Consultation Pakistan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report 2017 | 06 Notice of the Meeting

contents Company Information Company Information 06 Notice of the meeting 07 Corporate Governance Directors’ Profiles 11 Board of Directors 17 Chairman’s Message & Directors’ Report Chairman’s Message 21 Directors’ Report 23 Financial Review 31 Financial Summary 34 Financial Performance Indicators 2012-2017 35 Key Shareholding and Shares Traded 36 Pattern of Shareholding 38 Category of Shareholding 39 Shareholder Information 40 Our Brands Our Portfolio 43 Marketing Communication 47 Financial Statements Financials 55 Annexure 121 © 2017, Engro Foods All Rights Reserved. No part of this publication may be reproduced without the prior written permission of the publisher. company information company information Board of Directors Auditors Abdul Samad Dawood (Chairman) A. F. Ferguson & Company Ali Ahmed Khan (Chief Executive) Chartered Accountants Wim Torfs State Life Building No. 1- C Ghias Khan I.I. Chundrigar Road Heidi Van der Kooij Karachi - 74000, Pakistan. Jaska Marianne de Bakker Tel: +92(21) 32426682 -6 / 32426711-5 Johannes Petrus Fransiscus Laarakker Fax: +92(21) 32415007 / 32427938 Piet Johannes Hilarides Sabrina Dawood Share Registrar M/s. FAMCO Associates (Private) Limited Chief Financial Officer 8-F, Next to Hotel Faran, Block-6, PECHS, Imran Husain Shahrah-e-Faisal Karachi - Pakistan Tel: +92(21) 34380104-5, 34384621-3 Company Secretary Fax +92(21) 34380106 Muneeza Iftikar Registered Office Bankers 5th Floor, The Harbor Front Building HC-3, Marine Drive, Block - 4, Clifton Conventional Karachi - 75600, Pakistan. Allied Bank Limited Tel: +92(21) 35296000 (10 lines) Askari Bank Limited Fax: +92(21) 35295961-2 Bank Al-Falah Limited e-mail: [email protected] Bank Al-Habib Limited Website: www.engrofoods.com Citibank N.A. -

FACTSHEET - AS of 01-Oct-2021 Solactive GBS Pakistan Large & Mid Cap USD Index PR

FACTSHEET - AS OF 01-Oct-2021 Solactive GBS Pakistan Large & Mid Cap USD Index PR DESCRIPTION The Solactive GBS Pakistan Large & Mid Cap USD Index PR is part of the Solactive Global Benchmark Series which includes benchmark indices for developed and emerging market countries. The index intends to track the performance of the large and mid cap segment covering approximately the largest 85% of the free-float market capitalization in the Pakistani market. It is calculated as a pricereturn index in USD and weighted by free-float market capitalization. HISTORICAL PERFORMANCE 1,200 1,000 800 600 400 200 Jan-2008 Jan-2010 Jan-2012 Jan-2014 Jan-2016 Jan-2018 Jan-2020 Jan-2022 Solactive GBS Pakistan Large & Mid Cap USD Index PR CHARACTERISTICS ISIN / WKN DE000SLA8Y15 / SLA8Y1 Base Value / Base Date 1139 Points / 08.05.2006 Bloomberg / Reuters / .SPKLMCUP Last Price 347.48 Index Calculator Solactive AG Dividends Not included Index Type Price Return Calculation 8:00 am to 10:30 pm (CET), every 15 seconds Index Currency USD History Available daily back to 08.05.2006 Index Members 13 FACTSHEET - AS OF 01-Oct-2021 Solactive GBS Pakistan Large & Mid Cap USD Index PR STATISTICS 30D 90D 180D 360D YTD Since Inception Performance -11.24% -18.75% -20.18% -6.01% -14.20% -69.49% Performance (p.a.) - - - - - -7.42% Volatility (p.a.) 17.33% 14.90% 15.54% 17.78% 16.87% 23.20% High 391.47 429.41 459.90 459.90 459.90 1310.60 Low 343.18 343.18 343.18 343.18 343.18 250.61 Sharpe Ratio -4.42 -3.83 -2.37 -0.36 -1.11 -0.33 Max. -

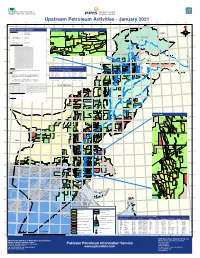

Upstream Petroleum Activities

Directorate General of Pakistan Petroleum Petroleum Concessions Information Service Upstream Petroleum Activities - January 2021 61.0.0 62.0.0 63.0.0 64.0.0 65.0.0 66.0.0 67.0.0 68.0.0 69.0.0 70.0.0 71.0.0 72.0.0 73.0.0 74.0.0 75.0.0 76.0.0 77.0.0 78.0.0 79.0.0 37.0.0 Inset North Average Production December ,2020 Oil 76,774.10 bbls /day BHAL SYEDAN 3371-10 Ʊ Ʋ Gas 3,582.33 mmcf/day OGDCL (KOHAT) Ʊ Ʋ LPG 2,263.61 m.tons/day OGDCL TOLANJ WEST SADKAL 36.0.0 MOL TOLANJ OGDCL Seismic Crews Active 07 MOL SOGHRI 3372-14 BDGBDU76GUDTU6I 2-D Seismic Acquisition Onshore 219.10 L.Kms. D&PL (FATEH JANG) 36.0.0 DHOK HUSSAIN 3-D Seismic Acquisition Onshore 91.75 Sq.Kms. OGDCL OGDCL 3371-17 OGDCL 4 (BARATAI) Gilgit Rigs Active 16 OGDCL Ʊ Ʋ 3370-3 DAKHNI Ʊ G I LG I T-BALTI STAN Area under Exploration Licences 206,736.00 Sq. Kms. (TAL) OGDCL Area under Mining/D&P Leases 14,010.00 Sq. Kms. MOL Area under Applications 114,396.00 Sq. Kms. MAMIKHEL 3371-5 RATANA (GURGALOT) OGDCL UCHRI OPI MAMIKHEL SOUTH DHURNAL BIDS OPENED FOR GRANT OF EL PARIWALI MOL POL OPI 3372-18 POL MAKORI&MAKORI DEEP 13 Bid round for following 20 blocks were held on January 15, 2021. MEYAL (IKHLAS) MOL MAKORI EAST 35.0.0 POL S.NO Block Name Zone POL MELA 3371-15 KHAUR 3372-23 OGDCL 1 Block No.3068-6 (Killa Saifullah) I (F) (DHOK SULTAN) POL (HISAL) 35.0.0 2 Block No.2762-2 (Desert) I (F) PPL PPL NASHPA DHULIAN 3 Block No.3067-7 (Sharan) I (F) OGDCL POL 4 Block No.3272-16 (Lilla) I CHANDA 5 Block No.3372-25 (Abbottabad) I OGDCL 6 Block No.3471-1 (Nowshera) I 3271-1 TOOT Ʊ Ʋ KALABAGH 10 (KARAK) OGDCL FC`7@SQ6FCUVIFCX6 7 Block No.3372-26 (Hazro) I MPCL MPCL HALINI 8 Block No.3273-5 (Jhelum) I MPCL 9 Block No.3372-27 (North Dhurnal) I Muzaffarabad 10 Block No.2668-23 (Khewari East) III 11 Block No. -

List of Acronyms

List of Acronyms A ADB Asian Development Bank APCMA All Pakistan Cement Manufacturers Association APEDA Agricultural and Processed Food Products Export Development Authority AIDP-I Auto Industry Development Program I ARPU Average Revenue Per User B BOP Balance of Payment BoDs Board of Directors BISP Benazir Income Support Program BISPP BQPS Bin Qasim Power Station BQPS BSCs Behbood Savings Certificates Bt Bacillus thuringiensis BTU British Thermal Units C CAA Civil Aviation Authority CAB Current Account Balance CAGR Compound Annual Growth Rate CBO Congressional Budget Office CBU Completely Built Unit CCAC Cotton Crop Assessment Committee CCI Council of Common Interest CCOR Cabinet Committee on Restructuring CCS Consumer Confidence Survey CDNS Central Directorate of National Savings CEO Chief Executive Officer CFT Cubic feet CGO Customs General Order CLCV Cotton Leaf Curl Virus CMI Census of Manufacturing Industries CNG Compressed Natural Gas CPI Consumer Price Index CPS Credit to Private Sector CPPA Central Power Purchase Agency CSF Coalition Support Fund, Cash Settled Futures CY Calendar Year D DAP Di-ammonium Phosphate DBC Dollar Bearer Certificate State Bank of Pakistan Annual Report 2013-14 DHCL Dawood Hercules Chemical Limited DISCOs Distribution Companies DRAP Drug Regulatory Authority of Pakistan DSCs Defense Saving Certificates DS Debt Servicing DPC Drug Pricing Committee DRAP Drug Regulatory Authority of Pakistan E EAD Economic Affairs Division EBA Everything but Arms ECB European Central Bank ED External Debt EDL External Debt -

Download Company Profile

www.accrescent.com.pk Marching towards SUCCESS Company Profile Accrescent Engineers was founded in the Accrescent Engineers provides technical year 1999, on the principles of integrity, solutions with quality services and traditional innovation and quality. Accrescent Engineers values, with a team of expertise, backed by is one of the fastest growing companies in years of experience. Pakistan, providing services in Electrical Designing, specializing in Power, Automation Accrescent Engineers enjoys a respectable & BMS. place at the top of the technology pyramid. Here at Accrescent we believe in taking Accrescent Engineers offers expertise in the time to listen to our clients, focusing electrical services, designing Industrial on team work, co-ordination and doing it Automation, Control Process, & Instrumentation. right the first time. Accrescent Engineers handles project ranging from one hour service calls to Our ultimate success lies not only in the complex, multi-phased design / build quality of our work but in our commitment projects. to the satisfaction of our customers. We are proud to say we are; Accrescent Engineers is a unique blend of experience, involved in installation, testing, commissioning, preventive maintenance, trouble shooting, projects designing, Marching Towards Success service of industrial plants, & Instrumentation, PLCs & SCADA (Supervisory control & data Acquisition ). Vision Statement Message from the It gives me an immense pleasure to The dedication of Accrescent's personnel To be a number one choice in the Industrial Electrical Products, and Power, Chief Executive introduce Accrescent Engineers as one of to client service is legendary. We believe Industrial, & Building Automation Products and Solutions, as well as being the the leading companies in the field of this zealous dedication separates us from recognized industry leader in Customer Care, quality and innovation. -

CFA Institute Research Challenge Hosted by CFA Society of Pakistan Institute of Business Administration – Karachi

CFA Institute Research Challenge hosted by CFA Society of Pakistan Institute of Business Administration – Karachi CFA Institute Research Challenge 2015-16 Institute of Business Administration (IBA) – Student Research This report is published for educational purposes only by [Oil & Gas Sector, Oil Marketing Company] Students competing in The CFA Institute Research Challenge. Pakistan Stock Exchange (PSX) Pakistan State Oil Date: 11/01/16 Current Price: 321.27 PKR/share Recommendation: BUY (33% upside) Ticker: PSO (PSX) Ticker: PSO PA (Bloomberg) PKR/USD: 105 Target Price: 428 PKR/share (4.08 USD) Market Profile Closing price (PKR) 321.27 PSO: Proxy for Pakistan’s economic revival 52-week price 283.75 - range (PKR) 415.40 We issue a BUY recommendation on Pakistan State Oil (PSO) with a one-year target price of PKR 428 using the Discounted Average daily Free Cash Flow to Firm (FCFF) and Relative Valuation Method. This offers a 33% upside from its closing price of PKR 321 volume (12M) 919,134 on January 11, 2016. PSO is one of the biggest and most liquid blue-chips on KSE with average daily volume being 0.34% As a % of shares of shares outstanding. Our investment thesis is based on PSO’s earnings growth, backed by volumes growth, outstanding 0.34% improving operating cash flows, and being a cheap blue-chip asset. PSO’s earnings growth is primarily driven by its volumetric sales growth during FY16-21 (CAGR: 12%) due to a changing energy mix, lower financing costs which will Dividend yield reduce over the years due to lower borrowings and positive operating cash flows. -

Annual Report 2016 3 OUR BUSINESSES

MAKING FOOD & ENERGY AVAILABLE, AFFORDABLE, SUSTAINABLE Dawood Hercules is a partner in Pakistan’s growth and prosperity, and this ethos serves as the foundation of our business operations. Energy, agriculture and food sectors are the strongest drivers of Pakistan’s economic growth, and are therefore the core areas of investment for our group. We are a holding company founded on family values. This allows us to deploy capital and invest in people and partnerships over a long period of time to solve two of the most pressing issues the world is facing today: making food and energy available, affordable and sustainable. CONTENTS 03 Vision 03 Purpose 08 Business ethics and core values 12 Performance highlights 16 Company information 20 Board of Directors 27 Committees 30 Operating Highlights 30 Six years at a glance 32 Horizontal analysis (Balance sheet) 34 Vertical analysis (Balance sheet) 36 Horizontal analysis (Profit & loss) 36 Vertical analysis (Profit & loss) 38 Statement of value addition 42 Notice of annual general meeting 60 Directors training programme 56 Directors’ Report 60 Related party transactions 56 Economic scenario 60 Future outlook 57 Business overview 61 Acknowledgment 58 Financial performance 66 Review report on statement of compliance 58 Earnings per share 67 Statement of compliance 58 Auditors 72 Financial Statements 58 Shares traded 73 Auditor’s report to the members 59 Pattern of shareholding 74 Financial statements 59 Market capitalization & book value 79 Notes to the financial statements 59 Appropriation 109 Consolidated -

A Solid Relief Rally; 5 May 2020 Breather Can Be Forgiven

Pakistan Equities Monthly Commentary A solid relief rally; 5 May 2020 breather can be forgiven . Interestingly, the local stock market and crude oil (WTI) both happened to Syed Hussain Haider, CFA, CIPM close the month at key resistance levels. Both have already gone through [email protected] a commendable relief rally; WTI has doubled and the KSE-100 has posted +9221 111-574-111 Ext: 3118 25% returns. Hence, any breather during May should not be concerning. Ali H. Zaidi [email protected] . Looking at the decent stock market performance in the ongoing holy +9221 111-574-111 Ext: 3103 month, it might just be the best one in a decade. However, empirical evidence suggests May has historically been relatively tamer. Perhaps this Ahmed Lakhani time, we could be in for something different? [email protected] +9221 111-574-111 Ext: 3035 . Presently, the market is basking in the glory of sympathetic measures (and potential budgetary relief around the corner) in lieu of Covid-19 – both local and foreign. Also, even with the back-to-back policy-rate cuts already announced by the central bank, a further cumulative 200bps cut (at least 100 bps in coming MPC meeting) should not be too surprising. With the market trading at forward P/E of 6.2x and a forward P/B of 1.03x (10-yr average of 8.2x and 1.6x) as per Bloomberg, there is no denying that valuations are more than attractive from a longer term perspective, even though the near-term earnings outlook remains hazy. -

Habibmetro Modaraba Management (AN(AN ISLAMICISLAMIC FINANCIALFINANCIAL INSTITUTION)INSTITUTION)

A N N U A L R E P O R T 2017 1 HabibMetro Modaraba Management (AN(AN ISLAMICISLAMIC FINANCIALFINANCIAL INSTITUTION)INSTITUTION) 2 A N N U A L R E P O R T 2017 JOURNEY OF CONTINUOUS SUCCESS A long term partnership Over the years, First Habib Modaraba (FHM) has become the sound, strong and leading Modaraba within the Modaraba sector. Our stable financial performance and market positions of our businesses have placed us well to deliver sustainable growth and continuous return to our investors since inception. During successful business operation of more than 3 decades, FHM had undergone with various up and down and successfully countered with several economic & business challenges. Ever- changing requirement of business, product innovation and development were effectively managed and delivered at entire satisfaction of all stakeholders with steady growth on sound footing. Consistency in perfect sharing of profits among the certificate holders along with increase in certificate holders' equity has made FHM a sound and well performing Modaraba within the sector. Our long term success is built on a firm foundation of commitment. FHM's financial strength, risk management protocols, governance framework and performance aspirations are directly attributable to a discipline that regularly brings prosperity to our partners and gives strength to our business model which is based on true partnership. Conquering with the challenges of our operating landscape, we have successfully journeyed steadily and progressively, delivering consistent results. With the blessing of Allah (SWT), we are today the leading Modaraba within the Modaraba sector of Pakistan, demonstrating our strength, financial soundness and commitment in every aspect of our business. -

OICCI CSR Report 2018-2019

COMBINING THE POWER OF SOCIAL RESPONSIBILITY Corporate Social Responsibility Report 2018-19 03 Foreword CONTENTS 05 OICCI Members’ CSR Impact 06 CSR Footprint – Members’ Participation In Focus Areas 07 CSR Footprint – Geographic Spread of CSR Activities 90 Snapshot of Participants’ CSR Activities 96 Social Sector Partners DISCLAIMER The report has been prepared by the Overseas Investors Chamber of Commerce and Industry (OICCI) based on data/information provided by participating companies. The OICCI is not liable for incorrect representation, if any, relating to a company or its activities. 02 | OICCI FOREWORD The landscape of CSR initiatives and activities is actively supported health and nutrition related initiatives We are pleased to present improving rapidly as the corporate sector in Pakistan has through donations to reputable hospitals, medical care been widely adopting the CSR and Sustainability camps and health awareness campaigns. Infrastructure OICCI members practices and making them permanent feature of the Development was also one of the growing areas of consolidated 2018-19 businesses. The social areas such as education, human interest for 65% of the members who assisted communi- capital development, healthcare, nutrition, environment ties in the vicinity of their respective major operating Corporate Social and infrastructure development are the main focus of the facilities. businesses to reach out to the underprivileged sections of Responsibility (CSR) the population. The readers will be pleased to note that 79% of our member companies also promoted the “OICCI Women” Report, highlighting the We, at OICCI, are privileged to have about 200 leading initiative towards increasing level of Women Empower- foreign investors among our membership who besides ment/Gender Equality. -

First Quarter Accounts 2021

first quarter accounts 2021 engro corp Engro’s investments in food & agri, petrochemicals, telecommunication infrastructure, and energy & related infrastructure are designed to enable nutrition, prosperity, connectivity, and progress for Pakistan. About Us gains and strived to attain professional excellence. Engro Polymer & Chemicals Limited owned subsidiary of ETPL, set up a state of the art LNG terminal, at Port Qasim. The terminal – which is also one of Engro Corporation Limited is one of Pakistan's largest In 1991, following a decision by Exxon to divest its fertilizer Engro Polymer & Chemicals Limited-a 56% owned the most cost efficient terminals in the region – has the conglomerates with the company's business portfolio spanning business on a global basis, the employees of Exxon Chemical subsidiary of Engro – is the only fully integrated chlor-vinyl capacity for regasification of up to 600 mmcfd. across sectors including chemical fertilizers, PVC resin, Pakistan Limited decided to buy out Exxon's share. This was, chemical complex in Pakistan and produces poly-vinyl chloride (PVC), caustic soda, sodium hypochlorite, Engro Vopak Terminal Limited telecommunication infrastructure, bulk liquid chemical terminal, and perhaps still is, the most successful employee buy-out in hydrochloric acid and other chlorine by-products. The foods and power generation. At Engro, our ambition is to become the corporate history of Pakistan. Renamed Engro Chemical business was setup as a state-of-the-art plant in 1997, as Engro Vopak is a joint venture with Royal Vopak of the the premier Pakistani enterprise with a global reach. Pakistan Limited, the company continued to go from strength a 50:50 joint venture, with Mitsubishi and Asahi Glass with Netherlands – the world’s largest bulk liquid chemical to strength, reflected in its consistent financial performance, Asahi subsequently divesting its shareholding in 2006. -

2005 Information

• Company Information 2 • Committees of BOD & Management 4 • Notice of Meeting 6 • Operating Highlights 8 • Directors' Report 12 Agriculture and Fertilizer Environment 14 Company Performance 16 Balancing, Modernization & Replacement 20 Profitability 22 Equity Participation & Shareholding 24 Good Governance & Listing Regulations 26 Safety, Health & Environment 36 Future Outlook & WTO Challenges 38 • Standard of Conduct for Directors / Employees 39 • Core Values 40 • Financial Statements of FFC 41 Statement of Compliance 42 Review Report to the Members 44 Auditors’ Report to the Members 45 Balance Sheet 46 Profit and Loss Account 48 Cash Flow Statement 49 Statement of Changes in Equity 50 Notes to the Financial Statements 51 • Consolidated Financial Statements 77 Auditors’ Report to the Members 79 Consolidated Balance Sheet 80 Consolidated Profit and Loss Account 82 Consolidated Cash Flow Statement 83 Consolidated Statement of Changes in Equity 84 Notes to the Consolidated Financial Statements 85 • Pattern of Shareholding 116 • Form of Proxy 119 Our achievements over the years in every business sphere have developed FFC into “The House of Excellence” 1 Company 2005 Information BOARD OF DIRECTORS REGISTERED OFFICE Lt Gen Syed Arif Hasan, HI(M) (Retired) 93-Harley Street, Rawalpindi Cantt. Chairman Website: www.ffc.com.pk Tel No. 92-51-9272307-14 Lt Gen Mahmud Ahmed, HI(M) (Retired) Fax No. 92-51-9272316 Chief Executive and Managing Director E-mail: [email protected] Dr Haldor Topsoe PLANTSITES Mr Qaiser Javed Goth Machhi Brig Arshad Shah, SI(M) (Retired) Sadikabad Mr Tariq Iqbal Khan (Distt: Rahim Yar Khan) Brig Aftab Ahmed, SI(M) (Retired) Tel No. 92-68-5786420-9 Brig Ghazanfar Ali, SI(M) (Retired) Fax No.