University of Connecticut for the Fiscal Years Ended June 30, 2010 and 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Selected Highlights of Women's History

Selected Highlights of Women’s History United States & Connecticut 1773 to 2015 The Permanent Commission on the Status of Women omen have made many contributions, large and Wsmall, to the history of our state and our nation. Although their accomplishments are too often left un- recorded, women deserve to take their rightful place in the annals of achievement in politics, science and inven- Our tion, medicine, the armed forces, the arts, athletics, and h philanthropy. 40t While this is by no means a complete history, this book attempts to remedy the obscurity to which too many Year women have been relegated. It presents highlights of Connecticut women’s achievements since 1773, and in- cludes entries from notable moments in women’s history nationally. With this edition, as the PCSW celebrates the 40th anniversary of its founding in 1973, we invite you to explore the many ways women have shaped, and continue to shape, our state. Edited and designed by Christine Palm, Communications Director This project was originally created under the direction of Barbara Potopowitz with assistance from Christa Allard. It was updated on the following dates by PCSW’s interns: January, 2003 by Melissa Griswold, Salem College February, 2004 by Nicole Graf, University of Connecticut February, 2005 by Sarah Hoyle, Trinity College November, 2005 by Elizabeth Silverio, St. Joseph’s College July, 2006 by Allison Bloom, Vassar College August, 2007 by Michelle Hodge, Smith College January, 2013 by Andrea Sanders, University of Connecticut Information contained in this book was culled from many sources, including (but not limited to): The Connecticut Women’s Hall of Fame, the U.S. -

Legislative History for Connecticut Act

Legislative History for Connecticut Act PA 16-93 SB333 Senate 934-951 18 Gov. Admin. & 1364, 1370-1378 10 Elections Higher 737-789, 800-850 104 Education & Employment House Transcripts have not been received. They are available 132 on CGA website, but are not the Official copy. Contact House Clerk for assistance (860) 240-0400 Transcripts from the Joint Standing Committee Public Hearing(s) and/or Senate and House of Representatives Proceedings Connecticut State Library Compiled 2017 S - 693 CONNECTICUT GENERAL ASSEMBLY SENATE PROCEEDINGS 2016 VOL. 59 PART 3 679 – 1032 000934 cf 256 SENATE April 20, 2016 0 On Page 8, Calendar 265, Senate Bill Number 333, AN ACT CONCERNING THE FOUNDATION OF CONSTITUENT UNITS AND PUBLIC INSTITUTIONS OF HIGHER EDUCATION. There are amendments. THE CHAIR: Senator Bartolomeo. SENATOR BARTOLOMEO (13TH) : Yes, hi Madam President. I move acceptance of the Joint Committee's joint favorable report and I urge passage of this bill, please. THE CHAIR: Motions on acceptance and passage. Will you remark? 0 SENATOR BARTOLOMEO (13TH) : Yes. Thank you, Madam President. This bill is is relevant to the UConn foundation and it does a variety of things, but first I would like to, if I might, have the clerk please call LCO Number 4488, which is an Amendment and that I be given leave to summarize, please. THE CHAIR: Mr. Clerk. THE CLERK: LCO Number 4488, Senate "A" offered by Senators ~rtolo~eo, Witkqs, and Looney. 0 000935 cf 257 SENATE April 20, 2016 c THE CHAIR: Senator Bartolomeo. SENATOR BARTOLOMEO (13TH) : Madam President, I move adoption of this amendment please. -

Combined Guide for Web.Pdf

2015-16 American Preseason Player of the Year Nic Moore, SMU 2015-16 Preseason Coaches Poll Preseason All-Conference First Team (First-place votes in parenthesis) Octavius Ellis, Sr., F, Cincinnati Daniel Hamilton, So., G/F, UConn 1. SMU (8) 98 *Markus Kennedy, R-Sr., F, SMU 2. UConn (2) 87 *Nic Moore, R-Sr., G, SMU 3. Cincinnati (1) 84 James Woodard, Sr., G, Tulsa 4. Tulsa 76 5. Memphis 59 Preseason All-Conference Second Team 6. Temple 54 7. Houston 48 Troy Caupain, Jr., G, Cincinnati Amida Brimah, Jr., C, UConn 8. East Carolina 31 Sterling Gibbs, GS, G, UConn 9. UCF 30 Shaq Goodwin, Sr., F, Memphis 10. USF 20 Shaquille Harrison, Sr., G, Tulsa 11. Tulane 11 [*] denotes unanimous selection Preseason Player of the Year: Nic Moore, SMU Preseason Rookie of the Year: Jalen Adams, UConn THE AMERICAN ATHLETIC CONFERENCE Table Of Contents American Athletic Conference ...............................................2-3 Commissioner Mike Aresco ....................................................4-5 Conference Staff .......................................................................6-9 15 Park Row West • Providence, Rhode Island 02903 Conference Headquarters ........................................................10 Switchboard - 401.244-3278 • Communications - 401.453.0660 www.TheAmerican.org American Digital Network ........................................................11 Officiating ....................................................................................12 American Athletic Conference Staff American Athletic Conference Notebook -

Daily Program Schedule

59 DAILY PROGRAM SCHEDULE THURSDAY, APRIL 27 – 8:30 – 12:00 pm POSTER SESSION 1 EXHIBIT HALL (Authors will be present from 8:30-10:15 am) Section 9 Posters WOMEN IN ELECTIVE OFFICE 1. “Policy Priorities in Three Midwestern States: Are There Gendered Political Interests?” Elizabeth A. Bennion, University of Wisconsin-Madison/Indiana University South Bend, [email protected] Disc: Angela High-Pippert, University of St. Thomas, [email protected] 2. “Caucuses and Influence: An Examination of the Maryland General Assembly’s Women’s Caucus and the Outcome of Legislation.” M. Mitchell Brown, University of Maryland College Park, [email protected] Disc: Georgia Duerst-Lahti, Beloit College, [email protected] 3. “The Changing Nature of Gender and Political Candidacy in U.S. House Elections, 1982-1998.” Rosalyn Cooperman, Vanderbilt University, [email protected] Disc: Lonna Rae Atkeson, University of New Mexico, [email protected] 4. “Assessing the Lasting Impacts of the Year of the Woman.” Jason M. Roberts, Purdue University, [email protected]; Lisa M. Dean, Purdue University Disc: Debra L. Dodson, Rutgers University, [email protected] 5. "Women as School Board Candidates.” Melissa M. Deckman, American University, [email protected] Disc: Angela High-Pippert, University of St. Thomas, [email protected] 6. “Gender, Mass Media and the Vote.” Steven Greene, Oberlin College, [email protected]; Laurel Elder, Hartwick College, [email protected] Disc: Lonna Rae Atkeson, University of New Mexico, [email protected] 7. “Media Coverage of Senate Candidates: Does a Gender Bias Still Exist?” Bethany Machacek, Union College, Zoe M. Oxley, Union College, [email protected] Disc: Debra L. -

Downloaded 4999 Are Primarily for Seniors

2 UNIVERSITY OF CONNECTICUT CONTENTS Academic Calendar ........................................................................................................................................................3 Board of Trustees and Officers of Administration .........................................................................................................4 Admissions .....................................................................................................................................................................5 Advisory System ............................................................................................................................................................8 Fees and Expenses .........................................................................................................................................................9 Assistantships, Fellowships, and Other Aid .................................................................................................................10 University Supports for Graduate Students .................................................................................................................13 Registration ..................................................................................................................................................................15 Standards and Degree Requirements ...........................................................................................................................17 Graduate Certificate -

25Th Anniversary Conference Speakers' Bios (Pdf)

SPEAKER AND HONOREE BIOS H. SAMY ALIM H. Samy Alim is the David O. Sears Endowed Chair in the Social Sciences and Professor of Anthropology and African American Studies at the University of California, Los Angeles, and the Founding Director of the Center for Race, Ethnicity, and Language (CREAL). Alim began his scholarly trajectory as a Penn undergraduate working closely with Dr. Harkavy and others at the Netter Center. He continues to work in schools and communities in the U.S. and South Africa to develop “culturally sustaining pedagogies,” which is the subject of his most recent book, Culturally Sustaining Pedagogies: Teaching and Learning for Justice in a Changing World (Teachers College Press, 2017, with Django Paris). Other recent books include Raciolinguistics: How Language Shapes Our Ideas about Race (Oxford, 2016, with John Rickford & Arnetha Ball) and Articulate While Black: Barack Obama, Language, and Race in the U.S. (Oxford, 2012, with Geneva Smitherman), which examines former President Barack Obama’s language use—and America's response to it. He has written extensively about Black Language and Hip Hop Culture in his books, Street Conscious Rap (1999), You Know My Steez (2004), Roc the Mic Right (2006), Tha Global Cipha (2006), Talkin Black Talk (2007), and Global Linguistic Flows (2009). DAWN ANDERSON-BUTCHER Dawn Anderson-Butcher is a Full Professor in the College of Social Work at The Ohio State University (OSU) and a Licensed Independent Social Worker-Supervisor (LISW-S). At OSU, Dawn is the Director of the Community and Youth Collaborative Institute (http://cayci.osu.edu/), the Executive Director of Teaching/Learning and Research for the university-wide LiFEsports Initiative (www.osulifesports.org),and holds a courtesy appointment in the College of Education and Human Ecology. -

Relationship at a Time

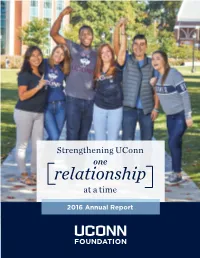

Strengthening UConn one relationship at a time 2016 Annual Report #UCONNNATION GIVES Fiscal 2016 (July 1, 2015 through June 30, 2016) Dollars Raised A total of 24,701 donors for Schools and Colleges gave $78.3M in 2016 Percentage increase from 2015 11% 15% 26% 86% 139% 170% Program Support $29.8M $10M $7.3M $3.8M $6.4M $4.4M $10.5M s y Scholarships and Fellowships $16.1M Faculty Support $5.3M School of Busines School of Medicine School of Pharmac Capital Improvement Projects $1.7M School of Engineering ollege of Liberal Arts and Sciences ollege of Liberal C RESEARCH SUPPORT $25.4M 164% increase C new55 endowed funds Resources Health and Natural ollege of Agriculture, created $9.6M 2015 2016 $55.5M Ways of Giving OUTRIGHT GIFTS TRANSFORM LIVES Cash and stock gifts for SCHOLARSHIP INITIATIVE immediate use 150 $14.4M $150M GOAL MULTIYEAR COMMITMENTS 100 Pledged gifts typically $78.3M paid over 5 years TOTAL $8.4M 50 PLEDGED ESTATE GIFTS $55.2M RAISED TO DATE Gifts pledged in a will, trust, charitable gift annuity, IRA, or other $16.1M RAISED IN 2016 estate plan 0 Fiscal 2016 (July 1, 2015 through June 30, 2016) Joshua R. Newton (left) and Daniel D. Toscano ’87 at the Husky Heritage Sports Museum [ engaged and [ energized [ It’s all about relationships Great relationships make a university. And a great university makes relationships. Lifelong bonds are built at UConn. Alumni are forever tied to the University that affected their lives in so many ways—introduced them to their best friend and the major that would, in most cases, become their life’s work. -

1718 WBB Media Guide for Web.Pdf

UConn gave The American its first NCAA title as the Huskies beat Kentucky to win the 2014 men’s basketball crown ... ... while the UConn women followed with a win against Notre Dame the next night to The American’s place on the national stage was set in the take the second of four straight NCAA titles. conference’s first year as Breshad Perriman and UCF topped Big 12 champion Baylor in the 2014 Fiesta Bowl. Temple’s Haason Reddick was the first of a league-record 15 players from The American taken in the 2017 NFL Draft. As of July 1, 2017, there were 118 players on NFL rosters who played in The American. Navy quarterback Keenan Reynolds finished fifth in the voting for the 2015 Heisman Trophy and shared the AAU Sullivan Award — given to the nation’s top amateur athlete — with UConn’s All-America basketball player Breanna Stewart. The American’s success has not been limited to the playing Houston made it two New Year’s Six wins in three years for The fields. Tulsa’s Kirk Smith highlighted an impressive collection American as the Cougars rolled past Florida State in the 2015 of academic achievements for the conference with his Chick-fil-A Peach Bowl. selection as a Rhodes Scholar in 2016. TABLETABLE OFOF CONTENTSCONTENTS CONTENTS About the American .....................................................................2-4 Commissioner Mike Aresco .....................................................5-6 Conference Staff ..........................................................................7-11 Conference Headquarters ..........................................................11 -

2017 Uconn Football Media Guide

2017 Football Media Supplement 2016 REVIEW 2016 TEAM STATISTICS 2017 UCONN FOOTBALL 2016 CONNECTICUT TEAM STATISTICS RECORD: OVERALL HOME AWAY NEUTRAL All Games 3-9 3-4 0-5 0-0 Conference 1-7 1-3 0-4 0-0 Non-Conference 2-2 2-1 0-1 0-0 DATE OPPONENT W/L SCORE ATTEND. Sept 1, 2016 MAINE W 24-21 29377 Sep 10, 2016 at Navy L 24-28 31501 Sep 17, 2016 VIRGINIA W 13-10 31036 Sep 24, 2016 SYRACUSE L 24-31 31899 Sept. 29, 2016 at #6 Houston L 13-42 40873 Oct 8, 2016 CINCINNATI W 20-9 24169 Oct 15, 2016 at USF L 27-42 30297 Oct 22, 2016 UCF L 16-24 28008 Oct 29, 2016 at East Carolina L 3-41 41370 Nov 4, 2016 TEMPLE L 0-21 22316 Nov 19, 2016 at Boston College L 0-30 36220 Nov 26, 2016 TULANE L 13-38 20764 TEAM STATISTICS ................................UCONN ...................OPP SCORING ..............................................178 .........................337 Points Per Game ................................14.8 .........................28.1 Points Off Turnovers ..........................35 ...........................48 FIRST DOWNS .....................................205 .........................251 Rushing ..............................................73 ............................89 Passing ..............................................117 ...........................149 Penalty ...............................................15 ............................13 RUSHING YARDAGE ...........................1408 ........................1753 Yards gained rushing .........................1729 ........................1971 Yards lost rushing ..............................321 -

University of Connecticut 2012 - 2013

1 UNIVERSITY OF CONNECTICUT University of Connecticut 2012 - 2013 GRADUATE CATALOG 2 UNIVERSITY OF CONNECTICUT CONTENTS Academic Calendar .......................................................................................................................................................................................3 Board of Trustees and Officers of Administration ..............................................................................................................................4 Admission ........................................................................................................................................................................................................5 Advisory System ............................................................................................................................................................................................7 Fees and Expenses ........................................................................................................................................................................................9 Assistantships, Fellowships, and Other Aid....................................................................................................................................... 13 University Programs and Services ........................................................................................................................................................ 24 Registration ................................................................................................................................................................................................. -

Protectingthe World Ofideas

Summer 2011 PROTECTINGTHE WORLD OF IDEAS Practice of intellectual property law explodes globally The anThropology of feasTing • Teaching in a war zone • social work issues Today Defeat Joint Pain! Whether you are 25 or 85, orthopaedic Learn more at nemsi.uchc.edu. experts at the Center for Joint Preservation Make an appointment by calling and Replacement, part of the New England 800-535-6232 Musculoskeletal Institute, offer a range of personalized Center for Joint Preservation options to help treat knee and hip pain including: and Replacement 263 Farmington Avenue, Farmington n Physical therapy 1132 West Street, Building 1, Southington n Medical management 2 Simsbury Road, Avon n State-of-the-art joint preservation procedures to Scan the code to see a patient diagnose and repair joint damage and relieve pain story on your phone n Partial knee replacement n Hip resurfacing n Total joint replacement to help patients Get the free mobile app at of all ages maintain an active lifestyle http://gettag.mobi There’s an option that’s right for you. contents UCONN Summer 2011 Volume 12, Number 2 24 Protecting the World of Ideas BY TODD ROSENTHAL The legal wrangling over who came up with the idea for Facebook is just one legal issue arising today in the burgeoning field of intellectual property law. 28 The Anthropology of Feasting BY NATALIE MUNRO Humans gathering together for a sumptuous feast can be traced to the Middle East, according to a UConn anthropologist who has discovered evidence of feasting dating back 10,000 years. Departments 30 Teaching in Wartime 2 FROM THE EDITOR BY ANGELA GRANT ’73 (CLAS), ’77 J.D. -

2018 BB Media Guide.Indd

2018 BASEBALL CONTACTS Ian MacDougall Mollie Radzinski Chris Jones [email protected] [email protected] [email protected] (407) 823-5395 (office) (513) 556-0667 (office) (860)-486-3531 (office) www.ucfknights.com www.gobearcats.com www.uconnhuskies.com Malcolm Gray Allison McClain Kevin Rodriguez [email protected] [email protected] [email protected] (252)737-4523 (office) (713) 743-9406 (901) 678-5108 (office) www.ecupirates.com www.uhcougars.com www.gotigersgo.com Patrick Puzzo Eric Hollier Tami Cutler [email protected] [email protected] [email protected] (813) 974-4087 (office) (504) 314-7271 (office) (316) 978-5559 (office) www.gousfbulls.com www.tulanegreenwave.com www.goshockers.com Greg Barlow [email protected] (401) 453-0660 (office) www.theamerican.org 2 2018 BASEBALL MEDIA GUIDE TABLE OF CONTENTS CONTENTS About the American ..........................................4-5 Commissioner Mike Aresco ...........................6-7 2018 Composite Schedule ...........................8-11 Preseason Awards ...............................................12 About Spectrum Field ........................................13 2018 NCAA Championship ..............................14 American Digital Network ..............................15 15 Park Row West Providence, R.I. 02903 (401) 244-3278 TEAMS UCF ........................................................................16-19 Cincinnati ..........................................................20-23 AMERICAN ATHLETIC CONFERENCE STAFF UConn .................................................................