Nonlinear Optimization with GAMS /LGO

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

University of California, San Diego

UNIVERSITY OF CALIFORNIA, SAN DIEGO Computational Methods for Parameter Estimation in Nonlinear Models A dissertation submitted in partial satisfaction of the requirements for the degree Doctor of Philosophy in Physics with a Specialization in Computational Physics by Bryan Andrew Toth Committee in charge: Professor Henry D. I. Abarbanel, Chair Professor Philip Gill Professor Julius Kuti Professor Gabriel Silva Professor Frank Wuerthwein 2011 Copyright Bryan Andrew Toth, 2011 All rights reserved. The dissertation of Bryan Andrew Toth is approved, and it is acceptable in quality and form for publication on microfilm and electronically: Chair University of California, San Diego 2011 iii DEDICATION To my grandparents, August and Virginia Toth and Willem and Jane Keur, who helped put me on a lifelong path of learning. iv EPIGRAPH An Expert: One who knows more and more about less and less, until eventually he knows everything about nothing. |Source Unknown v TABLE OF CONTENTS Signature Page . iii Dedication . iv Epigraph . v Table of Contents . vi List of Figures . ix List of Tables . x Acknowledgements . xi Vita and Publications . xii Abstract of the Dissertation . xiii Chapter 1 Introduction . 1 1.1 Dynamical Systems . 1 1.1.1 Linear and Nonlinear Dynamics . 2 1.1.2 Chaos . 4 1.1.3 Synchronization . 6 1.2 Parameter Estimation . 8 1.2.1 Kalman Filters . 8 1.2.2 Variational Methods . 9 1.2.3 Parameter Estimation in Nonlinear Systems . 9 1.3 Dissertation Preview . 10 Chapter 2 Dynamical State and Parameter Estimation . 11 2.1 Introduction . 11 2.2 DSPE Overview . 11 2.3 Formulation . 12 2.3.1 Least Squares Minimization . -

How to Use Your Favorite MIP Solver: Modeling, Solving, Cannibalizing

How to use your favorite MIP Solver: modeling, solving, cannibalizing Andrea Lodi University of Bologna, Italy [email protected] January-February, 2012 @ Universit¨atWien A. Lodi, How to use your favorite MIP Solver Setting • We consider a general Mixed Integer Program in the form: T maxfc x : Ax ≤ b; x ≥ 0; xj 2 Z; 8j 2 Ig (1) where matrix A does not have a special structure. A. Lodi, How to use your favorite MIP Solver 1 Setting • We consider a general Mixed Integer Program in the form: T maxfc x : Ax ≤ b; x ≥ 0; xj 2 Z; 8j 2 Ig (1) where matrix A does not have a special structure. • Thus, the problem is solved through branch-and-bound and the bounds are computed by iteratively solving the LP relaxations through a general-purpose LP solver. A. Lodi, How to use your favorite MIP Solver 1 Setting • We consider a general Mixed Integer Program in the form: T maxfc x : Ax ≤ b; x ≥ 0; xj 2 Z; 8j 2 Ig (1) where matrix A does not have a special structure. • Thus, the problem is solved through branch-and-bound and the bounds are computed by iteratively solving the LP relaxations through a general-purpose LP solver. • The course basically covers the MIP but we will try to discuss when possible how crucial is the LP component (the engine), and how much the whole framework is built on top the capability of effectively solving LPs. • Roughly speaking, using the LP computation as a tool, MIP solvers integrate the branch-and-bound and the cutting plane algorithms through variations of the general branch-and-cut scheme [Padberg & Rinaldi 1987] developed in the context of the Traveling Salesman Problem (TSP). -

Numerical Methods for Large-Scale Nonlinear Optimization

Technical Report RAL-TR-2004-032 Numerical methods for large-scale nonlinear optimization N I M Gould D Orban Ph L Toint November 18, 2004 Council for the Central Laboratory of the Research Councils c Council for the Central Laboratory of the Research Councils Enquires about copyright, reproduction and requests for additional copies of this report should be addressed to: Library and Information Services CCLRC Rutherford Appleton Laboratory Chilton Didcot Oxfordshire OX11 0QX UK Tel: +44 (0)1235 445384 Fax: +44(0)1235 446403 Email: [email protected] CCLRC reports are available online at: http://www.clrc.ac.uk/Activity/ACTIVITY=Publications;SECTION=225; ISSN 1358-6254 Neither the Council nor the Laboratory accept any responsibility for loss or damage arising from the use of information contained in any of their reports or in any communication about their tests or investigations. RAL-TR-2004-032 Numerical methods for large-scale nonlinear optimization Nicholas I. M. Gould1;2;3, Dominique Orban4;5;6 and Philippe L. Toint7;8;9 Abstract Recent developments in numerical methods for solving large differentiable nonlinear optimization problems are reviewed. State-of-the-art algorithms for solving unconstrained, bound-constrained, linearly-constrained and nonlinearly-constrained problems are discussed. As well as important conceptual advances and theoretical aspects, emphasis is also placed on more practical issues, such as software availability. 1 Computational Science and Engineering Department, Rutherford Appleton Laboratory, Chilton, Oxfordshire, OX11 0QX, England, EU. Email: [email protected] 2 Current reports available from \http://www.numerical.rl.ac.uk/reports/reports.html". 3 This work was supported in part by the EPSRC grants GR/R46641 and GR/S42170. -

Derivative-Free Optimization: a Review of Algorithms and Comparison of Software Implementations

J Glob Optim (2013) 56:1247–1293 DOI 10.1007/s10898-012-9951-y Derivative-free optimization: a review of algorithms and comparison of software implementations Luis Miguel Rios · Nikolaos V. Sahinidis Received: 20 December 2011 / Accepted: 23 June 2012 / Published online: 12 July 2012 © Springer Science+Business Media, LLC. 2012 Abstract This paper addresses the solution of bound-constrained optimization problems using algorithms that require only the availability of objective function values but no deriv- ative information. We refer to these algorithms as derivative-free algorithms. Fueled by a growing number of applications in science and engineering, the development of derivative- free optimization algorithms has long been studied, and it has found renewed interest in recent time. Along with many derivative-free algorithms, many software implementations have also appeared. The paper presents a review of derivative-free algorithms, followed by a systematic comparison of 22 related implementations using a test set of 502 problems. The test bed includes convex and nonconvex problems, smooth as well as nonsmooth prob- lems. The algorithms were tested under the same conditions and ranked under several crite- ria, including their ability to find near-global solutions for nonconvex problems, improve a given starting point, and refine a near-optimal solution. A total of 112,448 problem instances were solved. We find that the ability of all these solvers to obtain good solutions dimin- ishes with increasing problem size. For the problems used in this study, TOMLAB/MULTI- MIN, TOMLAB/GLCCLUSTER, MCS and TOMLAB/LGO are better, on average, than other derivative-free solvers in terms of solution quality within 2,500 function evaluations. -

TOMLAB –Unique Features for Optimization in MATLAB

TOMLAB –Unique Features for Optimization in MATLAB Bad Honnef, Germany October 15, 2004 Kenneth Holmström Tomlab Optimization AB Västerås, Sweden [email protected] ´ Professor in Optimization Department of Mathematics and Physics Mälardalen University, Sweden http://tomlab.biz Outline of the talk • The TOMLAB Optimization Environment – Background and history – Technology available • Optimization in TOMLAB • Tests on customer supplied large-scale optimization examples • Customer cases, embedded solutions, consultant work • Business perspective • Box-bounded global non-convex optimization • Summary http://tomlab.biz Background • MATLAB – a high-level language for mathematical calculations, distributed by MathWorks Inc. • Matlab can be extended by Toolboxes that adds to the features in the software, e.g.: finance, statistics, control, and optimization • Why develop the TOMLAB Optimization Environment? – A uniform approach to optimization didn’t exist in MATLAB – Good optimization solvers were missing – Large-scale optimization was non-existent in MATLAB – Other toolboxes needed robust and fast optimization – Technical advantages from the MATLAB languages • Fast algorithm development and modeling of applied optimization problems • Many built in functions (ODE, linear algebra, …) • GUIdevelopmentfast • Interfaceable with C, Fortran, Java code http://tomlab.biz History of Tomlab • President and founder: Professor Kenneth Holmström • The company founded 1986, Development started 1989 • Two toolboxes NLPLIB och OPERA by 1995 • Integrated format for optimization 1996 • TOMLAB introduced, ISMP97 in Lausanne 1997 • TOMLAB v1.0 distributed for free until summer 1999 • TOMLAB v2.0 first commercial version fall 1999 • TOMLAB starting sales from web site March 2000 • TOMLAB v3.0 expanded with external solvers /SOL spring 2001 • Dash Optimization Ltd’s XpressMP added in TOMLAB fall 2001 • Tomlab Optimization Inc. -

Process Optimization

Process Optimization Mathematical Programming and Optimization of Multi-Plant Operations and Process Design Ralph W. Pike Director, Minerals Processing Research Institute Horton Professor of Chemical Engineering Louisiana State University Department of Chemical Engineering, Lamar University, April, 10, 2007 Process Optimization • Typical Industrial Problems • Mathematical Programming Software • Mathematical Basis for Optimization • Lagrange Multipliers and the Simplex Algorithm • Generalized Reduced Gradient Algorithm • On-Line Optimization • Mixed Integer Programming and the Branch and Bound Algorithm • Chemical Production Complex Optimization New Results • Using one computer language to write and run a program in another language • Cumulative probability distribution instead of an optimal point using Monte Carlo simulation for a multi-criteria, mixed integer nonlinear programming problem • Global optimization Design vs. Operations • Optimal Design −Uses flowsheet simulators and SQP – Heuristics for a design, a superstructure, an optimal design • Optimal Operations – On-line optimization – Plant optimal scheduling – Corporate supply chain optimization Plant Problem Size Contact Alkylation Ethylene 3,200 TPD 15,000 BPD 200 million lb/yr Units 14 76 ~200 Streams 35 110 ~4,000 Constraints Equality 761 1,579 ~400,000 Inequality 28 50 ~10,000 Variables Measured 43 125 ~300 Unmeasured 732 1,509 ~10,000 Parameters 11 64 ~100 Optimization Programming Languages • GAMS - General Algebraic Modeling System • LINDO - Widely used in business applications -

Click to Edit Master Title Style

Click to edit Master title style MINLP with Combined Interior Point and Active Set Methods Jose L. Mojica Adam D. Lewis John D. Hedengren Brigham Young University INFORM 2013, Minneapolis, MN Presentation Overview NLP Benchmarking Hock-Schittkowski Dynamic optimization Biological models Combining Interior Point and Active Set MINLP Benchmarking MacMINLP MINLP Model Predictive Control Chiller Thermal Energy Storage Unmanned Aerial Systems Future Developments Oct 9, 2013 APMonitor.com APOPT.com Brigham Young University Overview of Benchmark Testing NLP Benchmark Testing 1 1 2 3 3 min J (x, y,u) APOPT , BPOPT , IPOPT , SNOPT , MINOS x Problem characteristics: s.t. 0 f , x, y,u t Hock Schittkowski, Dynamic Opt, SBML 0 g(x, y,u) Nonlinear Programming (NLP) Differential Algebraic Equations (DAEs) 0 h(x, y,u) n m APMonitor Modeling Language x, y u MINLP Benchmark Testing min J (x, y,u, z) 1 1 2 APOPT , BPOPT , BONMIN x s.t. 0 f , x, y,u, z Problem characteristics: t MacMINLP, Industrial Test Set 0 g(x, y,u, z) Mixed Integer Nonlinear Programming (MINLP) 0 h(x, y,u, z) Mixed Integer Differential Algebraic Equations (MIDAEs) x, y n u m z m APMonitor & AMPL Modeling Language 1–APS, LLC 2–EPL, 3–SBS, Inc. Oct 9, 2013 APMonitor.com APOPT.com Brigham Young University NLP Benchmark – Summary (494) 100 90 80 APOPT+BPOPT APOPT 70 1.0 BPOPT 1.0 60 IPOPT 3.10 IPOPT 50 2.3 SNOPT Percentage (%) 6.1 40 Benchmark Results MINOS 494 Problems 5.5 30 20 10 0 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 Not worse than 2 times slower than -

Specifying “Logical” Conditions in AMPL Optimization Models

Specifying “Logical” Conditions in AMPL Optimization Models Robert Fourer AMPL Optimization www.ampl.com — 773-336-AMPL INFORMS Annual Meeting Phoenix, Arizona — 14-17 October 2012 Session SA15, Software Demonstrations Robert Fourer, Logical Conditions in AMPL INFORMS Annual Meeting — 14-17 Oct 2012 — Session SA15, Software Demonstrations 1 New and Forthcoming Developments in the AMPL Modeling Language and System Optimization modelers are often stymied by the complications of converting problem logic into algebraic constraints suitable for solvers. The AMPL modeling language thus allows various logical conditions to be described directly. Additionally a new interface to the ILOG CP solver handles logic in a natural way not requiring conventional transformations. Robert Fourer, Logical Conditions in AMPL INFORMS Annual Meeting — 14-17 Oct 2012 — Session SA15, Software Demonstrations 2 AMPL News Free AMPL book chapters AMPL for Courses Extended function library Extended support for “logical” conditions AMPL driver for CPLEX Opt Studio “Concert” C++ interface Support for ILOG CP constraint programming solver Support for “logical” constraints in CPLEX INFORMS Impact Prize to . Originators of AIMMS, AMPL, GAMS, LINDO, MPL Awards presented Sunday 8:30-9:45, Conv Ctr West 101 Doors close 8:45! Robert Fourer, Logical Conditions in AMPL INFORMS Annual Meeting — 14-17 Oct 2012 — Session SA15, Software Demonstrations 3 AMPL Book Chapters now free for download www.ampl.com/BOOK/download.html Bound copies remain available purchase from usual -

Theory and Experimentation

Acta Astronautica 122 (2016) 114–136 Contents lists available at ScienceDirect Acta Astronautica journal homepage: www.elsevier.com/locate/actaastro Suboptimal LQR-based spacecraft full motion control: Theory and experimentation Leone Guarnaccia b,1, Riccardo Bevilacqua a,n, Stefano P. Pastorelli b,2 a Department of Mechanical and Aerospace Engineering, University of Florida 308 MAE-A building, P.O. box 116250, Gainesville, FL 32611-6250, United States b Department of Mechanical and Aerospace Engineering, Politecnico di Torino, Corso Duca degli Abruzzi 24, Torino 10129, Italy article info abstract Article history: This work introduces a real time suboptimal control algorithm for six-degree-of-freedom Received 19 January 2015 spacecraft maneuvering based on a State-Dependent-Algebraic-Riccati-Equation (SDARE) Received in revised form approach and real-time linearization of the equations of motion. The control strategy is 18 November 2015 sub-optimal since the gains of the linear quadratic regulator (LQR) are re-computed at Accepted 18 January 2016 each sample time. The cost function of the proposed controller has been compared with Available online 2 February 2016 the one obtained via a general purpose optimal control software, showing, on average, an increase in control effort of approximately 15%, compensated by real-time implement- ability. Lastly, the paper presents experimental tests on a hardware-in-the-loop six- Keywords: Spacecraft degree-of-freedom spacecraft simulator, designed for testing new guidance, navigation, Optimal control and control algorithms for nano-satellites in a one-g laboratory environment. The tests Linear quadratic regulator show the real-time feasibility of the proposed approach. Six-degree-of-freedom & 2016 The Authors. -

Standard Price List

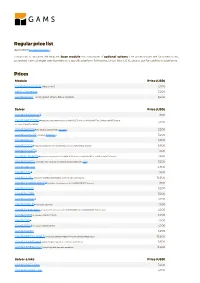

Regular price list April 2021 (Download PDF ) This price list includes the required base module and a number of optional solvers. The prices shown are for unrestricted, perpetual named single user licenses on a specific platform (Windows, Linux, Mac OS X), please ask for additional platforms. Prices Module Price (USD) GAMS/Base Module (required) 3,200 MIRO Connector 3,200 GAMS/Secure - encrypted Work Files Option 3,200 Solver Price (USD) GAMS/ALPHAECP 1 1,600 GAMS/ANTIGONE 1 (requires the presence of a GAMS/CPLEX and a GAMS/SNOPT or GAMS/CONOPT license, 3,200 includes GAMS/GLOMIQO) GAMS/BARON 1 (for details please follow this link ) 3,200 GAMS/CONOPT (includes CONOPT 4 ) 3,200 GAMS/CPLEX 9,600 GAMS/DECIS 1 (requires presence of a GAMS/CPLEX or a GAMS/MINOS license) 9,600 GAMS/DICOPT 1 1,600 GAMS/GLOMIQO 1 (requires presence of a GAMS/CPLEX and a GAMS/SNOPT or GAMS/CONOPT license) 1,600 GAMS/IPOPTH (includes HSL-routines, for details please follow this link ) 3,200 GAMS/KNITRO 4,800 GAMS/LGO 2 1,600 GAMS/LINDO (includes GAMS/LINDOGLOBAL with no size restrictions) 12,800 GAMS/LINDOGLOBAL 2 (requires the presence of a GAMS/CONOPT license) 1,600 GAMS/MINOS 3,200 GAMS/MOSEK 3,200 GAMS/MPSGE 1 3,200 GAMS/MSNLP 1 (includes LSGRG2) 1,600 GAMS/ODHeuristic (requires the presence of a GAMS/CPLEX or a GAMS/CPLEX-link license) 3,200 GAMS/PATH (includes GAMS/PATHNLP) 3,200 GAMS/SBB 1 1,600 GAMS/SCIP 1 (includes GAMS/SOPLEX) 3,200 GAMS/SNOPT 3,200 GAMS/XPRESS-MINLP (includes GAMS/XPRESS-MIP and GAMS/XPRESS-NLP) 12,800 GAMS/XPRESS-MIP (everything but general nonlinear equations) 9,600 GAMS/XPRESS-NLP (everything but discrete variables) 6,400 Solver-Links Price (USD) GAMS/CPLEX Link 3,200 GAMS/GUROBI Link 3,200 Solver-Links Price (USD) GAMS/MOSEK Link 1,600 GAMS/XPRESS Link 3,200 General information The GAMS Base Module includes the GAMS Language Compiler, GAMS-APIs, and many utilities . -

Research and Development of an Open Source System for Algebraic Modeling Languages

Vilnius University Institute of Data Science and Digital Technologies LITHUANIA INFORMATICS (N009) RESEARCH AND DEVELOPMENT OF AN OPEN SOURCE SYSTEM FOR ALGEBRAIC MODELING LANGUAGES Vaidas Juseviˇcius October 2020 Technical Report DMSTI-DS-N009-20-05 VU Institute of Data Science and Digital Technologies, Akademijos str. 4, Vilnius LT-08412, Lithuania www.mii.lt Abstract In this work, we perform an extensive theoretical and experimental analysis of the char- acteristics of five of the most prominent algebraic modeling languages (AMPL, AIMMS, GAMS, JuMP, Pyomo), and modeling systems supporting them. In our theoretical comparison, we evaluate how the features of the reviewed languages match with the requirements for modern AMLs, while in the experimental analysis we use a purpose-built test model li- brary to perform extensive benchmarks of the various AMLs. We then determine the best performing AMLs by comparing the time needed to create model instances for spe- cific type of optimization problems and analyze the impact that the presolve procedures performed by various AMLs have on the actual problem-solving times. Lastly, we pro- vide insights on which AMLs performed best and features that we deem important in the current landscape of mathematical optimization. Keywords: Algebraic modeling languages, Optimization, AMPL, GAMS, JuMP, Py- omo DMSTI-DS-N009-20-05 2 Contents 1 Introduction ................................................................................................. 4 2 Algebraic Modeling Languages ......................................................................... -

Notes 1: Introduction to Optimization Models

Notes 1: Introduction to Optimization Models IND E 599 September 29, 2010 IND E 599 Notes 1 Slide 1 Course Objectives I Survey of optimization models and formulations, with focus on modeling, not on algorithms I Include a variety of applications, such as, industrial, mechanical, civil and electrical engineering, financial optimization models, health care systems, environmental ecology, and forestry I Include many types of optimization models, such as, linear programming, integer programming, quadratic assignment problem, nonlinear convex problems and black-box models I Include many common formulations, such as, facility location, vehicle routing, job shop scheduling, flow shop scheduling, production scheduling (min make span, min max lateness), knapsack/multi-knapsack, traveling salesman, capacitated assignment problem, set covering/packing, network flow, shortest path, and max flow. IND E 599 Notes 1 Slide 2 Tentative Topics Each topic is an introduction to what could be a complete course: 1. basic linear models (LP) with sensitivity analysis 2. integer models (IP), such as the assignment problem, knapsack problem and the traveling salesman problem 3. mixed integer formulations 4. quadratic assignment problems 5. include uncertainty with chance-constraints, stochastic programming scenario-based formulations, and robust optimization 6. multi-objective formulations 7. nonlinear formulations, as often found in engineering design 8. brief introduction to constraint logic programming 9. brief introduction to dynamic programming IND E 599 Notes 1 Slide 3 Computer Software I Catalyst Tools (https://catalyst.uw.edu/) I AIMMS - optimization software (http://www.aimms.com/) Ming Fang - AIMMS software consultant IND E 599 Notes 1 Slide 4 What is Mathematical Programming? Mathematical programming refers to \programming" as a \planning" activity: as in I linear programming (LP) I integer programming (IP) I mixed integer linear programming (MILP) I non-linear programming (NLP) \Optimization" is becoming more common, e.g.