08Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2013 Annual Report

For personal use only 2013 Annual Report Cover image Lower Hatea River Crossing Project, New Zealand Project delivered by Transfield Services McConnell Dowell Joint Venture Architect — Knight Architects Bridge constructed by McConnell Dowell Constructors Limited Photograph by Patrick Reynolds All financials are in Australian dollars unless otherwise stated. The financial figures provided in the front section of the report (pages 6 to 47) have been rounded. In some cases, totals and percentages have been calculated from financial figures that have not been rounded; hence, some financials and percentages may not add up exactly. Notice of Annual General Meeting Shareholders are advised that the 2013 Annual General Meeting of Transfield Services will be held on Friday, 25 October 2013 at 10.00am (AEDT), at the AGL Theatre, Museum of Sydney, 37 Philip Street For personal use only (Corner Bridge Street), Sydney, New South Wales. Transfield Services Limited ABN 69 000 484 417 2 TRANSFIELD SERVICES 2013 “In just nine months, we have made major changes to the way Transfield Services is both structured and operated. Those changes have touched almost every aspect of our organisation.” Graeme Hunt Managing Director and Chief Executive Officer CONTENTS Business snapshot 4 Performance overview 6 Chairman’s report 8 MD and CEO’s report 12 Board of Directors 14 Senior executive team 16 Review of operations 19 Infrastructure, 20 Australia and New Zealand Resources and Energy, 22 Australia and New Zealand Americas 24 Middle East and Asia 25 Sustainable -

Transfield Services 2009 Annual Report

2009 ANNUAL REPORT { essential } Transfield Services Limited Annual Report 2009 i Contents 002 Who We Are and What We Do 004 Growth and Financial Highlights 006 Chairman’s Report Transfield Services exceeded on the guidance we gave to the market, with underlying Net Profit After Tax (pre- amortisation and impairment charge) increasing by 16.6 per cent to $123.6 million. 008 Managing Director and CEO’s Report Increased business efficiency in challenging market conditions has created a much stronger than usual second half result and an improved platform for growth. 012 Review of Operations 012 Australia Australian revenue, including our joint ventures, achieved growth of 2.1 per cent to $2.07 billion from Infrastructure Services and government stimulus package growth. 014 New Zealand New Zealand revenue, including joint ventures, increased by 4.7 per cent to $560.6 million due to a strong second half. 016 North America North American revenue grew by 48.9 per cent to $1.5 billion with the ongoing expansion of the FT Services joint venture and new contracts in transport infrastructure. 018 Emerging Markets Strong growth in shutdown and long-term maintenance contracts led to revenue increasing by 117 per cent to $179.7 million. 020 Transfield Services Infrastructure Fund (TSI Fund) Our investment delivered our shareholders a cash distribution of $15.6 million. 022 Our People and Our Achievements We reduced our Lost Time Injury Frequency Rate by 16.44 per cent, from 2.25 injuries per million hours worked the previous year to 1.88 this year. 026 Board of Directors 028 Senior Executive Team 030 Corporate Governance 037 Financial Report 141 Corporate Directory Two control room operators on our EastLink contract in Notice of Annual General Meeting Melbourne, Australia. -

Working on Tomorrow Today ANNUAL REPORT 2011 Challenge | Collaboration | Ingenuity | Integrity All Financials Are in Australian Dollars Unless Otherwise Specified

TRANSFIELD SERVICES ANNUAL REPORT Working on tomorrow today ANNUAL REPORT 2011 Challenge | Collaboration | Ingenuity | Integrity All financials are in Australian dollars unless otherwise specified. The financial figures provided in the front section of the report (pages 1 to 38) have been rounded. In some cases, totals and percentages have been calculated from financial figures that have not been rounded, hence some financials and percentages may not add up exactly. Notice of Annual General Meeting Shareholders are advised that the 2012 Annual General Meeting of Transfield Services will be held on Thursday, 1 November at 10.00am (AEDST), at the AGL Theatre, Museum of Sydney, 37 Philip Street (Corner Bridge Street), Sydney, New South Wales. CONTENTS 004 Business snapshot 006 Financial highlights 008 Chairman’s report 010 Managing Director and CEO’s report 014 Board of Directors 016 Senior executive team 018 Review of operations 020 Australia and New Zealand 024 Americas 026 Middle East and Asia 028 Sustainable business 034 Corporate governance 039 Financial report 140 Index 141 Corporate directory 142 Office locations 2012 TRANSFIELD SERVICES 3 BUSINESS SNAPSHOT MIDDLE EAST AND ASIA • Hydrocarbons • Manufacturing • Power Generation • Facilities Management * • Minerals Processing • Process Industries Our global workforce of 24,000+ • Chemicals • Power FAST FACT Hofincons supports the employees provides operations, generation of power for more than maintenance and construction 33 million people in India per year. services in the Resources, Energy, 6,734 Contract highlights • The region secured more than $37 million in new Industrial, Infrastructure, contracts and $20 million in renewed contracts. • Transfield Mannai Facilities Management Services now provides an end-to-end offering for the provision of heating, ventilation, Property and Defence sectors. -

Australian Solar Energy Generation Industry Capability Report

Australian Solar Energy Generation Industry Capability Report Prepared by the Clean Energy & Environment Team December 2010 Any person relying on this information does so entirely at their own discretion and Austrade strongly recommends the reader obtain independent professional advice prior to acting on this information. Any reference to companies or investment activities is for illustrative purposes only and does not constitute an endorsement of those companies or any investment activity. The Commonwealth does not accept any liability for loss arising from reliance on the contents of this work. To obtain information about the content of this report, please contact: Kerry Rooney National Industry Manager – Clean Energy The Australian Trade Commission (Austrade) Tel. +61 2 6201 8350 Email: [email protected] Web www.austrade.gov.au Australian Solar Industry Capability Report Table of Contents Overview .................................................................................................................... 1 Photovoltaic ............................................................................................................... 9 Solar Hot Water ....................................................................................................... 14 Solar Thermal .......................................................................................................... 15 Project Developers & Announcements .................................................................... 16 Other Solar Technology Announcements -

Inquiry Into Electoral and Political Party Funding

Submission No 83 INQUIRY INTO ELECTORAL AND POLITICAL PARTY FUNDING Organisation: Terrigal Area Residents Association “TARA” Inc Name: Ms Sue Edwards Position: President Telephone: 4385-6020 Date received: 13/02/2008 Terrigal Area Residents Association “TARA” Inc. 2007-08 Officers President: Sue Edwards Vice-President: Ted Sandeman Secretary: Mary Johnsson Treasurer: Ted Edwards P.O. Box 523, Terrigal 2260 Submission by email to: [email protected] 13 February 2008 The Legislative Council Select Committee on Electoral and Political Party Funding TARA welcomes the Legislative Council of NSW’s initiative on 27.06.07 in appointing a select committee to inquire into and report on the funding of, and disclosure of donations to, political parties, and candidates in state and local government elections. It is disappointing, however, that apart from the media release on 15.11.07 and a call for submissions on 19.11.07 little publicity has been given to this matter. The period 19.11.07 - 15.02.07 (closure of submissions) conveniently some might add, coincided with Federal Elections, Christmas and the January holidays. All media attention is currently on the return to Parliament of the new Federal Government and The Sorry Bill. One must ask the Question: Who could fund the advertising to raise awareness of the people of the Inquiry by this Select Committee into Electoral & Political Party Funding? The Liberal Party? The Labour Party? The Unions? The Development Industry? The Association of Hotels, The Gaming/Racing Industry? The Food Industry? The big Corporations? The answer of course is “NO” because all of the above are either major donors or major beneficiaries of electoral and political donations, and it would not be in their interest. -

For Personal Use Only Use Personal For

TRANSFIELD SERVICES ANNUAL REPORT For personal use only Working on tomorrow today ANNUAL REPORT 2011 Challenge | Collaboration | Ingenuity | Integrity All financials are in Australian dollars unless otherwise specified. For personal use only The financial figures provided in the front section of the report (pages 1 to 38) have been rounded. In some cases, totals and percentages have been calculated from financial figures that have not been rounded, hence some financials and percentages may not add up exactly. Notice of Annual General Meeting Shareholders are advised that the 2012 Annual General Meeting of Transfield Services will be held on Thursday, 1 November at 10.00am (AEDST), at the AGL Theatre, Museum of Sydney, 37 Philip Street (Corner Bridge Street), Sydney, New South Wales. CONTENTS 004 Business snapshot 006 Financial highlights 008 Chairman’s report 010 Managing Director and CEO’s report 014 Board of Directors 016 Senior executive team 018 Review of operations 020 Australia and New Zealand 024 Americas 026 Middle East and Asia 028 Sustainable business 034 Corporate governance 039 Financial report Index 140 For personal use only 141 Corporate directory 142 Office locations 2012 TRANSFIELD SERVICES 3 BUSINESS SNAPSHOT MIDDLE EAST AND ASIA • Hydrocarbons • Manufacturing • Power Generation • Facilities Management * • Minerals Processing • Process Industries Our global workforce of 24,000+ • Chemicals • Power FAST FACT Hofincons supports the employees provides operations, generation of power for more than maintenance and construction 33 million people in India per year. services in the Resources, Energy, 6,734 Contract highlights • The region secured more than $37 million in new Industrial, Infrastructure, contracts and $20 million in renewed contracts. -

[email protected] Website

30 June 2010 Research Director Environment and Resources Committee Parliament House Brisbane, QLD 4000 By email: [email protected] Website: www.parliament.qld.gov.au/erc Dear Sir/ Madam, Response to Environment and Resources Committee Inquiry into Growing QLD’s Renewable Energy Electricity Sector The Clean Energy Council (CEC) is the peak body representing Australia’s clean energy and energy efficiency industries. Its priorities are to: create the optimal conditions in Australia to stimulate investment in the development and deployment of world’s best clean energy technologies; develop effective legislation and regulation to improve energy efficiency; and work to reduce costs and remove all other barriers to accessing clean energy. The CEC works with members and the government to identify and address the barriers to efficient industry development in the stationary energy sector and energy efficiency. The clean energy industry and its members contribute to the generation of electricity using wind, hydro, solar, biomass, geothermal and ocean energy as well as the emerging technologies and service providers in the energy efficiency sector including solar hot water and cogeneration. The CEC welcomes this opportunity to provide a submission in response to the QLD Parliament Environment and Resources Committee’s Inquiry into Queensland’s Renewable Energy Electricity Sector. Policy Opportunities With its diverse clean energy industry, abundant energy resources and its commitment to reduce greenhouse gas emissions to mitigate the effects of climate change, Queensland is an ideal location to become a leader in the renewable energy industry. To transform to a low carbon economy will require the accelerated deployment of proven clean energy technologies such as wind, hydro, biomass, photovoltaic and cogeneration and the accelerated development of emerging technologies such as solar thermal, geothermal and wave/ocean power. -

JLR Corporate Client List

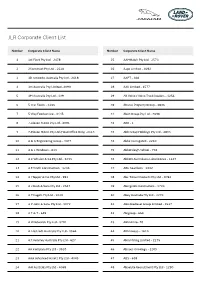

JLR Corporate Client List Number Corporate Client Name Number Corporate Client Name 1 1st Fleet Pty Ltd - 2478 25 AAMHatch Pty Ltd - 2573 2 2Construct Pty Ltd - 2620 26 Aapc Limited - 4092 3 3D networks Australia Pty Ltd - 2618 27 AAPT - 468 4 3m Australia Pty Limited -4090 28 AAV Limited - 1577 5 3M Australia Pty Ltd - 139 29 AB Volvo / Volvo Truck Dealers - 1256 6 5 Star Foods - 3166 30 Abacus Property Group - 3036 7 5 Way Foodservice - 3145 31 Abah Group Pty Ltd - 2698 8 7-eleven Stores Pty Ltd - 4091 32 ABB - 1 9 7-Eleven Stores Pty Ltd (Head Office Only) -2113 33 Abb Group Holdings Pty Ltd - 4093 10 A & G Engineering Group - 3473 34 Abbe Corrugated - 2210 11 A & L Windows - 613 35 Abbotsleigh School - 702 12 A C Whalan & Co Pty Ltd - 3233 36 Abbott Australasia Laboratories - 1247 13 A E Smith Construction - 1236 37 ABC Seamless - 1002 14 A I Topper & Co. Pty Ltd - 991 38 Abc Tissue Products Pty Ltd - 4094 15 A J Bush & Sons Pty Ltd - 2647 39 Abergeldie Contractors - 1724 16 A P Eagers Pty Ltd - 3020 40 Abey Australia Pty Ltd - 3270 17 A P John & Sons Pty Ltd - 1072 41 ABG Biodiesel Group Limited - 1537 18 A T & T - 649 42 Abigroup - 650 19 A W Edwards Pty Ltd - 3701 43 ABN Amro -70 20 A. Hartrodt Australia Pty Ltd - 3564 44 ABN Group - 1610 21 A.T. Kearney Australia Pty Ltd - 627 45 Abra Mining Limited - 2275 22 AA Company Pty Ltd - 3510 46 Abraxis Oncology - 2209 23 AAA Advanced Assets Pty Ltd - 4045 47 ABS - 638 24 AAI Australia Pty Ltd - 4068 48 Absolute Recruitment Pty Ltd - 1290 JLR Corporate Client List Number Corporate Client -

Australian Naval Shipbuilders

Chapter 4 Australian naval shipbuilders 4.1 The previous chapter traced the development of Australia's naval shipbuilding industry to the mid-1980s. This chapter concentrates on how Australia's prime contractors have developed their capacity over the past 20 years. It looks closely at the build of six Collins class submarines by the Australian Submarine Corporation (ASC) at Osborne, ten ANZAC frigates by Tenix at Williamstown and six Huon class minehunters by ADI at Newcastle. It notes the niche naval markets of two highly successful commercial aluminium shipbuilders in Austal and Incat. Finally, the chapter looks at the air warfare destroyer (AWD) and amphibious ship (LHD) projects, which are now in their early stages. 4.2 These past and current projects were referred to by a majority of witnesses to explain Australia's current capacity to construct large naval vessels. The projects will be mentioned throughout this report, particularly in connection with the role of small and medium sized enterprises (chapter 5), the pattern of infrastructure development (chapter 6), the productivity of the Australian naval shipbuilding industry (chapter 9) and the wider economic benefits from naval shipbuilding in Australia (chapter 11). The prime contractors 4.3 Australia's major naval shipbuilders face the challenges of their counterparts worldwide. Their survival depends on finding the most cost-effective way to produce modern warships with highly sophisticated and expensive systems. They must keep pace with the rapid advances in technology in the face of falling demand for ships, escalating costs associated with the increasing pressure for improved capability and the need to develop and retain highly skilled workers. -

Publish What You Pay Australia and the Uniting Church in Australia, Synod of Victoria and Tasmania

Committee Secretary Senate Economics Legislation Committee PO Box 6100 Parliament House Canberra, ACT, 2600 E-mail: [email protected] Publish What You Pay Australia and the Uniting Church in Australia, Synod of Victoria and Tasmania Submission to Inquiry into Foreign Bribery 24 August 2015 Publish What You Pay (PWYP) Australia and the Uniting Church in Australia Synod of Victoria and Tasmania welcome the opportunity to provide this joint submission to the Government’s inquiry into foreign bribery. PWYP Australia is a coalition of 30 humanitarian, faith, environmental, research and union organisations campaigning for greater transparency and accountability in the extractive industries that enjoy broad support across the Australian community. PWYP Australia works with the international PWYP network of over 800 civil society organisations to ensure that mining and oil and gas revenues are used for economic development and poverty reduction in resource-rich countries, including Australia. Foreign bribery falls on the continuum of corruption that plagues the extractives industry, particularly its activities within developing countries, and is inextricably tied to a countries economic and human development. The Australian Government has a responsibility to ensuring fair, equitable and sustainable practices are operating in the extractive sector, particularly as Australian extractive companies increase their presence in many of these developing nations. For example, in Africa, more than 150 Australian companies, holding about 1500 licenses, work across 33 African countries currently, an organisational presence higher than Canada, China or the United Kingdom.1 PWYP Australia endorses a strengthening of Australia’s legislation around foreign bribery, along with the introduction of mandatory disclosure legislation for extractives industries’ payments to foreign governments and Australia’s implementation of the Extractive Industries Transparency Initiative. -

Annual Report Annual

ANNUAL REPORT ANNUAL Transfield Services Limited 69 000 484 417 ANNUAL REPORT 2014 Cover image: Transfield Services’ Perth Naval Fire Fighters, WA All financials are in Australian dollars unless otherwise stated. The financial figures provided in the front section of the report (pages 4 to 27) have been rounded. In some cases, totals and percentages have been calculated from financial figures that have not been rounded; hence, some financials and percentages may not add up exactly. Notice of Annual General Meeting Shareholders are advised that the 2014 Annual General Meeting of Transfield Services Limited (the “Company”) will be held on Wednesday, 5 November 2014 at 1:30pm (AEDT), at the AGL Theatre, Museum of Sydney, 37 Phillip Street (Corner Bridge Street), Sydney, New South Wales. Transfield Services Limited ABN 69 000 484 417 2| Transfield Services Annual Report 2014 CONTENTS CONTENTS PAGE Our business 4 A year of progress 6 Chairman’s report 8 Managing Director and Chief Executive Officer’s report 10 Board of Directors 12 Senior executive team 14 Social responsibility 16 Corporate governance report 22 Directors’ report 29 Operating and financial review 33 Remuneration report 49 Auditor’s independence declaration 72 Financial report 73 Independent auditor’s report to the members 125 Shareholder information 127 Corporate directory 128 To view this report online, visit: www.transfieldservices.com/media/annual-report/2014 Register with Computershare to receive electronic copies of Transfield Services Annual Reports in the future. Transfield Services -

Recruitment Advertising with EA Network

Recruitment Advertising with EA Network Sydney & Melbourne ExecAssist.com.au For further information please contact Wendy Ward on (02) 9973 3848 An Introduction to the Executive Assistant Network EAN is the unique professional networking group for the most senior Executive and Personal Assistants working for leading executives in Australia’s top companies. EAN’s goal is to provide its members with high quality support services, education and website based tools and to facilitate them becoming more efficient and proficient in their roles. Founded in August 2005 with 140 handpicked members, many of whom worked with executives on the Business Council of Australia, we now have over 2,050 members throughout Australia, drawn from over 1,050 of the most prominent businesses in the country. Today our selection and acceptance criteria are still as stringent, ensuring that ALL our members are of the desired calibre – management level EAs and PAs each capable of influencing decisions at senior management or Board level. EAN Highlights Website Traffic to, and use of, our website, ExecAssist.com.au, continues to grow month on month: - over 10,200 unique visitors to the site in May 2009 - an average of over 69,000 page views on the site each month from March to May 2009 Networking Functions Since our launch, EAN has hosted over 30 exciting networking functions in Sydney and Melbourne attracting over 3,627 senior EAs to these events – an average of more than 110 EAs or PAs per event. Our EAN networking events have been held at venues as diverse as the Presidential Suite at the Intercontinental Hotel, Taronga Zoo, L’Aqua, Sydney Aquarium, The Bayside Lounge, Terrace at Home Nightclub, ExecuJet Base Lounge, Strike Bowling Bar, Crowne Plaza Coogee Beach, Greenwood Dental Surgery Melbourne, Capitol Theatre, Touch of Mandela Gallery, Sheraton on the Park, Lindt Chocolate Café, Peter Rowland Kitchens, Ivy Bar plus many more.