North Haledon Board of Education Comprehensive

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Passaic County Superintendent of Schools' Office

GENERAL INFORMATION PASSAIC COUNTY CODE: 31 SCHOOL DISTRICTS: 21 CHARTER SCHOOLS: 8 PRIVATE SCHOOLS FOR THE DISABLED 9 (NJDOE APPROVED): BLOOMINGDALE PREK-8 P.C. TECHNICAL INSTITUTE 9-12 CLIFTON PREK-12 PASSAIC VALLEY REGIONAL H.S. DISTRICT 9-12 CLASSICAL CS OF CLIFTON ** 6-8 PATERSON PREK-12 COLLEGE ACHIEVE CS OF PATERSON** K-8 (NO 4TH) PATERSON ARTS & SCIENCE CS ** K-9 COMMUNITY CS OF PATERSON** K-8 PATERSON CS FOR SCIENCE & TECH. ** K-12 HALEDON PREK-8 PHILIPS CS OF PATERSON ** K-3 HAWTHORNE K-12 POMPTON LAKES K-12 JOHN P. HOLLAND CS ** PREK-8 PROSPECT PARK PREK-8 LAKELAND 9-12 RINGWOOD K-8 LITTLE FALLS K-8 TOTOWA K-8 NORTH HALEDON K-8 WANAQUE K-8 NORTHERN REG. ED. SERVICES COMM. 9-12 WAYNE PREK-12 PASSAIC PREK-12 WEST MILFORD K-12 PASSAIC ARTS & SCIENCE CS ** K-12 WOODLAND PARK K-8 P.C. MANCHESTER REGIONAL H.S. 9-12 ** DENOTES CHARTER SCHOOLS - 2 - TABLE OF CONTENTS Page # RESPONSIBILITIES – EXECUTIVE COUNTY SUPT. OF SCHOOLS’ OFFICE……………………………………..………………………………… 4 PASSAIC COUNTY OFFICE/OFFICE OF COMPREHENSIVE SUPPORT….…………………………………………………………………………. 5 N.J. DEPARTMENT OF EDUCATION AND STATE BOARD OF EDUCATION………………………………………………......................... 6 PASSAIC COUNTY BOARD OF CHOSEN FREEHOLDERS…………………………………………………………….……….......................... 7 NORTH JERSEY FEDERAL CREDIT UNION…………………………………………………………………………….……………………………….. 7 PASSAIC COUNTY CAMP HOPE COMMISSION………………………………………………………………………………………………………. 7 WORKFORCE DEVELOPMENT BOARD OF PASSAIC COUNTY………….……………………………................................................ 7 COUNTY INSTITUTIONS OF HIGHER EDUCATION (BERKELEY, PCCC, WPU)……………………………….................................... 8 PASSAIC COUNTY LEGISLATORS……………………………………………………………............................................................... 9 THE EDUCATIONAL COUNCIL OF PASSAIC COUNTY………………………………………………………….…………………………………….. 10 PASSAIC COUNTY ASSOCIATIONS………………………………………………………………………...…………………………………………. 11 P.C. Association of School Administrators P.C. Education Association P.C. Association of School Business Officials P.C. -

Passaic County Superintendent of Schools' Office

EXECUTIVE COUNTY SUPERINTENDENT OF SCHOOLS GENERAL INFORMATION COUNTY CODE: 31 ADDRESS: 501 River Street Paterson, New Jersey 07524 TELEPHONE #: (973) 569-2110 FACSIMILE #: (973) 754-0241 OFFICE HOURS: Monday – Friday 8:00 a.m. - 4:00 p.m. DISTRICTS: 21 CHARTER SCHOOLS: 8 ELEMENTARY SCHOOLS: 69 40 ELEMENTARY/MIDDLE SCHOOLS: 14 MIDDLE SCHOOLS: MIDDLE/HIGH SCHOOLS: 4 HIGH SCHOOLS: 25 ADULT HIGH SCHOOLS: 2 - 2 - TABLE OF CONTENTS Page # RESPONSIBILITIES – EXECUTIVE COUNTY SUPT. OF SCHOOLS’ OFFICE……………………………………..………………………………… 4 PASSAIC COUNTY OFFICE/REGIONAL ACHIEVEMENT CENTER (RAC)…………………………………………………………………………. 5 N.J. DEPARTMENT OF EDUCATION AND STATE BOARD OF EDUCATION………………………………………………......................... 6 PASSAIC COUNTY BOARD OF CHOSEN FREEHOLDERS…………………………………………………………….……….......................... 7 NORTH JERSEY FEDERAL CREDIT UNION…………………………………………………………………………….……………………………….. 7 PASSAIC COUNTY CAMP HOPE COMMISSION………………………………………………………………………………………………………. 7 WORKFORCE DEVELOPMENT BOARD OF PASSAIC COUNTY………….……………………………................................................ 7 COUNTY INSTITUTIONS OF HIGHER EDUCATION (BERKELEY, PCCC, WPU)……………………………….................................... 8 PASSAIC COUNTY LEGISLATORS……………………………………………………………............................................................... 9 THE EDUCATIONAL COUNCIL OF PASSAIC COUNTY………………………………………………………….…………………………………….. 10 PASSAIC COUNTY ASSOCIATIONS………………………………………………………………………...…………………………………………. 11 P.C. Association of School Administrators P.C. Education Association P.C. Association -

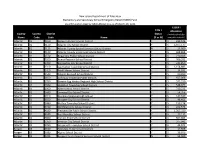

ESSER I Allocation Atlantic 01 0010 Absecon Public Schools Di

New Jersey Department of Education Elementary and Secondary School Emergency Relief (ESSER) Fund Local Education Agency (LEA) Allocations as of March 29, 2021 ESSER I Title I Allocation County County District Status (includes funds for Name Code Code Name (Y or N) nonpublic schools) Atlantic 01 0010 Absecon Public Schools District Y $ 232,945 Atlantic 01 0110 Atlantic City School District Y $ 3,977,177 Atlantic 01 0125 Atlantic County Special Services School District N $ 15,000 Atlantic 01 0120 Atlantic County Vocational School District Y $ 468,868 Atlantic 01 0570 Brigantine Public School District Y $ 210,406 Atlantic 01 0590 Buena Regional School District Y $ 766,392 Atlantic 01 1300 Egg Harbor City School District Y $ 243,850 Atlantic 01 1310 Egg Harbor Township School District Y $ 1,154,885 Atlantic 01 1410 Estell Manor School District Y $ 34,931 Atlantic 01 1540 Folsom Borough School District Y $ 60,490 Atlantic 01 1690 Galloway Township Public Schools Y $ 657,068 Atlantic 01 1790 Greater Egg Harbor Regional High School District Y $ 575,150 Atlantic 01 1940 Hamilton Township School District Y $ 548,921 Atlantic 01 1960 Hammonton School District Y $ 710,222 Atlantic 01 2680 Linwood City School District Y $ 54,356 Atlantic 01 2910 Mainland Regional High School Y $ 147,940 Atlantic 01 3020 Margate City School District Y $ 48,451 Atlantic 01 3480 Mullica Township School District Y $ 159,718 Atlantic 01 3720 Northfield City School District Y $ 222,573 Atlantic 01 4180 Pleasantville Public School District Y $ 1,267,320 Atlantic 01 4240 -

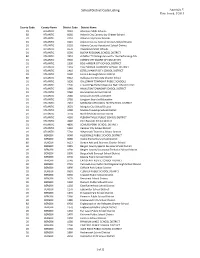

Appendix V Date Issued: 5/2015

School District Code Listing Appendix V Date Issued: 5/2015 County Code County Name District Code District Name 01 ATLANTIC 0010 Absecon Public Schools 80 ATLANTIC 6060 Atlantic City Community Charter School 01 ATLANTIC 0110 Atlantic City Public Schools 01 ATLANTIC 0125 Atlantic County Special Services School District 01 ATLANTIC 0120 Atlantic County Vocational School District 01 ATLANTIC 0570 Brigantine Public Schools 01 ATLANTIC 0590 BUENA REGIONAL SCHOOL DISTRICT 80 ATLANTIC 7410 chARTer~TECH High School for the Performing Arts 01 ATLANTIC 0960 CORBIN CITY BOARD OF EDUCATION 01 ATLANTIC 1300 EGG HARBOR CITY SCHOOL DISTRICT 01 ATLANTIC 1310 EGG HARBOR TOWNSHIP SCHOOL DISTRICT 01 ATLANTIC 1410 ESTELL MANOR CITY SCHOOL DISTRICT 01 ATLANTIC 1540 Folsom Borough School District 80 ATLANTIC 6612 Galloway Community Charter School 01 ATLANTIC 1690 GALLOWAY TOWNSHIP PUBLIC SCHOOLS 01 ATLANTIC 1790 Greater Egg Harbor Regional High School District 01 ATLANTIC 1940 HAMILTON TOWNSHIP SCHOOL DISTRICT 01 ATLANTIC 1960 Hammonton School District 01 ATLANTIC 2680 Linwood City School District 01 ATLANTIC 2780 Longport Board of Education 01 ATLANTIC 2910 MAINLAND REGIONAL HIGH SCHOOL DISTRICT 01 ATLANTIC 3020 Margate City School District 01 ATLANTIC 3480 Mullica Township School District 01 ATLANTIC 3720 Northfield City School District 01 ATLANTIC 4180 PLEASANTVILLE PUBLIC SCHOOL DISTRICT 01 ATLANTIC 4240 Port Republic School District 01 ATLANTIC 4800 SOMERS POINT SCHOOL DISTRICT 01 ATLANTIC 5350 Ventnor City School District 01 ATLANTIC 5760 Weymouth Township