Meat and Meat Products Market Summary

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Product List March 2019 - Page 1 of 53

Wessex has been sourcing and supplying active substances to medicine manufacturers since its incorporation in 1994. We supply from known, trusted partners working to full cGMP and with full regulatory support. Please contact us for details of the following products. Product CAS No. ( R)-2-Methyl-CBS-oxazaborolidine 112022-83-0 (-) (1R) Menthyl Chloroformate 14602-86-9 (+)-Sotalol Hydrochloride 959-24-0 (2R)-2-[(4-Ethyl-2, 3-dioxopiperazinyl) carbonylamino]-2-phenylacetic 63422-71-9 acid (2R)-2-[(4-Ethyl-2-3-dioxopiperazinyl) carbonylamino]-2-(4- 62893-24-7 hydroxyphenyl) acetic acid (r)-(+)-α-Lipoic Acid 1200-22-2 (S)-1-(2-Chloroacetyl) pyrrolidine-2-carbonitrile 207557-35-5 1,1'-Carbonyl diimidazole 530-62-1 1,3-Cyclohexanedione 504-02-9 1-[2-amino-1-(4-methoxyphenyl) ethyl] cyclohexanol acetate 839705-03-2 1-[2-Amino-1-(4-methoxyphenyl) ethyl] cyclohexanol Hydrochloride 130198-05-9 1-[Cyano-(4-methoxyphenyl) methyl] cyclohexanol 93413-76-4 1-Chloroethyl-4-nitrophenyl carbonate 101623-69-2 2-(2-Aminothiazol-4-yl) acetic acid Hydrochloride 66659-20-9 2-(4-Nitrophenyl)ethanamine Hydrochloride 29968-78-3 2,4 Dichlorobenzyl Alcohol (2,4 DCBA) 1777-82-8 2,6-Dichlorophenol 87-65-0 2.6 Diamino Pyridine 136-40-3 2-Aminoheptane Sulfate 6411-75-2 2-Ethylhexanoyl Chloride 760-67-8 2-Ethylhexyl Chloroformate 24468-13-1 2-Isopropyl-4-(N-methylaminomethyl) thiazole Hydrochloride 908591-25-3 4,4,4-Trifluoro-1-(4-methylphenyl)-1,3-butane dione 720-94-5 4,5,6,7-Tetrahydrothieno[3,2,c] pyridine Hydrochloride 28783-41-7 4-Chloro-N-methyl-piperidine 5570-77-4 -

NPPC GSP Oral Comments on the Kingdom of Thailand Maria Zieba

NPPC GSP Oral Comments on The Kingdom of Thailand Maria Zieba I appreciate the opportunity to represent the National Pork Producers Council at today’s hearing. NPPC is a national association representing 42 state producer organizations. It represents the federal policy and global interests of 60,000 U.S. pork producers. The United States is the top global exporter of pork, shipping nearly 2.5 million metric tons (MT), valued at over $6.4 billion to more than 100 nations in 2018. While Thailand consumes more than one million metric tons of pork annually, it imported no U.S. pork in 2018. That’s because Thailand effectively maintains a ban on U.S. pork. It defends its unwarranted ban on uncooked pork and other pork products by pointing to the use of ractopamine by some U.S. pork producers. Ractopamine hydrochloride (or ractopamine) is a feed ingredient approved for use in the United States for swine and beef cattle. In swine, it is used for increased weight gain, feed efficiency, and carcass leanness in finishing swine. Thailand maintains a ban on imports of pork produced with ractopamine, despite the approval by its own Ministry of Health for domestic use. After an extensive risk assessment, the U.S. Food and Drug Administration approved ractopamine for use in hogs in 1999, and no adverse human health problems have been reported since approval. In 2012, the Codex Alimentarius recognized the safety of ractopamine, establishing a recommended maximum residue level (MRL) for the product. At least 25 other countries have also approved the use of ractopamine in pork production, and an additional 75 countries permit imports of pork produced using ractopamine. -

Ractopamine and Clenbuterol Urinary Residues in Pigs As Food-Producing Animals

J. PLEADIN et al.: RTC and CLB Urinary Residues in Pigs, Food Technol. Biotechnol. 49 (4) 517–522 (2011) 517 ISSN 1330-9862 scientific note (FTB-2714) Ractopamine and Clenbuterol Urinary Residues in Pigs as Food-Producing Animals Jelka Pleadin1*, Ana Vuli}1, Nina Per{i1, Dinka Mili}2 and Nada Vah~i}3 1Laboratory for Analytical Chemistry, Croatian Veterinary Institute, Savska 143, HR-10000 Zagreb, Croatia 2Dubravica Swine Farm, Ltd., Pavla [toosa 109, HR-10293 Dubravica, Croatia 3Faculty of Food Technology and Biotechnology, University of Zagreb, Pierottijeva 6, HR-10000 Zagreb, Croatia Received: January 17, 2011 Accepted: April 21, 2011 Summary The aim of the study is to determine residual ractopamine (RCT) and clenbuterol (CLB) concentrations in urine during and after their administration in anabolic dose to male pigs. RCT and CLB residues were determined using previously validated enzyme-linked immunosorbent assay (ELISA) as a quantitative screening method. Hydrolysis of urine samples with b-glucuronidase showed significantly higher (p<0.05) RCT residues. Study results showed RCT and CLB urine concentrations to vary greatly during oral treatment for 28 days, with maximal RCT and CLB concentration recorded on day 25 ((327.4±161.0) ng/mL) and day 20 ((68.4±32.2) ng/mL), respectively. RCT concentration of (57.1±10.6) ng/mL and CLB concentration of (38.8±20.1) ng/mL were measured on day 0 of treatment withdrawal; on day 7 of treatment withdrawal, the measured concentration of RCT ((5.0±0.9) ng/mL) was 20-fold of CLB concentration ((0.3±0.2) ng/mL). -

2017 Anti-Doping Testing Figures Report

2017 Anti‐Doping Testing Figures Please click on the sub‐report title to access it directly. To print, please insert the pages indicated below. Executive Summary – pp. 2‐9 (7 pages) Laboratory Report – pp. 10‐36 (26 pages) Sport Report – pp. 37‐158 (121 pages) Testing Authority Report – pp. 159‐298 (139 pages) ABP Report‐Blood Analysis – pp. 299‐336 (37 pages) ____________________________________________________________________________________ 2017 Anti‐Doping Testing Figures Executive Summary ____________________________________________________________________________________ 2017 Anti-Doping Testing Figures Samples Analyzed and Reported by Accredited Laboratories in ADAMS EXECUTIVE SUMMARY This Executive Summary is intended to assist stakeholders in navigating the data outlined within the 2017 Anti -Doping Testing Figures Report (2017 Report) and to highlight overall trends. The 2017 Report summarizes the results of all the samples WADA-accredited laboratories analyzed and reported into WADA’s Anti-Doping Administration and Management System (ADAMS) in 2017. This is the third set of global testing results since the revised World Anti-Doping Code (Code) came into effect in January 2015. The 2017 Report – which includes this Executive Summary and sub-reports by Laboratory , Sport, Testing Authority (TA) and Athlete Biological Passport (ABP) Blood Analysis – includes in- and out-of-competition urine samples; blood and ABP blood data; and, the resulting Adverse Analytical Findings (AAFs) and Atypical Findings (ATFs). REPORT HIGHLIGHTS • A analyzed: 300,565 in 2016 to 322,050 in 2017. 7.1 % increase in the overall number of samples • A de crease in the number of AAFs: 1.60% in 2016 (4,822 AAFs from 300,565 samples) to 1.43% in 2017 (4,596 AAFs from 322,050 samples). -

Pork and Swine: Industry and Trade Summary

Pork and Swine Industry & Trade Summary Office of Industries Publication ITS-11 October 2014 Control No. 2014002 UNITED STATES INTERNATIONAL TRADE COMMISSION Robert B. Koopman Director, Office of Operations Karen Laney Director, Office of Industries This report was prepared principally by: John Giamalva, Office of Industries Livestock, Dairy, and Fishery Products [email protected] With supporting assistance from: Phyllis Boone, Office of Industries Peg Hausman and David Lundy, Office of Analysis and Research Services Carolyn Holmes and Darlene Smith, Statistical Support Division, Office of Investigations Sonya Wilson, Help Desk and Customer Service Division, Office of the Chief Information Officer Under the direction of: Jonathan Coleman, Chief Agriculture and Fisheries Division Address all communications to: Secretary to the Commission United States International Trade Commission Washington, DC 20436 www.usitc.gov Preface The United States International Trade Commission (USITC) initiated its current Industry and Trade Summary series of reports to provide information on the rapidly evolving trade and competitive situation of the thousands of products imported into and exported from the United States. International supply chains have become more global and competition has increased. Each Industry and Trade Summary addresses a different commodity/industry and contains information on trends in consumption, production, and trade, as well as an analysis of factors affecting industry trends and competitiveness in domestic and foreign markets. This report on swine and pork primarily covers the period 2008 through 2013. Papers in this series reflect ongoing research by USITC international trade analysts. The work does not represent the views of the USITC or any of its individual Commissioners. -

Drug and Medication Classification Schedule

KENTUCKY HORSE RACING COMMISSION UNIFORM DRUG, MEDICATION, AND SUBSTANCE CLASSIFICATION SCHEDULE KHRC 8-020-1 (11/2018) Class A drugs, medications, and substances are those (1) that have the highest potential to influence performance in the equine athlete, regardless of their approval by the United States Food and Drug Administration, or (2) that lack approval by the United States Food and Drug Administration but have pharmacologic effects similar to certain Class B drugs, medications, or substances that are approved by the United States Food and Drug Administration. Acecarbromal Bolasterone Cimaterol Divalproex Fluanisone Acetophenazine Boldione Citalopram Dixyrazine Fludiazepam Adinazolam Brimondine Cllibucaine Donepezil Flunitrazepam Alcuronium Bromazepam Clobazam Dopamine Fluopromazine Alfentanil Bromfenac Clocapramine Doxacurium Fluoresone Almotriptan Bromisovalum Clomethiazole Doxapram Fluoxetine Alphaprodine Bromocriptine Clomipramine Doxazosin Flupenthixol Alpidem Bromperidol Clonazepam Doxefazepam Flupirtine Alprazolam Brotizolam Clorazepate Doxepin Flurazepam Alprenolol Bufexamac Clormecaine Droperidol Fluspirilene Althesin Bupivacaine Clostebol Duloxetine Flutoprazepam Aminorex Buprenorphine Clothiapine Eletriptan Fluvoxamine Amisulpride Buspirone Clotiazepam Enalapril Formebolone Amitriptyline Bupropion Cloxazolam Enciprazine Fosinopril Amobarbital Butabartital Clozapine Endorphins Furzabol Amoxapine Butacaine Cobratoxin Enkephalins Galantamine Amperozide Butalbital Cocaine Ephedrine Gallamine Amphetamine Butanilicaine Codeine -

Clenbuterol: Effects and Usage in Livestock and Show Animals

Clenbuterol: Effects and Usage in Livestock and Show Animals Clenbuterol a beta-adrenergic agonist and the illegal use in food producing animals and show animals to improve lean muscle mass and market value. Tag Words: Clenbuterol, Growth Promoter, hormones, rbGH, factory farm, beta-adrenergic agonists, Contador, Doping, sports enhancement, livestock Authors: Aimee Wood, Tzeh Keong Foo, Mohd Ahmad with Julie M. Fagan, Ph.D. Summary (Aimee Wood) This classapedia is on the effects of clenbuterol on livestock such as cattle, poultry and swine. Clenbuterol is and illegal growth promoter illegally used in farms to fatten up animals before sending them to slaughter. In recent news Tour de France winner Alberto Contador has been tested positive for clenbuterol. Clenbuterol can also be used as a sport enhancement drug and is banned by the World Anti-Doping Agency. Our service project was to investigate the chance that the beef he had eaten the night before his urine was tested really poisoned Contador. It is unlawful and unethical for farmers to be using illegal substances on their animals that are harmful to the animals and humans alike. It is a huge injustice to Contador not to mention meat consumers if the meat he had ingested was tainted and he loses his titles and is banned from cycling. Video Link Class Project 2010 Fall: http://www.youtube.com/watch?v=ZTeJiBvbLhA The Issue: Clenbuterol Introduction (Aimee Wood) In today’s society “the bigger the better” seems to be the way of thinking about most things; houses, cups of coffee, bicep size and farm animals. -

(12) Patent Application Publication (10) Pub. No.: US 2007/0208029 A1 Barlow Et Al

US 20070208029A1 (19) United States (12) Patent Application Publication (10) Pub. No.: US 2007/0208029 A1 Barlow et al. (43) Pub. Date: Sep. 6, 2007 (54) MODULATION OF NEUROGENESIS BY PDE Related U.S. Application Data INHIBITION (60) Provisional application No. 60/729,366, filed on Oct. (75) Inventors: Carrolee Barlow, Del Mar, CA (US); 21, 2005. Provisional application No. 60/784,605, Todd A. Carter, San Diego, CA (US); filed on Mar. 21, 2006. Provisional application No. Kym I. Lorrain, San Diego, CA (US); 60/807,594, filed on Jul. 17, 2006. Jammieson C. Pires, San Diego, CA (US); Kai Treuner, San Diego, CA Publication Classification (US) (51) Int. Cl. A6II 3 L/506 (2006.01) Correspondence Address: A6II 3 L/40 (2006.01) TOWNSEND AND TOWNSEND AND CREW, A6II 3/4I (2006.01) LLP (52) U.S. Cl. .............. 514/252.15: 514/252.16; 514/381: TWO EMBARCADERO CENTER 514/649; 514/423: 514/424 EIGHTH FLOOR (57) ABSTRACT SAN FRANCISCO, CA 94111-3834 (US) The instant disclosure describes methods for treating dis eases and conditions of the central and peripheral nervous (73) Assignee: BrainCells, Inc., San Diego, CA (US) system by stimulating or increasing neurogenesis. The dis closure includes compositions and methods based on use of (21) Appl. No.: 11/551,667 a PDE agent, optionally in combination with one or more other neurogenic agents, to stimulate or activate the forma (22) Filed: Oct. 20, 2006 tion of new nerve cells. Patent Application Publication Sep. 6, 2007 Sheet 1 of 6 US 2007/0208029 A1 Figure 1: Human Neurogenesis Assay: budilast + Captopril Neuronal Differentiation budilast + Captopril ' ' ' 'Captopril " " " 'budilast 10 Captopril Concentration 10-8.5 10-8.0 10-7.5 10-7.0 10-6.5 10-6.0 10-5.5 10-5.0 10-4.5 10-40 ammammam 10-9.0 10-8.5 10-8-0 10-75 10-7.0 10-6.5 10-6.0 10-5.5 10-50 10-4.5 Conc (M) Ibudilast Concentration Patent Application Publication Sep. -

Marrakesh Agreement Establishing the World Trade Organization

No. 31874 Multilateral Marrakesh Agreement establishing the World Trade Organ ization (with final act, annexes and protocol). Concluded at Marrakesh on 15 April 1994 Authentic texts: English, French and Spanish. Registered by the Director-General of the World Trade Organization, acting on behalf of the Parties, on 1 June 1995. Multilat ral Accord de Marrakech instituant l©Organisation mondiale du commerce (avec acte final, annexes et protocole). Conclu Marrakech le 15 avril 1994 Textes authentiques : anglais, français et espagnol. Enregistré par le Directeur général de l'Organisation mondiale du com merce, agissant au nom des Parties, le 1er juin 1995. Vol. 1867, 1-31874 4_________United Nations — Treaty Series • Nations Unies — Recueil des Traités 1995 Table of contents Table des matières Indice [Volume 1867] FINAL ACT EMBODYING THE RESULTS OF THE URUGUAY ROUND OF MULTILATERAL TRADE NEGOTIATIONS ACTE FINAL REPRENANT LES RESULTATS DES NEGOCIATIONS COMMERCIALES MULTILATERALES DU CYCLE D©URUGUAY ACTA FINAL EN QUE SE INCORPOR N LOS RESULTADOS DE LA RONDA URUGUAY DE NEGOCIACIONES COMERCIALES MULTILATERALES SIGNATURES - SIGNATURES - FIRMAS MINISTERIAL DECISIONS, DECLARATIONS AND UNDERSTANDING DECISIONS, DECLARATIONS ET MEMORANDUM D©ACCORD MINISTERIELS DECISIONES, DECLARACIONES Y ENTEND MIENTO MINISTERIALES MARRAKESH AGREEMENT ESTABLISHING THE WORLD TRADE ORGANIZATION ACCORD DE MARRAKECH INSTITUANT L©ORGANISATION MONDIALE DU COMMERCE ACUERDO DE MARRAKECH POR EL QUE SE ESTABLECE LA ORGANIZACI N MUND1AL DEL COMERCIO ANNEX 1 ANNEXE 1 ANEXO 1 ANNEX -

The U.S.-EU Beef Hormone Dispute

The U.S.-EU Beef Hormone Dispute Renée Johnson Specialist in Agricultural Policy January 14, 2015 Congressional Research Service 7-5700 www.crs.gov R40449 The U.S.-EU Beef Hormone Dispute Summary The United States and the European Union (EU) have engaged in a long-standing and acrimonious trade dispute over the EU’s decision to ban hormone-treated meat. Despite an ongoing series of dispute settlement proceedings and decisions by the World Trade Organization (WTO), there is continued disagreement between the United States and the EU on a range of legal and procedural issues, as well as the scientific evidence and consensus concerning the safety of hormone-treated beef. To date, the EU continues to ban imports of hormone-treated meat and restricts most meat exports to the European Union to a limited quantity of beef imports that are certified as produced without the use of hormones. Starting in 1981, the EU adopted restrictions on livestock production limiting the use of natural hormones to therapeutic purposes, banning the use of synthetic hormones, and prohibiting imports of animals and meat from animals that have been administered the hormones. In 1989, the EU fully implemented its ban on imports of meat and meat products from animals treated with growth promotants. Initially the ban covered six growth promotants that are approved for use and administered in the United States. The EU amended its ban in 2003, permanently banning one hormone—estradiol-17β—while provisionally banning the use of the five other hormones. The United States has suspended trade concessions with the European Union by imposing higher import tariffs on EU products. -

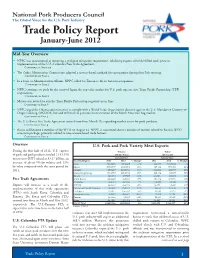

Trade Policy Report January-June 2012

National Pork Producers Council The Global Voice for the U.S. Pork Industry Trade Policy Report January-June 2012 Mid-Year Overview • NPPC was instrumental in removing a trichinae mitigation requirement, inhibiting exports of fresh/chilled pork, prior to implementation of the U.S.-Colombia Free Trade Agreement. Continued on This page • The Codex Alimentarius Commission adopted a science-based standard for ractopamine during their July meeting. Continued on Page 2 • In a letter to Administration officials, NPPC called for Taiwan to lift its ban on ractopamine. Continued on Page 2 • NPPC continues to push for the entry of Japan, the top value market for U.S. pork exports, into Trans-Pacific Partnership (TPP) negotiations. Continued on Page 2 • Mexico was invited to join the Trans-Pacific Partnership negotiations in June. Continued on Page 3 • NPPC urged the Obama administration to comply with a World Trade Organization decision against the U.S. Mandatory Country-of- Origin Labeling (MCOOL) law and will work to promote harmonization of the North American hog market. Continued on Page 3 • The U.S.-Korea Free Trade Agreement entered into force March 15, expanding market access for pork products. Continued on Page 4 • Russia will become a member of the WTO on August 22. NPPC is concerned about a number of matters related to Russia’s WTO accession package, primarily related to non-science-based trade barriers. Continued on Page 5 Overview U.S. Pork and Pork Variety Meat Exports During the first half of 2012, U.S. exports Volume Value of pork and pork products totaled 1,133,550 (Metric Tons) (US $1,000) metric tons (MT) valued at $3.17 billion, an January-June January-June Country/Region 2011 2012 % Change 2011 2012 % Change increase of about 5% by volume and 13% Japan 249,483.6 231,984.9 -7% 944,321 1,013,548 7% by value compared with the same period for Mexico 260,930.5 294,097.4 13% 485,141 537,473 11% 2011. -

4563 World Anti-Doping Agency (WADA) V

Tribunal Arbitral du Sport Court of Arbitration for Sport Arbitration CAS 2016/A/4563 World Anti-Doping Agency (WADA) v. Egyptian Anti-Doping Organisation (EGY-NADO) & Radwa Arafa Abd Elsalam, award of 16 January 2017 Panel: Mr Lars Halgreen (Denmark), Sole Arbitrator Karate Doping (ractopamine) Burden of proof Balance of probability Duty of the athlete to establish how the prohibited substance entered his/her body Intentional use Intentional violation 1. It is the athlete that bears the burden of proof of establishing that the violation was unintentional and thus to establish how the relevant forbidden substance entered into his/her body. 2. The burden of proof is based on the “balance of probability” standard, which entails that the athlete has the burden of convincing that the occurrence of the circumstances on which the athlete relies is more probable than their non-occurrence. 3. To establish the origin of a prohibited substance, it is not sufficient for an athlete merely to protest his or her innocence and suggest that the substance must have entered his or her body inadvertently from some supplement, medicine or other product, which the athlete was taken at the relevant time. Rather, an athlete must adduce concrete evidence to demonstrate that a particular supplement, medication or other product that the athlete took contained the substance in question. The mere presentation of invoices or bills as evidence for the purchase of contaminated foods cannot fulfil the athlete’s burden of proof that this food was indeed the source of the contamination. In cases of meat contamination, it must – as a minimum – be a requirement that the athlete sufficiently demonstrates where the meat originated from.