg til den framforhandlede byvekstavtalen. Fornebubanen -

A TWIN CITIES CAMPUS I 1 I Emergency Numbers Contents

PREGNANT? ABORTION SERVICES - CONFIDENTIAL • Non-Surgical Abortion • Board Certified Physicians in If Less Than 8 Weeks OB/GYN •Surgical Abortion to 21 Weeks •Serving Women Since 1973 • Free Pregnancy Testing • Located Close to U of M • Private Clinic • Most Insurance Accepted Meadowbrook Women's Clinic Call For Information 825 S 8th St #1018 612-376-7708 7am - 6pm M-F Minneapolis, MN www.meadowbrookclinic.com gam - 3pm Saturday Leasing: Office and Maintenance: 612-366-4659 612-331-8369 Espanol: Property Manager: 612-282-8749 TWIN CITIES 651-208-4680 1229 E Minneapolis Hennepin Ave HOUSING AND REALTY, LLC MN 55414 OnThe6oPC. com ~ 100% Satisfaction 6uaranteedl ill low ilL. 121m MLL COMPAQ. SONY. IBM Man - Thurs 7am - 11 pm Friday 7am - 8pm Saturday 12pm - 11 pm 612-378-3787 212 Ontario Street SE On ThelioPC. com q' . ",rr1IItrMs. Located on Ontario Street iust off Washington Ave, in Stadium Village. l "m,", LCD Mlflilltr, 612--379 2127 1OAt, Ii,,.,,,"m"., • All New Beds • Mystic Tan, UV-Free Tanning CJ nthe L 0 f \I [am p[/., ! 1l,ifJ/pttt Drim,S",fMf • On-Site Licensed Aesthetician MDAlti3 dU-D r UNIVERSITY OF MINNESOTA TWIN CITIES CAMPUS I 1 I Emergency Numbers Contents Directory of Services 2 TTYfTDD Calling Info & Pay Phone Locations, Campus Mail 3 To report fire, serious injury, illness, Phone Information & Instructions .4 or major utility failure University Organization ; 5 Board of Regents 5. From all locations 911 Administration 5 Regents Professors 6 Other Emergency Numbers (area code 612 Distinguished McKnight University Professors .•... 6 unless otherwise noted) Senate Members 6 Crisis Connection.................................. -

Newsletterwinter2014

NEWSLETTERWINTER2014 WELCOME NRC Realty & Capital Advisors, LLC is pleased to provide you with its first quarterly newsletter dealing with topics of interest to owners and operators in the convenience store and gasoline station industry. Given our industry experience and expertise, particularly as it relates to real estate and financial services, we believe that we are able to provide a wide array of information that should be of benefit to you and your business. In this inaugural issue, we begin a four-part series on Finally, we have enclosed an article entitled “NRC Achieves “Understanding the Value of Your Business.” The first article Banner Year in 2013” which highlights the notable in the series is “Why Should I Have My Company Valued?” transactions that NRC was involved in last year. Again, and is written by Evan Gladstone, Executive Managing looking at recent transactions and trends will provide a good Director and Ian Walker, Senior Vice President. “barometer” of things to look for in the future. This issue also contains a reprint of the “2013 C-Store We at NRC are excited about our quarterly newsletter and Industry Year in Review: An M&A and Capital Markets hope that you will find it of value. Should you have any Perspective” written by Dennis Ruben, Executive Managing questions about anything contained in this newsletter or any Director, which first appeared online on CSP Daily News other matter, please feel free to contact Evan Gladstone on January 8th through 10th as a three-part series. A at (312) 278-6801 or [email protected], Dennis review of that article should prove to be particularly useful Ruben at (480) 374-1421 or [email protected], or in understanding where the industry has been recently and Ian Walker at (312) 278-6830 or [email protected]. -

Byvekstavtale Mellom Oslo Kommune, Bærum Kommune, Skedsmo Kommune, Oppegård Kommune, Akershus Fylkeskommune Og Staten 2019 – 2029

Byvekstavtale Oslo og Akershus 26.06.19 Byvekstavtale mellom Oslo kommune, Bærum kommune, Skedsmo kommune, Oppegård kommune, Akershus fylkeskommune og Staten 2019 – 2029 Samferdselsdepartementet, Oslo kommune og Akershus fylkeskommune inngikk 13. juni 2017 en bymiljøavtale som skal legge til rette for at veksten i persontransporten i Oslo og Akershus skal tas med kollektivtrafikk, sykkel og gange. Avtalen var basert på Nasjonal transportplan (NTP) 2014-2023 og revidert avtale for Oslopakke 3 og beskriver oppgavedeling og ansvar for finansiering av tiltak mellom aktørene. Arealdelen av bymiljøavtalen ble nærmere konkretisert i en byutviklingsavtale som ble inngått mellom Kommunal- og moderniseringsdepartementet, Oslo kommune og Akershus fylkeskommune 29. september 2017. Her ble Regional Plan for areal og transport i Oslo og Akershus (RP-ATP), vedtatt 2015, lagt til grunn. Bymiljøavtalen og byutviklingsavtalen er nå reforhandlet til en felles byvekstavtale, basert på NTP 2018-2029, revidert avtale Oslopakke 3 for 2017-2036 og RP-ATP. Denne byvekstavtalen er inngått mellom Staten ved Samferdselsdepartementet og Kommunal- og moderniseringsdepartementet, Oslo kommune, Bærum kommune, Skedsmo kommune, Oppegård kommune og Akershus fylkeskommune, for perioden 2019-2029. Avtalen er et samarbeid mellom staten, fylkeskommunen og kommunene, der alle partene bidrar innenfor sine ansvarsområder. Avtalen er geografisk avgrenset til Oslo kommune og Akershus fylke. 1. Mål Overordnet mål Det overordnede målet for byvekstavtalen er nullvekstmålet, det vil si å sikre at veksten i persontransport tas med kollektivtransport, sykling og gange. Løsningene som velges må bidra til å sikre bedre framkommelighet totalt sett, spesielt ved å tilrettelegge for attraktive alternativer til privatbil. Befolkningsveksten i Oslo og Akershus utgjør rundt halvdelen av befolkningsveksten nasjonalt. -

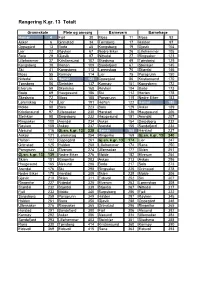

Rangering K.Gr. 13 Totalt

Rangering K.gr. 13 Totalt Grunnskole Pleie og omsorg Barnevern Barnehage Hamar 4 Fjell 30 Moss 11 Moss 92 Asker 6 Grimstad 34 Tønsberg 17 Halden 97 Oppegård 13 Bodø 45 Kongsberg 19 Gjøvik 104 Lier 22 Røyken 67 Nedre Eiker 26 Lillehammer 105 Sola 29 Gjøvik 97 Nittedal 27 Ringsaker 123 Lillehammer 37 Kristiansund 107 Skedsmo 49 Tønsberg 129 Kongsberg 38 Horten 109 Sandefjord 67 Steinkjer 145 Ski 41 Kongsberg 113 Lørenskog 70 Stjørdal 146 Moss 55 Karmøy 114 Lier 75 Porsgrunn 150 Nittedal 55 Hamar 123 Oppegård 86 Kristiansund 170 Tønsberg 56 Steinkjer 137 Karmøy 101 Kongsberg 172 Elverum 59 Skedsmo 168 Røyken 104 Bodø 173 Bodø 69 Haugesund 186 Ski 112 Horten 178 Skedsmo 72 Moss 188 Porsgrunn 115 Nedre Eiker 183 Lørenskog 74 Lier 191 Horten 122 Hamar 185 Molde 88 Sola 223 Sola 129 Asker 189 Kristiansund 97 Ullensaker 230 Harstad 136 Haugesund 206 Steinkjer 98 Sarpsborg 232 Haugesund 151 Arendal 207 Ringsaker 100 Arendal 234 Asker 154 Sarpsborg 232 Røyken 108 Askøy 237 Arendal 155 Sandefjord 234 Ålesund 116 Gj.sn. k.gr. 13 238 Hamar 168 Harstad 237 Askøy 121 Lørenskog 254 Ringerike 169 Gj.sn. k.gr. 13 240 Horten 122 Oppegård 261 Gj.sn. k.gr. 13 174 Lier 247 Grimstad 125 Halden 268 Lillehammer 174 Rana 250 Porsgrunn 133 Elverum 274 Ullensaker 177 Skien 251 Gj.sn. k.gr. 13 139 Nedre Eiker 276 Molde 182 Elverum 254 Skien 151 Ringerike 283 Askøy 213 Askøy 256 Haugesund 165 Ålesund 288 Bodø 217 Sola 273 Arendal 176 Ski 298 Ringsaker 225 Grimstad 278 Nedre Eiker 179 Harstad 309 Skien 239 Molde 306 Gjøvik 210 Skien 311 Eidsvoll 252 Ski 307 Ringerike -

Supplementary File for the Paper COVID-19 Among Bartenders And

Supplementary file for the paper COVID-19 among bartenders and waiters before and after pub lockdown By Methi et al., 2021 Supplementary Table A: Overview of local restrictions p. 2-3 Supplementary Figure A: Estimated rates of confirmed COVID-19 for bartenders p. 4 Supplementary Figure B: Estimated rates of confirmed COVID-19 for waiters p. 4 1 Supplementary Table A: Overview of local restrictions by municipality, type of restriction (1 = no local restrictions; 2 = partial ban; 3 = full ban) and week of implementation. Municipalities with no ban (1) was randomly assigned a hypothetical week of implementation (in parentheses) to allow us to use them as a comparison group. Municipality Restriction type Week Aremark 1 (46) Asker 3 46 Aurskog-Høland 2 46 Bergen 2 45 Bærum 3 46 Drammen 3 46 Eidsvoll 1 (46) Enebakk 3 46 Flesberg 1 (46) Flå 1 (49) Fredrikstad 2 49 Frogn 2 46 Gjerdrum 1 (46) Gol 1 (46) Halden 1 (46) Hemsedal 1 (52) Hol 2 52 Hole 1 (46) Hurdal 1 (46) Hvaler 2 49 Indre Østfold 1 (46) Jevnaker1 2 46 Kongsberg 3 52 Kristiansand 1 (46) Krødsherad 1 (46) Lier 2 46 Lillestrøm 3 46 Lunner 2 46 Lørenskog 3 46 Marker 1 (45) Modum 2 46 Moss 3 49 Nannestad 1 (49) Nes 1 (46) Nesbyen 1 (49) Nesodden 1 (52) Nittedal 2 46 Nordre Follo2 3 46 Nore og Uvdal 1 (49) 2 Oslo 3 46 Rakkestad 1 (46) Ringerike 3 52 Rollag 1 (52) Rælingen 3 46 Råde 1 (46) Sarpsborg 2 49 Sigdal3 2 46 Skiptvet 1 (51) Stavanger 1 (46) Trondheim 2 52 Ullensaker 1 (52) Vestby 1 (46) Våler 1 (46) Øvre Eiker 2 51 Ål 1 (46) Ås 2 46 Note: The random assignment was conducted so that the share of municipalities with ban ( 2 and 3) within each implementation weeks was similar to the share of municipalities without ban (1) within the same (actual) implementation weeks.