2016 Legislative Sessions Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Candidate's Report

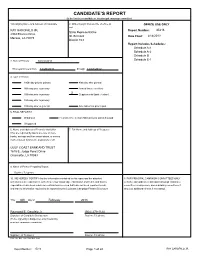

CANDIDATE’S REPORT (to be filed by a candidate or his principal campaign committee) 1.Qualifying Name and Address of Candidate 2. Office Sought (Include title of office as OFFICE USE ONLY well RAY GAROFALO JR. Report Number: 35216 State Representative 2304 Etienne Drive St. Bernard Date Filed: 2/14/2013 Meraux, LA 70075 District 103 Report Includes Schedules: Schedule A-1 Schedule A-2 Schedule B Schedule E-1 3. Date of Primary 10/22/2011 This report covers from 12/20/2011 through 12/31/2012 4. Type of Report: 180th day prior to primary 40th day after general 90th day prior to primary Annual (future election) X 30th day prior to primary Supplemental (past election) 10th day prior to primary 10th day prior to general Amendment to prior report 5. FINAL REPORT if: Withdrawn Filed after the election AND all loans and debts paid Unopposed 6. Name and Address of Financial Institution 7. Full Name and Address of Treasurer (You are required by law to use one or more banks, savings and loan associations, or money market mutual fund as the depository of all GULF COAST BANK AND TRUST 1615 E. Judge Perez Drive Chalmette, LA 70043 9. Name of Person Preparing Report Daytime Telephone 10. WE HEREBY CERTIFY that the information contained in this report and the attached 8. FOR PRINCIPAL CAMPAIGN COMMITTEES ONLY schedules is true and correct to the best of our knowledge, information and belief, and that no a. Name and address of principal campaign committee, expenditures have been made nor contributions received that have not been reported herein, committee’s chairperson, and subsidiary committees, if and that no information required to be reported by the Louisiana Campaign Finance Disclosure any (use additional sheets if necessary). -

74 Senate Concurrent Resolution No

OFFICIAL JOURNAL SENATE CONCURRENT RESOLUTION NO. 123— BY SENATORS PEACOCK, ALARIO, ALLAIN, APPEL, BARROW, OF THE BISHOP, BOUDREAUX, CARTER, CHABERT, CLAITOR, COLOMB, CORTEZ, DONAHUE, ERDEY, FANNIN, GATTI, HEWITT, JOHNS, LAFLEUR, LAMBERT, LONG, LUNEAU, MARTINY, MILKOVICH, SENATE MILLS, MIZELL, MORRELL, MORRISH, PERRY, PETERSON, RISER, GARY SMITH, JOHN SMITH, TARVER, THOMPSON, WALSWORTH, OF THE WARD AND WHITE AND REPRESENTATIVES STEVE CARTER, FOIL, STATE OF LOUISIANA JAMES, EDMONDS, DAVIS AND HOFFMANN _______ A CONCURRENT RESOLUTION To commemorate the lifetime achievements of publisher and entrepreneur, Robert G. "Bob" Claitor Sr. THIRTY-FIFTH D__A__Y__'S_ PROCEEDINGS Forty-Third Regular Session of the Legislature Reported without amendments. Under the Adoption of the Constitution of 1974 SENATE CONCURRENT RESOLUTION NO. 124— _______ BY SENATOR PEACOCK AND REPRESENTATIVES CARMODY, CREWS AND HORTON Senate Chamber A CONCURRENT RESOLUTION State Capitol To express the sincere condolences of the Legislature of Louisiana Baton Rouge, Louisiana upon the passing of Coach John Thompson, renowned football Wednesday, June 7, 2017 coach, teacher, and mentor and to celebrate his sports legacy that has spanned the greater portion of five decades. The Senate was called to order at 10:40 o'clock A.M. by Hon. John A. Alario Jr., President of the Senate. Reported without amendments. Respectfully submitted, Morning Hour ALFRED W. SPEER Clerk of the House of Representatives CONVENING ROLL CALL Message from the House The roll being called, the following members answered to their names: DISAGREEMENT TO HOUSE BILL PRESENT June 7, 2017 Mr. President Erdey Morrell To the Honorable President and Members of the Senate: Allain Fannin Morrish Appel Gatti Peacock I am directed to inform your honorable body that the House of Barrow Hewitt Perry Representatives has reconsidered to concur in the proposed Senate Bishop Johns Peterson Amendment(s) to House Bill No. -

Election 2015

Election 2015 OFFICE (*INCUMBENT) PARTY OFFICE (*INCUMBENT) PARTY GOVERNOR STATE REPRESENTATIVE 43RD REPRESENTATIVE DISTRICT (1 to be elected) (1 to be elected) Scott A. Angelle Republican Stuart Bishop* Unopposed Republican Beryl Billiot No Party ‘Jay’ Dardenne Republican STATE REPRESENTATIVE 44TH REPRESENTATIVE DISTRICT Cary Deaton Democrat (1 to be elected) John Bel Edwards Democrat Desmond Onezine Other Jeremy ‘JW’ Odom No Party Vincent J. Pierre* Democrat Eric Paul Orgeron Other STATE REPRESENTATIVE 45TH REPRESENTATIVE DISTRICT S L Simpson Democrat (1 to be elected) David Vitter Republican André Comeaux Republican OFFICE LIEUTENANT GOVERNOR Jean-Paul Coussan Republican (1 to be elected) Jan Swift Republican Elbert Lee Guillory Republican Melvin L. ‘Kip’ Holden Democrat STATE REPRESENTATIVE 48TH REPRESENTATIVE DISTRICT ‘Billy’ Nungesser Republican Taylor Barras* Unopposed Republican John Young Republican TH OFFICE STATE REPRESENTATIVE 96 REPRESENTATIVE DISTRICT SECRETARY OF STATE (1 to be elected) (1 to be elected) Terry C. Landry Sr.* Democrat ‘Tom’ Schedler* Republican Raymond ‘Shoe-Do’ Lewis Democrat ‘Chris’ Tyson Democrat SHERIFF ATTORNEY GENERAL (1 to be elected) (1 to be elected) ‘Rick’ Chargois Republican Geraldine ‘Geri’ Broussard Baloney Democrat Mark T. Garber Republican James D. ‘Buddy’ Caldwell* Republican Chad Leger Republican Isaac ‘Ike’ Jackson Democrat John Rogers Republican ‘Jeff’ Landry Republican CLERK OF COURT ‘Marty’ Maley Republican Louis Perret* Unopposed Republican OFFICE TREASURER ASSESSOR (1 to be elected) (1 to be elected) John Kennedy* Republican Conrad Comeaux* Republican Jennifer Treadway Republican Rachelle Falgout No Party OFFICE COMMISSIONER OF AGRICULTURE AND FORESTRY CORONER (1 to be elected) Kenneth Odinet Jr.* Unopposed Republican ‘Charlie’ Greer Democrat Adrian ‘Ace’ Juttner Green CITY-PARISH PRESIDENT Jamie LaBranche Republican (1 to be elected) Michael G. -

Louisiana State University Student Government

Louisiana State University Student Government Dear LSU Students and Friends, Students in the state of Louisiana are more relevant than ever before. Before the release of the first Higher Education Report Card, students pursuing a degree were not valued in the state of Louisiana—proven by the 41% cut to higher education over the past 8 years. Contrary to popular belief, investment in higher education is the best societal investment that our state lawmakers can make. Because of our initial report card, leaders in the legislature are listening. The Higher Education Report Card is a huge step forward in ensuring that students are heard in the state of Louisiana. The requests are clear. We want stability in higher education and a sincere commitment to invest in the future of our students. We extend our sincerest gratitude to the governor and lawmakers for their work during the longest legislative session in the history of the state. Unfortunately, a session ending in a fully funded higher education and a partially funded TOPS is not ideal for Louisiana’s students. My hope is that the Higher Education Report Card can shed light onto the difficult votes that our lawmakers made during these sessions to ensure that our education would be fully funded. At the same time, I hope students will see that some of their own lawmakers are still not valuing our education as much as they can. We also hope that students will continue to be involved with the affairs of our state capitol by participating in marches and making calls to their legislators. -

Membership in the Louisiana House of Representatives

MEMBERSHIP IN THE LOUISIANA HOUSE OF REPRESENTATIVES 1812 - 2024 Revised – July 28, 2021 David R. Poynter Legislative Research Library Louisiana House of Representatives 1 2 PREFACE This publication is a result of research largely drawn from Journals of the Louisiana House of Representatives and Annual Reports of the Louisiana Secretary of State. Other information was obtained from the book, A Look at Louisiana's First Century: 1804-1903, by Leroy Willie, and used with the author's permission. The David R. Poynter Legislative Research Library also maintains a database of House of Representatives membership from 1900 to the present at http://drplibrary.legis.la.gov . In addition to the information included in this biographical listing the database includes death dates when known, district numbers, links to resolutions honoring a representative, citations to resolutions prior to their availability on the legislative website, committee membership, and photographs. The database is an ongoing project and more information is included for recent years. Early research reveals that the term county is interchanged with parish in many sources until 1815. In 1805 the Territory of Orleans was divided into counties. By 1807 an act was passed that divided the Orleans Territory into parishes as well. The counties were not abolished by the act. Both terms were used at the same time until 1845, when a new constitution was adopted and the term "parish" was used as the official political subdivision. The legislature was elected every two years until 1880, when a sitting legislature was elected every four years thereafter. (See the chart near the end of this document.) The War of 1812 started in June of 1812 and continued until a peace treaty in December of 1814. -

Louisiana Right to Life Louisiana House of Representatives Scorecard 2012-2015 with Cumulative Score Since 2008 2012 2013 2014 2015 2012-2015 Cumulative NAME Dist

Louisiana Right to Life Louisiana House of Representatives Scorecard 2012-2015 with Cumulative Score Since 2008 2012 2013 2014 2015 2012-2015 Cumulative NAME Dist. P 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Score Lifetime Neil C. Abramson 98 D A A A A A A A A A A A A + + A ?* ?* Bryan Adams 85 R + + + + + + + + + + + + + + + 100% 100% Andy Anders 21 D + + + + + + + + + + + A + + + 100% 96% James K. Armes 30 D - + + + + + + + A + + + + + + 94% 89% Jeff Arnold 102 D A + + + + + + + + + + + + + + 100% 96% Austin Badon 100 D A + + + + A + + A A + - + + + 92% 75% Taylor F. Barras 48 R A + + + + + + + + + + + + + + 100% 100% Regina Barrow 29 D + + + + + A + + + + + + + + + 100% 92% John Berthelot 88 R + + + + + + + + + + + + + + + 100% 100% Robert E. Billiot 83 D + + + + + + + + + + + + + + + 100% 100% Stuart J. Bishop 43 R + A + + + + + + + + + + + + + 100% 100% Wesley Bishop 99 D - + A + A A + + + A A + A + A ?* ?* Joseph Bouie 97 D N N N N N N N N N N N N N N A No Score No Score Chris Broadwater 86 R + + + + + + + + + + + + + A + 100% 100% Jared C. Brossett 97 D - + + A - - - - + - - - + A N 33% 42% Terry R. Brown 22 I + + + + + + + + + + + + + + + 100% 100% Richard Burford 7 R + + + + + + + + + + + + + + + 100% 100% Henry Burns 9 R + + + + + + + + + + + + + + + 100% 100% Timothy G. Burns 89 R A + + + + + + + + + + + + + + 100% 100% Roy Burrell 2 D - + + + + + + + + + + + + + + 94% 78% Thomas Carmody 6 R + + + + A + + + + + + + + + + 100% 100% Stephen F. Carter 68 R + + + + + + + + + + + + + + + 100% 100% Simone Champagne 49 R + + + + + + + + + + + + + + N 100% 96% Charles R. Chaney 19 R + + + + + + + + + + + + + + + 100% 100% Patrick Connick 84 R + + + + + + + + + + + A + + + 100% 100% Kenny R. Cox 23 D - + + A + + + + + + + + + + + 94% 93% Gregory Cromer 90 R A + + + + + A + + + + A + A A 100% 100% Michael Danahay 33 D + + + + + + + + + + + + + + + 100% 100% Hebert Dixon 26 D - + + + + + + + + - + + + + N 88% 69% Gordon Dove 52 R A + + + + + + + A A + A + A + 100% 100% John Bel Edwards 72 D A + + + + + + + + + + A + + + 100% 100% James R. -

ALEC in Louisiana Uncovering the Influence of the American Legislative Exchange Council (ALEC) in the Louisiana Legislature

ALEC in Louisiana Uncovering the Influence of the American Legislative Exchange Council (ALEC) in the Louisiana Legislature ALEC in Louisiana Uncovering the Influence of the American Legislative Exchange Council (ALEC) in the Louisiana Legislature Common Cause August 2018 Acknowledgements The Common Cause Education Fund is the research and public education affiliate of Common Cause, founded in 1970 by John Gardner. Common Cause is a nonpartisan grassroots organization dedicated to upholding the core values of American democracy. We work to create open, honest, and accountable government that serves the public interest; promote equal rights, opportunity, and representation for all; and empower all people to make their voices heard in the political process. This report was written by Jay Riestenberg and edited by Stephen Spaulding, with research contributions by Lily Oberstein, Kaitlyn Bryan, Molly Robertson, Jane Hood, Ryan Pierannunzi, and Kiera Solomon. The report was de- signed by Kerstin Diehn. Common Cause thanks the Center for Media and Democracy for its outstanding, ongoing research and investigative reporting on ALEC and ALEC’s corporate funders. Contents What Is ALEC? . 4 ALEC’s Funding ....................................................................................4 ALEC’s Illegal Lobbying & Charitable Status ...........................................................5 Louisiana Legislators With ALEC Ties .................................................................5 ALEC “Model” Bills in Louisiana ......................................................................9 Common Cause 3 What Is ALEC? ALEC brings together corporate representatives and elected officials to create and lobby for passage of “model bills” that often benefit the corporations’ bottom line. The bills typically are drafted and refined at ALEC meetings that are closed to the public and press, then introduced in state legislatures, usually without any public acknowledgement of ALEC’s role in creating and pushing them. -

Legislative Update 6-28-2020

AIA-LA Political Update June 26, 2020 Special Session Adjournment in View The 2020 special session must adjourn by 6pm on Tuesday, June 30th. There are still a few moving parts ambling their way through the final days. The biggest unresolved issues still in play involve the state budget and a series of interrelated tort reform bills/resolutions. The House adjourned late Thursday and will return to work today (Sunday) at 3pm. The Senate was in session through late Friday to take up the state’s operating budget on the floor along with a handful of other bills; they return today at 4pm to receive a few more bills. Historic Rehab Tax Credits HB 4 by Speaker Pro Temp Tanner Magee, R-Houma, extends the date for eligible expenses to qualify for the tax credit for the rehabilitation of historic structures and extends the effectiveness of the credit to July 1, 2026. This bill was heavily amended in the Senate and, as a result, the author rejected those amendments. The bill is now in conference committee and is expected to be amended to more closely resemble its original version. We’ll know soon whether this bill survives the entire process and head’s to the governor for final action. Tort Reform There are at least ten pieces of legislation alive that attempt to reduce auto insurance rates, which are among the highest in the nation and attributed to the state’s highly litigious culture. Those measures include: • HB 44 by Rep. Ray Garofalo, R-Chalmette, is another bite at the Omnibus Premium Reduction Act but was amended to remove all provisions except for those addressing the collateral source rule. -

Organizational Session

Dove Landry, T. Thibaut OFFICIAL JOURNAL Edwards LeBas Thierry Fannin Leger Thompson OF THE Foil Leopold Whitney Franklin Ligi Williams, A. HOUSE OF Gaines Lopinto Williams, P. Garofalo Lorusso Willmott Total - 105 REPRESENTATIVES OF THE The Acting Speaker announced that there were 105 members- elect present and a quorum. STATE OF LOUISIANA Prayer Prayer was offered by Dr. Ken Ward. FIRST DAY'S PROCEEDINGS Pledge of Allegiance Organizational Session of the 70th Legislature Since Admission to Statehood Representative-elect Lorusso led the House in reciting the Pledge of Allegiance to the Flag of the United States of America. Eighth Organizational Session Since Miss Ali LeBlanc sang The National Anthem. Adoption of the Constitution of 1974 Petitions, Memorials, and Communications House of Representatives State Capitol The following petitions, memorials, and communications were received and read: Baton Rouge, Louisiana SECRETARY OF STATE State of Louisiana Monday, January 9, 2012 November 29, 2011 The House of Representatives was called to order at 10:00 A.M., To the Clerk of the House of Representatives by the Honorable Jeffery J. Arnold, Acting Speaker of the House of State of Louisiana Representatives. Sir: Morning Hour I have the honor to transit herewith, in compliance with R.S. ROLL CALL 18:573, the name of the persons who have received the greatest number of votes cast for State Representative in the Legislature of The roll being called, the following members-elect answered to Louisiana from their respective Representative Districts, and who their names: have been duly proclaimed elected. PRESENT Sincerely, Abramson Geymann Mack Tom Schedler Adams Gisclair Miller Secretary of State Anders Greene Montoucet Armes Guillory Moreno Arnold Guinn Morris, Jay UNITED STATES OF AMERICA Badon Harris Morris, Jim State of Louisiana Barras Harrison Norton Barrow Havard Ortego Tom Schedler Berthelot Hazel Pearson Secretary of State Billiot Henry Pierre Bishop, S. -

Past Officers

Past Officers 2011 2012 2013 Chairman Jonathan Perry Jonathan Perry Vincent Pierre Vice-Chair Simone Champagne Nancy Landry Jonathan Perry Secretary/Treasurer Mickey Guillory Mickey Guillory Mickey Guillory Executive Committee Fred Mills Fred Mills Fred Mills Executive Committee Taylor Barras Page Cortez Terry Landry Executive Committee Elbert Guillory Simone Champagne Michael Danahay Executive Committee Karen St. Germain Johnny Guinn John Berthelot Executive Committee Ledricka Thierry Ledricka Thierry Ledricka Thierry Executive Committee Nancy Landry Stephen Ortego Joel Robideaux 2014 2015 2016 Chairman Vincent Pierre Vincent Pierre Vincent Pierre Vice-Chair Jonathan Perry Jonathan Perry Jonathan Perry Secretary/Treasurer Mickey Guillory Mickey Guillory John Berthelot Executive Committee Ledricka Thierry Ledricka Thierry Gerald Boudreaux Executive Committee Nancy Landry Nancy Landry Julie Emerson Executive Committee Edward Price Edward Price Blake Miguez Executive Committee Jack Montoucet Jack Montoucet Dustin Miller Executive Committee John Berthelot John Berthelot Jack Montoucet Executive Committee Joel Robideaux Blake Miguez Fred Mills 2017 2018 2019 Chairman Mike Huval Mike Huval Mike Huval Vice-Chair Jonathan Perry Jonathan Perry Vincent Pierre Secretary/Treasurer John Berthelot John Berthelot John Berthelot Executive Committee Major Thibaut Major Thibaut Dustin Miller Executive Committee Vincent Pierre Vincent Pierre Gerald Boudreaux Executive Committee Tanner Magee Tanner Magee Tanner Magee Executive Committee Nancy Landry Nancy -

Abbeville Meridional Wednesday, April 7, 2021 Voice of Vermilion Parish - “The Most Cajun Place on Earth” - Since 1856 • Vol

Abbeville Meridional www.vermiliontoday.com Wednesday, April 7, 2021 Voice of Vermilion Parish - “The Most Cajun Place on Earth” - since 1856 • Vol. 165, No. 68, .75 cents , 1 section, • 10 pages Fusilier sworn in as new Erath alderman He won’t have to wait long for his first meeting By Chris Rosa Managing Editor On the Vermilion Parish Courthouse’s steps, Clarence Fusilier was sworn in as the new alderman for the Erath City Council. What makes Fusilier’s swearing-in so special is because it was historic. He is Photo above: Clarence Fusilier now the first Erath black alderman. holds up his right hand and puts his His first meeting with the aldermen left hand on his own Bible for the and Mayor Taylor Mencacci is April 12. swearig in. Swearing him in is Ver- The swearing-in took place on the court- milion Parish Clerk of Court Diane house’s steps, with Vermilion Parish Clerk Meaux Broussard. The swearing in of Court Diane Meaux Broussard swearing took place on the steps of the Vermil- him in. ion Parish Courthouse in Abbeville. Also, there was Fusilier’s family, in- Holding the Bible is Kendra Fusili- cluding his brother Pastor Walter August. er, Fusilier’s daughter. Pastor Walter Fusilier won a special election last August, Clarence’s brother, also at- month. Fusilier beat opponent Chris He- tended. bert by only 11 votes. This was Fusilier’s second go-around with running for an alderman seat. He Photo on the left is Clarence Fusilier threw his name in the hat two years ago signing the official swearing in docu- and finished in sixth place when only five ments with Vermilion Parish Clerk could win. -

2011 Louisiana Legislative Election Update

2011 Louisiana Legislative Election Update General Election - November 19 October 24, 2011 Candidates In November 19TH Run Off Senate ! SD 2 !Elton Aubert and Troy Brown !SD 24 !Donald Cravins and Elbert Guillory !SD 30 !James David Cain and John Smith !SD 39 !Lydia Jackson and Gregory Tarver House ! HD 3 !! Lynn Cawthorne and Barbara Norton !HD 10 !Jerri Ray de Pingre’ and Gene Reynolds !HD 12 !Jason Bullock and Rob Shadoin !HD 14 !Sam Little and Jay Morris !HD 17 !Billye Burns and Marcus Hunter !HD 22 !Terry Brown and Billy Chandler !HD 23 !Kenny Cox and Rick Nowlin !HD 39 !Don Menard and Stephen Ortego !HD 44 !Rickey Hardy and Vince Pierre !HD 53 !Billy Hebert and Lenar Whitney !HD 56 !Greg Miller and Ram Ramachandran !HD 57 !Randal Gaines and Russ Wise !HD 58 !Dwayne Bailey and Ed Price !HD 61 !Denise Marcelle and Alfred Williams !HD 62 !Ken Dawson and Kenny Havard !HD 81 !Kevin Hull and Clay Schexnayder !HD 86 !Chris Broadwater and George Holton !HD 96 !Terry Landry and Eric Martin !HD 101 !Tiffany Foxworth and Ted James !HD 103 !Ray Garofalo and Chad Lauga !HD 105 !Rocky Asevedo and Chris Leopold Senate Election Results by District ✓ SD 1 Includes St. Bernard (47%), St. Tammany (38%), Plaquemines (14%) and • Orleans (1%) • Incumbent State Sen. A.G. Crowe, R-Slidell ✦ SD 2 (New) Includes Ascension (17%), Assumption (11%), Iberville (9%), Lafourche • (14%), St. Charles (1%), St. James (15%), St. John (19%) and West Baton Rouge (13%) • State Rep. Elton Aubert, D-Vacherie - 30.90% • Troy Brown, D-Geismar - 34.02% ✓ SD 3 • Includes Orleans (53%), Jefferson (28%), St.